Abstract

Background:

Little is documented regarding objective financial metrics and their impact on subjective financial toxicity in head and neck cancer (HNC) survivors.

Methods:

In a cross-sectional analysis, 71 survivors with available claims data for HNC-specific out-of-pocket expenses (OOPE) completed a survey including patient-reported, subjective financial toxicity outcome tools: the Comprehensive Score for financial Toxicity (COST) and the Financial Distress Questionnaire (FDQ).

Results:

Worse COST scores were significantly associated with lower earnings at survey administration (coefficient = 3.79; 95% CI 2.63–4.95; p < 0.001); loss of earnings after diagnosis (coefficient = 6.03; 95% CI 0.53–11.52; p = 0.032); and greater annual OOPE as a proportion of earnings [log10(Annual OOPE: Earnings at survey): coefficient = −5.66; 95% CI −10.28 to −1.04; p = 0.017]. Similar results were found with FDQ.

Conclusion:

Financial toxicity is associated with particular socioeconomic characteristics which, if understood, would assist the development of pre-treatment screening tools to detect at-risk individuals and intervene early in the HNC cancer survivorship trajectory.

Keywords: financial toxicity, head and neck cancer, health expenditures, health services, multidisciplinary research, out-of-pocket expenses, patient-reported outcomes, survivorship, treatment costs

1 |. INTRODUCTION

Cancer care is a major source of economic burden for patients and the health care system. Each year the United States spends 20.1 billion USD on the care of nonelderly cancer survivors, 1.3 billion of which comes directly out of their pockets.1 Survivors have higher OOPE than those with other chronic illnesses,2 with reports as high as 27% of earnings in low-income households.3 Cancer represents one of the highest-cost diagnoses among individuals who file for medical bankruptcy.4 The combination of high medical out-of-pocket expenses (OOPE) and reduced income associated with cancer treatment and/or recovery contributes to the financial toxicity experienced by patients with cancer and their families.5 This financial toxicity can be defined as the objective and subjective patient-level impact of the costs of cancer care and is linked to poorer health-related quality of life, decreased treatment adherence, greater symptom burden, and increased mortality risk.6–8

This is particularly relevant for head and neck cancer (HNC), which is costly to treat9 and creates long-term health needs.10 HNC survivors have higher medical expenses and out-of-pocket costs compared to non-HNC oncological patients.11 These elevated expenses persist beyond the immediate treatment period,11 as patients with HNC are at risk for a number of long-term treatment-related functional deficits such as lymphedema, fibrosis, dysphagia, ototoxicity, trismus, neck and shoulder dysfunction, and xerostomia.12 As a result, survivors are at risk for loss of vital functions and compromised ability to return to work,13 potentially exacerbating financial toxicity by decreasing available income. Following treatment, up to 48% of HNC survivors reduce their workload, among whom 33% leave the workforce entirely.13

Though numerous studies have investigated aspects of financial toxicity, there is variability in study methods and heterogeneity among cancer cohorts examined.2,5 Little has been quantitatively documented regarding the financial burden of HNC care and how it impacts subjective financial toxicity, particularly within the survivorship stage of care. The nature of the disease and the effects treatment-related complications have on necessary functions such as speech, swallow, and breathing imply potentially persistent HNC-related OOPE and subsequently worse financial toxicity long after cure is achieved. We hypothesized that patients with greater HNC-related OOPE relative to income, characterized as objective financial burden, experience worse associated subjective financial toxicity. The present study aims to examine objective financial metrics in post-treatment HNC survivors, and the relationships between these factors and financial toxicity.

2 |. MATERIALS AND METHODS

2.1 |. Design, setting, and participants

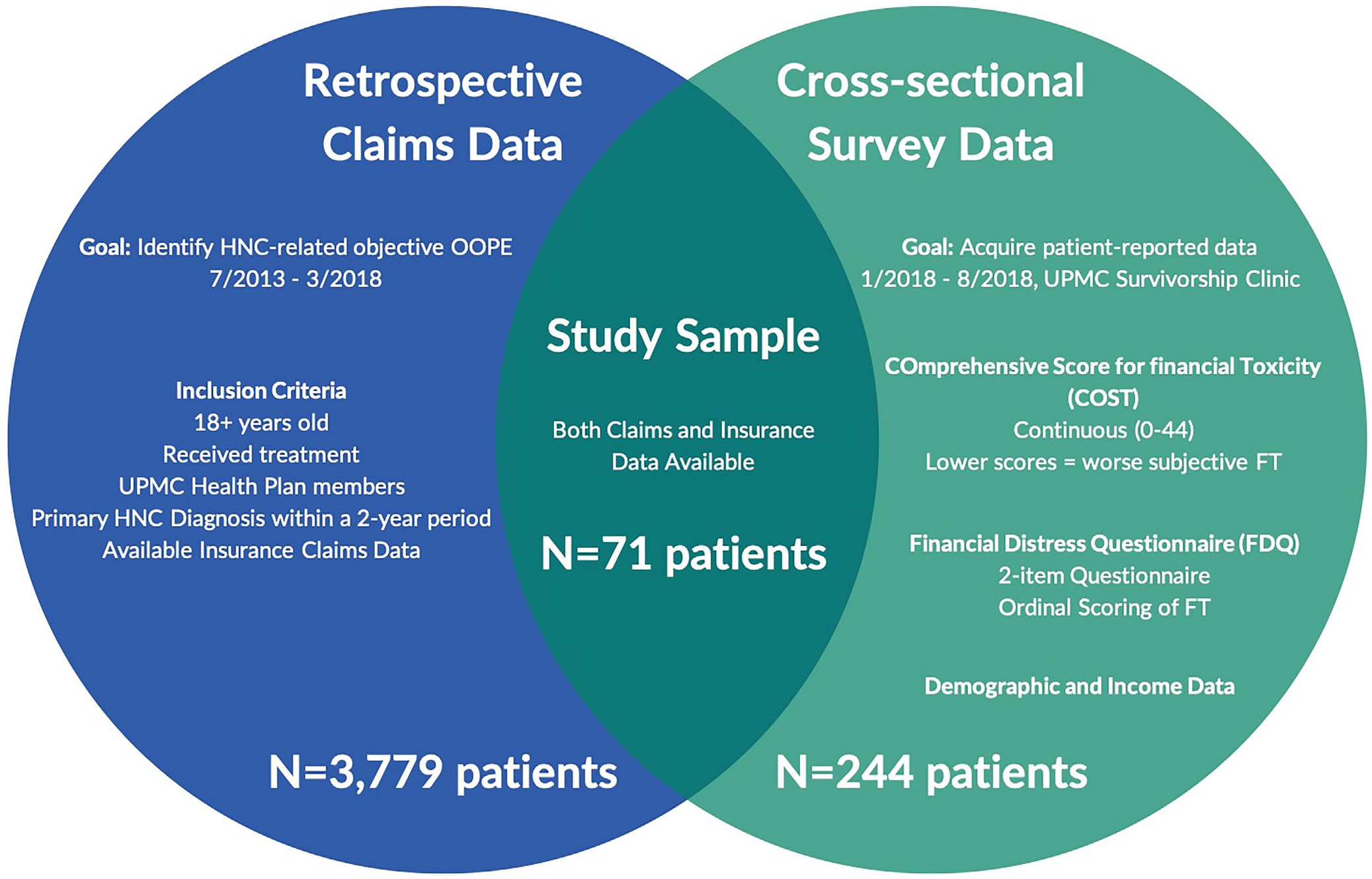

This is a cross-sectional analysis of health plan data and patient surveys assessing HNC survivors’ financial toxicity. We queried paid insurance claims data for University of Pittsburgh Medical Center (UPMC) Health Plan members with HNC primary diagnosis codes between July 2013–June 2015 (n = 5156 members). UPMC Health Plan is part of an integrated health care delivery system in partnership with UPMC. UPMC Health Plan is available to the general population and is not limited to UPMC employees. Along with its affiliates, UPMC Health Plan offers a full range of insurance lines of business, including Medicare and Medicaid. Of the 5156 members, those who received either/or a combination of surgery, chemotherapy or radiation were included for data collection. We also surveyed patients seen in a multidisciplinary HNC survivorship clinic between January 2018 and August 2018 (n = 252). Eligibility criteria included survivors ≥18 years of age having completed treatment at the time of survey data collection. The final sample included patients for whom both health plan and survey data were available (Figure 1). This study was approved by the University of Pittsburgh Institutional Review Board (PRO18010403). Patients were informed of the study, its risks and benefits, and written informed consent was obtained prior to participation.

FIGURE 1.

Study design and participants. Patients with both HNC-related claims and survey data were included for analysis (N = 71)

2.2 |. Main outcomes, variables, and measures

Main outcomes were OOPE, gross annual earnings at diagnosis and at time of survey administration, earning change from diagnosis to time of survey, and subjective financial toxicity. Demographic variables collected also included age, sex, race, marital status, education level, insurance type at time of survey, tumor site, stage, histology, HPV status, and treatment modality. OOPE refer to all costs in USD associated with HNC-related medical and pharmacy expenses incurred by health plan members between July 2013 and March 2018. These are payments not covered by the insurance plan and requiring payment directly by the members. Claims were identified based on specific financial service subgroup codes and descriptions. Gross annual earnings were defined as the annual individual employment-related earnings in USD, excluding all other sources of income. The variables are herein referred to as “earnings at diagnosis” and “earnings at survey,” respectively. To calculate earning change, earning variables were re-coded by taking the median value of each category (e.g., the category “$10 000–$19 999” was re-coded as “$15 000”). Earning change was then calculated as “Earnings at Survey minus Earnings at Diagnosis.” The variable was then dichotomized into “negative earning change” and “no/positive earning change.”

Line of business health plans were classified as Medicare (Medicare Advantage product within Part C of Medicare); Medicaid (managed care plan); Special Needs Plan (SNP; Medicare product designed specifically for special needs populations); Individual Exchange (products purchased through the Pennsylvania Marketplace under the Affordable Care Act); Commercial; and Administrative Service Only (ASO). The latter two are employer-based benefit plans. Commercial groups (i.e., employers) purchase the plan and pay per-member premiums with the insuring institution (i.e., UPMC), incurring the responsibility for all claims expenses. ASO plans engage UPMC to configure benefit designs and pay claims based on those benefits but are ultimately liable for paying for their own claims expense. They do not pay a premium, rather a USD amount for administering the benefits and adjudicating claims. For patients with coverage with more than one line of business, insurance plans were classified according to plans which provided primary coverage of HNC-related claims.

Subjective financial toxicity was assessed using previously validated patient-reported outcome (PRO) measures: The COmprehensive Score for financial Toxicity (COST) questionnaire and the Financial Distress Questionnaire (FDQ). The COST is an 11-item instrument that has demonstrated reliability and validity in measuring financial toxicity in patients with cancer.14,15 Responses are measured on a continuous scale (0–44) with lower COST scores suggesting worse toxicity. The FDQ is a 2-item questionnaire developed at the University of Pittsburgh and provides a quick assessment of an individual’s financial ability to afford everyday items. The FDQ has strong face validity and has been used in numerous populations including COPD, HIV/AIDS, heart disease, and multiple cancer types.16 It has exhibited a significant and strong correlation with COST when used in the HNC survivor population (p < 0.001).17 Financial toxicity severity by FDQ was initially scored using an ordinal classification scheme of three grade categories. Responses were then further examined as a dichotomous variable to describe low (Grade 1) or high (Grade 2 + Grade 3) toxicity. With regards to treatment modality, “nonoperative” and “adjuvant” represent radiotherapy or chemoradiotherapy. The COST and FDQ instruments are provided in Appendix (Table A1).

2.3 |. Statistical methods

COST scores are reported by mean and standard deviation. Differences in COST and FDQ by demographic and clinical characteristics were examined using Kruskal–Wallis and Fishers Exact tests, respectively. Factors associated with financial toxicity, as measured by COST, were further examined using univariable linear regression modeling. Data normality and homoscedasticity was ensured prior to regression analysis. Univariable associations with a p ≤ 0.1 were considered for inclusion in a multivariable model. Care was taken to respect sample size by maintaining a number of 15–20 subjects per included variable. Collinearity was additionally considered in selecting the final variables to include in the model by ensuring all included variables have a variable inflation factor below 5. “Earning at diagnosis” was selected in the model as its statistical significance may shed light on a variable that can be collected pretreatment in the context of a screening tool for financial toxicity. Participants with missing data points were excluded from analysis of the corresponding variables. A 95% CI was calculated around the unstandardized Beta coefficient. Results were based on 2-tailed tests and were considered significant for an observed p < 0.05. Data analysis was performed using RStudio 1.3.959 (RStudio, Boston, MA) and IBM SPSS v25 (IBM Corp., Armonk, NY). Reporting methodology followed The Strengthening the Reporting of Observational Studies in Epidemiology (STROBE) guidelines for cross-sectional studies. For simplicity and in order to avoid redundancy, associations below will be presented only with regards to COST scores. Similar results were found with FDQ and are available upon request.

3 |. RESULTS

3.1 |. Patient characteristics and financial toxicity

Of 5156 health plan members with HNC-related diagnosis codes, 3779 had HNC treatment-related claims data (73%). Two hundred forty-four of 252 patients in our HNC survivorship clinic completed financial toxicity surveys (survey response rate: 97%). Seventy-one patients had both survey and insurance claim data available for analysis, constituting our study cohort. Demographic and clinical characteristics, as well as COST scores across different patient groups are summarized in Table 1.

TABLE 1.

Patient characteristics

| Variable | Patients, no. (%) (n = 71) | COSTa (mean ± SD) | p-valueb |

|---|---|---|---|

| Age at visit (mean ± SD), years | 63.03 ± 10.45 | 24.79 ± 11.49 | |

| 28–40 | 1 (1.4%) | 0.08 | |

| 41–50 | 5 (7.0%) | ||

| 51–60 | 22 (31.0%) | ||

| 61–70 | 26 (36.6%) | ||

| 71–80 | 13 (18.3%) | ||

| >80 | 4 (5.6%) | ||

| Sex | |||

| Female | 23 (32.4%) | 20.81 ± 12.97 | 0.09 |

| Male | 48 (67.6%) | 26.57 ± 10.42 | |

| Race | |||

| White | 65 (91.5%) | 25.52 ± 11.45 | 0.07 |

| Black or African American | 6 (8.5%) | 17.33 ± 9.79 | |

| Marital status | |||

| Married/living with partner | 45 (63.4%) | 27.42 ± 11.26 | 0.007 |

| Single/divorced/separated/widowed | 26 (36.6%) | 20.28 ± 10.62 | |

| Education level | |||

| Associate degree or less | 47 (66.2%) | 22.11 ± 11.82 | 0.02 |

| Bachelor’s degree or more | 23 (32.4%) | 29.74 ± 9.38 | |

| Unknown | 1 (1.4%) | ||

| Insurance (at survey) | |||

| ASO | 5 (7.0%) | 19.60 ± 16.77 | 0.11 |

| Commercial | 17 (23.9%) | 23.94 ± 12.92 | |

| Individual exchange | 10 (14.1%) | 22.10 ± 11.62 | |

| Medicaid | 10 (14.1%) | 19.30 ± 9.89 | |

| Medicare | 27 (38.0%) | 30.00 ± 8.49 | |

| Special needs plan | 2 (2.8%) | 20.50 ± 12.02 | |

| Stage (based on AJCC 7th edition) | |||

| Stage I-II | 11 (15.5%) | 28.70 ± 10.36 | 0.14 |

| Stage III-IV | 52 (73.2%) | 23.18 ± 11.90 | |

| Not available | 8 (11.3%) | 30.00 ± 7.87 | |

| Treatment | |||

| Nonoperative | 26 (36.6%) | 22.96 ± 11.16 | 0.12 |

| Surgery alone | 9 (12.7%) | 32.33 ± 4.21 | |

| Surgery + adjuvant | 36 (50.7%) | 24.18 ± 12.47 | |

| Immunotherapy | |||

| Yes | 4 (5.6%) | 21.75 ± 11.12 | 0.54 |

| No | 67 (94.4%) | 24.98 ± 11.57 | |

| Site | |||

| Oropharynx | 22 (31.0%) | 25.18 ± 11.46 | 0.42 |

| Larynx | 17 (23.9%) | 20.47 ± 13.86 | |

| Oral cavity | 15 (21.1%) | 27.21 ± 11.13 | |

| Other | 17 (23.9%) | 26.87 ± 8.13 | |

| HPV | |||

| Positive | 22 (31.0%) | 26.91 ± 10.57 | 0.15 |

| Negative | 1 (1.4%) | ||

| Unknown/not applicable | 48 (67.6%) | 24.31 ± 11.45 | |

| Histology | |||

| Squamous cell carcinoma (SCC) | 60 (84.5%) | 24.60 ± 12.06 | 0.92 |

| Non-SCC | 11 (15.5%) | 25.90 ± 7.71 | |

| Recurrence and/or metastasis and/or second primary | |||

| Yes | 14 (19.7%) | 24.64 ± 10.23 | 0.80 |

| No | 57 (80.3%) | 24.83 ± 11.88 | |

| Time since diagnosis, years | |||

| 0–1.9 | 20 (28.2%) | 19.05 ± 12.95 | 0.02 |

| 2–3.9 | 15 (21.1%) | 22.60 ± 11.40 | |

| 4–10.9 | 18 (25.4%) | 28.25 ± 8.87 | |

| >10.9 | 18 (25.4%) | 30.24 ± 8.75 | |

| Time since completion of treatment, years | |||

| 0–1.9 | 23 (32.4%) | 19.45 ± 12.41 | 0.02 |

| 2–3.9 | 12 (16.9%) | 21.92 ± 12.65 | |

| 4–10.9 | 18 (25.4%) | 28.25 ± 8.87 | |

| >10.9 | 18 (25.4%) | 30.24 ± 8.75 | |

Note: The italic values are statistically significant.

Abbreviations: AJCC, American Joint Committee on Cancer; ASO, Administrative Service Only; COST, comprehensive score for financial toxicity; HPV, human papillomavirus; SCC, squamous cell carcinoma; SD, standard deviation.

Lower COST scores represent higher toxicity.

Kruskal–Wallis test.

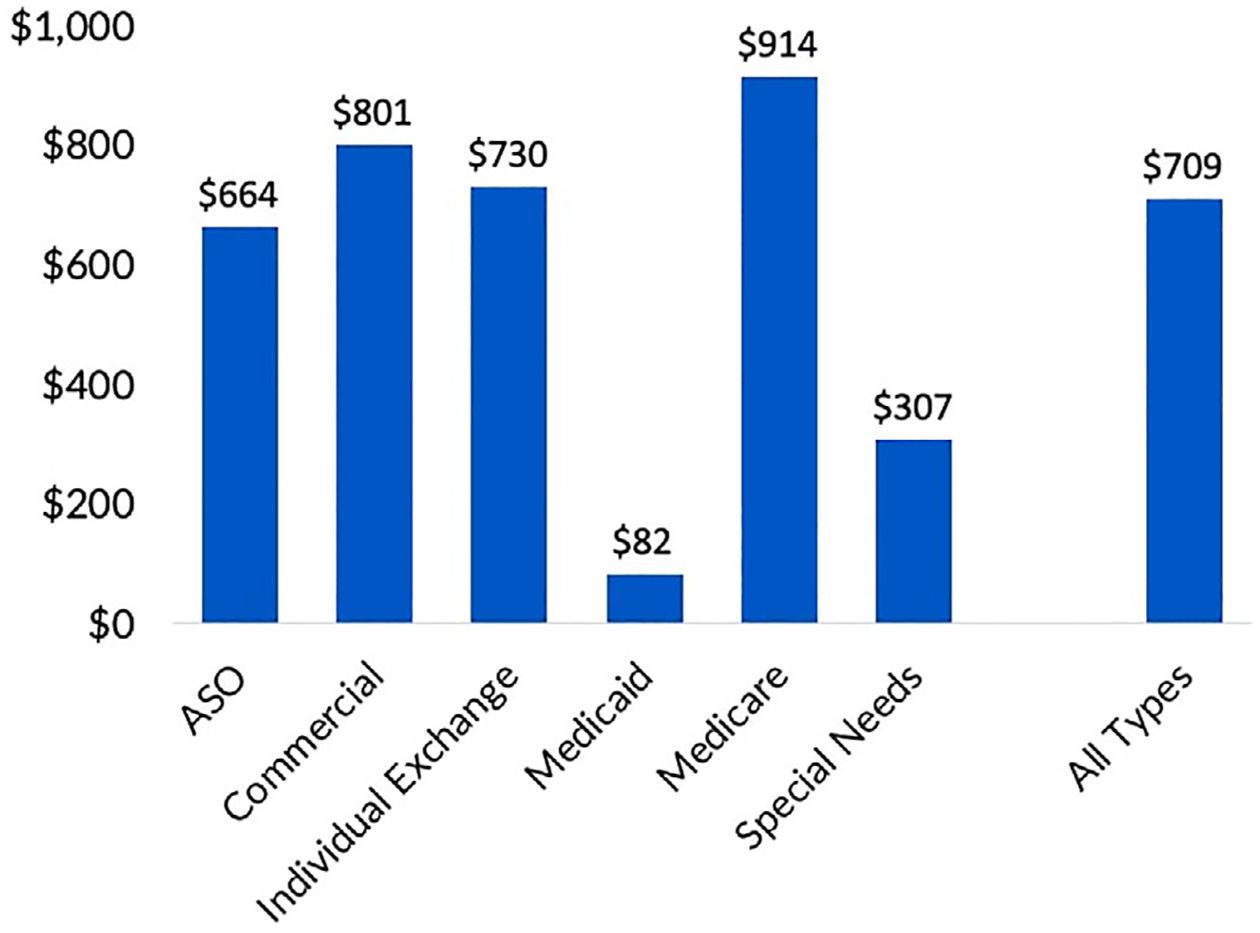

Mean annual per-member HNC-related OOPE were $709 ± 626 per year, with the highest incurred by Medicare members ($914), followed by Commercial members ($801), and the lowest incurred by Medicaid members ($82) (Figure 2). HNC-related OOPE were found to persist long after treatment completion as patients greater than 10.9 years post-treatment demonstrated mean per-member OOPE of $773 ± 626 per year. Table 2 summarizes financial metrics analyzed in this study and COST distribution across different groups. Mean COST was 24.79 ± 11.49 with the worst toxicity reported by Medicaid members (COST = 19.30 ± 9.89). Thirty-two patients (45%) reported high financial distress by FDQ.

FIGURE 2.

Mean annual per-member OOPE by insurance type (n = 71). Mean per-member HNC-related OOPE were $709 ± 626 per year, with the highest incurred by Medicare members ($914 per year), followed by Commercial members ($801 per year), and the lowest incurred by Medicaid members ($82 per year)

TABLE 2.

Factors associated with financial toxicity

| COSTa - univariate linear regression | ||

|---|---|---|

| Variable | Coefficient (95% CI) | p-value |

| Age (Δ 10y) | 3.56 (1.03–6.08) | 0.006 |

| Time since diagnosis (Δ 1y) | 0.45 (0.13–0.76) | 0.007 |

| Time since treatment completion (Δ 1y) | 0.45 (0.15–0.77) | 0.006 |

| Earnings at time of diagnosisb (Δ $10 000) | 2.24 (0.90–3.57) | 0.001 |

| Earnings at time of surveyb (Δ $10 000) | 3.79 (2.63–4.95) | <0.001 |

| log10 (Annual OOPE: Earnings at time of survey)b | −5.66 (−10.28 to −1.04) | 0.017 |

| Earning change from diagnosis to time of surveyb | ||

| Negative change | (Reference) | 0.032 |

| No/positive change | 6.03 (0.53–11.52) | |

| Marital status | ||

| Single/divorced/separated/widowed | (Reference) | 0.012 |

| Married/living with partner | 7.14 (1.60–12.68) | |

| Education levelc | ||

| Associate degree or less | (Reference) | 0.009 |

| Bachelor’s degree or more | 7.63 (1.95–13.31) | |

Abbreviations: CI, confidence interval; COST, comprehensive score for financial toxicity; OOPE, out-of-pocket expenses; y, years.

Lower COST scores represent higher toxicity.

Earnings data reflects gross/pre-tax annual earnings at the respective time-point.

One patient with an unknown education level was excluded from the analysis.

3.2 |. Clinicodemographic factors associated with financial toxicity

Significantly less subjective toxicity as measured by COST was observed in patients with greater time since diagnosis and treatment completion as compared to those who had been diagnosed or completed treatment more recently (p = 0.02 by Kruskal–Wallis test). Lower education level and lack of spousal support (i.e., single/divorced/separated/widowed) were associated with lower COST scores and thus higher subjective financial toxicity (p = 0.02 and p = 0.007, respectively, by Kruskal–Wallis test).

In univariate linear COST modeling, younger age (coefficient = 3.56; 95% CI 1.04–6.08, p = 0.006), shorter time since diagnosis (coefficient = 0.45; 95% CI 0.13–0.76; p = 0.007), and treatment completion (coefficient = 0.45; 95% CI 0.15–0.77; p = 0.006) were significantly associated with worse financial toxicity (Table 2). For every increase of 10 years in age, COST scores improved by 3.56 points, indicating less toxicity in older individuals. For every 1-year increase since diagnosis and treatment completion, COST scores increased by 0.45 points. This indicates that patients who are further out from treatment have less financial toxicity as measured by COST.

Marital status and education were also associated with financial toxicity by univariable linear regression (Table 2). Patients with lack of spousal support had worse financial toxicity compared to their married/partnered counterparts (7.14; 95% CI 1.60–12.68; p = 0.012). Survivors with lower education level (associate degree or less) also had lower COST scores (worse toxicity) compared to survivors who had a bachelor’s degree or more (7.63; 95% CI 1.95–13.31; p = 0.009). Site (p = 0.42), HPV status (p = 0.37), and histology type (p = 0.74) were not associated with worse financial toxicity by univariable linear regression. A near-significant association was found between stage and financial toxicity with higher stages being associated with worse toxicity (p = 0.059).

3.3 |. Objective financial metrics and subjective toxicity

Patients with lower gross annual earnings (p = 0.012 and p < 0.001, respectively, for diagnosis and time of survey) and/or negative earning change from diagnosis to time of survey administration (p = 0.028) had significantly lower COST scores (worse subjective financial toxicity) (Table 3). Among study participants, lower earnings were found to be significantly associated with worse subjective financial toxicity as measured by COST. This was true for both earnings at time of diagnosis (coefficient = 2.24; 95% CI 0.90–3.57; p = 0.001) and earnings at time of survey administration (coefficient = 3.79; 95% CI 2.63–4.95; p < 0.001) in univariable linear regression (similar results found in logistic regression with FDQ, data not shown) (Table 2). For every $10 000 more in earnings, survivors saw a 3.79-point improvement in their COST scores.

TABLE 3.

Patient financial data

| Variable | Patients, no. (%) (n = 71) | COSTa (mean ± SD) | p-valueb |

|---|---|---|---|

| Annual out-of-pocket expenses (mean ± SD), USD | 709 ± 626 | 24.79 ± 11.49 | |

| Annual OOPE:Earnings at time of diagnosis,c median (range) | 1.32% (0%−35%) | 24.78 ± 11.57 | |

| Annual OOPE:Earnings at time of survey,c median (range) | 1.59% (0%−25%) | 24.97 ± 11.48 | |

| Earnings at time of diagnosisc | |||

| Less than $10 000 | 6 (8.5%) | 22.83 ± 12.55 | 0.012 |

| $10 000–$19 999 | 10 (14.1%) | 20.63 ± 14.04 | |

| $20 000–$39 999 | 18 (25.4%) | 19.00 ± 10.83 | |

| $40 000–$59 999 | 11 (15.5%) | 25.18 ± 10.57 | |

| $60 000–$79 999 | 10 (14.1%) | 27.10 ± 8.21 | |

| $80 000–$99 999 | 2 (2.8%) | 40.00 ± 5.66 | |

| $100 000–$150 000 | 10 (14.1%) | 29.30 ± 10.78 | |

| Over $150 000 | 3 (4.2%) | 38.00 ± 2.65 | |

| Earnings at time of surveyc | |||

| Less than $10 000 | 11 (15.5%) | 12.82 ± 9.11 | <0.001 |

| $10 000–$19 999 | 12 (16.9%) | 20.10 ± 13.55 | |

| $20 000–$39 999 | 22 (31.0%) | 23.50 ± 8.90 | |

| $40 000–$59 999 | 11 (15.5%) | 31.20 ± 6.51 | |

| $60 000–$79 999 | 4 (5.6%) | 35.50 ± 4.44 | |

| $80 000–$99 999 | 1 (1.4%) | 43 | |

| $100 000–$150 000 | 7 (9.9%) | 34.71 ± 3.77 | |

| Over $150 000 | 2 (2.8%) | 37.00 ± 2.83 | |

| Earning change from diagnosis to time of surveyc | |||

| Negative change | 28 (39.4%) | 21.25 ± 12.37 | 0.028 |

| No/positive change | 43 (60.6%) | 27.28 ± 10.26 | |

Abbreviations: COST, comprehensive score for financial toxicity; OOPE, out-of-pocket expenses; SD, standard deviation.

Lower COST scores represent higher toxicity.

Kruskal–Wallis test.

Earnings data reflects gross/pre-tax annual earnings at the respective time-point.

Annual OOPE alone were not associated with subjective financial toxicity as measured by COST (p = 0.100) in a univariable linear regression model. However, when annual OOPE were analyzed as a proportion of annual earnings at time of survey administration (Annual OOPE:Earnings at time of survey), there was a significant association between subjective financial toxicity and objective financial burden. The association appears to be exponential. Univariable linear regression modeling exhibited a significant association between log10(Annual OOPE:Earnings at time of survey) and COST score (coefficient = −5.66; 95% CI −10.28 to −1.04; p = 0.017). In other words, the greater the proportion of earnings that OOPE constitute, the lower the COST scores (i.e., the worse the subjective financial toxicity).

In multivariable linear regression, lower earnings at diagnosis, younger age, and greater annual OOPE as a proportion of earnings at time of survey were significantly associated with worse financial toxicity as measured by COST (Table 4). Change in earnings as a categorical variable (“negative earning change” vs. “no/positive earning change”) from diagnosis to time of survey was significantly associated with COST score by univariate linear regression (coefficient = 6.03; 95% CI 0.53–11.52; p = 0.032). Survivors who had no/positive earning change had higher COST scores, thereby less financial toxicity, than those who experienced loss of earnings during their cancer survivorship. There was a significant difference in average COST scores between patients who witnessed a loss in earnings (lower score, worse toxicity) compared to those who did not (higher score, less toxicity) (mean = 21.25 ± 12.37 vs. 27.28 ± 10.26, respectively; p = 0.028).

TABLE 4.

Factors associated with financial toxicity in a multivariable model

| COSTa – multivariable linear regression | ||

|---|---|---|

| Variable | Coefficient (95% CI) | p-value |

| Age (Δ 10y) | 3.88 (1.46–6.31) | 0.002 |

| Earnings at time of diagnosisb (Δ $10 000) | 0.69 (0.05–1.34) | 0.035 |

| Log10 (Annual OOPE: Earnings at time of survey)b | −4.82 (−9.26 to −0.37) | 0.034 |

| Education level | ||

| Associate degree or less | (Reference) | 0.54 |

| Bachelor’s degree or more | ||

Abbreviations: CI, confidence interval; COST, comprehensive score for financial toxicity; OOPE, out-of-pocket expenses; y, years.

Lower COST scores represent higher toxicity.

Earnings data reflects gross/pre-tax annual earnings at the respective time-point.

4 |. DISCUSSION

Previous studies on financial toxicity among HNC survivors have provided a foundational understanding of the economic burden associated with the diagnosis and treatment of HNC.14,18,19 To the best of the authors’ knowledge, our results build on these findings and represent the first and largest investigation of cancer-specific subjective financial toxicity and objective health-related financial burden in a dedicated cohort of HNC survivors. Understanding these associations is an important first step for standardizing methods of screening patients in the clinical setting at highest risk for the sequelae of treatment-related financial toxicity.

4.1 |. Financial harms of cancer treatment

Our results indicate that, even with insurance, HNC survivors experience significant annual OOPE that can persist greater than a decade after treatment completion. The implications of these expenditures on long-term subjective financial toxicity remains a poorly investigated research need. Though examination of changes in insurance type post-treatment may also explain, in part, the persistence of OOPE beyond treatment completion, this cannot be done through the data collected in this study. It is an important point to examine in future prospective, longitudinally designed studies. Due to the nature of the disease and treatment, HNC survivors often require extensive, long-term support even after their cancer has been eradicated. These potentially life-long interventions prolong the costs of care and place HNC survivors in a particularly vulnerable financial position. Additionally, HNC survivors are often socioeconomically disadvantaged.11 It is well-documented that financial toxicity may impact individuals from any socioeconomic group, country, or insurance coverage.20,21 However, low-income workers are at higher risk for financial toxicity, and are also more likely to work in unsupportive environments.22

When survivors are unable to manage the cost of care, they turn to maladaptive coping mechanisms to temporarily alleviate economic burden. These include borrowing money, using savings, taking less than the prescribed amount of medication, avoiding procedures, tests or appointments due to cost.2,14,23–25 Patients with cancer were shown to file for bankruptcy at a rate of 2.65 times that of age, sex, and zip-code matched peers.6 These very mechanisms, however, impart negative health consequences, leading to poorer clinical outcomes and higher cancer-specific mortality.7,8,22,26–28

4.2 |. Risk factors for financial toxicity

The association between financial toxicity and poor health outcomes calls for recognition of the risk factors associated with financial toxicity. In this investigation, older age was found to be protective independently of earnings or education level. This echoes similar previously published findings and plausibly reflects the protective effects of Medicare coverage.6,29,30 Despite higher annual OOPE and greater healthcare use in older adults, elderly survivors on Medicare have higher COST scores (less financial toxicity) according to our results. In a previous investigation of 104 HNC survivors, we found patients with laryngeal/hypopharyngeal tumors had significantly lower COST scores (worse financial toxicity) compared to those with tumors of the oral cavity or oropharynx.17 Although this was not replicated in the present study, presumably due to limitations in sample size, site-specific implications on HNC financial toxicity is a topic that warrants further assessment in future studies.

Higher earnings may independently protect against, while loss of earnings may exacerbate, financial toxicity and its sequelae in HNC survivors. Earnings at time of diagnosis may thus serve as a useful criterion to include in future screening strategies aimed at identifying survivors at highest risk for financial toxicity. Lower household income and/or educational attainment have, indeed, been well-documented as being positively associated with financial hardship.30–32 Many households, particularly those with low income, lack the funds and resources to cover the cost-sharing requirements of today’s insurance plans.33,34 Others may not have sufficient savings to cope with income loss brought on by the functional implications of HNC, or other financial emergencies. A report by the Board of Governors of the Federal Reserve System found that over a third of U.S. households experienced a health emergency and/or job loss in the prior year and nearly half could not cover unexpected expenses of $400 or more.35,36 This potential unpreparedness for treatment-related expenses coupled with significant OOPE may impact future cost-conscious decision making.37

Of note, annual OOPE alone were not a predictive metric of patient-reported subjective financial toxicity. However, annual OOPE were found to be associated with greater financial toxicity when they constituted a larger proportion of the patient’s gross annual earnings. The latter findings may suggest that there is a complex interplay of factors that may affect subjective financial toxicity in addition to direct medical costs. Factors such as food and housing insecurity, household size, utility bills, employment status, and additional medical comorbidities, may all affect a patient’s income and day-to-day expenses. This is supported by our results which demonstrate that Medicaid members had the lowest OOPE but the worse financial toxicity compared to patients covered under other insurance types. Though not explicitly examined in this analysis, these findings suggest that financial stressors beyond direct cancer-related expenditures impact patient-reported financial toxicity.

The multifactorial complexity of subjective financial toxicity is particularly salient within the HNC survivor population. Factors such as treatment modality and primary site can contribute to loss of vital communication mechanisms such as hearing and speech, in addition to critical physiologic functions including breathing and swallowing. These deficits have obvious devastating consequences on patients’ work and personal lives. These functional consequences may lead to increased absenteeism,38 potential workplace discrimination,39 and eventual loss of earnings or employment. These are issues that cancer survivors in general already face at greater levels than patients without a cancer history.29,40,41 While HNC survivors experience many of the same financial challenges faced by survivors with other cancer types, there are unique factors related to the nature and location of cancers affecting the head and neck that may be important to consider in our evaluation of financial toxicity risk.

4.3 |. Interventions for prevention and mitigation of financial toxicity

As previously discussed, cancer invades the finances of those with its diagnosis. Insurance attempts to provide an avenue for relieving the patient’s burden, however, regardless of type, status, or even system, health insurance has not protected against financial toxicity as perhaps intended.42 Therefore, alternative solutions to implement at various levels of healthcare require attention and discourse.

On a hospital level, financial navigation programs that aim to address nonmedical needs of patients have developed as a specialized form of case of management.43,44 Our aforementioned results further emphasize the importance of such navigation services in intervening early, serving as liaisons between patients and community resources to connect with financial assistance programs like those mentioned above. These services have shown value in bridging the gap between medical care and financial concerns arising from such treatments.43,44 While it is not possible to infer an association between site, stage, or treatment modality given our results, understanding patient-specific financial variables that are associated with financial toxicity is important in developing targeted interventions for at-risk individuals. The ideal screening tool should be a feasible and quick assessment to identify patients most vulnerable for financial toxicity in the pre-treatment phase of cancer survivorship. The development of such tools requires the fund of knowledge that is built from studies such as this.

Beyond direct medical intervention, informal caregiving and the presence of a support system (e.g., being married, having children) have been associated with less financial toxicity among cancer survivors.45 Although less studied, informal caregivers (e.g., spouses, children of cancer survivors) may also suffer themselves from financial toxicity due to employment disruptions and loss of income during caregiving.46 Ongoing studies by our group are aimed at further understanding this relationship and the economic, psychological, and health-related impact of informal caregiving on the caregivers themselves. In this way, caregivers represent a potential avenue to target additional actionable interventions to attenuate the harms of cancer-related financial toxicity.

On a national level, strategies to decrease financial strain on patients have prioritized value by maximizing quality and minimizing cost. For example, the National Comprehensive Cancer Network has incorporated affordability as one of it five tenets of value to maximize the benefit of their recommendations.47 Outside the United States, European countries like the UK and Italy have also moved towards safeguarding cancer survivors’ employment and financial status. This includes, but is not limited to, mentioning cancer in the legal definition of “disability,” and requiring employers to make “reasonable adjustments” (e.g., time off for treatments or rehabilitation, flexibility in working hours, phased return to work policies, guaranteed return to a full-time contract) after employees have taken time off or reduced work hours to accommodate treatment and post-treatment sequelae.48,49 The United States has not provided such a definition in its disabilities act equivalent, the Americans with Disabilities Act.50 Other strategies such as price transparency legislation, included in the Affordable Care Act, seek to improve patient awareness of costs by mandating hospitals to publish standard service and testing charges.51 Further studies that can parse out the impact of treatment-related sequela, including financial toxicity, on returning to work and maintaining earning potential are needed to translate research findings into practical and meaningful changes in health policy.

4.4 |. Limitations

Though there are many strengths and novelty in the design of this study, our findings are representative of patients treated in a single health system within a relatively homogeneous demographic cohort that may not be generalizable across a national sample of patients with HNC. Despite a high survey response rate (244/252; 97%), a residual self-selection bias is possible; patients most interested in participating in this study may represent those with worse financial toxicity. The setting of our survivorship clinic within a tertiary care center may also present a selection bias whereby patients without adequate insurance coverage and/or with significant financial burden may not be able to afford care or even have the means (e.g., transportation, ability to miss work) to access such care.

Our analysis suffers from weaknesses inherent to cross-sectional studies at a single institution. The sample size limits our ability to generalize our findings and undertake a multivariable analysis with several more relevant variables. Future studies will benefit from a larger group to perform subgroup analysis including clinically relevant variables such as treatment modality and site of disease. Collaborative and multi-institutional studies would facilitate cohorts that are adequately powered for more complex statistical modeling and improve the generalizability of study findings. Sharing the findings from our experience encourages opportunities for future initiatives with partnering health systems. Metrics collected that are subject to recall bias and/or hesitancy in disclosure, such as earnings at diagnosis and earnings at time of survey, are also a limitation of this study. Patient-reported income data was used to reflect individual earnings, without the inclusion of other sources of income, such as social security or disability claims. Though this is an acknowledged limitation, similar methods to analyze self-reported income data have been corroborated by other research groups.45,52,53

Our surveys were limited to demographic characteristics, annual earnings data, and subjective financial toxicity assessment tools (COST and FDQ). It is well documented that medically-related financial toxicity is influenced by non-healthcare-related factors. Considerations such as food insecurity,54 nonmedical costs of seeking care,55,56 and loss of employment have been studied57 but require more in-depth analysis within the HNC survivor population. Survey data were supplemented by HNC-specific OOPE data extracted via insurance claims for individuals who received care through the insuring institution. These expenditures may not reflect regional or health system variations in costs among other HNC populations.

5 |. CONCLUSIONS

To the best of the authors’ knowledge, this is the first and largest investigation of cancer-specific subjective financial toxicity and objective health-related financial burden in a dedicated cohort of HNC survivors. Through associations demonstrated between subjective financial toxicity and lower gross annual earnings, loss of earnings after treatment, as well as greater OOPE as a proportion of earnings, our data serves as a foray into the development of a screening strategies to effectively detect survivors at highest risk for financial toxicity in the pre-treatment setting. These results invite future multi-institutional, collaborative initiatives to investigate financial toxicity in a prospective, longitudinal context. An understanding of financial toxicity in an oncology population that is undoubtedly unique from other cancer types is challenging and entangled with competing variables. It requires thoughtful inquiry of potential causal relationships between economic metrics, (e.g., household income, employment, OOPE, etc.) and patient-reported outcomes (e.g., quality of life assessments, mental health screening tools, well-being)—all done simultaneously over multiple time points in the survivorship course. It is not something that can be accomplished by a single institution. We must align necessary strategic partners to acknowledge the problem, incorporate screening initiatives and referrals to appropriate resources for mitigation in clinical practices, and learn that discussions regarding the costs of treatment in clinical practice must become part of the conversation in cancer care.

ACKNOWLEDGMENTS

The authors would like to thank Dr. Shyamal Peddada for his contribution and advisement regarding statistical analysis and methods. This work was supported by grant funding from the AAO-HNSF Health Services Research Grant (Mady), the UPMC Hillman Cancer Center Specialized Programs of Research Excellence (Ferris, Mady), and the 5T32DC000066 NIH/NIDCD Research Training in Otolaryngology (Johnson, Mady). The funding bodies had no role in study design, data collection and analysis, decision to publish, or preparation of the manuscript.

Funding information

American Academy of Otolaryngology-Head and Neck Surgery Foundation Health Services Research Grant; NIH/NIDCD Research Training in Otolaryngology, Grant/Award Number: 5T32DC000066; UPMC Hillman Cancer Center Specialized Program of Research Excellence

CONFLICT OF INTEREST

Robert L. Ferris declares support for consulting/advisory role (Aduro Biotech, Inc., Amgen, AstraZeneca/MedImmune, Bain Capital Life Sciences, EMD Serano, GlaxoSmithKline, Iovance Biotherapeutics, Inc., Lilly, MacroGenics, Inc., Merck, Nanobiotix, Numbab Therapeutics AG, Oncorus, Inc., Ono Pharmaceutical Co., Ltd., Pfizer, PPD, Regeneron Pharmaceuticals, Inc., Tesaro, Torque Therapeutics, TTMS) and research funding (Astra-Zeneca/MedImmune, BristolMyers Squib, Merck, Tesaro, TTMS, VentiRx Pharmaceuticals).

APPENDIXA: COMPREHENSIVE SCORE FOR FINANCIAL TOXICITY

TABLE A1.

Below is a list of statements that other people with your illness have said are important. Please select one statement per line to indicate your response as it applies to the past 7 days14,15

| Not at all | A little bit | Somewhat | Quite a bit | Very much | |

|---|---|---|---|---|---|

| I know that I have enough money in savings, retirement, or assets to cover the costs of my treatment | ○ | ○ | ○ | ○ | ○ |

| My out-of-pocket medical expenses are more than I thought they would be | ○ | ○ | ○ | ○ | ○ |

| I worry about the financial problems I will have in the future as a result of my illness or treatment | ○ | ○ | ○ | ○ | ○ |

| I feel I have no choice about the amount of money I spend on care | ○ | ○ | ○ | ○ | ○ |

| I am frustrated that I cannot work or contribute as much as I usually do | ○ | ○ | ○ | ○ | ○ |

| I am satisfied with my current financial situation | ○ | ○ | ○ | ○ | ○ |

| I am able to meet my monthly expenses | ○ | ○ | ○ | ○ | ○ |

| I feel financially stressed | ○ | ○ | ○ | ○ | ○ |

| I am concerned about keeping my job and income, including work at home | ○ | ○ | ○ | ○ | ○ |

| My cancer or treatment has reduced my satisfaction with my present financial situation | ○ | ○ | ○ | ○ | ○ |

| I feel in control of my financial situation | ○ | ○ | ○ | ○ | ○ |

Footnotes

Data in this manuscript were presented at the American Society of Preventive Oncology 44th Annual Meeting and the 2020 Annual Meeting of the Pennsylvania Academy of Otolaryngology – Head and Neck Surgery.

DATA AVAILABILITY STATEMENT

The data that support the findings of this study are available from the corresponding author upon reasonable request.

REFERENCES

- 1.Howard DH, Molinari NA, Thorpe KE. National estimates of medical costs incurred by nonelderly cancer patients. Cancer. 2004;100(5):883–891. [DOI] [PubMed] [Google Scholar]

- 2.Zafar SY, Peppercorn JM, Schrag D, et al. The financial toxicity of cancer treatment: a pilot study assessing out-of-pocket expenses and the insured cancer patient’s experience. Oncologist. 2013;18(4):381–390. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 3.Langa KM, Fendrick AM, Chernew ME, Kabeto MU, Paisley KL, Hayman JA. Out-of-pocket health-care expenditures among older Americans with cancer. Value Health. 2004;7(2):186–194. [DOI] [PubMed] [Google Scholar]

- 4.Himmelstein DU, Warren E, Thorne D, Woolhandler S. Illness and injury as contributors to bankruptcy: even universal coverage could leave many Americans vulnerable to bankruptcy unless such coverage was more comprehensive than many current policies. Health Aff. 2005;24(Suppl 1):W5–63–W65–73. [DOI] [PubMed] [Google Scholar]

- 5.Gordon LG, Merollini KM, Lowe A, Chan RJ. A systematic review of financial toxicity among cancer survivors: we can’t pay the co-pay. Patient. 2017;10(3):295–309. [DOI] [PubMed] [Google Scholar]

- 6.Ramsey S, Blough D, Kirchhoff A, et al. Washington state cancer patients found to be at greater risk for bankruptcy than people without a cancer diagnosis. Health Aff (Millwood). 2013; 32(6):1143–1152. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 7.Ramsey SD, Bansal A, Fedorenko CR, et al. Financial insolvency as a risk factor for early mortality among patients with cancer. J Clin Oncol. 2016;34(9):980–986. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 8.Zafar SY, McNeil RB, Thomas CM, Lathan CS, Ayanian JZ, Provenzale D. Population-based assessment of cancer survivors’ financial burden and quality of life: a prospective cohort study. J Oncol Pract. 2015;11(2):145–150. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 9.Jacobson JJ, Epstein JB, Eichmiller FC, et al. The cost burden of oral, oral pharyngeal, and salivary gland cancers in three groups: commercial insurance, Medicare, and Medicaid. Head Neck Oncol. 2012;4(1):15. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 10.Cohen EE, LaMonte SJ, Erb NL, et al. American Cancer Society head and neck cancer survivorship care guideline. CA Cancer J Clin. 2016;66(3):203–239. [DOI] [PubMed] [Google Scholar]

- 11.Massa ST, Osazuwa-Peters N, Adjei Boakye E, Walker RJ, Ward GM. Comparison of the financial burden of survivors of head and neck cancer with other cancer survivors. JAMA Otolaryngol Head Neck Surg. 2019;145(3):239–249. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 12.Murphy BA, Deng J. Advances in supportive care for late effects of head and neck cancer. J Clin Oncol. 2015;33(29):3314–3321. [DOI] [PubMed] [Google Scholar]

- 13.Giuliani M, Papadakos J, Broadhurst M, et al. The prevalence and determinants of return to work in head and neck cancer survivors. Support Care Cancer. 2019;27(2):539–546. [DOI] [PubMed] [Google Scholar]

- 14.de Souza JA, Kung S, O’Connor J, Yap BJ. Determinants of patient-centered financial stress in patients with locally advanced head and neck cancer. J Oncol Pract. 2017;13(4): e310–e318. [DOI] [PubMed] [Google Scholar]

- 15.De Souza JA, Yap BJ, Hlubocky FJ, et al. The development of a financial toxicity patient-reported outcome in cancer: the COST measure. Cancer. 2014;120(20):3245–3253. [DOI] [PubMed] [Google Scholar]

- 16.Sereika S, Engberg S. Development of standardized sociodemographic and co-morbidity questionnaires. Paper presented at: Sigma Theta Tau International Honor Society of Nursing 17th International Nursing Research Congress; 2006. [Google Scholar]

- 17.Mady LJ, Lyu L, Owoc MS, et al. Understanding financial toxicity in head and neck cancer survivors. Oral Oncol. 2019;95:187–193. [DOI] [PubMed] [Google Scholar]

- 18.Divi V, Tao L, Whittemore A, Oakley-Girvan I. Geographic variation in Medicare treatment costs and outcomes for advanced head and neck cancer. Oral Oncol. 2016;61:83–88. [DOI] [PubMed] [Google Scholar]

- 19.Wissinger E, Griebsch I, Lungershausen J, Foster T, Pashos CL. The economic burden of head and neck cancer: a systematic literature review. Pharmacoeconomics. 2014;32(9):865–882. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 20.Gordon LG, Chan RJ. Financial toxicity among patients with cancer—Where to from here? Cancer Nurs. 2017;40(4):257–258. [DOI] [PubMed] [Google Scholar]

- 21.Head B, Harris L, Kayser K, Martin A, Smith L. As if the disease was not enough: coping with the financial consequences of cancer. Support Care Cancer. 2018;26(3):975–987. [DOI] [PubMed] [Google Scholar]

- 22.Carrera PM, Kantarjian HM, Blinder VS. The financial burden and distress of patients with cancer: understanding and stepping-up action on the financial toxicity of cancer treatment. CA Cancer J Clin. 2018;68(2):153–165. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 23.Costas-Muniz R, Leng J, Aragones A, et al. Association of socioeconomic and practical unmet needs with self-reported non-adherence to cancer treatment appointments in low-income Latino and Black cancer patients. Ethn Health. 2016;21(2):118–128. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 24.Kaisaeng N, Harpe SE, Carroll NV. Out-of-pocket costs and oral cancer medication discontinuation in the elderly. J Manag Care Pharm. 2014;20(7):669–675. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 25.Streeter SB, Schwartzberg L, Husain N, Johnsrud M. Patient and plan characteristics affecting abandonment of oral oncolytic prescriptions. J Oncol Pract. 2011;7(3S):46s–51s. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 26.Fenn KM, Evans SB, McCorkle R, et al. Impact of financial burden of cancer on survivors’ quality of life. J Oncol Pract. 2014;10(5):332–338. [DOI] [PubMed] [Google Scholar]

- 27.Kale HP, Carroll NV. Self-reported financial burden of cancer care and its effect on physical and mental health-related quality of life among US cancer survivors. Cancer. 2016;122(8):283–289. [DOI] [PubMed] [Google Scholar]

- 28.Lathan CS, Cronin A, Tucker-Seeley R, Zafar SY, Ayanian JZ, Schrag D. Association of financial strain with symptom burden and quality of life for patients with lung or colorectal cancer. J Clin Oncol. 2016;34(15):1732–1740. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 29.Banegas MP, Guy GP Jr, de Moor JS, et al. For working-age cancer survivors, medical debt and bankruptcy create financial hardships. Health Aff. 2016;35(1):54–61. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 30.Rim SH, Guy GP Jr, Yabroff KR, McGraw KA, Ekwueme DU. The impact of chronic conditions on the economic burden of cancer survivorship: a systematic review. Expert Rev Pharmacoecon Outcomes Res. 2016;16(5):579–589. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 31.Huang I-C, Bhakta N, Brinkman TM, et al. Determinants and consequences of financial hardship among adult survivors of childhood cancer: a report from the St. Jude Lifetime Cohort Study. J Natl Cancer Inst. 2019;111(2):189–200. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 32.Wheeler SB, Spencer JC, Pinheiro LC, Carey LA, Olshan AF, Reeder-Hayes KE. Financial impact of breast cancer in black versus white women. J Clin Oncol. 2018;36(17):1695–1701. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 33.Claxton G, Rae M, & Panchal N. Consumer assets and patient cost sharing. http://kff.org/health-costs/issue-brief/consumer-assets-and-patient-cost-sharing/. Accessed March 30, 2021.

- 34.Yousuf ZS. Financial toxicity of cancer care: it’s time to intervene. J Natl Cancer Inst. 2016;108(5):djv370. [DOI] [PubMed] [Google Scholar]

- 35.Despard MR, Friedline T, Martin-West S. Why do households lack emergency savings? The role of financial capability. J Family Econ Issues. 2020;41:542–557. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 36.Larrimore J, Dodini S, Thomas L. Report on the economic well-being of U.S. households in 2015. Board of Governors of the Federal Reserve System Report; 2016.

- 37.Chino F, Peppercorn JM, Rushing C, et al. Out-of-pocket costs, financial distress, and underinsurance in cancer care. JAMA Oncol. 2017;3(11):1582–1584. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 38.Steiner JF, Cavender TA, Main DS, Bradley CJ. Assessing the impact of cancer on work outcomes. Cancer. 2004;101(8):1703–1711. [DOI] [PubMed] [Google Scholar]

- 39.Mehnert A. Employment and work-related issues in cancer survivors. Crit Rev Oncol Hematol. 2011;77(2):109–130. [DOI] [PubMed] [Google Scholar]

- 40.Ekwueme DU, Yabroff KR, Guy GP Jr, et al. Medical costs and productivity losses of cancer survivors—United States, 2008–2011. MMWR Morb Mortal Wkly Rep. 2014;63(23):505–510. [PMC free article] [PubMed] [Google Scholar]

- 41.Howlader N, Noone A, Krapcho M, et al. SEER cancer statistics review, 1975–2016. Bethesda, MD: National Cancer Institute; 2019. [Google Scholar]

- 42.Desai A, Gyawali B. Financial toxicity of cancer treatment: moving the discussion from acknowledgement of the problem to identifying solutions. EClinicalMedicine. 2020;20:100269. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 43.Shankaran V, Leahy T, Steelquist J, et al. Pilot feasibility study of an oncology financial navigation program. J Oncol Pract. 2018;14(2):e122–e129. [DOI] [PubMed] [Google Scholar]

- 44.Yezefski T, Steelquist J, Watabayashi K, Sherman D, Shankaran V. Impact of trained oncology financial navigators on patient out-of-pocket spending. Am J Manag Care. 2018;24 (5):S74–S79. [PubMed] [Google Scholar]

- 45.De Souza JA, Yap BJ, Wroblewski K, et al. Measuring financial toxicity as a clinically relevant patient-reported outcome: the validation of the COmprehensive Score for financial Toxicity (COST). Cancer. 2017;123(3):476–484. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 46.Syse A, Tretli S, Kravdal Ø. The impact of cancer on spouses’ labor earnings: a population-based study. Cancer. 2009;115 (S18):4350–4361. [DOI] [PubMed] [Google Scholar]

- 47.NCCN. Evidence blocks: Frequently asking questions. https://www.nccn.org/evidenceblocks/pdf/EvidenceBlocksFAQ.pdf. Published 2016. Accessed July 5, 2020.

- 48.Equality Act c 15, sch 1, pt 1(6). In; 2010.

- 49.Italy Cancer Survivorship Country Profile. The Economist. http://cancersurvivorship.eiu.com/countries/italy/. Accessed October 22, 2020. [Google Scholar]

- 50. 42 U.S.C. §12101. In.

- 51. 42 U.S.C. §300gg-18. In.

- 52.Blinder V, Eberle C, Patil S, Gany FM, Bradley CJ. Women with breast cancer who work for accommodating employers more likely to retain jobs after treatment. Health Aff. 2017;36 (2):274–281. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 53.Shankaran V, Jolly S, Blough D, Ramsey SD. Risk factors for financial hardship in patients receiving adjuvant chemotherapy for colon cancer: a population-based exploratory analysis. J Clin Oncol. 2012;30(14):1608–1614. [DOI] [PubMed] [Google Scholar]

- 54.Zheng Z, Jemal A, Tucker-Seeley R, et al. Worry about daily financial needs and food insecurity among cancer survivors in the United States. J Natl Compr Canc Netw. 2020;18(3):315–327. [DOI] [PubMed] [Google Scholar]

- 55.Lee A, Shah K, Byun J, Chino F. Nickel and dimed: parking fees at NCI-designated cancer centers. Journal of Clinical Oncology. 2020;38:2029. [Google Scholar]

- 56.Premnath N, Grewal US, Gupta A. Park the parking. JCO Oncol Pract. 2020;16(5):215–217. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 57.Yabroff KR, Bradley C, Shih Y-CT. Understanding financial hardship among cancer survivors in the United States: strategies for prevention and mitigation. J Clin Oncol. 2020;38(4): 292–301. [DOI] [PMC free article] [PubMed] [Google Scholar]

Associated Data

This section collects any data citations, data availability statements, or supplementary materials included in this article.

Data Availability Statement

The data that support the findings of this study are available from the corresponding author upon reasonable request.