Abstract

Introduction

There were repeated reports of increased cannabis sales, use and health impacts in Canada during the COVID‐19 pandemic. However, it was unclear whether the increases were due to pandemic effects or industry expansion.

Methods

We performed interrupted time series regressions of monthly per capita legal cannabis sales from March 2019 to February 2021, first with national averages, then with provincial/territorial data after adjusting for store density. We considered two interruption alternatives: January 2020, when product variety increased; and March 2020, when pandemic restrictions began.

Results

The provincial/territorial regression with the January interruption explained R 2 = 69.6% of within‐jurisdiction variation: baseline monthly per capita sales growth averaged $0.21 (95% confidence interval [CI] 0.15, 0.26), sales immediately dropped in January by $1.02 (95% CI −1.67, −0.37), and monthly growth thereafter increased by $0.16 (95% CI 0.06, 0.25). With the March interruption, the regression instead explained 68.7% of variation: baseline sales growth averaged $0.14 (95% CI 0.06, 0.22), there was no immediate drop and growth thereafter increased by $0.22 per month (95% CI 0.08, 0.35).

Discussion and Conclusions

Increasing cannabis sales during the pandemic was consistent with pre‐existing trends and increasing store numbers. The extra increased growth was more aligned with January's new product arrivals than with March's pandemic measures, though the latter cannot be ruled out. We found little evidence of pandemic impacts on Canada's aggregate legal cannabis sales. We therefore caution against attributing increased population‐level cannabis use or health impacts primarily to the pandemic.

Keywords: cannabis, COVID‐19 pandemic, interrupted time series analysis, health economics, legalisation

Introduction

Beginning in March 2020, Canada's provinces and territories (hereinafter, ‘jurisdictions’) responded to the COVID‐19 pandemic with lockdowns and other public health measures [1]. During the pandemic's first year, annual legal cannabis sales doubled from $1.25 billion to $2.49 billion [2]. News reports frequently attributed that increase wholly [3] or largely [4] to the pandemic.

Surveys meanwhile reported increased Canadian cannabis use. During the pandemic, 40% of respondents reported more frequent cannabis usage compared to 15% reporting less [5]. Daily or almost daily cannabis use increased from 6.1% (95% confidence interval [CI] 5.2, 7.1) of respondents in 2019 to 7.9% (95% CI 6.8, 9.2) in 2020 [6]. Cannabis‐related hospitalisations (5%) and emergency department visits (8%) also increased between 2019 and 2020 [7].

However, these increases could have been effects of Canada's recent recreational (i.e. non‐medical) cannabis legalisation. Cannabis retailing expanded enormously after licensed stores first opened in October 2018 [8, 9]: store counts rose from 178 in January 2019 to 707 in January 2020, and to 1398 in January 2021. Retail sales likewise grew: $55 million in January 2019, $154 million in January 2020 and $279 million in January 2021 [2]. After initial production shortfalls eased in March 2019, store numbers became good predictors of legal sales [10, 11].

Canada's cannabis market also evolved in other ways during 2020. Prices for legal dry cannabis products dropped below those of illegal products in some jurisdictions [12]; legal vapes and edibles became available for sale; and legal sales surpassed illicit sales as the latter declined [13].

So, while legal sales clearly increased during the pandemic, it was unclear whether that was due to pandemic effects, industry evolution or both. Our study investigated this question using interrupted time series models to analyse legal sales from March 2019 to February 2021. We compared two competing interruption timings: March 2020, when the pandemic hit Canada, and January 2020, when legal product selection expanded. Both timings considered two levels of geographic aggregation for mutual corroboration.

Methods

Data

We examined monthly Canadian legal recreational cannabis retail sales (in‐store and online combined in Canadian dollars) for 12 jurisdictions from March 2019 to February 2021 [2]. We excluded earlier months because product shortages prevented sales growth until March 2019 [10]. We divided each month's sales by its length in days and multiplied by 30, to create standardised 30‐day totals.

Licensed store counts came from each jurisdiction's cannabis agency website at the beginning of each month. We prorated these to account for two events: pandemic lockdowns closed all Prince Edward Island stores from 19 March to 21 May 2020 [14] and labour disputes closed 10 Newfoundland stores from 23 August to 16 November 2020 [15]. See Appendix S1 for further details about this adjustment.

We converted sales totals to per capita amounts by dividing by the population aged 15 and over in July of each year [16]. We similarly converted store counts to stores per 100 000 residents aged 15+.

Exposure

To test whether sales changes were associated with pandemic measures, we defined March 2019 to February 2020 as the pre‐pandemic baseline period, and March 2020 to February 2021 as the treatment period. We investigated two time‐related effects: a level change when the pandemic began (e.g. did average monthly sales jump?) and a slope change thereafter (e.g. did month‐over‐month sales growth accelerate?).

To test whether sales changes were instead associated with industry expansion, we redefined the treatment period to begin in January 2020, when processed products, such as vapes and edibles, became available.

Analysis

We performed segmented linear regressions in Stata 17 software at two levels of geographic aggregation: a ‘national’ analysis that used limited but easily visualised data and a ‘provincial/territorial’ analysis that adjusted for additional covariates.

The national analysis used monthly nationwide sales per capita as the dependent variable. The regressions included a constant, a slope variable representing baseline monthly sales growth over both periods, a slope change variable representing altered monthly growth during the treatment period and a level change variable equalling 0 during baseline months and 1 during treatment months. We used Stata's ‘newey’ command to calculate Newey‐West standard errors to account for autocorrelation and heteroskedasticity. We compared two models:

The ‘March’ model considered slope and level changes in March 2020.

The ‘January’ model instead considered slope and level changes in January 2020.

The provincial/territorial analysis used monthly sales per capita in 12 jurisdictions as the dependent variable and adjusted for stores per 100 000 residents. We used Stata's ‘xtscc’ fixed effect panel data regression to calculate Driscoll‐Kraay standard errors to compensate for autocorrelation, cross‐sectional correlation and heteroskedasticity. We compared three models:

The ‘Base’ model did not include slope or level change variables.

The ‘March’ model added slope and level change variables for March 2020.

The ‘January’ model instead added slope and level change variables for January 2020.

Research ethics

The Public Health Ontario Ethics Review Board (file number 2020‐038.01) approved this study.

Results

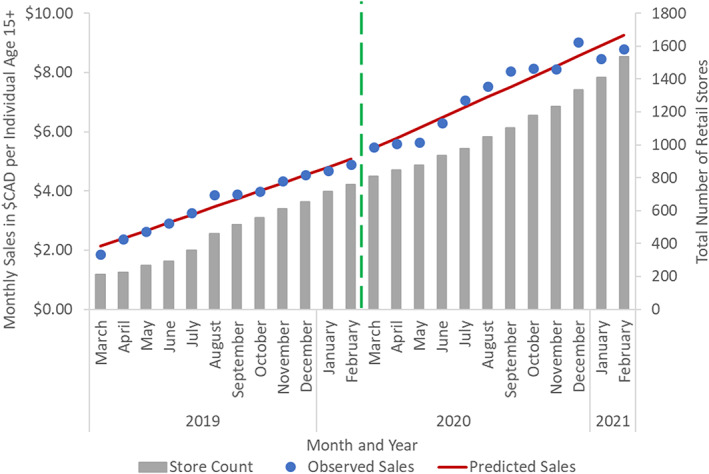

Figure 1 demonstrates Canada's legal recreational cannabis retail sales and store growth from March 2019 to February 2021. The first two columns of Table 1 summarise the national analysis. The March and January models gave very similar results: both had excellent fit and statistically significant baseline slopes, but neither the level changes nor the slope changes were significant.

Figure 1.

National monthly legal cannabis retail sales, from March 2019 to February 2021, in Canadian dollars per resident age 15+. Dots represent observed monthly sales, solid lines represent regression‐predicted sales assuming a March 2020 interruption and vertical bars represent total licensed cannabis stores. The vertical dashed line separates the pre‐pandemic and pandemic periods.

Table 1.

Regression summary of monthly cannabis sales in Canadian dollars per capita for national analysis (left), using n = 24 observations, and provincial/territorial analysis (right), using n = 288 observations

| National | National | Provincial | Provincial | Provincial | |

|---|---|---|---|---|---|

| March model | January model | Base model | March model | January model | |

| R 2 within | 98.4% | 98.5% | 67% | 68.7% | 69.6% |

| Stores | — | — | $0.51 | $0.51 | $0.51 |

| 95% CI | 0.378, 0.632 | 0.386, 0.644 | 0.383, 0.643 | ||

| P | 0.001 | 0.001 | 0.001 | ||

| Slope | $0.27 | $0.29 | $0.24 | $0.14 | $0.21 |

| 95% CI | 0.234, 0.302 | 0.260, 0.324 | 0.189, 0.295 | 0.064, 0.224 | 0.149, 0.262 |

| P | 0.001 | 0.001 | 0.001 | 0.001 | 0.001 |

| Slope change | $0.08 | $0.06 | — | $0.22 | $0.16 |

| 95% CI | −0.002, 0.157 | −0.000, 0.122 | 0.076, 0.359 | 0.062, 0.250 | |

| P | 0.055 | 0.050 | 0.004 | 0.002 | |

| Level change | $0.06 | −$0.32 | — | −$0.19 | −$1.02 |

| 95% CI | −0.454, 0.581 | −0.697, 0.059 | −1.097, 0.709 | −1.668, −0.367 | |

| P | 0.801 | 0.094 | 0.661 | 0.004 |

Each column shows the model's within‐jurisdiction fit R 2, plus each variable's regression coefficient, 95% confidence interval and significance. Regression constants are omitted for brevity.

‐ indicates when covariate was not included in model.

Meanwhile, the last three columns of Table 1 provide the provincial/territorial analysis. The Base model's baseline slope and store density variables explained R 2 = 67% of within‐province sales variation. The March model's slope and level changes increased this by 1.7% points: the slope change was positive and significant, whereas the level change was negative and not significant. By contrast, the January model's slope and level changes increased the fit by 2.6 points over the Base model: both the positive slope change and negative level change were significant. Coefficients from all model covariates are presented in Appendix S1.

Discussion

Our study found three principal results. First, rising store numbers and ongoing market trends explained most sales growth during 2020–2021, but sales grew more than what those two factors alone would have predicted. Second, there was no statistically significant or economically meaningful level change in March 2020, when pandemic responses began; but a sales drop was observed in January 2020, perhaps due to a post‐holiday spending slump. Third, there was a modest but statistically significant slope change, as month‐over‐month sales growth accelerated during 2020–2021: the acceleration's timing better fit January's increasing product selection than March's increasing pandemic stressors, though we cannot rule out the latter.

These findings differ from news reports [e.g. 3,4] that attributed annual sales increases largely or entirely to the pandemic. Our results suggest the pandemic was not associated with an immediate sales increase and that the sales acceleration during the pandemic could be explained by new product arrivals and other industry factors. The findings therefore also indirectly imply that reported increases in usage [5, 6] and cannabis‐related medical visits [7] could be partially explained by industry expansion rather than pandemic stress.

Our study had several limitations. One was that it ignored medical and illicit cannabis sales. However, recreational sales surpassed medical sales in late 2018 and illicit sales in summer 2020; so, our analysis covered most Canadian sales. Furthermore, whereas recreational sales grew, the other two markets declined during 2019–2021 [13].

The study was also limited by having only 12 months of pre‐pandemic data, which reduced its power to detect small sales changes. It was nonetheless sufficient for correcting media misperceptions and for estimating changes large enough to be policy relevant. A third limitation was that we analysed sales dollars, rather than product volumes used, for example grams of flower. We anticipate that higher pricing for edibles balanced‐out lower pricing for dry cannabis during the study period, but future research should investigate how pricing and product variety affects quantities used.

Finally, our study examined population‐level data. It did not consider possible changes within certain population subgroups, such as individuals with pre‐existing mental health conditions or individuals with cannabis use disorders [5]. Research targeting such subgroups should be encouraged.

Conclusion

Canada's legal cannabis sales growth during the pandemic's first year was more consistent with ongoing market expansion than with pandemic effects. Consequently, reports attributing increased usage and health impacts to the pandemic may be underestimating industry effects. This highlights the need to monitor the legal cannabis industry that now exists in Canada, and that might soon exist in countries considering legalisation, such as Mexico, Israel and Germany.

Conflict of Interest

The authors have all completed International Committee of Medical Journal Editors conflict of interest forms. The authors declare that they have no conflicts.

Supporting information

Appendix S1. Supporting Information.

Acknowledgements

This study was supported by a project grant (452360) from the Canadian Institute for Health Research (CIHR). The analyses, conclusions, opinions and statements expressed herein are solely those of the authors and do not reflect those of the funding or data sources; no endorsement is intended or should be inferred. DM was supported by a CIHR Research Fellowship and a uOttawa Department of Family Medicine Innovation Fellowship.

Michael J. Armstrong PhD, Associate Professor of Operations Research, Nathan Cantor MSc, Medical Student, Brendan T. Smith PhD, Scientist, Rebecca Jesseman MA, Policy Director, Erin Hobin PhD, Scientist, Daniel T. Myran MD MPH, CIHR and uOttawa Department of Family Medicine Research Fellow.

References

- 1. McCoy LG, Smith J, Anchuri K et al. Characterizing early Canadian federal, provincial, territorial and municipal nonpharmaceutical interventions in response to COVID‐19: a descriptive analysis. CMAJ Open 2020;8:E545–53. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 2. Statistics Canada . Table 20‐10‐0008‐01, Retail trade sales by province and territory (x 1,000); 2021a. Available at: 10.25318/2010000801-eng (accessed March 2021). [DOI]

- 3. Fletcher R. Alberta walks back claim people are buying more alcohol and cannabis during pandemic. CBC News, 15 June 2020. Available at: https://www.cbc.ca/news/canada/calgary/alberta-health-liquor-cannabis-sales-no-actual-data-1.5612664 (accessed June 2021).

- 4. Saint‐Arnaud P. Quebec's cannabis profits nearly double in a year. Montreal Gazette. 2021. Available at: https://montrealgazette.com/cannabis/cannabis-business/quebecs-cannabis-profits-nearly-double-in-a-year (accessed June 2021).

- 5. Mental Health Commission of Canada . Mental Health and Substance Use During COVID‐19: Summary Report; 2021. Available at: https://www.mentalhealthcommission.ca/sites/default/files/2021-04/mhcc_ccsa_covid_leger_poll_eng.pdf (accessed July 2021).

- 6. Rotermann M. Looking back from 2020, how cannabis use and related behaviours changed in Canada. Health Rep 2021;32:3–14. [DOI] [PubMed] [Google Scholar]

- 7. Canadian Institute for Health Information . Unintended Consequences of COVID‐19: Impact on Harms Caused by Substance Use; 2021. Available at: https://www.cihi.ca/sites/default/files/document/unintended-consequences-covid-19-substance-use-report-en.pdf (accessed July 2021).

- 8. Myran DT, Brown CRL, Tanuseputro P. Access to cannabis retail stores across Canada 6 months following legalization: a descriptive study. CMAJ Open 2019;7:E454–61. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 9. Myran DT, Staykov E, Cantor N et al. How has access to legal cannabis changed over time? An analysis of the cannabis retail market in Canada 2 years following the legalisation of recreational cannabis. Drug Alcohol Rev 2021;41:377. [DOI] [PubMed] [Google Scholar]

- 10. Armstrong MJ. Legal cannabis market shares during Canada's first year of recreational legalization. Int J Drug Policy 2021;88:103028. [DOI] [PubMed] [Google Scholar]

- 11. Armstrong MJ. Relationships between increases in Canadian cannabis stores, sales, and prevalence. Drug Alcohol Depend 2021;228:109071. [DOI] [PubMed] [Google Scholar]

- 12. Ontario Cannabis Store A Quarterly Review (1 October– 31 December 2020). Available at: https://ocs.ca/pages/insights-publication. Accessed June 2021.

- 13. Statistics Canada . Table 36‐10‐0124‐01, detailed household final consumption expenditure, Canada, quarterly (x 1,000,000); 2021b. Available at: 10.25318/3610012401-eng (accessed June 2021). [DOI]

- 14. Fraser S. P.E.I. Cannabis stores to reopen next week, CBC News , 14 May 2020. Available at: https://www.cbc.ca/news/canada/prince-edward-island/pei-government-reopen-public-services-1.5570157 (accessed June 2021).

- 15. Canadian Press . Strike is over for N.L. Dominion store workers, but there is no happy ending: Unifor. CTV News , 16 November 2020. Available at: https://atlantic.ctvnews.ca/strike-is-over-for-n-l-dominion-store-workers-but-there-is-no-happy-ending-unifor-1.5190787 (accessed June 2021).

- 16. Statistics Canada . Table 17‐10‐0005‐01, Population estimates on July 1st, by age and sex; 2021c. Available at: 10.25318/1710000501-eng (accessed 19 June 2021). [DOI]

Associated Data

This section collects any data citations, data availability statements, or supplementary materials included in this article.

Supplementary Materials

Appendix S1. Supporting Information.