Abstract

As a once-in-a-century global pandemic, COVID-19 severely hit the global economy and disrupted the worldwide supply chain. Based on 505 Chinese firms, we use the event study method to explore the effect of COVID-19 on the financial performance of firms. The findings show that COVID-19 has an immediate impact on Chinese firms. Hubei firms experience stronger effects than non-Hubei firms. Supply chain disruptions effects from COVID-19 are observed. Transportation industry is hit more severely than retail industry. Insurance companies experience a strong adverse effect. On the other hand, both medical and competitor firms experience significantly positive spillover effects.

Keywords: COVID-19, Abnormal returns, Event study, Supply chain disruption

1. Introduction

At the end of 2019, an unanticipated disease technically called COVID-19 broke out and spread worldwide. COVID-19 is a once-in-a-century global pandemic. It has taken the world by storm (Yan, Tu, Stuart, & Zhang, 2020). As a public health emergency (Shahzad, Naeem, Peng, & Bouri, 2021), it has fundamentally affected the global economy. International Monetary Fund (IMF) officials stated that “We anticipate the worst economic fallout since the Great Depression.”1 The real economic activity has already been damaged by COVID-19, and it is still unknown the extent of its impact (Chowdhury & Abedin, 2020). Furthermore, COVID-19 causes previously unprecedented economic damages, which are present in every area of the world (Goodell, 2020). A contraction of −3.1% in 2020 of the global economy was estimated by International Monetary Fund (2021a). The value of world merchandise exports declined by 8%, and services trade contracted by 21% in 2020 (WTO, 2021). Additionally, the society, policy makers, and all financial markets participants and individual investors are the economic and social costs of COVID-19 (Sharif, Aloui, & Yarovaya, 2020). For market participants, COVID-19 came as a shock (Ramelli & Wagner, 2020). On 9 March 2020, the S&P dropped by 7% in just four minutes (Samitas, Kampouris, & Polyzos, 2022). The global bourses saw almost 30% of wealth loss within 100 days (Ali, Alam, & Rizvi, 2020). Additionally, the COVID-19 pandemic causes the increase of the stock market crash risk (Liu, Huynh, & Dai, 2021). As the pandemic was an extremely unlikely event resulting in severe unfavorable economic consequences, it is seen as a “black swan” (AlAli, 2020). The short-term impact brought by COVID-19, which does not cyclically affect the economy, surpasses any endogenous and extreme events in the past (He, Sun, Zhang, & Li, 2020). Furthermore, both the domestic demand and supply sides are significantly affected by the pandemic (Liu et al., 2021; Samitas et al., 2022). Due to the significant impact from COVID-19, this paper aims to assess the effects of the COVID-19 pandemic on the economy, especially focuses on China's stock market reaction to supply chain disruptions from COVID-19.

To control the spread of the disease, measures such as restrictions in transportation facilities, border closure, and stopping the operation of factories were made, which inevitably lead to supply chain disruption. Because many of the supply chains were not at all prepared to bear such a serious pandemic (Veselovská, 2020). To grasp the financial market reaction to supply chain disruptions from COVID-19, we employ the event study method (ESM) to empirically examine the effects of COVID-19 on the financial performance of firms. Following Hendricks, Jacobs, and Singhal (2019), we use changes in stock prices to measure financial performance. Since stock price reaction is taken as a preview of the future economic impact of the pandemic (Ramelli & Wagner, 2020).

In the analysis, 406 publicly traded firms are collected from news reports in the China Infobank database to identify firms affected by COVID-19. The firm's place of incorporation is in China, with 19% in Hubei, and 81% not in Hubei. Additionally, 99 firms with the largest scale in the transportation and retail industries are also chosen. The direct effects, propagation effects, including upstream, downstream, and multiple effects of supply chain disruptions, and the competitive effects are examined to develop insights into the impact of COVID-19.

The results show that COVID-19 has an immediate impact on Chinese firms. But the sample firms as a result of COVID-19 benefit on average 0.87% of their shareholder value during one-month period after the pandemic. In addition, Hubei firms experience stronger effects than non-Hubei firms. Furthermore, a positive downstream supply chain propagation effect from suppliers to customers resulting from COVID-19 is observed, while the upstream propagation effect from customers to suppliers is negative. The multiple effects are positive but do not sustain. Transportation and retail industries are severely hit by COVID-19, with negative effects on the former industry being greater and more persistent. Besides, insurance companies experience a strong adverse effect over the first month after the outbreak of COVID-19. On the other hand, both medical and competitor subsamples experience significantly positive spillover effects over one-month period. In addition, an immediate reaction to the global spread of COVID-19 is not observed for the directly affected firms. The downstream supply chain propagation effect from suppliers to customers is negative, while positive effect prevails for upstream propagation effect from customers to suppliers after lifting the lockdown of Wuhan. Considering the multiple effects, the firms are hit so severely by the global spread of COVID-19 due to the global economic integration.

Our study contributes to the existing literature in the following ways. First of all, we thoroughly investigate China's stock market reaction to supply chain disruptions from COVID-19, including upstream, downstream, and multiple effects of supply chain disruptions. Secondly, we distinguish the effects of COVID-19 on Hubei firms from that on non-Hubei firms. Since Wuhan, the provincial capital of Hubei, is the first city to announce “lockdown”. Last but not least, COVID-19, unlike other epidemics, gradually spreads worldwide. We explore the effects of supply chain disruptions due to the global spread of COVID-19 besides the impact when China is the epicenter.

The remainder of the study proceeds as follows. Section 2 summarizes the related literature. The methodology, sample and data employed in the study are detailed in section 3. Section 4 discusses the empirical results and implications. The last section concludes the work.

2. Related literature

Since the outbreak of COVID-19, the impact of this epidemic disease on the economy has attracted wide attention in academia. It is undeniable that the COVID-19 outbreak has shocked the global economy. Sudden and massive disruptions in the flow of goods and services have been caused by the measures including lockdowns, travel restrictions, shelter-in-place orders and social distancing measures adopted to curb the spread of COVID-19 (Harjoto, Rossib, & Paglia, 2021). Furthermore, the effect is severe and sustained (Iyke, 2020). All sectors around the world are influenced by COVID-19 (Machmuddah, Utomo, Suhartono, Ali, & Ghulam, 2020). However, countries and sectors are disrupted differently by the pandemic, and the extent of policy support as well as economic recoveries are varied (IMF, 2021b).

2.1. The effects of COVID-19 on the global economy

Compared to modern history pandemics, COVID-19 comes at a larger scale (Khatatbeh, Hani, & Abu-Alfoul, 2020). Zhang, Wang, and Nosheen (2021) consider COVID-19 as one of the biggest pandemics in history. The real economy is severely hit by COVID-19 (Albulescu, 2021). Ozili and Arun (2020) point that there are two methods by which COVID-19 stifled economic activities. The first one is social distancing resulting from the spread of the virus, which leads to the shutdown of economic activities. Another one is safe consumption and investment due to the rising uncertainty. In addition, risk spillover effects could be incorporated in COVID-19 (Yan & Qian, 2020). Since both the demand and supply sides of almost every area of human endeavor are shocked by the pandemic (El-Erian, 2020). Employing t-tests and non-parametric Mann-Whitney tests, He, Liu, Wang, and Yu (2020) examine the direct effects and spillover effects of COVID-19 on the stock market. They find a negative but short-term effect of COVID-19 on the stock markets of affected countries. Furthermore, bidirectional spillover effects are observed between Asian countries and European and American countries.

The worldwide financial markets are the reflection of the businesses which begin to be affected by the global spread of the COVID-19 pandemic (Latif et al., 2021). COVID-19 causes market uncertainty (Latif et al., 2021; Phan & Narayan, 2020), which could lead to financial volatility (Hartwell, 2018), and cause markets to become highly unpredictable (Zhang, Hu, & Ji, 2020). And financial sector was most affected (Herwany, Febrian, Anwar, & Gunardi, 2021). As an important capital market that can intuitively reflect the financial behavior of a resident and the economic conditions of a country (Yan & Qian, 2020), the stock market could provide a perspective for predicting real economic activity (Khatatbeh et al., 2020). It is considered as the index of the economy of a country (Chowdhury & Abedin, 2020). Thus, the impact of COVID-19 has been correctly anticipated by the global stock markets (Khatatbeh et al., 2020), and it is predicted to be amplified through financial channels (Ramelli & Wagner, 2020).

Ali et al. (2020) consider the COVID-19 as a bane for the financial markets. The stock market has not been impacted as forcefully as COVID-19 by previous infectious disease outbreak (Baker et al., 2020). Using daily data series of stock price indices, Khatatbeh et al. (2020) provide evidence for the immediate reactions of global stock markets to the outbreak of the COVID-19 pandemic. Hoang, Nguyen, and Nguyen (2022) argue that the increase in the accumulated COVID-19 confirmed cases worsens stock returns. Latif et al. (2021) estimate that a 1% increase in COVID-19 leads to a 0.8% and 0.56% decline in stock return and GDP, respectively. Phan and Narayan (2020) consider the stock price as the most active financial indicator. They examine the real-time reaction of stock price to different stages in COVID-19's evolution. The findings show an overreaction of the stock market to COVID-19. Since the stock prices are influenced by emergencies, such as COVID-19, which affect investor sentiment, hence investor behavior (He, Sun, et al., 2020). Sun, Wu, Zeng, and Peng (2021) present a stronger positive correlation between individual investor sentiment and stock returns than usual. Hence, the COVID-19 outbreak would then cause short-term investor overreaction (Liu, Manzoor, Wang, Zhang, & Manzoor, 2020). But Khatatbeh et al. (2020) suggest an underreaction to the pandemic's announcement. Nevertheless, the market is going to correct itself as more information becomes more available with time (Phan & Narayan, 2020; Yan et al., 2020). Zhang et al. (2021) argue that the stock market could be badly affected by COVID-19 in the long run. So, it is too early to be certain of the pandemic effects (Khatatbeh et al., 2020).

2.2. The effects of COVID-19 on the economy: Country-level

No economy is immune to the negative effects of COVID-19 (Samitas et al., 2022). Using indices in G-20 countries, Singh, Dhall, Narang, and Rawat (2020) observe that stock markets of both developing and developed economies are negatively affected by COVID-19. Focusing on the US stock market, Chowdhury and Abedin (2020) explore the impact of COVID-19, measured by confirmed cases and death cases. They show that the US stock market reacts negatively to the two variables. Since market illiquidity and volatility increase for the occurrence of COVID-19 (Baig, Butt, Haroon, & Rizvi, 2021). Using text-based methods, Baker et al. (2020) point out that the COVID-19 pandemic has unprecedentedly affected the US stock market mainly due to the government restrictions on commercial activity and voluntary social distancing, operating with powerful effects in a service-oriented economy. From the perspective of firm's international exposure and multinationality, Yong and Laing (2021) reveal that international exposure through foreign sales, foreign assets, imports and exports are significant and negatively related to standardized cumulative abnormal returns in the short run, while the effect reverses in the long run. Furthermore, firms with international exposure (or are more multinational) are more resilient to economic shocks as a consequence of COVID-19.

Besides the US economy, the pandemic destroys the other economy. Employing the average daily returns of the five largest Asian stock markets (Shanghai SE, Nikkei 225, Bombay SE, Hang Seng Index, and South Korea KOSPI Composite Index), AlAli (2020) finds a negative effect of WHO announcement2 on stock markets returns on the five Asian stock markets. Besides, Al-Awadhi, Alsaifi, Al-Awadhi, and Alhammadi (2020), Khatatbeh et al. (2020) find a significant negative effect of COVID-19 on Chinese stock returns and affected countries' stock markets, respectively. Employing Exponential GARCH models, Ali et al. (2020) suggest that China, as the earlier epicenter, has stabilized, while the global markets have seen larger volatility. Ftiti, Ameur, and Louhichi (2021) argue that the COVID-19 outbreak is accompanied by various types of new. They use the data in China and present that the stock market returns volatility is elevated and the level of stock market liquidity is impaired by the non-fundamental news, which is measured by the number of deaths and cases related to COVID-19. Employing China's A-share listed companies, Sun et al. (2021) finds an overall negative effect on stock market of COVID-19 during the post-event window. Shen and Zhang (2021) distinguish the stay-at-home stocks (SAH) from the go-outsides stocks (GO).3 They find a significantly negative return on the event day and reversed cumulative abnormal return for the GO stocks, while no significantly negative return on the event day and increasing cumulative abnormal return for the SAH stocks.

2.3. The effects of COVID-19 on the economy: Industry-level

Sectors are unequally affected by the pandemic (Guerrieri, Lorenzoni, Straub, & Werning, 2020; Yan & Qian, 2020). He, Sun, et al. (2020) investigate the impact of COVID-19 on Chinese industries. They find that Chinese traditional industries, such as transportation, mining, electricity and heating, and the environment, are adversely affected by the pandemic. While it generates development opportunities for high-tech industries, including manufacturing, information technology, education, and health. The offline consumer purchases have been disrupted by restricting the travel and movement of people due to the outbreak of COVDI-19. Yan and Qian (2020) explore the reaction of the consumer industry in China's stock market to the pandemic. Their results show that the return on consumer stocks gradually recovered as the event spread, even if China's consumer stock market is dramatically influenced by the pandemic in the short run. For the reason of investors' overreactions to the pandemic lockdown, Huo and Qiu (2020) observe reversals both at industry and firm levels in China's stock market. They also find that Leisure Service industry is the most negatively affected industry, while industries such as Pharmaceutical & Biotechnology, Computer and Electronics are positively affected. Furthermore, industries and stocks that reacted positively to the announcement of the pandemic lockdown have mostly driven the overreactions.

2.4. The channels

The possible explanation for the effects of COVID-19 on the economy could be as follows. Substantial risk and great uncertainty rise accompanied by the pandemic (Herwany et al., 2021; Zhang et al., 2020). Because investors' pessimistic sentiments such as anxiety, bad mood, and fear would be catalyzed by the media coverage of drastic events ( Ichev & Marinč, 2018). Duan, Liu, and Wang (2021) develop the real-time and forward-looking COVID-19 sentiment indices to capture the moods related to COVID-19 and find that stock returns and turnover rates are positively predicted by the COVID-19 sentiments during the research period. Furthermore, the effects of COVID-19 are amplified by the sentiments. Sun et al. (2021) prove that the COVID-19 pandemic causes widespread negative sentiment, which cause investor anxiety and market turbulence. The uncertainty and investor fear lead to the suspension in economic activities and the price pressure, which would cause the downfall of stock markets (Singh et al., 2020).

Furthermore, Khatatbeh et al. (2020) summarize the channels through which the effects of COVID-19 could be transmitted to stock markets, which are as follows. Firstly, as Adda (2016) argues that economic activity would decline and business profitability and continuity might be challenged due to the spread of contagious diseases. Furthermore, globalization and financial integration result in the rapid spread of shock from one country to others (Chen, Lee, Lin, & Chen, 2018). Additionally, panic selling, profit-taking, and the search for more safe assets during the crises are other channels (Lucey & Li, 2015). Different from the aforementioned literature, Alexakis, Eleftheriou, and Patsoulis (2021) take trade and financial channels as the transmission channels of COVID-19 to the economy.

Overall, the majority of the existing literature provides evidence for the negative impact of the COVID-19 pandemic on the global economy. However, the degree of the effects varies among different countries as well as different sectors. China is the first economy hit by COVID-19. The effects of the pandemic on Chinese stock markets deserve further in-depth analysis even though some studies paid attention to it. Furthermore, the supply chain networks are disrupted by the pandemic. But few studies discuss how China's stock market reacts to the supply chain disruptions from COVID-19. In addition, Wuhan, the provincial capital of Hubei province, reported the first COVID-19 case and is the first city to announce “lockdown”. Hubei firms are supposed to be affected first by the pandemic.

Following the previous studies, we therefore explore the effects of COVID-19 on Chinese firms. Specifically, our paper examines the effects of COVID-19 on Chinese firms, including direct effects, propagation effects (upstream, downstream, and multiple effects of supply chain disruptions), and the competitive effects. Different from the extant literature, our analysis concerns on how the supply chain disruptions from COVID-19 influence China's stock market. Secondly, the effects of COVID-19 on Hubei firms and non-Hubei firms are separately analyzed. Lastly, the effects of supply chain disruptions due to the global spread of COVID-19 are also discussed owing to the gradual worldwide spread of the pandemic.

3. Methodology

3.1. Estimating abnormal returns and statistical testing

Recently, the event study method (ESM) has been considered as a common research method in business studies (He, Sun, et al., 2020). It is especially considered as one of the most popular and applicable methods for investigating the impact of an event during an event period (Singh et al., 2020). ESM is widely used to examine the effect of a particular event on the stock prices, such as Hendricks et al. (2019), Kim, Kim, Lee, and Tang (2020), and Yong and Laing (2021). The method is based on the assumption that the stock prices change immediately in response to an event (Hendricks et al., 2019; Nicolau, 2002). Thus, ESM can evaluate the abnormal returns in the market value of a firm after a specific event occurs (He, Sun, et al., 2020; Lee & Connolly, 2010; MacKinlay, 1997). Following Hendricks et al. (2019), abnormal return is defined as the difference between the return with the event happening and the return if the event had not happened, which is the part of the actual return that can be accounted by the event. Since the outbreak of the COVID-19 pandemic, ESM has been extensively employed to examine the short-run stock market response to the pandemic (Nicola et al., 2020; Singh et al., 2020; Yan & Qian, 2020; Yong & Laing, 2021).

At present, there are three models to estimate abnormal returns, namely, the mean adjustment model, market adjustment model, and market model. When the stock values are falling or rising on the event day, there would be a large deviation for the mean adjustment model (Klein & Rosenfeld, 1987). The market-adjusted return is positively or negatively biased when the market return departs from its expectation during the event period (Binder, 1998). By contrast, the predictive power is good for the market model (Brenner, 1979). Furthermore, the market model is straightforward and relatively easy to use (Binder, 1998). Therefore, we adopt the market model to estimate the abnormal returns.

The market model is from the revised capital asset pricing model (CAPM), which assumes that there is a correlation between the systemic risk-return of individual stocks and the market return. The normal rate of return is calculated as

| (1) |

where R it is the return of stock i on Day t; R mt is the market return on Day t; α i is the intercept of the relationship for stock i; β i measures the sensitivity of stock i's return to the market return, and ε it is the error term for stock i on Day t.

Because our sample firm stocks are mostly from the A-share market, we generate R mt by using a comprehensive daily market rate of return considering reinvestment of cash dividends (weighted average method of circulating market value). The length of the estimation window is not consentient in the existing literature. Following Sun et al. (2021), the 100 days before the event date is chosen as the estimation window. That is, Ordinary Least Squares (OLS) regression over an estimation period of 100 trading days is employed to estimate and . We begin the estimation period 110 trading days prior to the event on 23 January 2020, and we end it 11 trading days prior. To estimate abnormal returns, firms must have a minimum of 40 stock returns during the 100-day estimation period. The abnormal return for firm i on Day t (AR it) is the difference between the actual and the expected return, which can be explained by the event rather than overall stock market movements (Kim et al., 2020). Therefore, AR it is given by

| (2) |

Where is the estimated expected return for firm i on Day t.

Cumulative abnormal return (CAR) of stock i in the event period (t 1 , t 2) is computed by

| (3) |

Then, we can compute the arithmetic average of ARs for all the firms on each event day to get the average (mean) abnormal returns (AAR). Thus,

| (4) |

where N represents the number of firms in the sample on Day t.

Furthermore, cumulative average abnormal return (CAAR) of stock i for the event period (t 1 , t 2) is calculated as the aggregate of daily AARs for the event window (t 1 , t 2) to examine the accumulated effects of the event during a specified time period (Singh et al., 2020). So,

| (5) |

As we estimate multiple firms' abnormal returns on the same day, cross-sectional dependence in abnormal returns across the sample firms may lead to underestimation of standard deviation and overestimation of the magnitude of the test statistics (Hendricks et al., 2019). Following Hendricks et al. (2019), the test advocated by Brown and Warner (1985) is employed to adjust for cross-sectional dependence. Thus, the test statistic for the Day t is

| (6) |

where is the estimated standard deviation from the mean daily abnormal returns for the 100-day estimation period and defined as

| (7) |

where is the estimated mean abnormal return for the 100-day estimation period and calculated as

| (8) |

Similarly, the test statistic for a j-day event period (TS j) is

| (9) |

Because there are some small subsamples, outliers may influence the mean value. Following Hendricks et al. (2019), we also analyze the median and negative (positive) percentage of abnormal returns, using Wilcoxon's signed-rank test and sign test, respectively. For these tests, we report two-tailed p-values.

3.2. Event window, sample selection, and data description

3.2.1. Event day

For event study method, it is primarily important to choose the event day. Following Kim et al. (2020), an event is taken as public recognition of an incident outbreak, an event day is thus considered as the first day when the outbreak of the event is released to the public through media. However, in order to more accurately examine the impact of COVID-19 on stock prices, it is necessary to determine the date when the outbreak and a series of epidemic prevention measures began to have a widespread impact on enterprises. On 30 December 2019, Wuhan Health Commission announced that patients with unknown pneumonia causes occurred. Although the epidemic began to appear at this time, it had a limited impact and has not affected the normal production and operation activities of the enterprises. As the epidemic situation gradually becomes tense on 23 January 2020, Wuhan, a city of Hubei province, announced the “lockdown”, with the city's transportation temporarily closed, including bus, subway, ferry, airport, railway to prevent the contagion of COVID-19. It hit the “pause” button on the economy due to the destructive impact on economic activities. So we select 23 January 2020, the date when the news was released to the public by the media and hit the economy to a stir, as the event day, namely Day 0. It is also the date selected as the event day by He, Sun, et al. (2020). The trading day following the event is denoted as Day 1, and the trading day before the event is represented by Day −1, etc.

3.2.2. Event window

According to the efficient market hypothesis, the impact of an event on shareholder value will be quickly reflected in the stock price, so it is appropriate to select one or two days after the event date as the event window. However, the severity of the COVID-19 is uncertain at the beginning of the epidemic outbreak. More information about the pandemic is gradually released in the following days. In this case, a longer event period must be considered to capture the abnormal returns related to the event (Hendricks et al., 2019). Hence, we use a 16-day event period as our main focus, that is, from the event day to the following 15 trading days. Because our 16-day event period covers about one calendar month.4 Distinct responses of the stock markets could be observed in different phases of the pandemic (Singh et al., 2020). It is necessary to examine different lengths of event window to grasp the response of market expectations from the specific event (Yan & Qian, 2020). Therefore, results for alternative event periods are also reported. Three factors are considered when choosing the window period.

Firstly, the COVID-19 pandemic is accompanied by great uncertainty, and its impact on supply chain disruptions may not be reflected in the price in time. While if the window is too long, the results could be intervened by other information.

Secondly, the stock market volatility can indicate the investors' sentiment to the event. Fig. 1 depicts the fluctuation of CSI 300 index from 15 trading days before the lockdown of Wuhan (t = −15) to 60 trading days after the event (t = 60). The CSI 300 index fluctuated significantly for the first several days following the COVID-19 outbreak.

Fig. 1.

CSI 300 index fluctuation. Data source: CSMAR database.

Lastly, the development, prevention, and control of the COVID-19 epidemic are characterized by phases. Wuhan was put on lockdown, shut down businesses, isolated people at home, and disrupted supply chains, marking hitting the “pause” button for the national economy on 23 January 2020. On 23 February of 2020, a meeting to coordinate the efforts to curb the COVID-19 outbreak and promote economic and social development was held. Chinese president Xi Jinping encouraged the nation to turn pressure into strength and adversity into opportunities, and steadily resume normal work and daily life. This meeting marked the beginning of the resumption of work and production across the country. Wuhan was lifting the lockdown on 8 April 2020, which means the resumption of work and production in most parts of China.

Therefore, we select 23 January 2020, as the event day and focus on the 16-day event period. To provide more information on the pattern of abnormal returns, we also report abnormal returns for Days (0,2) and Days (0,10) following the existing studies. Our event day is the date when Wuhan was put on lockdown. The city began to lift its lockdown on 8 April 2020. Thus, we also report the abnormal returns for the 47-day event period. Since the effects of the COVID-19 pandemic continue and the COVID-19 challenges are far from over, we will also report results over longer event periods (121-day and 181-day).

3.2.3. Sample selection

We select a sample from news reports in the China Infobank database. It is a database that collects financial information about China and related overseas businesses mainly based on media reports. The data comes from more than a thousand media companies, both from China and outside China, and leading government and enterprise organizations. We use the keyword search method to select reports about firms affected by the COVID-19. Specifically, the keywords mainly include “COVID-19 epidemic”, “epidemic impact”, “health incident”, etc. The search covers the period from1 January 2020 to 20 November 2020. By reading these articles, we determine which companies are affected by the COVID-19. To address potential bias from selecting the sample based on the reports, we additionally selected 99 companies with the largest scale in the transportation and retail industries as supplementary subsamples.

Our sample consists of 406 publicly traded firms located in China. The sample is segmented into different categories to grasp the exact effects of COVID-19. The subsamples are described in Table 1 . Furthermore, 346 negatively (including directly and indirectly) and 60 positively affected firms are separately divided into five and two sub-categories.

Table 1.

Subsample categories for the sample of 406 publicly-traded firms affected by COVID-19.

| All firms |

Hubei firms |

Non-Hubei firms |

|||||

|---|---|---|---|---|---|---|---|

| Category | Description | Frequency | % of sample | Frequency | % of sample | Frequency | % of sample |

| Potential negative effects | |||||||

| Supply chain disruption | |||||||

| Direct | Operations directly affected | 99 | 29.2 | 41 | 41.4 | 58 | 58.6 |

| Downstream | Effects from suppliers | 42 | 12.4 | 1 | 2.4 | 41 | 97.6 |

| Upstream | Effects from customers | 152 | 45 | 23 | 15.1 | 129 | 84.9 |

| Multiple | Effects from suppliers and customers | 46 | 14 | 10 | 21.7 | 36 | 78.3 |

| Supply chain disruptions subtotals | 339 | 100 | 75 | 22.1 | 264 | 77.9 | |

| Other negative effects | |||||||

| Insurance | Insurance industry | 7 | 100 | 0 | 0 | 7 | 100 |

| Negative effect subtotals | 346 | 100 | 75 | 21.7 | 371 | 78.3 | |

| Potential positive effects | |||||||

| Competitors | Direct competitors affected | 30 | 50 | 2 | 6.6 | 28 | 93.3 |

| Medical | Medical | 30 | 50 | 0 | 0 | 30 | 100 |

| Positive effect subtotals | 60 | 100 | 2 | 3.3 | 58 | 96.7 | |

| Total | 406 | 100 | 77 | 19 | 329 | 81 | |

Direct (99 firms): Firms that are directly affected by COVID-19, resulting in the interruption of production or service.

Downstream (42 firms): Firms whose operations are not directly affected by COVID-19, but indirectly affected by downstream infection from the suppliers affected by the epidemic.

Upstream (152 firms): Firms whose operations are not directly affected by the epidemic, but are indirectly affected by the upstream infection of their consumers affected by COVID-19.

Multiple (46 firms): Firms that are not directly influenced by COVID-19 but instead indirectly affected by both upstream and downstream propagation effects from their consumers and suppliers. Nowadays, as the supply chain becomes more and more complex and the enterprise relationship becomes closer and closer, firms are not only affected by the one-way supply chain but also affected by both the upstream and downstream impacts of some customers and suppliers.

This paper uses the abovementioned four subsamples to get an in-depth understanding of the impact of COVID-19 on supply chain disruptions.

Insurance (7 firms): They are mainly insurance companies, reinsurance companies, and life insurance companies. COVID-19 has a great threat to the safety of people's lives, and the production and operation activities of enterprises. In the short term, an insurance company must pay for claims related to property loss, loss of life, interruption of business, and discontinuities, and thus suffers a negative impact.

Medical (30 firms): Firms whose products or services are used to prevent damage caused by COVID-19. The sample is mainly the medical industry.

Competitors (30 firms): Firms that benefit from COVID-19 due to the negative impact of their competitors from COVID-19. For example, the suspension of offline entertainment provides opportunities for the development of online entertainment.

Transportation and retail (99 firms): This sample includes the top 70 firms from the transportation and retail industry.

In addition, Hubei firms5 are separated from non-Hubei firms in each sub-category as shown in Table 1. 41 of the 77 Hubei firms are in the “direct” category, that is, more than half of Hubei firms are directly influenced by COVID-19, which is as expected. Since Wuhan, the provincial capital city of Hubei province in China is the first city to declare lockdown and quarantine to prevent the spread of the pandemic, which directly affect the operations of Hubei firms. Non-Hubei firms make up the majority of the rest six categories.

Information on the firm's place of incorporation is from the WIND database. The data on firms' daily return of individual stocks and daily return of markets are obtained from the CSMAR database.

4. Empirical findings

4.1. Abnormal returns for the full sample

Table 2 presents the results of the stock market reaction to the COVID-19 for the full sample. Panel A provides evidence for the negative effect of COVID-19 on firms. For Days (0, 2), the mean and median CARs are separately −0.42% and − 2.85%, significant at the 10% and 1% level, respectively. The percentage of samples with negative abnormal returns is 62.07%, significant at the 1% level. The results indicate that the COVID-19 had an immediate negative effect on the sample firms. For Days (0,10), the mean and median CARs are −0.08% (not significant) and − 1.74% (significant at the 1% level), respectively. Over 59% of firms experience negative returns, significate at the 1% level. The mean CAR for Days (0, 15) is 0.87%, significant at the 10% level, different from that of the Days (0, 10). The median CAR for Days (0, 15) is −1.18%, with a magnitude lower than that for Days (0, 10), but also significant at the 1% level. More than 55% of the firms experience negative returns, significant at the 5% level. The mean (median) CAR for Days (0, 46) is 2.66% (1.89%), but not significant (significant at the 1% level). With less than 50% of the firms experience negative returns, but not significant. Our results are consistent with Topcu and Gulal (2020), who find a gradually falling and tapering off negative impact of the pandemic by mid-April of 2020. When we consider a longer period, the mean CARs for Days (0,120) and Days (0, 180) are negative, but not significant. However, the median CARs for the two periods are separately −2.07% and 1.64%, both significant at the 1% level.

Table 2.

Cumulative abnormal returns for the sample of publicly-traded firms affected by COVID-19.

| Panel A: Total sample | |||||||

|---|---|---|---|---|---|---|---|

| Days | N | Mean (%) | T | Median (%) | Z1 | % negative | Z2 |

| [0,2] | 406 | −0.42 | −1.87* | −2.85 | −3.63*** | 62.07 | −4.81*** |

| [0,10] | 406 | −0.08 | −0.21 | −1.74 | −4.89*** | 59.36 | −3.72*** |

| [0, 15] | 406 | 0.87 | 1.94* | −1.18 | −4.16*** | 55.17 | −2.04** |

| [0, 46] | 406 | 2.66 | 1.43 | 1.89 | −6.82*** | 47.04 | −1.14 |

| [0,120] | 406 | −0.32 | −0.03 | −2.07 | −17.09*** | 53.20 | −1.24 |

| [0, 180] | 406 | −1.35 | −0.06 | 1.64 | −19.96*** | 48.28 | −0.65 |

| Panel B: Negative effect sample | |||||||

| Days | N | Mean (%) | T | Median (%) | Z1 | % negative | Z2 |

| [0, 2] | 346 | −2.45 | −10.11*** | −3.83 | −6.91*** | 69.36 | −7.15*** |

| [0, 10] | 346 | −1.65 | −4.16*** | −2.97 | −5.86*** | 65.61 | −5.75*** |

| [0, 15] | 346 | −0.33 | −0.70 | −1.73 | −4.49*** | 59.83 | −3.60*** |

| [0, 46] | 346 | −0.21 | −0.11 | −0.64 | −8.00*** | 51.16 | −0.38 |

| [0, 120] | 346 | −4.28 | −0.38 | −4.39 | −17.58*** | 58.09 | −2.96*** |

| [0, 180] | 346 | −5.03 | −0.20 | −1.07 | −20.22*** | 51.73 | −0.59 |

| Panel C: Supply chain disruption sample | |||||||

| Days | N | Mean (%) | T | Median (%) | Z1 | % negative | Z2 |

| [0, 2] | 339 | −2.54 | −10.33*** | −3.89 | −7.12*** | 70.21 | −7.39*** |

| [0, 10] | 339 | −1.64 | −4.06*** | −2.87 | −5.72*** | 65.78 | −5.76*** |

| [0, 15] | 339 | −0.30 | −0.61 | −1.72 | −4.36*** | 59.29 | −3.37*** |

| [0, 46] | 339 | −0.12 | −0.06 | −0.60 | −7.82*** | 51.03 | −0.33 |

| [0, 120] | 339 | −4.38 | −0.38 | −4.47 | −17.51*** | 58.11 | −2.93*** |

| [0, 180] | 339 | −5.31 | −0.21 | −1.32 | −20.29*** | 52.51 | −0.87 |

Notes: 1. All tests are two-tailed: *** p < 0.01; ** p < 0.05; * p < 0.10.

2. Z1-statistics for medians are obtained using Wilcoxon signed-rank tests.

3. Z2-statistics for % negatives are obtained using binomial sign tests.

The results indicate that the stock market immediately reacts to the outbreak of COVID-19. And the pandemic has an adverse effect on the economy. It may be possible because of the limited information about the nature of COVID-19 and the effective containment measures until the lockdown of Wuhan (Khatatbeh et al., 2020). Financial markets reflect economic expectations (Alexakis et al., 2021). Thus, great uncertainty rises following the unprecedented pandemic, which permeates every aspect of life and business ( Szczygielski, Charteris, Bwanya, & Brzeszczynski, 2022), and leads to the increasing pessimistic sentiment of investors. It is known that the China's stock market was closed during 24 January to 2 February 2020. It jumped downwards significantly on the first trading day after the COVID-19 outbreak as the stock market was closed for a longer period than usual, and the reopening of the market on 3 February 2020 was seen as risky, which leads to the overreactions of stocks (Huo & Qiu, 2020). On the other hand, the market would correct itself with time as more information about COVID-19 becomes available (Phan & Narayan, 2020). Furthermore, the government of China takes measures and policies to respond to the pandemic. First, early lockdown/restrictions improve the confidence of the stock market (Pandey & Kumari, 2021). Second, a meeting to coordinate efforts to curb the COVID-19 outbreak and promote economic and social development was held on 23 February 2020, one month after the outbreak of COVID-19. China gradually started to resume its economic and activities, and investors rebuilt their confidence. But it was not the end of the pandemic, however, it spread globally and was declared as the global pandemic in the mid-March of 2020. Even though Chinese stock markets are more comfortable with the pandemic, the effects of COVID-19 last.

4.2. Abnormal returns for the negatively-affected firms

Table 1 shows that there are 346 firms affected negatively by the COVID-19. Because insurers have to pay claims for life, travel cancellation, and letter of credit related to international trade. In addition, insurance firms belong to the financial industry. So we divide the subsample into insurance and one that would experience supply chain disruptions in the conventional sense.

Panel B of Table 2 shows that COVID-19 has an enormous instant negative effect on the sample firms, which is implied by the significant negative mean and median CARs for Days (0, 2) and Days (0, 10). Additionally, over 65% of the sample firms experience negative returns, significant at the 1% level. For the remaining event periods, the mean CARs are negative but not statistically significant, while the median CARs are significantly negative at the 1% level. It is worth noting that more than 50% of the sample firms experience significant negative returns for Days (0, 15) and Days (0, 120). The results could be due to the influence of the COVID-19 outbreak in different countries around the world.

The results for the firms that reported supply chain disruptions are presented in Panel C of Table 2. The CARs for different event periods are not substantively different from that for the negative effect subsample. That is, the firms that reported supply chain disruptions immediately react to the outbreak of COVID-19.

To further investigate the stock market reaction to COVID-19, the subsamples are divided into Hubei firms and non-Hubei firms. The results are reported in Table 3 . As shown in Panel A, the mean and median CARs for Days (0, 2) for Hubei firms are −4.97% and − 4.50%, respectively, both significant at the 1% level. Over 78% of Hubei firms experience negative returns, also significant at the 1% level. As the window expanded to (0, 10), the negative impact of COVID-19 on Hubei firms falls in magnitude, with the mean (median) declining to −2.55% (−3.21%). In addition, more than 65% of sample firms experience negative returns, significant at the 5% level. For Days (0, 15), the mean and median CARs are −0.63% and − 1.47%, respectively, both are not significant. About 58% of Hubei firms experience negative returns, but insignificant. For Days (0, 46), the mean CAR is 3.20%, but not significant. The median CAR is reversed to positive, that is 3.35%, significant at the 5% level. For the following two event periods, the mean CARs sustain insignificant signs. The median CARs for Days (0, 120) and Days (0, 180) are −1.57% and − 2.95%, respectively, both significant at the 1% level. More than 50% of Hubei firms experience negative returns, but not significant. The results provide evidence for the fact that Hubei firms are immediately hit by COVID-19. With various policies taken and the gradual resumption of work and economic production, the negative effects of the pandemic appear to subside. However, the global spread of COVID-19 negatively affects Hubei firms again, although the effects are lower than that when Wuhan was the epicenter.

Table 3.

Cumulative abnormal returns for the sample of Hubei and non-Hubei firms.

| Panel A: Sample of Hubei firms | |||||||

|---|---|---|---|---|---|---|---|

| Days | N | Mean (%) | T | Median (%) | Z1 | % negative | Z2 |

| [0, 2] | 75 | −4.97 | −9.67*** | −4.50 | −5.27*** | 78.67 | −4.85*** |

| [0, 10] | 75 | −2.55 | −3.04*** | −3.21 | −2.46** | 65.33 | −2.54** |

| [0, 15] | 75 | −0.63 | −0.62 | −1.47 | −1.54 | 58.67 | −1.39 |

| [0, 46] | 75 | 3.20 | 0.76 | 3.35 | −2.08** | 44.00 | −0.92 |

| [0, 120] | 75 | −3.56 | −0.10 | −1.57 | −8.82*** | 52.00 | −0.23 |

| [0, 180] | 75 | −9.26 | −0.17 | −2.95 | −10.58*** | 52.00 | −0.23 |

| Panel B: Sample of non-Hubei firms | |||||||

| Days | N | Mean (%) | T | Median (%) | Z1 | % negative | Z2 |

| [0, 2] | 264 | −1.85 | −6.60*** | −3.34 | −5.22*** | 67.80 | −5.72*** |

| [0, 10] | 264 | −1.37 | −2.99*** | −2.87 | −5.20*** | 65.91 | −5.11*** |

| [0, 15] | 264 | −0.21 | −0.37 | −1.79 | −4.14*** | 59.47 | −3.02*** |

| [0, 46] | 264 | −1.06 | −0.46 | −1.69 | −7.77*** | 53.03 | −0.92 |

| [0, 120] | 264 | −3.55 | −0.27 | −4.29 | −14.94*** | 57.58 | −2.40** |

| [0, 180] | 264 | −4.18 | −0.14 | −1.27 | −17.35*** | 52.65 | −0.80 |

Notes: 1. All tests are two-tailed: *** p < 0.01; ** p < 0.05; * p < 0.10.

2. Z1-statistics for medians are obtained using Wilcoxon signed-rank tests.

3. Z2-statistics for % negatives are obtained using binomial sign tests.

In terms of the non-Hubei firms, Panel B of Table 3 presents that the mean (median) CAR for Days (0, 2) is −1.85% (−3.34%), significant at the 1% level. Over 67% of firms experience negative abnormal returns, significantly greater than 50% at the 1% level. The CAR for Days (0, 10) is not substantively different from that for Days (0, 2). For the remaining event periods, the mean CARs are not significant, while the median CARs are significantly negative at the 1% level. Furthermore, the magnitude of median CARs has gradually become lower until the Days (0, 46). However, the magnitude of median CARs reaches a peak for the Days (0, 120) among our considered event periods, which could be attributable to the global spread of the pandemic.

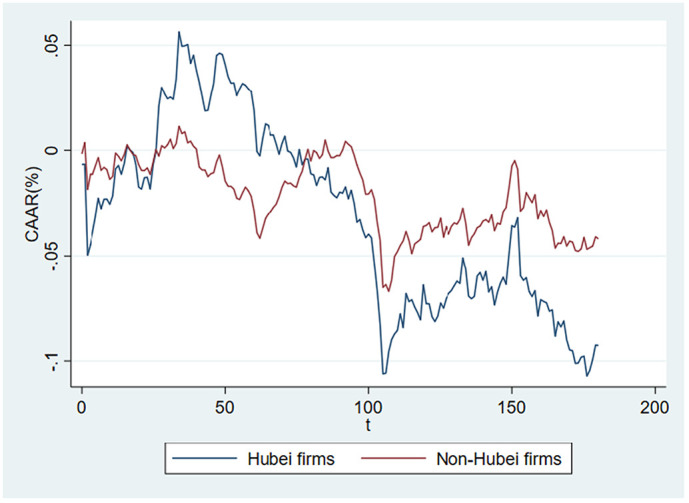

The abovementioned results imply that both Hubei and non-Hubei firms are immediately negatively affected by COVID-19. The negative effects gradually decrease before the global spread of the pandemic, while all the firms are shocked again when COVID-19 spread globally. Nonetheless, the negative effects on Hubei firms are especially stronger than thoes on non-Hubei firms in the early stage of the pandemic. The results are also demonstrated in Fig. 2 . It may be explained by the fact that Hubei, as the epicenter at that time, firstly implemented lockdown measures. The markets did not prepare for the unexpected pandemic, which completely halted economic activities. But the epidemic situation outside Hubei province is not as severe as that in Hubei province. Some economic and production activities of non-Hubei firms can still be carried out at the onset of COVID-19 outbreak. With the spread of the pandemic, more information is known about the epidemic. Moreover, the government implements a series of macroeconomic policies to resume the economic and production activities.

Fig. 2.

The fluctuation of mean CARs for Hubei and non-Hubei firms.

4.3. Propagation effects of supply chain disruptions

Consumer demand for products and services has declined sharply and both national and international production and service supply chains have been suspended due to the lockdowns in response to COVID-19 (De Vito & Gómez, 2020). As one of the most important economies in the world, China's supply chains has been adversely lashed by the pandemic. To explore the contagion effects of supply chain disruption, we divide the sample into four subsamples: direct, upstream, downstream, and multiple effects. Panel A of Table 4 reports the results of the subsample whose operation is directly affected by COVID-19. The mean and median CARs for Days (0, 2) are −3.06% and − 3.91%, respectively, significant at the 1% level. Over 73% of firms experience negative abnormal returns, significant at the 1% level. The mean and median CARs for Days (0, 10) are separately −1.94% and − 3.37%, significant at the 5% and 1% levels, respectively. Over the 16 days from the date of the event to the 15th day of the event, the mean and median stock market reaction are separetely −0.32% (not significant) and − 1.47% (significant at the 5% level). During this event period, more than 56% of the sample firms experience negative abnormal returns, but not significant. The mean and median CARs for Days (0, 46) are reversed to be positive, namely 1.95% (not significant) and 4.00% (significant at the 1% level), respectively. Only 44.44% of the firms experience a negative reaction, but not significant. In the following two event period, the mean CARs become negative again, and the proportion of firms experiencing negative abnormal returns is about 50%, but both are not significant. The median CARs for Days (0, 120) and Days (0, 180) are −1.16% and 0.03%, respectively, significant at the 1% level. In addition, the fluctuation of mean CARs of the directly affected firms is shown in the upper left panel of Fig. 3 . The negative influence of COVID-19 gradually subsides before lifting the lockdown of Wuhan, which could reflect the effectiveness of Chinese efforts to fight against the epidemic.

Table 4.

Cumulative abnormal returns for firms directly and indirectly affected by COVID-19.

| Panel A: Directly affected | |||||||

|---|---|---|---|---|---|---|---|

| Days | N | Mean (%) | T | Median (%) | Z1 | % negative | Z2 |

| [0, 2] | 99 | −3.06 | −6.55*** | −3.91 | −4.13*** | 73.74 | −4.62*** |

| [0, 10] | 99 | −1.94 | −2.54** | −3.37 | −3.19*** | 67.68 | −3.42*** |

| [0, 15] | 99 | −0.32 | −0.35 | −1.47 | −2.13** | 56.57 | −1.21 |

| [0, 46] | 99 | 1.95 | 0.51 | 4.00 | −2.79*** | 44.44 | −1.01 |

| [0, 120] | 99 | −4.26 | −0.20 | −1.16 | −8.67*** | 50.51 | 0.00 |

| [0, 180] | 99 | −8.12 | −0.17 | 0.03 | −10.82*** | 49.49 | 0.00 |

| Panel B: Downstream (Effects from suppliers) | |||||||

| Days | N | Mean (%) | T | Median (%) | Z1 | % negative | Z2 |

| [0, 2] | 42 | −1.92 | −2.66*** | −2.24 | −1.61 | 64.29 | −1.70* |

| [0, 10] | 42 | −0.16 | −0.14 | −2.11 | −1.08 | 57.14 | −0.77 |

| [0, 15] | 42 | 4.48 | 3.13*** | 0.68 | 0.45 | 42.86 | −0.77 |

| [0, 46] | 42 | 0.80 | 0.14 | 1.35 | −3.50*** | 47.62 | −0.15 |

| [0, 120] | 42 | −10.53 | −0.31 | −10.95 | −8.89*** | 69.05 | −2.31** |

| [0, 180] | 42 | −11.18 | −0.15 | −8.60 | −9.45 | 69.05 | −2.31** |

| Panel C: Upstream (Effects from customers) | |||||||

| Days | N | Mean (%) | T | Median (%) | Z1 | % negative | Z2 |

| [0, 2] | 152 | −2.67 | −7.56*** | −4.17 | −5.48*** | 71.05 | −5.11*** |

| [0, 10] | 152 | −2.46 | −4.25*** | −3.59 | −5.10*** | 69.08 | −4.62*** |

| [0, 15] | 152 | −2.40 | −3.43*** | −3.68 | −5.39*** | 69.74 | −4.79*** |

| [0, 46] | 152 | −2.43 | −0.84 | −3.32 | −6.57*** | 58.55 | −2.03** |

| [0, 120] | 152 | −3.29 | −0.20 | −4.39 | −11.14*** | 59.87 | −2.35** |

| [0, 180] | 152 | 3.98 | −0.11 | −0.42 | −13.03*** | 50.66 | −0.08 |

| Panel D: Multiple effects | |||||||

| Days | N | Mean (%) | T | Median (%) | Z1 | % negative | Z2 |

| [0, 2] | 46 | −1.57 | −2.22** | −3.35 | −1.78* | 65.22 | −1.92* |

| [0, 10] | 46 | 0.40 | 0.35 | −2.58 | −0.73 | 58.70 | −1.03 |

| [0, 15] | 46 | 2.23 | 1.65 | 1.06 | 0.30 | 45.65 | −0.44 |

| [0, 46] | 46 | 2.20 | 0.38 | 2.76 | −1.88* | 43.48 | −0.74 |

| [0, 120] | 46 | −2.60 | −0.08 | −5.54 | −6.13*** | 58.70 | −1.03 |

| [0, 180] | 46 | 1.73 | 0.02 | −0.41 | −6.51*** | 50.00 | 0 |

Notes: 1. All tests are two-tailed: *** p < 0.01; ** p < 0.05; * p < 0.10.

2. Z1-statistics for medians are obtained using Wilcoxon signed-rank tests.

3. Z2-statistics for % negatives are obtained using binomial sign tests.

Fig. 3.

The fluctuation of mean CARs for directly and indirectly affected firms.

The results of the subsample of firms whose upstream suppliers have been hit by COVID-19 are given in Panel B of Table 4. The results measure the extent to which upstream suppliers have impacted their customers. The average abnormal return is significantly negative in the first two following trading days. But the CARs become insignificant for Days (0, 10). It may be because the market did not have sufficient information on which customers were affected on account of the effects from their suppliers. For Days (0, 15), the mean (median) CAR is 4.48% (0.68%), which is significant at the level of 1% (not significant). During this period, less than 50% of the sample firms experience negative abnormal returns, but not significant. The mean and median CARs for Days (0, 46) are separately 0.80% (not significant) and 1.35% (significant at the 1% level), less than 50% of the sample firms experience negative abnormal returns, but not significant. When expanding the event period, the mean CARs for Days (0, 120) and Days (0, 180) are −10.53% and − 11.18%, respectively, but not significant. For Days (0, 120), the median CAR is negative and statistically significant. Over 69% of firms experience negative abnormal returns, significantly greater than 50% at the 5% level. The upper right panel of Fig. 3 depicts the trend of mean CARs of downstream firms. At the onset of COVID-19 outbreak, the supply of products, goods and services, labors is affected by COVID-19 (Samitas et al., 2022), which hit the unprepared downstream firms. However, downstream firms usually hold some inventory for operations. The negative effect for downstream firms does not last after Day 2 and the reversed effect persists until Day 46.

To further investigate the size of downstream transmission effects of COVID-19, we compare the results in Panel B with those of other relevant studies. Carvalho, Nirei, Saito, and Tahbaz-Salehi (2020) compare the post-earthquake sales growth rates of firms at different distances,6 from the disaster-area firms to a control group of firms that are relatively more distant. They find that the disaster results in a 3.6% decline in the growth rate of firms with disaster-hit suppliers. Barrot and Sauvagnat (2016) study the reaction of stock markets to US-based suppliers and their business customers who have suffered natural disasters. The results show that the customer's average CAR during the (−10, 40) period is −1.13%. Hertzel, Li, Officer, and Rodgers (2008) argue that the average stock market response to a corporate client filing for bankruptcy was −0.19%. Aktas, de Bodt, and Derbaix (2003) assess the effects of horizontal mergers on the suppliers and customers and finds that the CAAR is −0.79% (insignificant) for the customers with a p-value of 0.25 at the end of the 5 days. Therefore, we can observe that the effect of COVID-19 on customers is greater than an earthquake, natural disasters, bankruptcy, and horizontal mergers.

Panel C of Table 4 reports the results for firms whose downstream customers were impacted by COVID-19, which measure the propagation effects of downstream customers on the firms. The mean CARs are displayed in the lower left panel of Fig. 3. The CARs are significantly negative for the first three event periods. The mean and median CARs for Days (0, 2) are −2.67% and − 4.17%, respectively, both are significant at the level of 1%. More than 70% of the sample firms experience negative abnormal returns, significantly greater than 50% at the level of 1%. For Days (0, 10), the average stock market reaction is −2.46%, significant at the 1% level. Meanwhile, more than 69% of the sample firms experience negative abnormal returns, significant at the level of 1%. For Days (0, 15), the mean (median) CAR is −2.40% (−3.68%), with both the mean and median CARs being significant at the 1% level. Over 69% of firms experience negative abnormal returns, also significant at the 1% level. We do not observe statistically significant mean CARs for the following three event periods, while the median CARs are separately −3.32%, −4.39%, and − _0.42%, all significant at the 1% level. Over 50% of the sample firms experience significantly negative abnormal returns except for the Days (0, 180). The results suggest that the customers might gradually recover from the effect of COVID-19, even if they are affected again by the continued spread of the pandemic. It could be because of the suspension of economic activities at the beginning of the pandemic. Upstream firms hold lots of products, but have few customers. Since the businesses and household incomes decrease due to the pandemic (Samitas et al., 2022), hence the falling purchasing power. To boost the consumption, China's local governments formulated a package of measures. For instance, a total of 11.5 billion yuan worth of consumption coupons had been issued in 25 provinces and municipalities, with 13 of them granting vouchers worth more than 100 million yuan each by 26 April 2020.7

To provide a perspective on the extent of the upstream contagion effect of COVID-19, we compare the results in Panel C with existing studies documenting the upstream transmission effect. Hertzel et al. (2008) find that the average stock market response to suppliers of companies that filed for bankruptcy is −1.96%. Aktas et al. (2003) suggest that the CAAR is −0.19% for the suppliers with a p-value of 0.17 at the end of the 5 days period, but it is not significant. Funke, Gebken, Johanning, and Michel (2010) show that supplier 20-day CARs are statistically significant positive 0.57% after large positive events and that are statistically significant negative 0.37% after large negative events. Carvalho et al. (2020) compare the post-earthquake sales growth rates of firms at different distances and find that the disaster resulted in a 2.9% decline in the growth rate of firms with disaster-hit suppliers. The results imply that the upstream contagion effect of the COVID-19 epidemic is greater than that of bankruptcy, horizontal merger, and bad earnings news, but it is slightly less than the Japanese earthquake shown in Carvalho et al. (2020). We attribute it to the difference in nature and incidence of the events.

The supply chain of firms is getting closer and closer at present. After the outbreak of the COVID-19, some enterprises have been affected both upstream and downstream simultaneously. Panel D of Table 4 shows the results for those firms.

The mean and median CARs for Days (0, 2) are separately −1.57% (significant at the 5% level) and − 3.35% (significant at the 10% level). Over 65% of the firms experience negative abnormal returns during this 3-day period, significantly greater than 50% at the 10% level. The results indicate the negative immediate stock market reaction to COVID-19. The mean CAR for Days (0, 10) is slightly positive, but not significant. The mean and median CARs for Days (0, 15) are 2.23% and 1.06%, respectively, both are not significant. Over 45% of the firms experience negative abnormal returns, but not significant. Similar to the results for downstream and upstream affected firms, the mean CARs for Days (0, 46), Days (0, 120) and Days (0, 180) are not statistically significant. But the median CARs are statistically positive for Days (0, 46) (2.76%) and statistically negative for Days (0, 120) and Days (0, 180) (−5.54% and − 0.41%, respectively). The fluctuation of mean CARs is demonstrated in the lower right panel of Fig. 3.

4.4. Comparison with GEJE

Hendricks et al. (2019) empirically estimate the effect of the 2011 Great East Japan Earthquake (GEJE) on the stock prices of 470 companies. They find that supply chain disruptions from GEJE make firms lose 5.21% of their shareholder value within one month. The effect for Japanese firms is more severe than that for non-Japanese firms. They also observe that the effects of GEJE for supply chain propagation are negative. Given that both the GEJE and COVID-19 are unpredictable and have had a huge impact on the stock prices and supply chains of firms, we compare our results with Hendricks et al. (2019) to better understand the impact of the COVID-19 epidemic on the supply chain.

Table 5 illustrates the difference in the 16-day CARs for the supply chain disruptions in our sample (columns (1)–(4)) and 21-day CARs for the supply chain disruptions in GEJE sample (columns (5)–(8)).8 Column (9) shows that the CARs for supply chain disruptions from COVID-19 are less statistically significant and less negative than those for GEJE except the downstream subsample.

Table 5.

Comparison of the results from COVID-19 with that from GEJE.

| Supply chain disruption from COVID-19 | Supply chain disruption from GEJE | Difference | |||||||

|---|---|---|---|---|---|---|---|---|---|

| Subsample | N (1) |

Mean (%) | Median (%) | % negative | N (5) |

Mean (%) | Median (%) | % negative | Mean (%) |

| (Z1) (2) |

(Z2) (3) |

(Z3) (4) |

(Z1) (6) |

(Z2) (7) |

(Z3) (8) |

(Z4) (9) |

|||

| All disruption sample | 339 | −0.30 | −1.72 | 59.29 | 284 | −5.21 | −4.47 | 77.11 | 4.91 |

| (−0.61) | (−4.36)*** | (−3.37)*** | (−5.68)*** | (−9.78)*** | (9.14)*** | (9.27)*** | |||

| Hubei/Japanese firms | 75 | −0.63 | −1.47 | 58.67 | 75 | −9.32 | −7.34 | 93.33 | 8.69 |

| (−0.62) | (−1.54) | (−1.39) | (−6.95)*** | (−6.68)*** | (7.51)*** | (9.77)*** | |||

| non-Hubei/Japanese firms | 264 | −0.21 | −1.79 | 59.47 | 209 | −3.37 | −2.93 | 71.29 | 3.16 |

| (−0.37) | (−4.14)*** | (−3.02)*** | (−3.23)*** | (−7.05)*** | (6.16)*** | (4.94)*** | |||

| Direct | 99 | −0.32 | −1.47 | 56.57 | 97 | −7.19 | −5.49 | 81.44 | 6.87 |

| (−0.35) | (−2.13)** | (−1.21) | (−6.79)*** | (−6.76)*** | (6.19)*** | (8.94)*** | |||

| Downstream | 42 | 4.48 | 0.68 | 42.86 | 72 | −3.06 | −2.59 | 73.61 | 7.54 |

| (3.31)*** | (0.45) | (−0.77) | (−2.10)*** | (−4.27)*** | (4.01)*** | (4.97)*** | |||

| Upstream | 152 | −2.40 | −3.68 | 69.74 | 113 | −4.97 | −4.44 | 76.11 | 2.57 |

| (−3.43)*** | (−5.39)*** | (−4.79)*** | (−3.57)*** | (−5.77)*** | (5.55)*** | (3.72)*** | |||

Notes: 1. All tests are two-tailed: *** p < 0.01; ** p < 0.05; * p < 0.10.

2. Z1-statistics for means are obtained using t-tests.

3. Z2-statistics for medians are obtained using Wilcoxon signed-rank tests.

4. Z3-statistics for % negatives are obtained using binomial sign tests.

5. Z4-statistics for mean difference are obtained using two-sample t-tests.

6. Difference is “the mean of COVID-19 – the mean of GEJE”, and the GEJE results (columns (5)-(8)) come from Hendricks et al. (2019).

The possible explanations could be as follows. First, after the outbreak of the COVID-19, the Chinese government quickly took measures to fight against the epidemic spread, which had greatly enhanced investors' confidence in the stock market. Thus, the impact on the supply chain was limited. Second, the occurrence of both earthquake and COVID-19 are unpredictable, but the earthquake is more destructive than COVID-19. Last but not least, the earthquake is uncontrollable and has a severe one-time impact on the economy. In contrast, COVID-19 is controllable and it takes a certain time to spread.

4.5. Abnormal returns for the transportation and retail firms

Since our samples are selected from news reports, we may ignore the firms that do not make their voices heard in the media. When COVID-19 broke out, China quickly took quarantine measures to prevent its spread. The first industry hit was transportation and the subsequent collapse in demand has taken a toll on the retail sector. Therefore, we add firms of transportation and retail industries to subsamples additionally.

Panel A of Table 6 reports the results for transportation firms. The mean and median CARs for Days (0, 2) are −5.20% and − 5.37%, respectively, both are significant at the 1% level. Over 90% of sample firms experience negative abnormal returns, significantly greater than 50% at the 1% level. For Days (0, 10), the magnitude of the negative reaction of the stock market to the pandemic is increasing. The mean and median of the abnormal returns are separately −6.66% and − 7.00%, both significant at the 1% level. More than 95% of firms experience negative abnormal returns during this period, significant at the 1% level. The mean and median CARs for Days (0, 15) are very similar to those for Days (0, 10). In the following three event periods, we do not find a significant mean CAR. But for the last two event periods, the median CARs are statistically significantly negative, namely, −5.25%, and − 4.39%, respectively. At least 50% of firms experience negative abnormal returns, but not significant. The results provide evidence for the fact that the transportation industry is severely hit by COVID-19, especially in the first month after the lockdown of Wuhan. It could be explained by the fact that transportation is the first industry to be hit when China takes quarantine measures to prevent the spread of the epidemic (He, Sun, et al., 2020). With the global spread of the pandemic, travel restrictions are imposed by many other countries, which leads to persistent influence. It is estimated that 96% of all worldwide destinations have introduced travel restrictions in the early April of 2020 in response to the COVID-19 pandemic.9 As of mid-May 2020, 100% of all destinations worldwide continue to have some form of COVID-19-related travel restrictions in place.10 There are 59 destinations that have kept their borders closed to tourists as of 1 November 2020, a decrease of 34 over the same two-month period.11

Table 6.

Cumulative abnormal returns for transportation and retail sample.

| Panel A: Transportation | |||||||

|---|---|---|---|---|---|---|---|

| Days | N | Mean (%) | T | Median (%) | Z1 | % negative | Z2 |

| [0, 2] | 44 | −5.20 | −11.01*** | −5.37 | −5.20*** | 90.91 | −5.28*** |

| [0, 10] | 44 | −6.66 | −8.61*** | −7.00 | −6.70*** | 95.45 | −5.88*** |

| [0, 15] | 44 | −5.70 | −6.08*** | −6.13 | −6.08*** | 90.91 | −5.28*** |

| [0, 46] | 44 | −2.32 | −0.60 | −0.76 | −0.60 | 59.10 | −1.06 |

| [0, 120] | 44 | 3.98 | 0.12 | −5.25 | −5.43*** | 54.55 | −0.45 |

| [0, 180] | 44 | 1.95 | 0.04 | −4.39 | −6.02*** | 56.82 | −0.75 |

| Panel B: Retail | |||||||

| Days | N | Mean (%) | T | Median (%) | Z1 | % negative | Z2 |

| [0, 2] | 55 | −5.02 | −9.88*** | −4.88 | −5.85*** | 85.45 | −5.12*** |

| [0, 10] | 55 | −6.15 | −7.39*** | −6.11 | −7.41*** | 89.09 | −5.66*** |

| [0, 15] | 55 | −5.07 | −5.02*** | −5.73 | −6.10*** | 85.46 | −5.12*** |

| [0, 46] | 55 | 5.18 | 1.25 | 2.30 | −1.34 | 40.00 | −1.35* |

| [0, 120] | 55 | 8.17 | 0.35 | 4.59 | −4.21*** | 36.36 | −1.89* |

| [0, 180] | 55 | 4.57 | 0.09 | 6.68 | −6.95*** | 38.18 | −1.62 |

Notes: 1. All tests are two-tailed: *** p < 0.01; ** p < 0.05; * p < 0.10.

2. Z1-statistics for medians are obtained using Wilcoxon signed-rank tests.

3. Z2-statistics for % negatives are obtained using binomial sign tests.

Considering retail firms, Panel B of Table 6 reports that the mean and median CARs for Days (0, 2) are −5.02% and − 4.88%, respectively, both significant at the 1% level. Over 85% of sample firms experience negative abnormal returns, significantly greater than 50% at the 1% level. For Days (0, 10) and Days (0, 15), the CARs are not substantively different from that for Days (0, 2). For Days (0, 46), the mean and median CARs are not significant. Only about 40% of retail firms experience negative abnormal returns, marginally significantly less than 50%. For Days (0, 120) and Days (0, 180), the insignificant mean CARs are persisted, while the median CARs become significantly positive. The possible explanations could be as follows. The actions, such as home quarantines and lockdowns, taken to curb the spread of COVID-19 lead to the slump of consumer demand for products and services (De Vito & Gómez, 2020). That is, the retail industry is enormously shocked by the home quarantine measures due to the unpredictable outbreak of COVID-19 in the early stage of the epidemic. When the economic production and activities gradually resume, the retail industry starts to recover. In addition, COVID-19 speeds up the transformation of consumers' way of shopping. In the first quarter of 2020, 23.6% of China's total consumer product consumption are the products sold online, 5.4 percentage points higher from the same period of 2019.12

4.6. Stock market reaction for the insurance firms

There are only seven listed insurance firms in China. Due to the small number of firms in the sample, the median is more appropriate than the mean. The results are reported in Table 7 . For days (0, 2), the median CAR is significantly greater than 0. The positive median CAR is reversed for Days (0, 10), but not significant. For Days (0, 15), the insignificant negative median CAR is persistent. The magnitude of median CAR declines to −2.02% for Days (0, 46), significant at the 10% level. In the following two event periods, median CARs are not significant. The results suggest a delayed negative effect of COVID-19 on insurance firms. But the effects appear to subside after Day 46. The reasons are as follows. On the one hand, the insurance companies pay for the claims incurred by COVID-19. Since protecting people from risks is the fundamental function of insurance (Wang, Zhang, Wang, & Fu, 2020). On the other hand, declined household income and increased unemployment rate resulting from the unprecedented outbreak of COVID-19 leads to limited purchase power to insurance. In the first quarter of 2020, the year-on-year growth rate of gross premium was 6.27%, a decrease of 9.53 percentage points compared to the same period of the previous year (Wang et al., 2020). However, the purchase power is restored with the gradual resumption of work and economic activities. Meanwhile, residents' awareness of purchasing insurance is strengthened with the spread of the pandemic. For example, the COVID-19 outbreak and spread encourage people to concern more on their health, increasing the demand for insurance to transfer risk (Qian, 2021).

Table 7.

Cumulative abnormal returns for insurance sample.

| Days | N | Median (%) | Z1 |

|---|---|---|---|

| [0, 2] | 7 | 2.62 | 2.07** |

| [0, 10] | 7 | −3.21 | −1.57 |

| [0, 15] | 7 | −2.01 | −1.34 |

| [0, 46] | 7 | −2.02 | −1.86* |

| [0, 120] | 7 | −0.83 | −1.52 |

| [0, 180] | 7 | 6.11 | −0.62 |

Notes: 1. All tests are two-tailed: *** p < 0.01; ** p < 0.05; * p < 0.10.

2. Z1-statistics for medians are obtained using Wilcoxon signed-rank tests.

4.7. Competitive effects of COVID-19

Unpredictable events such as COVID-19 can generate a great impact on the social economy, while also create opportunities for some industries (Khatatbeh et al., 2020). The demand for goods and services in industries such as healthcare, online entertainment, information technology, and telecommunication services show an increase or at least stability (Bouri, Naeem, Nor, Mbarki, & Saeed, 2021). To examine the competitive effects of COVID-19, we divide the firms with competitive effect into two subsamples: medical and competitors.

Panel A of Table 8 demonstrates that the immediate stock market reaction of medical firms is strong and positive. The mean and median CARs for Days (0, 2) are 17.41% and 14.25%, respectively, significant at the 1% level. No firms experience negative abnormal returns during this period, significant at the 1% level. The mean and median CARs for Days (0, 10) are separately 11.08% (significate at 1% level) and 9.82% (insignificant), and 90% of firms experience positive abnormal returns, significantly greater than 50% at the 1% level. The CAR for Days (0, 15) is not substantively different from the CAR for Days (0, 10). For Days (0, 46), the mean and median CARs are 27.80% (significant at the 1% level) and 25.65% (significant at the 10% level), respectively. Over 93% of sample firms experience positive abnormal returns, significantly greater than 50% at the 1% level. For Days (0, 120) and Days (0, 180), both mean and median CARs are positive but statistically insignificant. The results could be explained by the huge demand for medical supplies in the early stage of the pandemic. It is estimated that the daily demand for medical protective clothing is 1.5 million pieces during the pandemic.13 In addition, China's consumption of disposable medical protective clothing is 141 million pieces during the end of January to the end of April of 2020, about 33 times of the whole annual consumption in 2019.14 With the epidemic then began to spread in other countries, the impact being far greater than expectations. Taking the demand for ventilator as example. The total demand gap of the ventilator in the five major countries (the US, Germany, the UK, France and Italy) during the 2020 epidemic is 1 million.15 It is worth noting that many countries including China speed up the vaccine development to fight against the epidemic. Nowadays, they have never desisted from trying to develop an effective vaccine.

Table 8.

Cumulative abnormal returns for the sample with competitive effect.

| Panel A: Medical | |||||||

|---|---|---|---|---|---|---|---|

| Days | N | Mean (%) | T | Median (%) | Z1 | % positive | Z2 |

| [0, 2] | 30 | 17.41 | 20.66*** | 14.25 | 6.28*** | 100.00 | −5.29*** |

| [0, 10] | 30 | 11.08 | 8.02*** | 9.82 | 1.01 | 90.00 | −4.20*** |

| [0, 15] | 30 | 8.81 | 5.26*** | 7.93 | −0.19 | 80.00 | −3.10*** |

| [0, 46] | 30 | 27.80 | 4.05*** | 25.65 | 1.84* | 93.33 | −4.56*** |

| [0, 120] | 30 | 39.26 | 0.65 | 40.53 | 0.06 | 86.67 | −3.83*** |

| [0, 180] | 30 | 41.09 | 0.47 | 43.96 | −0.52 | 83.33 | −4.56*** |

| Panel B: Competitors | |||||||

| Days | N | Mean (%) | T | Median (%) | Z1 | % positive | Z2 |

| [0, 2] | 30 | 5.15 | 5.54*** | 2.11 | 1.76* | 60.00 | −0.91 |

| [0, 10] | 30 | 6.86 | 4.50*** | 2.39 | 0.95 | 63.33 | −1.28 |

| [0, 15] | 30 | 6.77 | 3.66*** | 4.14 | 0.46 | 36.67 | −1.28 |

| [0, 46] | 30 | 10.61 | 1.40 | 13.62 | −0.01 | 40.00 | −0.91 |

| [0, 120] | 30 | 2.76 | 0.06 | 23.18 | −3.37*** | 60.00 | −0.91 |

| [0, 180] | 30 | −1.46 | −0.02 | 16.74 | 4.89*** | 60.00 | −0.91 |

Notes: 1. All tests are two-tailed: *** p < 0.01; ** p < 0.05; * p < 0.10.

2. Z1-statistics for medians are obtained using Wilcoxon signed-rank tests.

3. Z2-statistics for % negatives are obtained using binomial sign tests.

The results for the competitors' subsample are reported in Panel B of Table 8. The stock market immediately positively reacts to COVID-19 as shown by the statistically positive mean and median CARs for Days (0, 2). About 60% of sample firms experience positive abnormal returns, significantly more than 50% at the 1% level. The positive mean CAR is sustained over Days (0, 120), but only significant for the first three event periods. For Days (0, 180), the mean CAR reverses to negative, but insignificant. Furthermore, the magnitude of the mean CAR appears to increase in the early stage. In terms of the median CAR, the positive values are persistent through all the event periods and tend to increase over Days (0, 120). But the statistically significant positive median CAR is just observed for Days (0, 120) and Days (0, 180).

4.8. The impact of the global spread of COVID-19

After spreading in China for a period of time, COVIID-19 subsequently broke out in Japan, South Korea, Europe, the United States, and other countries. Besides local information, investors are also sensitive to global news (Liu et al., 2021). To better analyze the impact of COVID-19 on Chinese firms, we therefore choose the second event day and also use the event study method to examine the effects of the global epidemic spread on Chinese firms. The WHO declared COVID-19 as a global pandemic on 12 March 2020,16 indicating the global breakout of the pandemic. So we choose the date as the event day. To compare the results with our abovementioned results, the window period selection is the same as that in the previous parts, that is, (0, 2), (0, 10), (0, 15), (0, 46), (0, 120), (0, 180). To keep the estimation period not affected by the event, we choose the same estimation period as above, which is (−124, −25) for a total of 100 days. The results are presented in Table 9 .

Table 9.

Cumulative abnormal returns for samples directly and indirectly affected by the global spread of COVID-19.

| Panel A: Directly affected | |||||||

|---|---|---|---|---|---|---|---|

| Days | N | Mean (%) | T | Median (%) | Z1 | % negative | Z2 |

| [0, 2] | 99 | 0.48 | 1.18 | 0.05 | −0.69 | 48.48 | −0.20 |

| [0, 10] | 99 | 2.03 | 2.71*** | 1.40 | 0.96 | 40.40 | −1.81* |

| [0, 15] | 99 | −0.16 | −0.17 | −0.18 | −1.76* | 50.51 | 0.00 |

| [0, 46] | 99 | 0.08 | −0.05 | 0.76 | −2.90*** | 48.48 | −0.20 |

| [0, 120] | 99 | −0.20 | −0.08 | 10.16 | −7.08*** | 39.39 | −2.01** |

| [0, 180] | 99 | −8.68 | −2.84*** | 3.35 | −10.53*** | 45.45 | −0.80 |

| Panel B: Downstream (Effects from suppliers) | |||||||

| Days | N | Mean (%) | T | Median (%) | Z1 | % negative | Z2 |

| [0, 2] | 42 | 1.00 | 1.65 | 0.93 | 0.05 | 42.86 | −0.77 |

| [0, 10] | 42 | −1.88 | −1.68* | −1.07 | −3.24*** | 59.52 | −1.08 |

| [0, 15] | 42 | −3.34 | −2.49** | −2.78 | −3.79*** | 61.90 | −1.39** |

| [0, 46] | 42 | −8.11 | −3.57*** | −4.85 | −6.30*** | 78.57 | −3.55*** |

| [0, 120] | 42 | −8.73 | −2.36** | −5.74 | −8.26*** | 64.29 | −1.70* |

| [0, 180] | 42 | −8.28 | −1.82* | −0.05 | −8.5*** | 50.00 | 0.00 |

| Panel C: Upstream (Effects from customer) | |||||||

| Days | N | Mean (%) | T | Median (%) | Z1 | % negative | Z2 |

| [0, 2] | 152 | −0.44 | −1.43 | −0.01 | −2.07** | 50.00 | 0.00 |

| [0, 10] | 152 | 0.19 | 0.34 | 0.16 | −1.22 | 48.03 | −0.41 |

| [0, 15] | 152 | −0.75 | −1.09 | −0.73 | −2.96*** | 54.61 | −1.05 |

| [0, 46] | 152 | 1.25 | 1.83 | −0.75 | −4.20*** | 52.63 | −0.57 |

| [0, 120] | 152 | 4.10 | 2.17** | 3.73 | −7.92*** | 46.05 | −0.89 |

| [0, 180] | 152 | 3.01 | 1.30 | 8.12 | −10.05*** | 42.11 | −1.87* |

| Panel D: Multiple effects | |||||||

| Days | N | Mean (%) | T | Median (%) | Z1 | % negative | Z2 |

| [0, 2] | 46 | −1.14 | −1.86* | −1.16 | −2.45** | 60.87 | −1.33 |

| [0, 10] | 46 | −1.19 | −1.05 | −0.53 | −2.16** | 58.70 | −1.03 |

| [0, 15] | 46 | −3.46 | −2.55** | −4.54 | −3.640*** | 71.73 | −2.80*** |

| [0, 46] | 46 | −6.01 | −2.62** | −4.51 | −5.40*** | 67.39 | −2.21** |

| [0, 120] | 46 | 0.33 | 0.09 | 6.13 | −6.10*** | 45.65 | −0.44 |

| [0, 180] | 46 | −3.68 | −0.80 | 0.89 | −7.50*** | 47.83 | −0.15 |

Notes: 1. All tests are two-tailed: *** p < 0.01; ** p < 0.05; * p < 0.10.

2. Z1-statistics for medians are obtained using Wilcoxon signed-rank tests.

3. Z2-statistics for % negatives are obtained using binomial sign tests.