Abstract

How do firms in global value chains react to input shortages? We examine micro-level adjustments to supply chain shocks, building on the Covid-19 pandemic as a case study. French firms sourcing inputs from China just before the early lockdown in the country experienced a relative drop in imports that increases from February to April 2020. This shock on input purchases transmits to the rest of the supply chain through exposed firm’s domestic and export sales. Between February and June, firms exposed to the Chinese early lockdown experienced a 5.5% drop in domestic sales and a 5% drop in exports, in relative terms with respect to comparable non-exposed firms. The drop in foreign sales is entirely attributable to a lower volume of exports driven by a temporary withdrawal from occasional markets. We then dig into the heterogeneity of the transmission across treated firms. Whereas the ex-ante geographic diversification of inputs does not seem to mitigate the impact of the shock, firms with relatively high inventories have been able to absorb the supply shock better.

Keywords: Covid-19 pandemic, Supply chain disruptions, Transmission of shocks, Global value chains

Introduction

International flows of intermediate inputs constitute as much as two-thirds of international trade and half of global trade is embodied in global value chains (GVCs) (Johnson 2014; Antràs 2020). In this context, international production processes appear as a key channel of transmission of shocks across countries (di Giovanni et al. 2018; Boehm et al. 2019). The Covid-19 pandemic offers plenty of anecdotal evidence of firms’ vulnerability to shocks affecting their international supply chain. However, there is little quantitative evidence on the reaction of firms in GVCs to input shortages. This paper makes two contributions. First, it provides evidence of a firm-level transmission of shocks on imported inputs to the firm’s domestic and export sales. Second, it evaluates how the diversification of the firm’s supply chain and its inventory management can help mitigate the transmission of adverse shocks affecting its supply chain.

The empirical analysis exploits the January 2020 lockdown in China as a natural experiment of a shock to French firms’ supply chain. Six weeks separated the lockdown in China and lockdowns in France’s other main trading partners. This paves the way for a comparison of firms sourcing inputs from China with those that do not to explore the consequences of being exposed to supply chain disruptions. We study the real transmission of the shock using detailed data on French firms’ foreign and domestic activity. Firms relying on Chinese inputs before the beginning of the pandemic experienced a 5% decline in their exports and a 5.5% decline in domestic sales between February and June 2020, in relative terms with respect to similar firms involved in GVCs that were not exposed to Chinese inputs. The drop in firm-level exports is almost entirely driven by the extensive margin: exposed exporters temporarily stopped serving some of their occasional foreign partners. Whereas the ex-ante geographic diversification of inputs does not seem to influence the transmission of the shock, we provide evidence that holding inventories offers a buffer for firms exposed to such temporary supply shocks.

We organize the paper in three parts. First, we describe the data and present evidence that the Chinese lockdown has caused a shortage of inputs for French firms importing from China. Our analysis builds on French customs data that cover the universe of French importers and exporters, merged with domestic sales recovered from VAT statements. The final dataset contains transaction-level imports and exports as well as domestic sales, at the monthly frequency, before and during the pandemic. The monthly frequency of the data combined with information on the geography of firms’ input purchases allows us to exploit the timing of the pandemic to identify the propagation of a supply shock downstream in the value chain. In early 2020, when the world was to a large extent ignorant of the pandemic risk, China adopted stringent measures to contain the spread of SARS-CoV-2, which led to shuttering factories in the aftermath of the Chinese new year. In February 2020, French imports from China had already dropped by more than 10% and they reached a minimum in March, one month before imports from the rest of the world. The drop in imports from China immediately after the lockdown is more severe than the usual seasonal slowdown. We thus interpret it as a supply shock for French importers of Chinese inputs.

Our main analysis covers firms that participate in global value chains (GVCs). These firms both import intermediate inputs and export some of their output (WDR 2020). We split this sample into two groups: a treatment group composed of firms exposed to China through imports of intermediate inputs, and a control group that was not importing from China when the Covid crisis started. Having established that these groups display significantly divergent import patterns in the aftermath of the Chinese early lockdown, we examine the within-firm downstream propagation of the supply shock. We estimate the strength of the propagation using firms’ domestic and foreign sales as outcome variables. We find firms exposed to Chinese inputs incurred a 5% drop in exports, in comparison with the control group, in the five months following the Chinese lockdown. A similar relative adjustment is observed in domestic sales, which confirms that the trade adjustment is not attributable to substitution away from foreign markets. The relative drop peaks in April 2020 at –15% for exports and –12% for domestic sales. In June 2020, both groups have converged to the same contraction in sales, in comparison with their January level. Interestingly, the firm-level adjustment is mainly driven by the extensive margin. The average treated firm serves 10.3% less products and 9.2% less destinations in April, in comparison with the control group. Likewise, the (relative) recovery in May and June 2020 mostly involves (relative) extensive margin adjustments. We provide evidence of a temporarily higher probability for treated firms to stop serving some of the markets they were serving in the pre-shock period, in particular the firm’s secondary and/or occasional markets. To our knowledge, we are the first to provide evidence of within-firm temporary extensive margin adjustments in response to a shock.

We then investigate the extent to which risk management strategies can help mitigate the transmission of the supply shock downstream in the value chain. First, we explore the role played by the supply structure of the firm. Given the vulnerability of input–output structures to localized shocks, diversifying the supply chain in the spatial dimension should be an efficient resilience strategy. One should thus expect the impact of being exposed to the Chinese early lockdown to be muted for firms with a diversified supply chain, that can increase their demand for non-Chinese inputs when the shock kicks in. To test this assumption, we quantify the extent to which geographic diversification of imported inputs prior to the shock helped firms withstand the supply disruption. We do not find evidence that diversified firms performed better. It appears that exposed firms that were not diversified ex-ante have managed to find new suppliers. As a result, imports and exports of exposed firms, both diversified and undiversified, followed a similar trajectory. However, there are significant measurement challenges in measuring diversification using firm-level trade data, and the lack of results may also be due to poorly measured diversification opportunities.

We then ask whether stock pilling can offer firms a buffer against short-lived supply chain disruptions. Formally, we investigate how the export performances of firms with more inventories differ from the performances of firms with just-in-time production strategies. The level of inventories is recovered from balance-sheet data covering firms’ activity prior to the shock and is normalized to take into account systematic differences in the level of inventories across sectors. Among firms exposed to the Chinese lockdown, those holding more inventories ex-ante performed better in the aftermath of the shock. The dynamics of their exports is not significantly different than in the control group and the baseline relative drop in exports is thus entirely attributable to treated firms with relatively low levels of inventories. Holding stocks has thus been a useful buffer in the early stages of the 2020 crisis.1

Related literature

A series of paper examine how trade adjusted during the pandemic.2 Our contribution to the trade and Covid-19 literature is to trace out the quick transmission of supply chain disruptions induced by the pandemic at the firm level, and analyze heterogeneity in this transmission across firms with different risk management strategies.

We participate to the broad literature on GVCs (see, e.g., Antràs and Chor 2013; Baldwin and Lopez-Gonzalez 2015; Johnson 2018; Antràs 2020). We connect exogenous changes in input purchases to firms’ exports. In this respect, our work relates to the literature showing how imported inputs affect domestic (Goldberg et al. 2010; Huneeus 2018) and export performances (Halpern et al. 2015; Feng et al. 2016; Bas and Strauss-Kahn 2015; Amiti et al. 2014). High-frequency data make it possible to dig into the dynamics of the adjustment to a large but relatively short-lived supply-side shock.3 Whereas this literature mostly focuses on the structure and geography of global value chains, we instead study the consequences of this structure for firms’ exposure to localized shocks.

In doing so, we contribute to the recent literature measuring the transmission of shocks along supply chains.4 As in Boehm et al. (2019), we exploit the monthly frequency of firm-level trade data to trace the dynamics of firms’ adjustment to supply chain shocks. New to this strand of the literature is our investigation of geographic diversification of input purchases and inventories as buffers against adverse shocks.5 Several papers have highlighted the role of inventories for firms engaged in international trade (Alessandria et al. 2010b; Khan and Khederlarian 2021), notably during the 2008 Trade Collapse (Alessandria et al. 2010a). Here, we show inventories mitigate the international propagation of shocks along supply chains.6 Instead, we do not find evidence that diversification helped firms weather this particular shock.

The paper is organized as follows. Section 2 describes the data and shows the Chinese lockdown has induced a shortage of inputs for French firms sourcing these inputs from China. Section 3 provides evidence of the within-firm transmission of the Chinese shock to firms’ downstream partners. Section 4 examines differences in adjustments to shocks across firms with heterogeneous risk management strategies. Section 5 concludes.

Data and empirical strategy

This section presents the firm-level data used throughout the analysis and the definition of firms’ involvement in GVCs. We then provide evidence that the Chinese lockdown has severely reduced productivity, with consequences for firms importing their inputs from China.

Data

The main source of data for our empirical analysis is provided by the French customs. The dataset covers each unique transaction involving a French company and a non-French partner. For each export and import transaction, we have information on the French company that originated the trade flow, the product category, the partner country, the value and quantity of the shipment, the mode of transport, and the date of the transaction, at the monthly level.7 As discussed in Sect. 2.2, the monthly frequency is particularly useful as it captures the timing of the pandemic and its heterogeneous impact on bilateral trade.

We merge the estimation sample with an other two firm-level datasets. The INSEE-FARE dataset, available up to 2018, provides balance-sheet information on French firms, collected for tax purposes. Based on the balance-sheet data, we measure the ratio of imports over intermediate consumption and the share of exports in aggregate sales, which we use as proxies for the firm’s degree of vertical specialization. The balance-sheet data are also used to recover information on firms’ inventories. Second, we merge the data with monthly information on French firms domestic and overall sales, available in their VAT statements. These data can be used to compare the dynamics of foreign and domestic sales in the aftermath of the early lockdown in China.

In the rest of the analysis, our objective is to identify the diffusion of supply chain disruptions induced by the Chinese lockdown on GVCs, using French firms as reference. We follow the World Development Report (WDR 2020) and consider that a firm is engaged in GVCs if it both imports some of its inputs and exports part of its output. In the rest of the analysis, we thus restrict our attention to firms that display strictly positive exports and strictly positive imports of intermediates, where the definition of intermediates follows the UN-BEC classification of products and firms’ trade activities is measured between September 2019 and January 2020. Of course, there is ample heterogeneity in this sample regarding the intensity of these firms’ international activity. 49.4% of the firms export more than 10% of their output and 60.5% purchase more than 10% of their inputs from abroad. Our baseline results pool all firms together but we show in appendix A.4 that results are not very different across firms displaying heterogeneous degrees of trade exposure.

Table 1 shows descriptive statistics on the sample of firms under study. These approximately 30,000 firms account for about 40% of French firms’ domestic sales and three quarters of the value of French exports and imports. These numbers are consistent with the view that, in tradable sectors, large firms tend to be involved into two-way trade (Bernard et al. 2018). Among these firms, 45% import some of their inputs from China and 14% have interacted with Chinese producers on a monthly basis between September 2019 and January 2020.8 In the rest of the analysis, firms importing from China constitute our treatment group while firms that import part of their inputs but did not interact with Chinese firms in the months before the shock are used as controls. In Appendix A.3, we consider an alternative definition of the treatment restricted to firms with monthly interactions with China.

Table 1.

Summary Statistics on the estimation sample

| Nb. of firms | Avg. | % of aggregate | |||||

|---|---|---|---|---|---|---|---|

| Imports | Dom.Sales (2019) | Exports | Imports | Dom.Sales | Exports | ||

| All firms | 30,420 | 6.4 | 54.2 | 12.4 | 76.5 | 43.5 | 77.1 |

| Importers from | |||||||

| China | 13,701 | 10.0 | 77.7 | 20.7 | 54.1 | 28.1 | 58.3 |

| Elsewhere | 16,719 | 3.4 | 34.9 | 5.5 | 22.3 | 15.4 | 18.9 |

| Monthly importers from | |||||||

| China | 4228 | 19.0 | 138.1 | 38.1 | 31.6 | 15.4 | 33.0 |

| Elsewhere | 9697 | 5.6 | 47.0 | 7.9 | 21.3 | 12.0 | 15.8 |

Summary statistics computed in 2019 on firms that both import intermediates and export between September 2019 and January 2020. The sample is restricted to firms that we merge with VAT data. Statistics on imports are restricted to intermediate goods. Average sales are in millions euros. Shares in %. Source: Customs and INSEE-VAT data

The treated firms are about three times larger than other importers, in terms of the average value of their imports and exports. This size gap is not surprising because importing from China involves substantial fixed and variable costs that only the largest firms can afford.9 China is one of the largest suppliers to French firms, which explains that 54% of imports and 58% of exports originate from firms importing from China.

Empirical strategy

Supply chain disruptions have been at the heart of policy debates since the Covid-19 pandemic started. However, their actual impact on the economy is difficult to establish. From the Spring of 2020, many countries have simultaneously adopted lockdown strategies that affected both supply and demand. Since then, the world has experienced a series of epidemic waves followed by rapid economic recoveries that have disorganized world trade. To isolate the effect of a supply shock, we exploit the timing and geography of the early phases of the pandemic. The pandemic started in China and the Chinese government has been the first to implement lockdown measures at the end of January 2020, at a time when the rest of the world was not contaminated yet. As a result, industrial production in China collapsed, together with the volume of the country’s exports.10 It is only in the first half of March 2020 that the virus really started to spread to the rest of the world. In France, a national lockdown started in March 17th, which was partially released on May 11th. Our empirical strategy uses the monthly dynamics of sales to provide evidence of the transmission of the productivity consequences of the early lockdown in China along the value chain of exposed French firms.

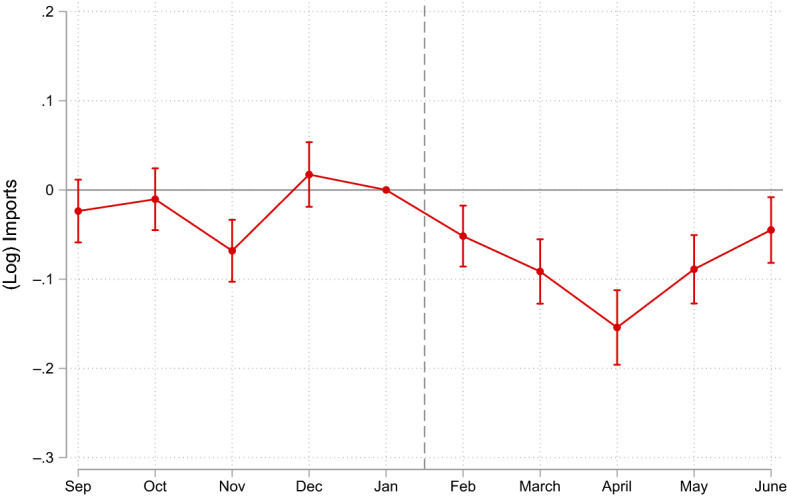

Figure 1 provides indicative evidence that the early lockdown in China has had consequences on French firms exposed to China through their input purchases. We compare the evolution of overall imports before and after the Chinese lockdown for firms directly exposed to the Chinese lockdown in comparison with the control group.11 Before the lockdown in February, there is no significant difference in the evolution of imports for firms in the treatment and the control groups, except in November due to the specific seasonality of Chinese exports. We observe a relative drop in imports in the treatment group in the month that followed the Chinese lockdown. The effect seems to be transitory with a peak in April before a rebound. In June, the level of imports is only marginally lower in the treatment than in the control group.12 The dynamics, recovered from a narrow comparison of firm-level imports in a treated and a control group, is in line with the behavior of aggregate imports displayed in Fig. A.3. Overall, the level of imports between February and June 2020 has been 7.4% lower in the treatment group than for firms in the control group (Table 2, columns (1) and (2)).

Fig. 1.

Impact of the Chinese lockdown on firm-level imports. Notes: The figure shows the dynamics of imports before and after the Chinese lockdown, for treated firms in comparison with the control group. Treated firms are those importing from China prior to the shock. Control firms are importers not exposed to China. The estimated equation includes firm and period fixed effects. Standard errors are clustered at the firm level. Confidence intervals are defined at 5%

Fig. A.3.

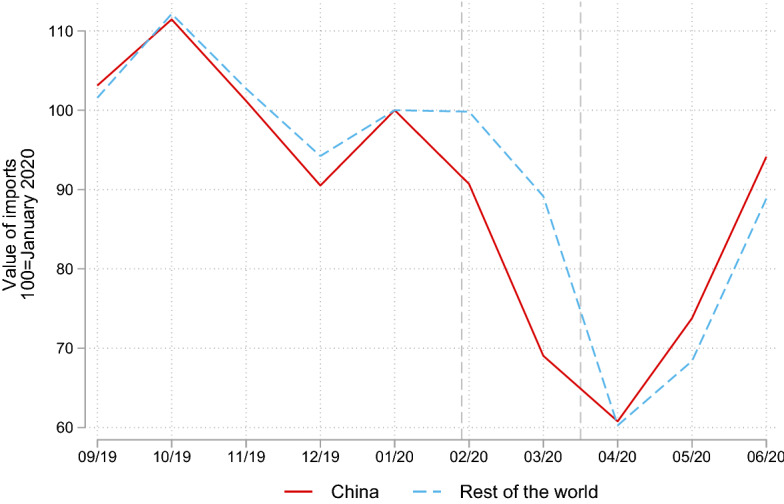

Value of French imports from China and from the rest of the world. Source: French customs, import files. The figure shows the evolution in the value of French imports from China and from the rest of the world, between September 2019 and June 2020. Both time series are normalized to 100 in January 2020. COVID products are excluded using the list of HS6 products produced by the WTO

Table 2.

Impact of the Chinese lockdown on various firm-level outcomes: Differences-in-difference results

| Dep. Var: log of | ||||||

|---|---|---|---|---|---|---|

| Imports | Exports | Dom sales | Export price | |||

| (1) | (2) | (3) | (4) | (5) | (6) | |

| Treatment Post | −0.074 | −0.074 | −0.050 | −0.035 | −0.055 | −0.007 |

| (0.010) | (0.006) | (0.011) | (0.005) | (0.007) | (0.002) | |

| Firm FE | Yes | Product | Yes | Product | Yes | Product |

| Time FE | Yes | Product | Yes | No | Yes | No |

| ProductDestinationPeriod | Yes | Yes | ||||

| # Treated | 12,086 | 10,852 | 12,086 | 11,542 | 12,086 | 11,542 |

| # Control | 13,563 | 24,174 | 13,563 | 13,566 | 13,563 | 13,566 |

| 0.857 | 0.869 | 0.856 | 0.735 | 0.901 | 0.864 | |

| # Obs. | 211,818 | 2,196,743 | 202,622 | 6,712,916 | 236,121 | 6,344,742 |

The table reports results of difference-in-difference estimations based on various firm-level outcome variables, estimated based on data from September 2019 to June 2020. The generic estimated equation writes: where is an outcome variable, that can further have the product dimension as in column (2) or the product and country dimensions as in columns (4) and (6). is a dummy equal to one for firms that were exposed to China in the pre-shock period, through their input purchases. In column (2), the “treatment” is defined at the firm and product level. is equal to one for periods between February and June 2020. The fixed effects FE include firm and period fixed effects in columns (1), (3) and (5), productfirm and productperiod fixed effects in column (2) and productfirm and productdestinationperiod fixed effects in columns (4) and (6). , and denote significance at the 1, 5 and 10% level, respectively. Standard errors are clustered at the firm-level, and firmproduct level in columns (2)-(4)-(6)

Results in Fig. 1 show that total imports of firms exposed to the Chinese lockdown have dropped after January 2020. These results thus justify our interpretation of the early lockdown in China as a (temporary) shock to French firms’ input purchases. In the next section, we investigate the propagation of this supply shock along GVCs by studying the dynamics of domestic and export sales, as a function of firms’ exposure to the Chinese lockdown. We will do so in the context of a differences-in-differences estimation, using the early lockdown in China as a quasi-natural experiment. Several factors complicate identification of the transmission of the supply shock. First of all, the “control” firms are not necessarily immune from the shock. Their suppliers may have been exposed to supply chain disruptions from China. By the same token, firms we dubbed as treated may as well be indirectly exposed. Since the empirical strategy focuses on a relatively short window, the analysis is implicitly based on the premise that a direct exposure has earlier and stronger consequences on firms’ input purchases than any indirect exposure. As such, our estimates recovered from the comparison of firms directly hit by the Chinese slowdown with firms that may be indirectly affected should be interpreted as a lower bound of the actual impact of the shock. Second, control firms are also affected by subsequent supply shocks affecting other input providers. Our identification strategy is indeed based on the timing of these shocks but one should keep in mind that all firms ultimately end up being “treated” one way or another. These subsequent shocks affecting control firms more than treated ones, they should play against us finding any difference in the dynamics of sales in the differences-in-differences framework. Third, the Covid crisis entails a combination of supply and demand shocks. Our identification uses the timing of the supply shocks but firms in our sample also had to cope with a series of bad demand shocks. The extent to which concurrent demand shocks impose a threat to the identification strategy is not entirely clear though, because treated and control firms are both exposed to these shocks, which in turn depend on their portfolio of clients around the world. As explained later, we will use the granularity of our data to control for heterogeneous demand shocks using fixed effects.13

Firm-level transmission along the supply chain

This section shows that the shortage of Chinese inputs, which followed China’s early lockdown, had a negative impact on the domestic and export sales of French firms that rely on these inputs. We first discuss the economic magnitude of the effect, before digging into the mechanisms of the adjustment. Sections A.3 and A.4 in the Appendix present a systematic robustness analysis to alternative specifications and discuss the heterogeneity of the transmission among treated firms.

Baseline results

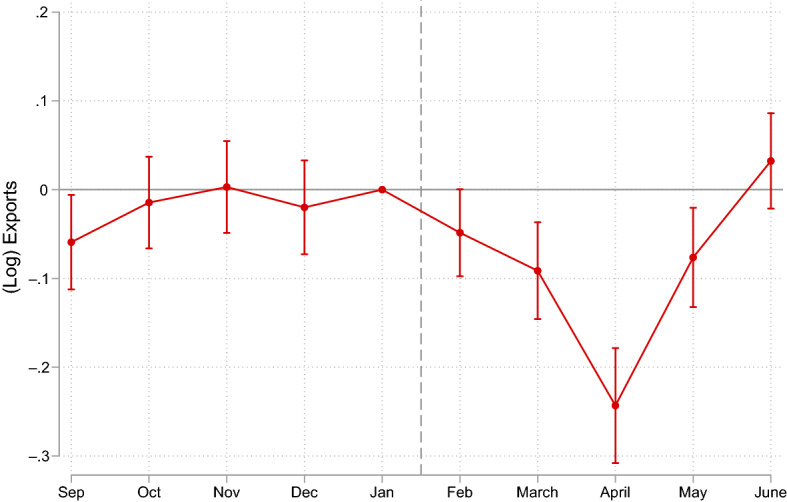

We compare the evolution of firm-level exports before and after the Chinese lockdown for firms directly exposed to the Chinese lockdown and firms in the control group. We use the same exposure variable as in the previous section, which takes the value of one for any French firm having imported inputs from China between September 2019 and January 2020. The control group is composed of French exporting firms that also imported inputs in this period but not from China. To investigate the dynamics of the adjustment of exposed firms, we use a dynamic differences-in-differences design, using firm-level (log) exports as the dependent variable and control for firm and time specific trends using fixed effects.

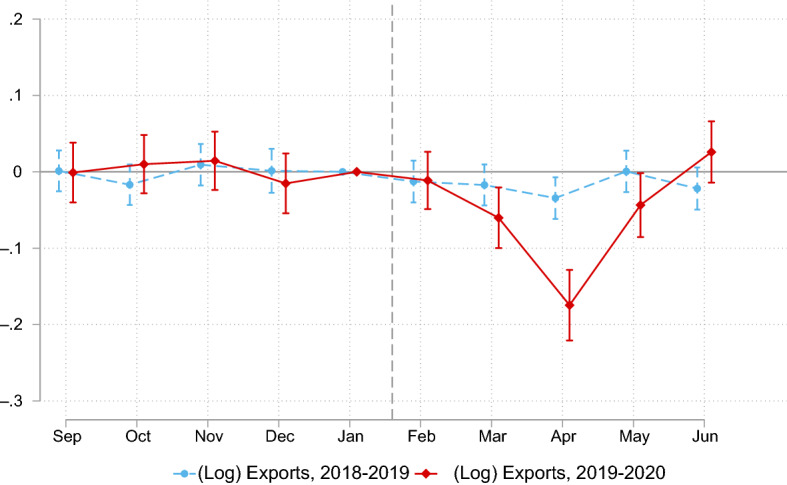

The time pattern of the relative (log) level of exports of treated firms is presented in Fig. 2, red line. We cannot distinguish between the export trends of treated and control firms before the Chinese lockdown. Exports of exposed firms then dropped abruptly relative to the control group in March and April 2020. The effect is transitory and the difference between the two groups’ exports is no longer significant from May 2020. In unreported results, we have extended the sample until December 2020 but did not find any sign of the two groups of firms diverging again later in the year. For comparison purposes, the dynamics of exports before and after the early lockdown in China is compared with the dynamics observed one year before (blue line). The comparison confirms that the dynamics observed post-lockdown is not due to the specific seasonality of exports for firms sourcing their inputs from China.

Fig. 2.

Impact of the Chinese lockdown on firm-level exports. Notes: The figure shows the dynamics of exports before and after the Chinese lockdown, for treated firms in comparison with the control group. Standard errors are clustered at the firm level. Confidence intervals are defined at 5%. Treated firms are those importing intermediate inputs from China prior to the shock. Control firms are importers not exposed to China. The estimated equation has firm and period fixed effects. The red line covers the period from September 2019 to June 2020. The blue line reproduces the same specification based on data from September 2018 to June 2019

We confirm the adverse impact of the Chinese lockdown on exports in various differences-in-differences estimations in Table 2. For comparison purposes, we first estimate the differences-in-differences model using the firm’s imports as left-hand side variable, before quantifying the propagation to the firm’s downstream partners. Column (3) thus corresponds to the DiD specification surrounding the results in Fig. 2. Overall, between February and June 2020, exports of exposed firms declined by 5% more than in the control group.

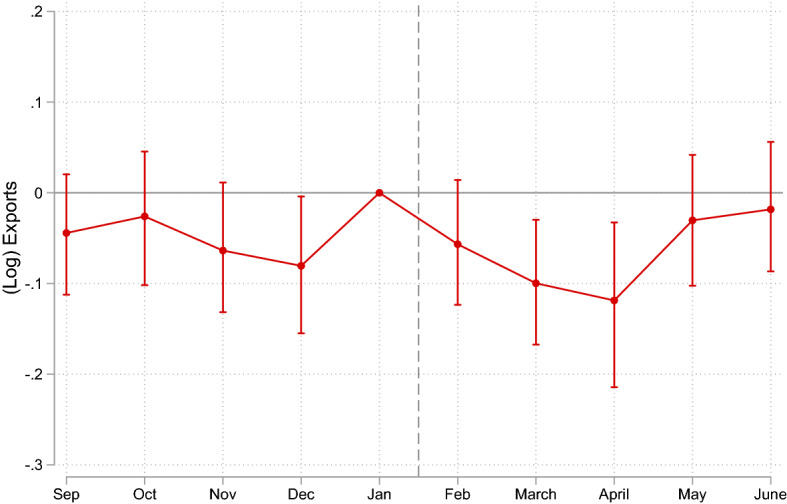

Column (4) further exploits the granularity of the data by estimating the effect of the treatment on exports at the firm–product–destination level. The upside of this specification is that it allows us to use product–destination–time fixed effects to control for monthly demand shocks in each market that are common to control and treated firms. For instance, differences in the rise of cases or in the adoption of containment measures may induce heterogeneity in the dynamics of exports across destinations. For firms sourcing inputs from China, export sales of a given product within a given destination have dropped by 3.5% after the Chinese lockdown, a smaller drop than in the baseline specification (−5%). One possible interpretation of the dampening is that the firm-level results capture extensive adjustments (the drop of destination-product pairs), which are neglected when we work at the firm–product–destination level. We come back to this issue when discussing the different adjustment margins of firm-level exports in Sect. 3.2. One may wonder the extent to which the export adjustment comes from a substitution away from foreign markets, to preserve the firm’s domestic market share. In column (5), we thus investigate how the supply chain disruption affects domestic sales, recovered from the firms’ VAT statements.1415 The general pattern is very similar for domestic sales as for foreign sales. Between February and June 2020, domestic sales have dropped by 5.5% in the treatment group in comparison with the control, with a negative peak in April. In unreported results, we found that the domestic to overall sales ratio did not adjust after the shock. Together, these results suggest that the drop in exports is not mostly attributable to a substitution away from foreign markets to maintain the firm’s domestic market share.

A natural question, that is particularly salient given inflationary pressures observed in 2021–2022, is the extent to which supply chain disruptions translate into higher prices. We investigate this question using export prices as an outcome variable. Results are reported in the last column of Table 2. In contrast with what would be expected, export prices of exposed firms have decreased after January 2020, although the average effect is very small, at −0.7%.16 In Section A.4 in the Appendix, we dig deeper into this result and show that the average (small) effect hides important heterogeneities across sectors.

Overall, these results thus confirm a significant transmission of the shock to input purchases on firms’ exports and domestic sales. Section A.3 in the Appendix provides an extensive robustness analysis of these baseline results. We first discuss how results vary with alternative definitions of the treatment and control groups. We then show that an alternative estimation based on a matching algorithm gives similar results. Finally, we conduct two placebo exercises. These are meant to provide support for our interpretation of the relative drop in exports as being the result of the transmission of the shock along the supply chain rather than the consequence of a global shock or country-specific seasonal patterns in trade data. These results support our interpretation that the dynamic of export sales following the early lockdown in China is consistent with a transmission of the shock along the firm’s value chain.

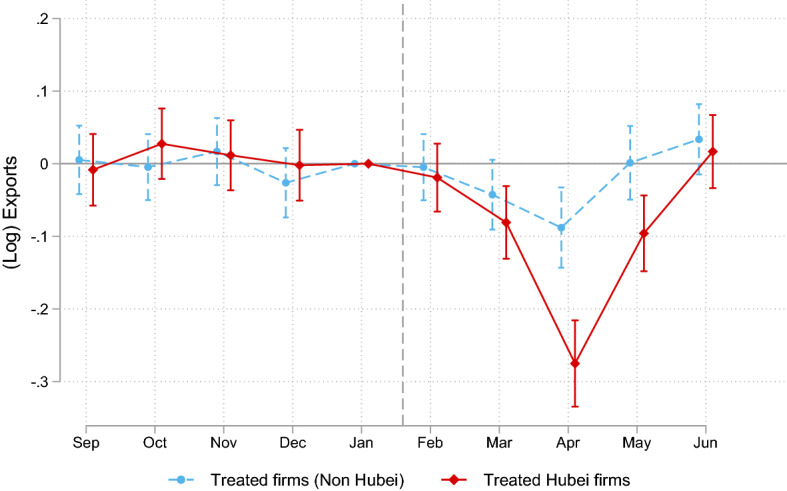

In Section A.4, we dig more into the heterogeneity of the transmission across treated firms. More specifically, we test for heterogeneous treatment effects depending on the firm’s sector of activity, size bin or degree of exposure to Chinese inputs. We do not find evidence that more exposed firms, as measured by the contribution of Chinese inputs to the firm’s overall input purchases, display stronger adjustment patterns. This result is consistent with anecdotal evidence that even a relatively marginal component can induce severe productive disturbances when missing. What appears to be affecting the level of the adjustment is the degree of exposure to products which production is concentrated in the Hubei, the first region entering into a stringent lockdown. Results in Section A.4 also suggest that the transmission to downstream partners is exacerbated for large and export-intensive firms. This result echoes those in Bricongne et al. (2021) who show large firms have played a specific role during the Covid-induced trade collapse. Finally, adjustments are found larger for final consumption producers, most notably in the apparel and footwear and the perfumes and soaps industries. A possible reason is that trade in intermediates is more strongly gathered within long-term contractual relationships. Still, the adjustment is also significant for firms that sell intermediate products, which points to second-tier propagation to downstream firms.

Adjustment margins

The importance of the extensive margin

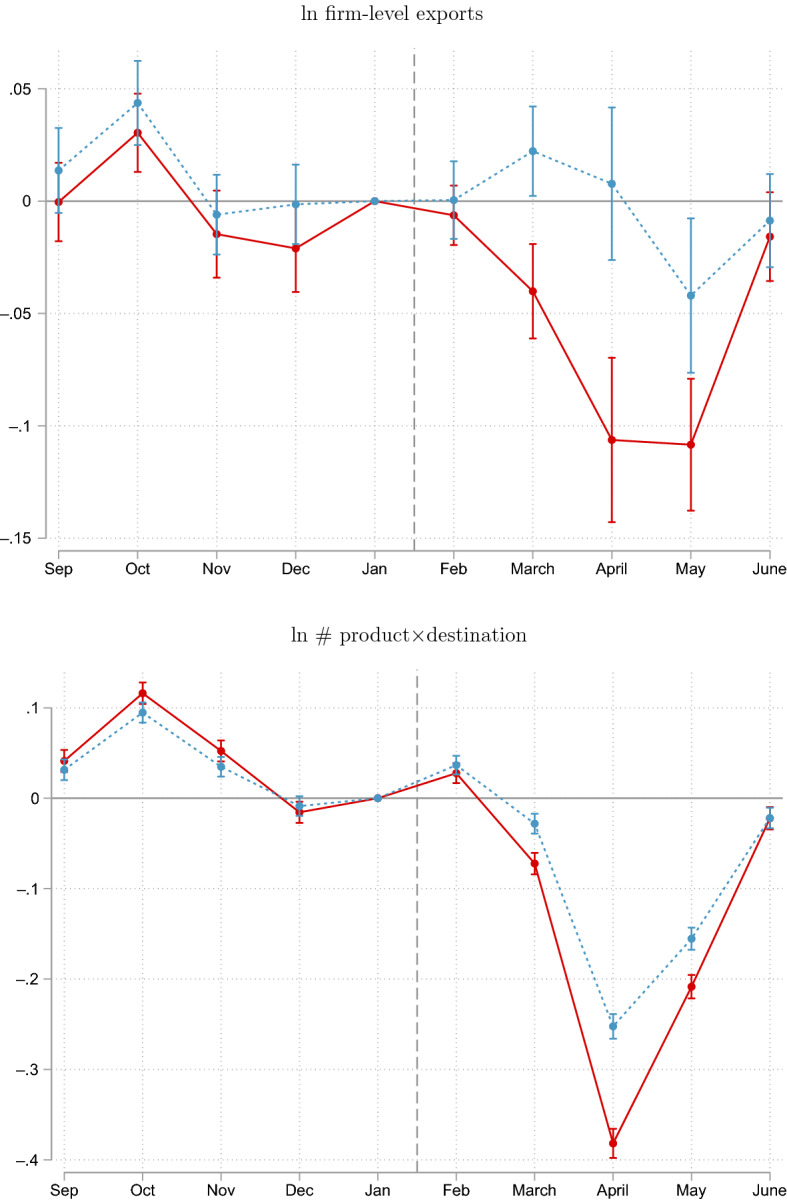

Having discussed the magnitude of the shock transmission to firms’ downstream partners, we now dig into the mechanism of the adjustment. Table 3 decomposes the adjustment of firms’ exports after the Chinese lockdown into different margins. In columns (2) and (3), exports are broken down into the value of exports per destination and the number of destinations. In columns (4) and (5), the decomposition involves the value of exports per product and the number of products. Finally, columns (6) and (7), respectively, display results based on the value of exports per product–destination and the number of product–destination pairs.

Table 3.

Margins decomposition of differences-in-differences results

| Baseline | Destination | Products | Product × Destinations | Firm | ||||

|---|---|---|---|---|---|---|---|---|

| Int | Ext | Int | Ext | Int | Ext | |||

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | |

| Treatment × Post | −0.050 | −0.010 | −0.040 | −0.003 | −0.046 | 0.004 | −0.054 | 0.004 |

| (0.011) | (0.010) | (0.004) | (0.010) | (0.005) | (0.009) | (0.005) | (0.003) | |

| Firm FE | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Time FE | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| # Treated | 12086 | 12086 | 12086 | 12086 | 12086 | 12086 | 12086 | 12086 |

| # Control | 13563 | 13563 | 13563 | 13563 | 13563 | 13563 | 13563 | 13563 |

| # Obs. | 202,622 | 202,622 | 202,622 | 202,622 | 202,622 | 202,622 | 202,622 | 256,490 |

| 0.856 | 0.784 | 0.918 | 0.824 | 0.899 | 0.785 | 0.927 | 0.481 | |

Columns (1)–(7) use the log of the firm’s exports (1), or one of its component (2-7), as left-hand side variable. “Int” denotes the intensive margin, whereas “Ext” is the extensive margin. Column (8) corresponds to a linear probability model of the likelihood that the firm exports. All variables are at the firm and period level. All specifications include firm fixed effects and time fixed effects. The treatment group is made of firms importing from China at least once before the treatment. Standard errors in parenthesis are clustered at the firm-level

All specifications point toward the same direction. Export adjustments occur along the extensive margin, whereas the effect of the treatment is not significant at the intensive margin. Firms sourcing inputs from China have reduced the number of products and the number of destinations they serve after the Chinese lockdown. The result on extensive adjustments at the product margin is consistent with the literature on multi-product firms showing that firms adjust to shocks by changing their product mix (see, e.g., Mayer et al. 2021). To our knowledge, this paper is, however, the first one to show evidence of adjustments to temporary supply shocks through the extensive margin.

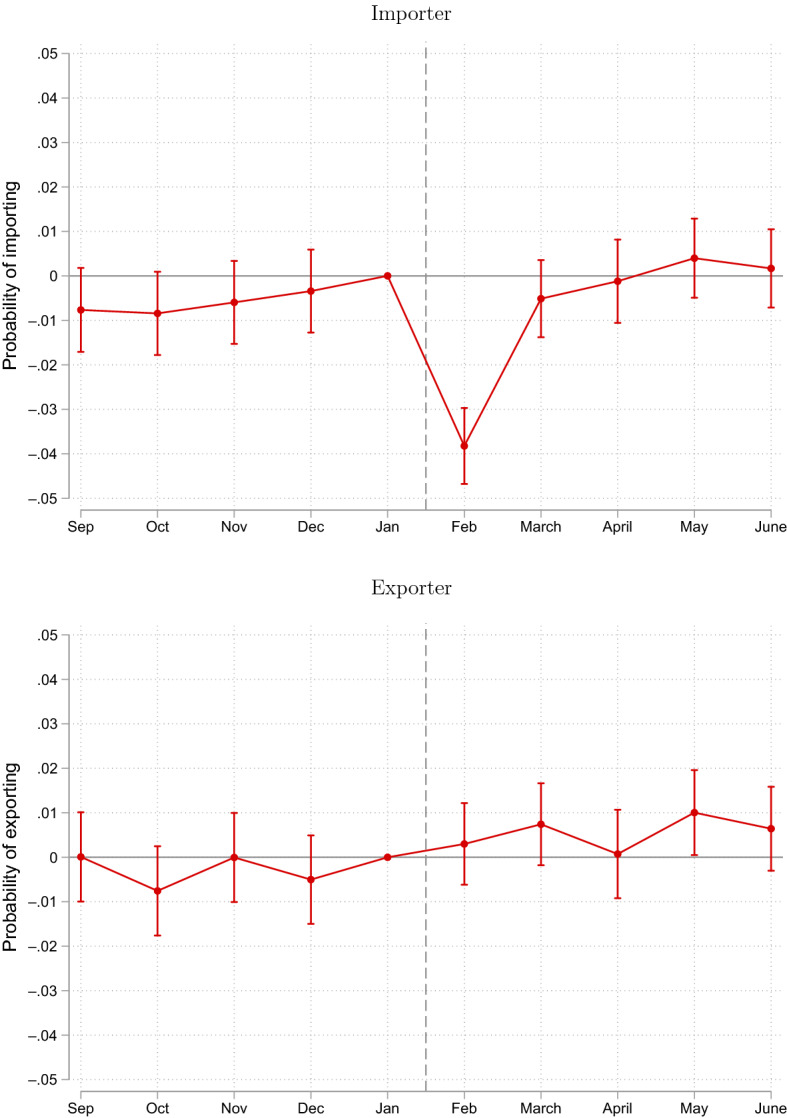

The last column in Table 3 complements the analysis with a model investigating extensive margin adjustments at the firm level. Up to now, the analysis has indeed been restricted to firmperiods with strictly positive exports. We estimate the probability that firms remain active on export markets before and after the shock.17 The effect is positive but not significant, suggesting that treated firms are equally likely to drop out of export than firms in the control group. As shown in Fig. A.14 (bottom panel), coefficients estimated period by period are never significant.

Fig. A.14.

Impact of the Chinese lockdown on the probability of staying as an... Note: Same specification as in Column (7) of Table 4 of the paper. The estimated equation reads: with that is equal to one when firm f displays strictly positive imports (top panel) or exports (bottom panel) in period t. Standard errors are clustered at the firm level. Confidence intervals are defined at 5%

A short-lived effect

Figure 3 shows the dynamics surrounding the specifications in Columns (6) and (7).18 Consistent with the differences-in-differences results, there is little action along the intensive margin. We find that the adverse impact of the shock on the treatment group has been short-lived on the extensive margin, in the sense that there is no statistical difference in the number of markets served by control and treated firms from June 2020. While the numbers are indicative of the relative persistence of the shock, we verified in separate regressions on treated and control firms that the various margins rebounded to their pre-shock level by June 2020.19

Fig. 3.

Impact of the Chinese lockdown on firm-level exports: Intensive versus extensive adjustments. Note: The figure shows the results of the event-study estimation, using the intensive and extensive components of firms’ exports as left-hand side variable. The corresponding difference-in-differences estimates are summarized in Table 3, columns (6) and (7). All specifications include firm and period fixed effects. Standard errors are clustered at the firm level. Confidence intervals are defined at 5%

Heterogeneity across markets

We now explore heterogeneity in these extensive adjustments along the distribution of markets composing a firm’s portfolio. More specifically, we distinguish core and secondary markets and occasional versus frequent markets. For each firm, a “Core” market is defined as the main destination of exports, in the five months before the shock. A “Frequent” market is instead a market served each single month during this period. Like above, market is used as a broad term to designate products, destinations and productdestination pairs. To test whether the above extensive adjustments are driven by some specific markets, we estimated triple differences linear probability models.20 The double difference dimension is similar to the baseline model: we estimate the probability that a particular market stops being served after the beginning of the Chinese lockdown for treated versus control firms. The triple interaction term allows us to estimate whether the relative probability to remain active in a market in the post-period, for treated relative to control firms, varies within a firm, across its core vs secondary markets, or across its frequent versus occasional markets.

The corresponding results are reported in Table 4. The negative coefficients on the TreatedPost-interaction confirm that treated firms were less likely to remain active on a market after the shock. However, the extensive margin adjustment is more pronounced in secondary than in core markets, as shown by the positive coefficient on the TreatedPostCore. Whereas we do find some evidence that the extensive adjustment is also more pronounced on occasional than on frequent markets, the result is not robust across the definition of what a market is.21 Overall, the finding that extensive margin adjustments are more pronounced towards treated firms’ secondary markets is consistent with a model in which firms facing input shortages try to preserve their core relationships. Another (complementary) explanation is that input shortages have affected only a subset of products that are sold on secondary markets.

Table 4.

Digging into the extensive adjustments

| Destinations | Products | ProductDestinations | ||||

|---|---|---|---|---|---|---|

| Core | Frequent | Core | Frequent | Core | Frequent | |

| (1) | (2) | (3) | (4) | (5) | (6) | |

| Post X | −0.066 | −0.106 | −0.150 | −0.093 | −0.169 | −0.137 |

| (0.002) | (0.002) | (0.003) | (0.003) | (0.003) | (0.004) | |

| Treated Post | −0.012 | −0.006 | −0.012 | −0.003 | −0.011 | −0.004 |

| (0.002) | (0.002) | (0.003) | (0.002) | (0.004) | (0.003) | |

| Treated Post X | 0.012 | 0.013 | 0.020 | 0.003 | 0.010 | −0.007 |

| (0.003) | (0.003) | (0.005) | (0.005) | (0.005) | (0.007) | |

| FirmMarket FE | Yes | Yes | Yes | Yes | Yes | Yes |

| MarketTime FE | Yes | Yes | Yes | Yes | Yes | Yes |

| # Treated firms | 12,732 | 12,732 | 12,732 | 12,732 | 12,709 | 12,709 |

| # Control firms | 15,026 | 15,026 | 15,026 | 15,026 | 14,977 | 14,977 |

| 0.476 | 0.477 | 0.489 | 0.490 | 0.483 | 0.484 | |

| # Obs. | 3,101,445 | 3,101,445 | 6,006,836 | 6,006,836 | 20,425,493 | 20,425,493 |

| # Obs. Treated | 1,853,612 | 1,853,612 | 3,979,596 | 3,979,596 | 15,108,404 | 15,108,404 |

| # Obs. Treated Post | 917,173 | 917,173 | 1,971,304 | 1,971,304 | 7,524,070 | 7,524,070 |

| # Obs. Treated Post X | 48,988 | 245,733 | 49,058 | 337,426 | 47,414 | 888,311 |

The table shows results of triple-differences linear probability models of the form: with a dummy that is equal to one when firm f displays strictly positive exports in period t in market m. A market can be defined as a destination in columns (1)-(2), a product in columns (3)-(4) or a destinationproduct pair in columns (5)-(6). is one if m is either the core market of firm f (columns (1), (3), (5)) or a market served every month in the pre-shock period (columns (2), (4), (6)). The analysis is restricted to firmmarket pairs that are active at least once in the pre-shock period and firms that stay active in at least one market in the post-shock period

Weathering supply shocks: diversification and inventories

Section 3 has established a statistically significant impact of being exposed to the Chinese lockdown through upstream suppliers on the dynamics of firm-level sales between February and June 2020. Extensive adjustments identified on treated firms are consistent with disruptions in input purchases forcing firms to ration their exports and delay the delivery of some markets. The granularity of our data makes it possible to go beyond this result and examine whether the effect is similar for firms having different strategies in the management of their value chain. The vulnerability of modern value chains to localized supply shocks is often argued to be attributable to mostly two properties of these production organizations: (i) The lack of diversification of production networks and (ii) The absence of inventory buffers in organizations that to a large extent produce just-in-time (Pisch 2020). We now consider these two arguments in turn, testing whether more diversified firms and firms with more inventories have been able to weather the supply chain disruption in the aftermath of the Chinese lockdown.

Diversification to hedge against localized supply chain disruptions

A popular argument in the literature discussing the vulnerability of global value chains is that the lack of diversification of production networks is at the root of the amplification of localized shocks. In this section, we investigate this claim, asking whether the geographic diversification of supply sources helps firms perform better when hit by the Chinese lockdown shock.

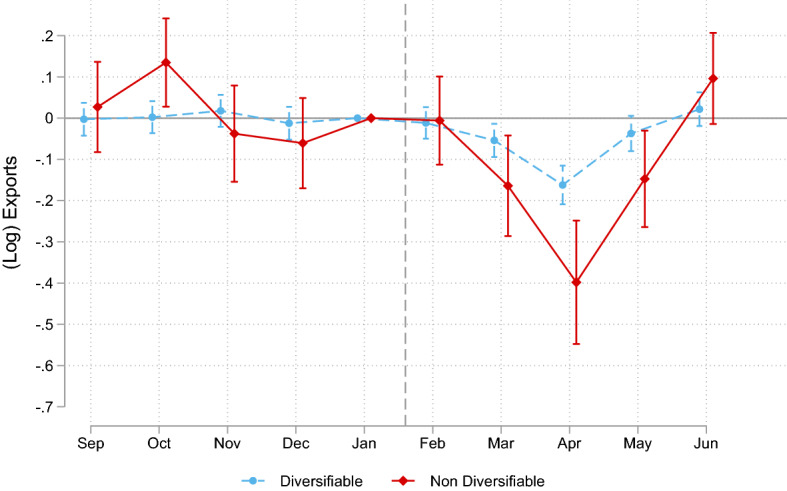

We first examine whether firms that source inputs whose production is concentrated in China has been more severely hit by the shock. We consider that production is concentrated in China if at least 60% of world exports in this product category originate from China.22 We then define a firm as locked-in with China if at least 10% of the value of its imports from China consist of products whose production is concentrated in China. About 5% of treated firms would face major issues to diversify away from China based on this definition. Figure 4 shows that firms importing inputs from China that display such high level of concentration have experienced a more severe drop in their exports than firms importing more diversifiable inputs. This heterogeneity in the strength of the treatment is consistent with the stronger decline in imports of firms purchasing inputs with a high concentration of Chinese production, relative to others (see Fig. A.17).

Fig. 4.

Impact of the Chinese lockdown on firm-level exports: Diversifiable and non-diversifiable firms. Notes: The figure shows the dynamics of exports for treated firms in comparison with the control group. The treatment group is separated into two subsamples. The “Non Diversifiable” group is composed of firms which imports from China include at least 10% on products for which China represents more than 60% of world exports. The “Diversifiable” group is made of firms that import inputs from China that they could source from elsewhere. The estimated equation includes firm and period fixed effects. Standard errors are clustered at the firm level. Confidence intervals are defined at 5%

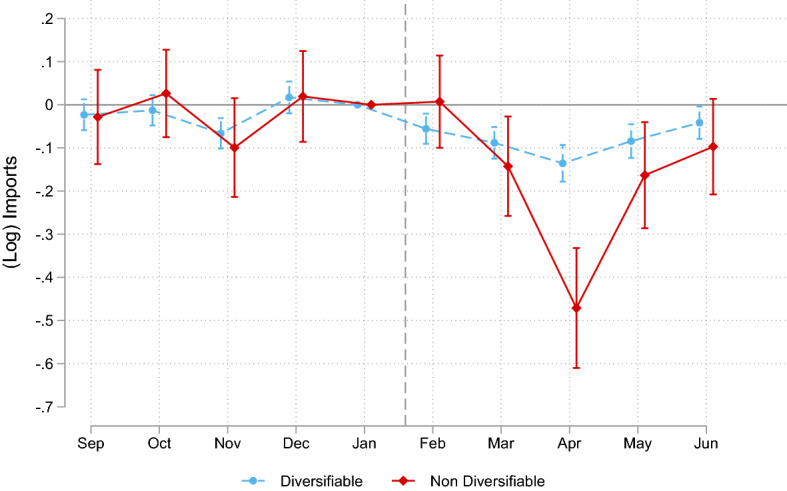

Fig. A.17.

Impact of the Chinese lockdown on firm-level imports: Diversifiable and non-diversifiable firms. Notes: Baseline regression after splitting the treatment group into two subsamples. Treated firms are labeled “diversifiable” if more than 90% of the value of their imports from China cover products for which China displays a world market share below 60%. The estimated equation includes firm and period fixed effects. Standard errors are clustered at the firm level. Confidence intervals are defined at 5%

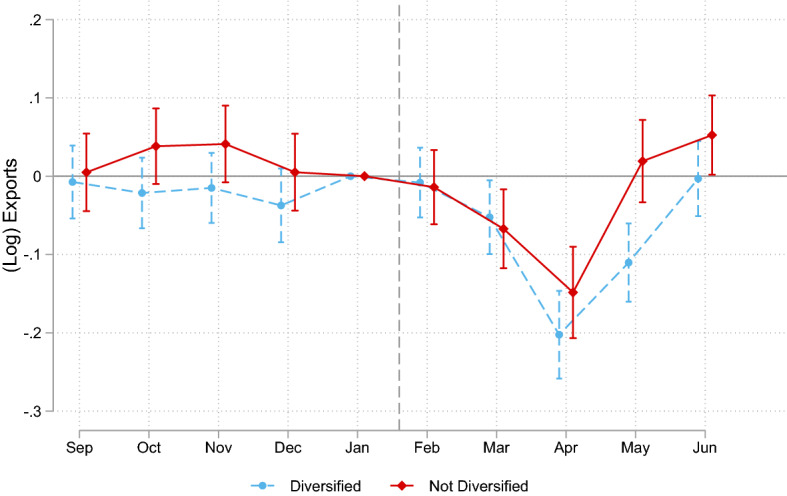

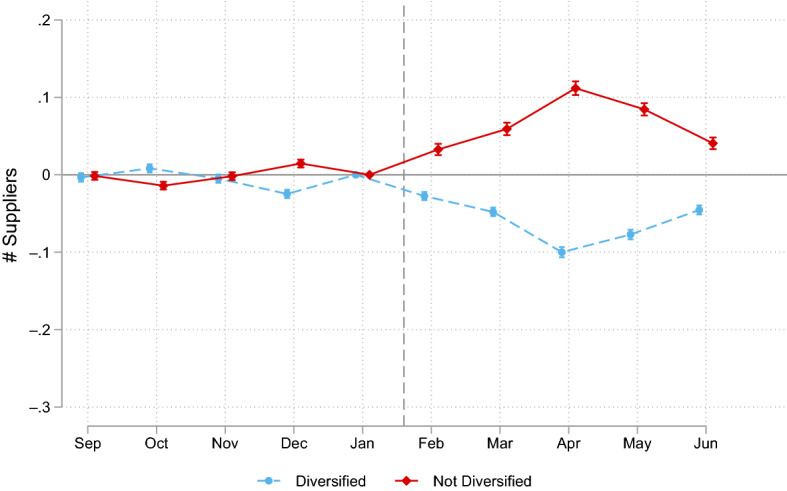

The analysis presented in Fig. 4 shows that firms importing inputs that are difficult to diversify due to the large share of China in worldwide production have been more strongly impacted by the shock. However, 95% of products can be sourced from other countries than China. A natural question is whether firms whose sourcing of inputs is geographically diversified have performed better than the others. To test for this, we define a treated firm as being diversified if it imports its inputs from China and at least one other country prior to the shock. We first tag an input as diversified if it is imported by the firm from more than one country between September 2019 and January 2020. A firm is then diversified if its main inputs (accounting for more than 1% of firm-level imports) are diversified.23 In the baseline sample, slightly more than 40% of treated firms are diversified according to our definition. To test for a role of diversification strategies, we reproduce the baseline estimation, distinguishing between diversified and non-diversified treated firms.

Figure 5 shows the coefficients of this dynamic specification. It appears that among firms exposed to the Chinese shock, ex-ante diversified firms did not perform better than non-diversified.24 Consistent with these results, we found no effect of ex-ante diversification on the adjustment of firm-level imports to the Chinese lockdown (see Fig. A.18).

Fig. 5.

Impact of the Chinese lockdown on firm-level exports: Diversified and non-diversified firms. Notes: Baseline regression after splitting the treatment group into two subsamples. Treated firms are labeled “diversified” if all their main inputs imported from China are also sourced from elsewhere in the pre-period. Main inputs are products accounting for at least of the firm’s imports in the pre-period. The estimated equation includes firm and period fixed effects. Standard errors are clustered at the firm level. Confidence intervals are defined at 5%

Fig. A.18.

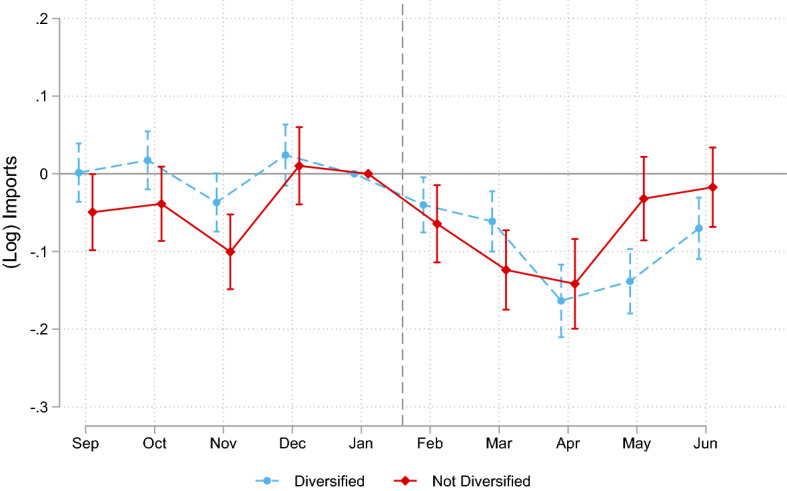

Impact of the Chinese lockdown on firm-level imports: Diversified and non-diversified firms. Notes: Baseline equation in (1) with the treatment group split into two groups. Treated firms are labeled “diversified” if all their main inputs imported from China are also sourced from elsewhere in the pre-period. Main inputs are products amounting to at least of the firm’s imports in the pre-period. The estimated equation includes firm and period fixed effects. Standard errors are clustered at the firm level. Confidence intervals are defined at 5%

At first glance, this result contradicts the premise that the geographic diversification of input purchases can be a useful strategy to insure against localized shocks hitting firms’ supply chain. We now examine several potential reasons for this absence of result.

First, we may not be able to properly identify ex-ante diversified firms. Here, our implicit assumption is that a firm that has interacted in the past with two input suppliers of the same product will be able to increase its demand to non-Chinese suppliers in response to the Chinese input shortage. Implicitly, products sold by Chinese and non-Chinese suppliers are thus considered as substitutes, once we condition on a particular (8-digit) category. In table A2, column (2), we show results recovered from the triple-difference estimation that defines diversified firms based on the diversification of inputs that are classified as non-differentiated by Rauch (1999). Among this subset of inputs, the assumption that inputs from different origins are substitutable is more likely hold. When diversified products are restricted to homogenous products based on the Rauch classification, results go in the expected direction. The relative drop in exports is found larger for treated firms that are not diversified than for diversified firms. However, the focus on non-differentiated products strongly narrows the set of firms that we consider as being potentially diversified and the result is statistically weaker as a consequence.

Table A2.

Impact of the Chinese lockdown on firm-level exports: Diversified and non-diversified firms

| Dep. Var: log of exports | |||

|---|---|---|---|

| (1) | (2) | (3) | |

| Treatment × Post | −0.046 | −0.055 | −0.044 |

| (0.014) | (0.011) | (0.013) | |

| –×–×Div | −0.009 | 0.086 | −0.020 |

| (0.016) | (0.034) | (0.016) | |

| Firm FE | Y | Y | Y |

| Time FE | Y | Y | Y |

| # Treated | 12,732 | 12,732 | 12,732 |

| # Control | 15,026 | 15,026 | 15,026 |

| # Diversified | 5422 | 557 | 4011 |

| 0.853 | 0.853 | 0.853 | |

| # Obs. | 215,530 | 215,530 | 215,530 |

The table reports results of differences-in-differences estimations on exporting firms. Here, treated firms are split into a group of “diversified” and a group of “non-diversified” firms. In column (1), diversified firms are those that import all of their main inputs from at least two countries during the pre-treatment period. In column (2), we focus on inputs classified as “non-differentiated” by Rauch (1999) and call a firm “diversified” if all of its main inputs sourced from China are non-differentiated and sourced from at least two countries in the pre-treatment period. In column (3), “diversified” firms are those that source all of their main inputs from China and an other country of the European Union (EU15), in the pre-crisis period. Standard errors are clustered at the firm level. , and denote significance at the 1, 5 and 10% level, respectively

Another possibility is that the pandemic has constrained firms in their ability to substitute away from China, even when knowing alternative sourcing partners from before. To test whether this could explain our results, we define a third dummy for “diversified” firms based on the subsample of diversified firms from Fig. 5 with former partners in the EU15. The intuition behind is that it was probably easier to reshore input sourcing to partners in the EU at a time when the pandemic started disrupting value chains outside of China. Results are reported in Table A2, column (3). However, the triple interaction is still nonsignificant meaning that ex-ante diversified firms with partners in the EU15 have not performed better ex-post than other treated firms.

Finally, it is also possible that firms that do no diversify ex-ante can benefit from some form of ex-post diversification, by switching to new suppliers once the shock hits. Selection into diversification may actually explain the (lack of) result in Fig. 5 if firms that do no diversify know that the type of inputs they are sourcing from China is easy to purchase in other countries in case of a shock. Again, it is difficult to formally test for this possibility although the results in Fig. 6 provide some support for this interpretation. Namely, Fig. 6 examines differences in extensive margin adjustments by diversified and non-diversified treated firms relative to the control group. We now work at the firmproduct level and consider the number of countries from which firms import a given product before and after the shock. We see a surge in the number of sourcing countries for the ex-ante non-diversified firms when the number drops for diversified firms. Some of the firms that were not diversified ex-ante thus managed to diversify in the aftermath of the shock. For this reason, the ex-ante diversification is not associated with significantly better trade performances in the aftermath of the shock.

Fig. 6.

Ex-ante diversification and the number of firms’ suppliers. Notes: Baseline at the firmproduct level with treated firmproduct pairs split into a “diversified” and “non-diversified” subsamples. The diversified sample corresponds to firms importing the product from China and somewhere else, whereas the non-diversified subsample includes firms that solely import from China. The outcome here is the (log-) number of countries the firm sources the product from. We perform a Poisson regression to account for the extensive margin at its full extent. The estimated equation includes firmproduct and productperiod fixed effects. Standard errors are clustered at the firmproduct level. Confidence intervals are defined at 5%

The ex-post diversification of some of the treated firms raises several questions. First, one may wonder if it means that new relationships are easier to set up for these firms. To approach this point, we have considered an extension of the estimation in which we compare the diversification of products sold on spot markets with the diversification of more differentiated products.25 The rational is again that it is likely to be easier for firms to substitute away from China for products sold on spot markets. We do not find that the ex-post diversification is more pronounced for products traded on spot markets. Another interpretation is that firms have accepted to pay high sunk costs to find new suppliers because they anticipated that the shock would be long lasting. Measuring firms’ expectations about the length of the disruption is not possible given the data at hands. But results from business surveys suggest that at least some firms have anticipated a huge increase in the downside risk on their annual sales, which suggests the shock was perceived as long-lasting (Bunn et al. 2020). The same surveys also show a strong dispersion in firms’ perception of the risk. Whether grounded on unobserved characteristics of the firms or due to different levels of risk aversion, the heterogeneity in the diversification structure of individual firms and their reaction to the shock would be worth exploring in future research.

Inventories as a buffer against input shortages

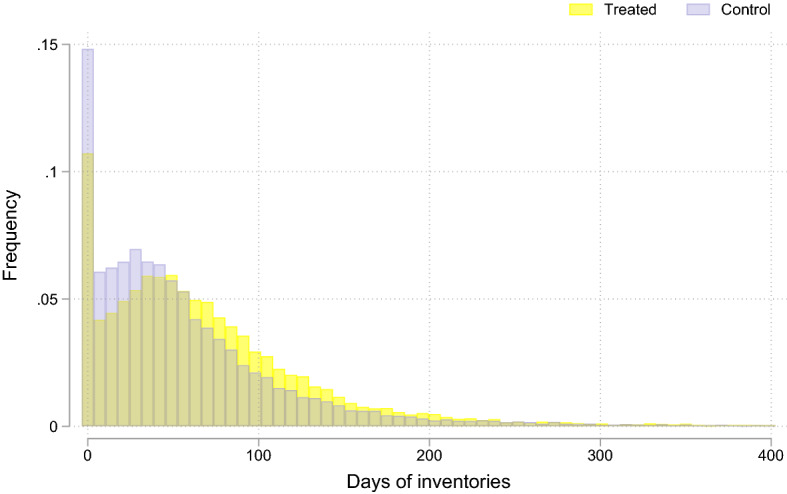

We now investigate the role of inventories in offering a buffer against input shortages. We merge the estimation sample with balance-sheet information provided by the French National Statistical Institute (FARE dataset). The dataset is exhaustive and contains information on the value of firms’ inventories at the end of the accounting year. Using the variable, normalized by the value of the firm’s activity, we obtain a proxy for the average level of inventories held by the firm. There are three caveats associated with the use of these data. First, the last year of data availability is 2018 and we will thus focus on firms in the estimation dataset that were already active in 2018 – more than 90% of the sample. Second, the inventory variable does not distinguish between inputs and output.26 Third, inventories are measured at the end of the accounting year (December for 3/5 of the firms, March, June or September for the rest), and they may not be representative of inventories during the rest of the year.

We first define a dummy for firms displaying a relatively high level of inventories in 2018. Under the assumption that inventory strategies are relatively smooth and persistent over time, these firms should also be less exposed to disruptions induced by input shortages in early 2020 thanks to their inventory buffer. The dummy variable is defined into two steps. First, we construct a measure of the level of inventories, defined by the value of end-of-the-year inventories, divided by the value of the firms’ yearly sales, times 365. The ratio can be interpreted as the average daily production held in inventories. Figure 26 in the Appendix shows the distribution of this variable in the estimation sample. Heterogeneity in the level of inventories is significant, in particular across firms in different sectors.27 In the analysis, we focus on the heterogeneity within a sector and define as high-inventory a firm which ratio of inventories over sales falls in the fifth quintile of its sector-specific distribution.28

Fig. A.19.

Distribution of inventory ratios in the estimation sample. Notes: The figure shows the distribution of firms’ inventories-to-sales ratios, in the estimation sample, for treated and control firms. Source: INSEE-FARE for 2018, merged with the customs data

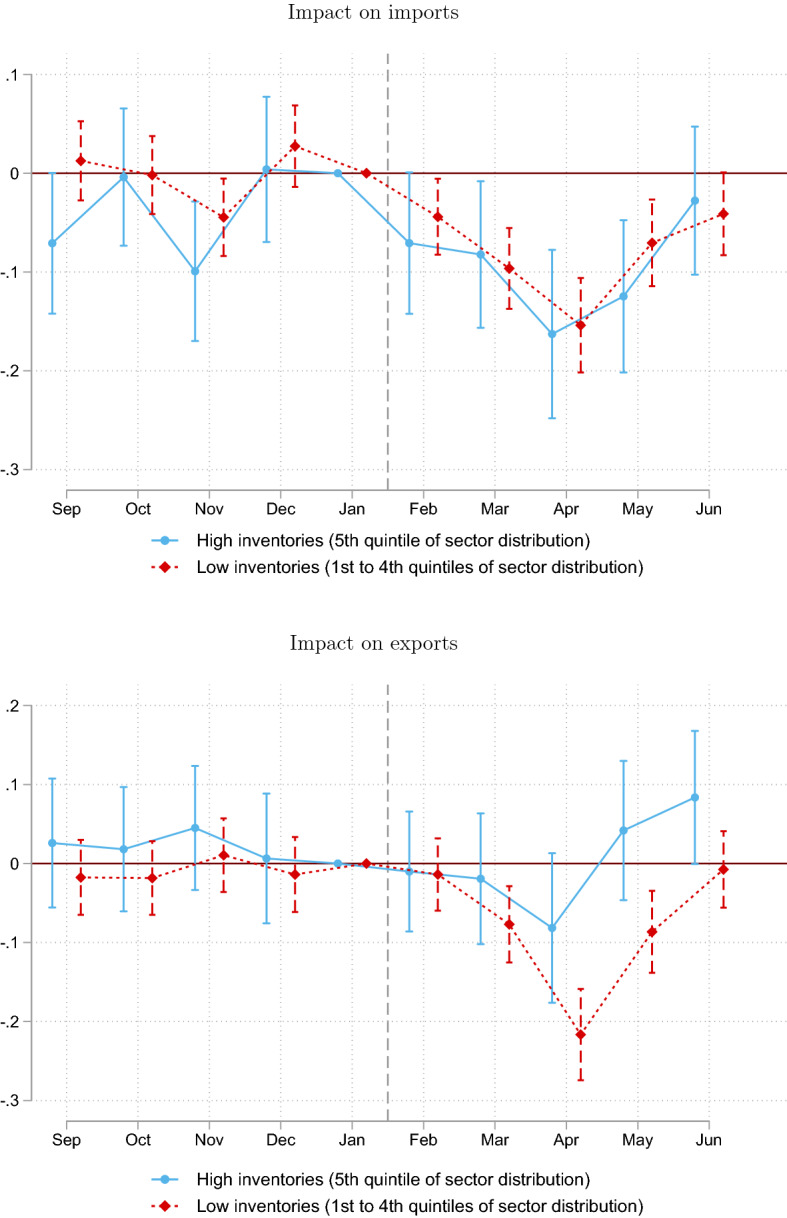

Results are displayed in Fig. 7. They are based on a variant of the dynamic differences-in-differences specification, using either the log of imports (upper panel) or the log of exports (bottom panel) as left-hand side variable and distinguishing between the dynamics of trade of high-inventory and low-inventory firms. The dynamics of imports is not significantly different in both groups, and is very similar to Fig. 1, which suggests that firms holding larger inventories were not the most exposed to the shock. We expect the role of inventories to materialize into an heterogeneous transmission of the shock to the rest of the value chain as firms with more inventories can keep on serving their downstream partners, even when facing an input shortage. It is indeed the dynamics observed in the bottom panel of Fig. 7. For firms with a high level of inventories, the dynamics of exports is not significantly different in the treatment and the control groups. Instead, firms exposed to the Chinese lockdown displaying low levels of inventories see their exports decline in relative terms with respect to unexposed firms. Although the period-by-period estimates are a bit noisy, a triple difference estimation confirms that the relative drop in exports among treated firms with low and high inventories is significantly different (coefficient estimated at .0532 with a standard error at .0268 implying significance at 5%).

Fig. 7.

Impact of the Chinese lockdown on firm-level exports: Low- and high-inventory firms. Notes: The figure shows the results of a dynamic differences-in-differences estimation, distinguishing between firms with high inventories, as defined by a ratio of inventories over sales larger falling in the fifth quintile of the firm’s sector-specific distribution, and the rest of the estimation sample. All coefficients interpret in relative terms with respect to firms in the control group that would display comparable inventory-to-sales ratios. The estimated equation has firm and period fixed effects. Standard errors are clustered at the firm level. Confidence intervals are defined at 5%

To our knowledge, such evidence of a heterogeneous transmission of the supply chain shock to the rest of the value chain among firms with different levels of inventories is new. These results offer empirical support to the statement that holding more inventories can be an efficient strategy to cover against (short-lived) supply chain disruptions.

What is the external validity of this result? The early Chinese lockdown starts at the end of January 2020 and we cannot exclude that firms hit by the crisis were by chance particularly well equipped to handle the supply chain disruption because of a relatively high level of inventories during this period. This concern is particularly legitimate given the seasonality of imports from China discussed in Section A.2. Since Chinese exports tend to slow down at the beginning of the year, firms importing from China may be used to accumulate inventories around these dates. Whereas this possibility cannot be ruled out in the absence of high-frequency data on inventories, it is unlikely that the seasonality of inventories entirely explains the above-mentioned results. First, firms had no incentives to accumulate inventories beyond what was expected to be optimal given the seasonality of Chinese shipments. Second, the result of inventories offering an efficient buffer against the shock is recovered from the comparison of treated firms with relatively high or low levels of average inventories, in 2018. The comparison conveys useful information beyond and above the overall impact of importing from China on firms’ inventory management.

Conclusion

This paper uses detailed firm-level data to gauge the transmission of supply shocks along global value chains. We find French firms sourcing inputs from China just before the early lockdown in the country experienced a drop in imports between February and June 2020 that is 7% larger than firms sourcing their inputs from elsewhere. This shock on input purchases transmits to the rest of the supply chain through exposed firms’ domestic and export sales. Between February and June, firms exposed to the Chinese early lockdown experienced a 5% drop in exports and a 5.5% drop in domestic sales, relative to French firms importing from other countries. The relative drop in export sales is entirely driven by the volume of exports, whereas export prices do not seem to adjust. Moreover, the adjustment is attributable to the extensive margin with firms temporarily rationing their exports in some (secondary) markets.

We then assess the role of risk management strategies in mitigating such supply shocks. We find firms diversifying the sources of their inputs before the shock have not performed better than others. Indeed, firms that were not diversified managed to find new suppliers in the aftermath of the shock. Unlike diversification, we find firms holding more inventories before the shock performed better than other firms exposed to the same supply chain disruption. This result confirms the popular idea than stockpiling may be an efficient buffer against supply chain disruptions.

Trade disruptions in GVCs such as the one induced by the early lockdown in China are not anecdotal. Semiconductors shortages have started to affect GVCs by the end of 2020, and supply chains disruptions are now reported for other critical materials.29 Whereas less easy to trace out, understanding how firms adjusted to this accumulation of input shortages during a long-lasting crisis that saw a surge in uncertainties is likely to be especially informative regarding the functioning of global value chains, from both a positive and a normative points of view.

Appendix

A. 1 Data Appendix

The empirical analysis mostly uses French customs data between September 2019 and June 2020. The dataset is constructed from the raw customs forms filled by French firms and made available to us by the French customs. The final dataset is constructed from four types of customs forms depending on whether the firm declares an export or an import flow and whether the partner country belongs to the EU or not. The combination and treatment of these files is described in details in Bergounhon et al. (2018).

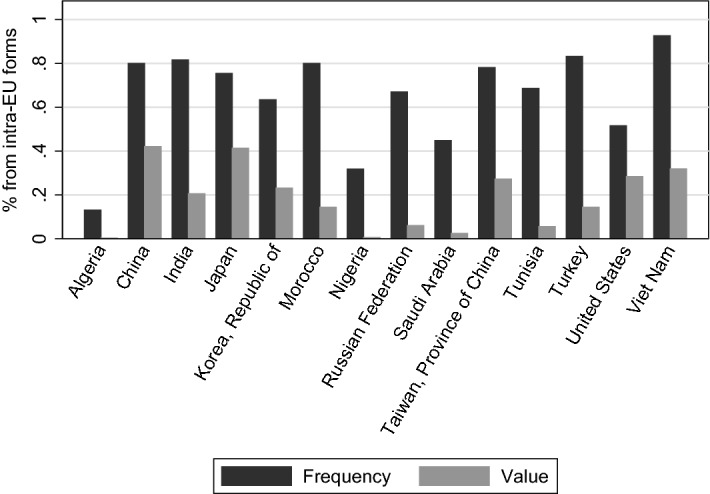

An important technical step in the process of constructing the final dataset concerns the treatment of imports originating from extra-EU countries that are intermediated by a third EU country before entry into France. This step is particularly important quantitatively as 80% of transactions accounting for almost half of the value of French imports from China are recovered from intra-EU customs forms. When the product enters Europe through another European country, say the Netherlands or Belgium, two countries that host major cargo ports, it is fairly common that two customs forms are filled. A first customs form, which is not part of our database, records the trade flow from China to the point of entry. A second customs form covers the intra-EU flow up to France and is thus included in our data. Thankfully, the second form keeps information on the origin of the good, which makes it possible to count the second flow as imports from China. Throughout the analysis, we treat all import forms so that the country of origin is systematically the first country at the root of the trade flow, China in our example. Figure A.1 shows the importance of this treatment across bilateral trade flows for 2019.

Fig. A.1.

Share of transactions and the value of imports from non-European countries recovered from intra-EU trade data. Notes: The figure shows the share of transactions and of the value of imports from one of the 15 largest non-European partners of France that is recovered from intra-EU trade data

Whereas the raw data offer a solution to treat the problem of intermediated trade flows, it is still tricky to measure the mode of transportation for the corresponding trade flows. The reason is that the only recorded transport mode corresponds to the last segment of the product journey. As is the case for the vast majority of intra-EU trade flows, the corresponding import flow is likely to be associated with a road transport mode. When the product enters France from Belgium or the Netherlands, it is quite likely that the good was shipped from China to Europe on a cargo. There is more uncertainty regarding the mode of transportation when the product enters France through Germany, the third most likely point of entry. Germany hosts large logistic companies that may intermediate trade using both maritime and aeronautic modes of transportation. However, one would expect that a product that has been imported from China to Germany by air would also travel from Germany to France by air, in which case the recorded transportation mode is still correct. Given this uncertainty, the best we can do is to keep information on goods entering France by air, whether directly or indirectly. The vast majority of goods that do not fly from China to France are shipped on cargos, with a delay of roughly one month between the time when the products are put onto the cargo and the date of the customs clearance in Europe.30

A.2 The early lockdown in China as a natural experiment

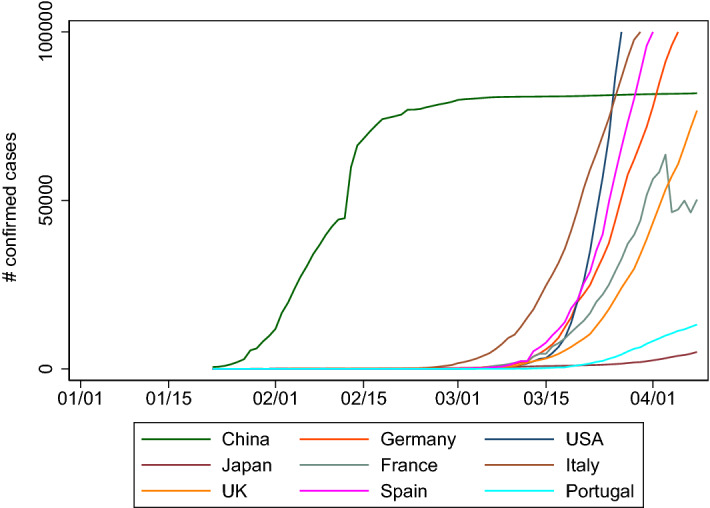

Figure A.2 illustrates the discrepancy in the rise of confirmed Covid cases across countries. Whereas most countries have been hit by the pandemic in the first half of March, China has been hit earlier in January 2020. As a consequence, China has been the first country to impose a severe lockdown, in the Hubei region from January 23rd. In other countries, government responses came later, at the end of February or the beginning of March.31 The rise in the number of cases and the containment policies have led to early production disruptions in China. Like Eppinger et al. (2021), we exploit this one-month lag to separate in the data the impact of the productivity slowdown in China from the general drop in productivity induced by the pandemic.

Fig. A.2.

Spread of the pandemic: number of confirmed cases for a selection of countries. Source: Oxford COVID-19 Government Response Tracker

A first hint that this one-month delay has had consequences on French firms is illustrated in Fig. A.3, which compares the monthly evolution of French imports from China and from the rest of the world.32 Whereas the value of imports from the rest of the world was stable in February 2020, it decreased by almost 10% for imports originating from China. Imports from the rest of the world instead started to decrease in March, when imports from China were already close to their lowest level. During the Spring 2020, the evolution of imports from China and from the rest of the world is more synchronized. It is only in the Fall that the two series start diverging again, due to the second wave affecting most European and American countries when the situation was much more under control in China. Importantly, the early contraction of imports from China is not innocuous from the point of view of the French economy as China is the second most important source of imports.33

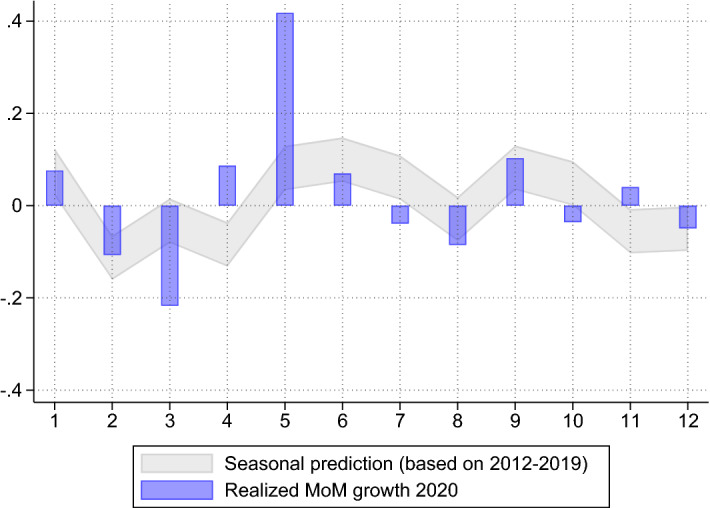

International trade displays important seasonal patterns, and the seasonality is in part country specific. One may thus wonder the extent to which the relative drop in imports from China observed in February and March 2020 is not a consequence of the specific seasonality of trade with China. Figure A.4 compares the monthly growth of imports from China in 2020, against the seasonal component of monthly growth estimated using data from 2012 to 2019.34 The relative drop in imports observed in February 2020 may be attributable to the normal seasonality of trade. The 20% drop observed between February and March is instead significantly larger than historical seasonal variations, as is the recovery in March and April.

Fig. A.4.

Actual versus predicted monthly growth of Chinese imports. Source: French customs, import files. The figure shows the monthly growth of imports from China in 2020 (blue bars) and the mean monthly growth estimated based on data over 2012–2019

A.3 Robustness

In this section, we test the robustness of our main findings. We first discuss how results vary with alternative definitions of the treatment and the control groups. We then test robustness to the estimation method, using a matching algorithm as an alternative. Finally, we conduct two placebo exercises. These are meant to provide support for our interpretation of the relative drop in exports as being the result of the transmission of the shock along the supply chain rather than the consequence of a global shock or country-specific seasonal patterns in trade data.

First, we replicated all results with an alternative definition of the treatment. In the baseline case, a firm is treated whenever it has imported from China at least once between September 2019 and January 2020. In the alternative definition, we keep the subset of importers that interacted at least once every month during this period. The control group is then composed of similar firms that also display regular ties with their input suppliers, but do not import from China. If any, results recovered from this “T2 Treatment" are stronger than our baseline results (Figure A.5). Overall between February and June 2020, the relative drop in these firms’ exports is estimated at 6.3%.

Fig. A.5.

Impact of the Chinese lockdown on firm-level exports: Monthly importers. Notes: The figure shows the dynamics of exports before and after the Chinese lockdown for treated firms in comparison with the control group. The treatment is based on monthly imports from China between September 2019 and January 2020 (T2) and the control corresponds to monthly importers from a third country and not importing from China. The estimated equation includes firm and period fixed effects. Standard errors are clustered at the firm level. Confidence intervals are defined at 5%

Second, one may worry that firms in the control group are exposed to systematically different supply shocks through their import portfolio. To deal with this issue, we exclude from the control group firms that solely import inputs from EU15 countries. The corresponding firms are small on average and given the degree of integration of the single market in these countries, the extent to which these firms participate to GVCs may be questionable. This restriction removes about six thousands firms from the control group. In an alternative exercise, we restrict the control group to firms importing some of their inputs from less-developed and emerging countries.35 The corresponding control group contains 6,673 firms which imports and exports on average represent 70 and 47% of the average treated firm’s pre-shock trade, respectively. Here as well, the objective is to move the average control firms closer to treated firms, in terms of their import activities. Finally, we also tested with a completely different control group composed of 33,645 non-importers. Here, the rational is to compare treated firms with a group that was not directly exposed to international supply chain disruptions, either in January nor later.

Results of these three exercises are summarized in Fig. A.6. Results obtained excluding firms solely importing from EU countries look very similar to those in Fig. 2, which confirms that the identified transmission of the shock is not attributable to extra-EU imports being more strongly affected by the world trade shock than intra-EU imports. Focusing on firms importing from developing countries as in the bottom panel of Fig. A.6 is costly in terms of the precision of the estimates. The relative drop in exports of treated firms in April 2020 is still significantly negative, although slightly lower. Finally, results recovered using non-importers as controls look very similar as in the baseline.

Fig. A.6.

Impact of the Chinese lockdown on firm-level exports: Alternative control groups. Notes: The figure shows the dynamics of exports before and after the Chinese lockdown for treated firms in comparison with the control group. The treatment is based on imports from China between September 2019 and January 2020. The control group is based on (i) Importers from other countries excluding firms that solely imports from the EU15 (Top Left Panel, 11,720 controls), (ii) Importers from other emerging countries (Top right Panel, 6,673 controls) and (iii) Non-importers (Bottom Panel, 33,645 controls). The estimated equation includes firm and period fixed effects. Standard errors are clustered at the firm level. Confidence intervals are defined at 5%

We then depart from the baseline specification and instead use a matching estimator. We back out propensity scores from a probit model in which we estimate the probability of being treated using the level of imports, the level of exports, the number of destination countries and the number of exported products in each month in the pre-period, as well as the 2-digit industry code of the firm. We keep units with a propensity score between .1 and .9 to ensure sufficient overlap in covariates distribution between treated and controls (see Crump et al. 2009). Armed with these scores, we can match each treated firm with a synthetic “control” based on its nearest neighbor in the population of control firms. We then use a simple inference method based on a generalized differences-in-differences to build the average treatment effect and use subsampling to construct confidence intervals.36 The results presented in Fig. A.7 confirm the negative impact of the Chinese lockdown on the exports of firms importing from China.37 In unreported regressions, we show this result is robust if one compares treated firms to their 4-nearest neighbors, or if we use covariates matching using Mahalanobis’ metric rather than propensity score matching.

Fig. A.7.

Impact of the Chinese lockdown on firm-level exports: Robustness based on propensity score matching and subsampling. Note: Results based on propensity score matching and subsampling. The effect months after the shock is the sample average over treated firms of where is the (observable) outcome for treated firm i and is the average outcome among firms chosen as control i. The nearest neighbor is selected by the propensity score matching. Inference is conducted using subsampling, using 500 repetitions with a tuning parameter (Politis and Romano 1994). Confidence intervals are defined at 5%

These results thus confirm that the estimated impact of the Chinese lockdown on exposed firms’ exports is robust to changes in the definition of the control group. Although the stability is reassuring, identification in these exercises still relies on the comparison of firms that source inputs from China with firms that do not, which may be worrisome in light of the country-specific seasonal patterns characterizing trade data. Although we have already argued that this seasonality is unlikely to fully explain the large relative drop in imports observed on treated firms, one may still argue that it may have consequences for the relative drop in exports. Unfortunately, ruling out this possibility is not straightforward as matching exposed units with firms facing the same seasonality is statistically complex. Our strategy to deal with this issue thus relies on a placebo constructed from pre-Covid data. If seasonality was important in driving the relative drop in exports observed in the treatment group after January 2020, then the exact same pattern would be observed in a placebo treatment group after January 2019. Figure A.8, left panel shows that it is not the case. In 2018-2019 data, the dynamics of exports is the same before and after January, for firms importing from China in relative terms with respect to firms importing from elsewhere. This finding confirms that the dynamics identified in Fig. 2 is specific to the Covid crisis period in early 2020.

Fig. A.8.

Impact of the Chinese lockdown on firm-level exports: Placebo tests. Notes: The figure shows the dynamics of exports for treated firms in comparison with the control group. In the left panel, the treatment is based on imports from China between September 2018 and January 2019 and the placebo date of the treatment is considered to be February 2019. IN the right panel, the treatment is based on import from the USA instead of China. The estimated equations include firm and period fixed effects. Standard errors are clustered at the firm level. Confidence intervals are defined at 5%

Finally, one may also suspect that the identified effect is attributable to the Covid crisis quickly disturbing production processes in complex value chains, which may produce the dynamics in Fig. 2 if firms importing from China are systematically more likely to have sophisticated supply chain structures. Whereas the use of various control groups, including those based on propensity score matching, is meant to control for this possibility, we ran another placebo exercise in which we defined the treatment as importing from the USA. In early 2020, US production was still immune from Covid-related problems. If the results displayed in Fig. 2 is indeed attributable to supply chain disruptions after the early Chinese lockdown, we should not see any difference between treated and control firms once treated firms are defined based on importing from the USA. Instead, if the dynamics of exports is driven by the worldwide disruption of complex value chains in the early stages of the Covid crisis, we shall see a similar pattern in this placebo test as in the baseline case. The right panel in Fig. A.8 shows that it is not the case. Firms importing from the USA do not display a different dynamics of exports than other firms in the first semester of 2020. If any, these firms’ trade patterns start diverging in June 2020, when the Covid crisis was hitting the USA much more severely.

A.4 Heterogeneity across treated firms