Abstract

Aims

Buying and consuming no- (per cent alcohol by volume, ABV = 0.0%) and low- (ABV = >0.0% and ≤ 3.5%) alcohol beers could reduce alcohol consumption but only if they replace buying and drinking higher-strength beers. We assess whether buying new no- and low-alcohol beers increases or decreases British household purchases of same-branded higher strength beers.

Methods

Generalized linear models and interrupted time series analyses, using purchase data of 64,280 British households from Kantar Worldpanel’s household shopping panel, 2015–2018. We investigate the extent to which the launch of six new no- and low-alcohol beers affected the likelihood and volume of purchases of same-branded higher-strength beers.

Results

Households that had never previously bought a same-branded higher-strength beer but bought a new same-branded no- or low-alcohol beer were less than one-third as likely to go on and newly buy the same-branded higher-strength product. When they did later buy the higher-strength product, they bought half as much volume as households that had not bought a new same-branded no- or low-alcohol beer. For households that had previously purchased a higher-strength beer, the introduction of the new same-branded no- or low-alcohol beer was associated with decreased purchases of the volume of the higher-strength beer by, on average, one-fifth.

Conclusions

The increased availability of new no- and low-alcohol beers does not seem to be a gateway to purchasing same-branded higher-strength beers but rather seems to replace purchases of these higher-strength products. Thus, introduction of new no- and low-alcohol beers could contribute to reducing alcohol consumption.

INTRODUCTION

Drinking less alcohol is good for health. Forty-year-old men and women who drink over six UK standard drinks a day (more than about 350 g of alcohol a week) lose 4–5 years of life, compared with those who drink under two standard UK drinks a day (100 g of alcohol or less a week) (Wood et al., 2018). Reducing alcohol consumption, particularly amongst the heaviest drinkers, reduces the chance of dying prematurely (Rehm and Roerecke, 2013) and reduces the likelihood of a wide range of conditions, including cancers, raised blood pressure, strokes, liver disease, mental ill-health and accidents and injuries (WHO, 2020a). There is much that can be done to enable people to drink less alcohol (WHO, 2020b). For example, reducing the affordability of alcohol (Burton et al., 2017), or introducing a minimum price per gram of alcohol sold (O’Donnell et al., 2019; Anderson et al., 2021a) results in less alcohol bought and drunk. Reducing the amount of alcohol contained in drinks represents an additional strategy to help people drink less, which appears to be gaining increasing traction amongst policy makers as well as in global alcohol markets (Salantă et al., 2020; Capitello and Todirica, 2021). In its consultation document, ‘Advancing our health: prevention in the 2020s,’ the UK Government made a commitment to work with the drinks industry to ‘deliver a significant increase in the availability of alcohol-free and low-alcohol products by 2025’ (UK Government, 2019).

Using British household purchase data, we have previously shown that buying no- (per cent alcohol by volume, ABV = 0.0%) and low- (ABV = >0.0% and ≤ 3.5%) alcohol beer is a relatively infrequent event (Jané Llopis et al., 2021; Anderson et al., 2021b). For every purchase of zero alcohol beer, there were 32 purchases of beer with an ABV of 3.5% or more, and for every purchase of low-alcohol beer, there were nearly 14 purchases of beer with an ABV of 3.5% or more (Anderson et al., 2021b). We found that purchases of no- and low-alcohol beers were greater amongst younger and more affluent households and more common amongst those who bought the most alcohol overall (Anderson et al., 2021b).

Other, largely qualitative, evidence suggests that that buying and consuming no- and low-alcohol beers are driven by health and wellbeing issues, price differentials and overall decreases in the social stigma associated with drinking alcohol-free beverages (Silva et al., 2016; Salantă et al., 2020; Capitello and Todirica, 2021). There is an extensive literature that demonstrates that brand loyalty, brand image and product familiarity are important determinants for choices of beer as a whole (Giacalone et al., 2015; Cardello et al., 2016; Betancur et al., 2020). For example, a systematic review of 65 papers investigating demand for beer found 37 papers related to the impact of branding on beer consumers’ attitudes, preferences and choices (Capitello and Todirica, 2021). A study from Spain, for example, found that both local and global beer preferences are strongly influenced by brand loyalty (Calvo Porral and Levy-Mangin, 2015). And there is some evidence that consumption choices of lower-strength products are driven by previous experience of higher-strength same-branded products (Chrysochou, 2014).

With respect to no- and low-alcohol beers, brand loyalty could act in two ways. If the purchase of no- and low-alcohol beers led to increased subsequent purchases of same-branded higher-strength products, this could lead to more alcohol being consumed with detrimental consequences for public health (Rehm et al., 2016). An additional concern with this scenario, particularly for younger drinkers, is that brand loyalty developed as a result of buying no- and low-alcohol beers could lead to drinkers purchasing same-branded higher-strength beers over time (Siegel et al., 2011; Albers et al., 2014). Conversely, if higher-strength brand loyalty leads to the up-take of same-branded lower-strength products with replacement in purchases, this could lead to less alcohol being consumed, more so for no- as opposed to low-alcohol beers and, provided that there is no compensation in terms of drinking higher volumes of low-alcohol beers (Rehm et al., 2016; Miller et al., 2021).

In this paper, we investigate the issue of branding. We define no-alcohol beer as beer with an ABV of 0.0% and low-alcohol beer with an ABV of >0.0% and ≤ 3.5% (European Commission, 2019). Using barcode scanned adult (aged 18 plus years) household purchase data for Great Britain for the years 2015–2018, we address the following two main questions:

Does the introduction of new no- and low-alcohol beers (hereafter, nablab beers) act as a gateway to subsequent purchases of same-branded higher-strength beers?

Does the previous purchase of higher-strength beers affect the subsequent purchases of newly introduced same-branded nablab beers?

METHODS

Study design

At the level of each household, we use a generalized linear model to estimate: (a) the odds ratios (ORs) of the impact of new nablab beers affecting the subsequent likelihood of purchases of same-branded higher-strength beers and (b), conversely, the impact of the previous purchase of higher-strength beers affecting the likelihood of purchases of new same-branded nablab beers. At the level of each study day over time, we use interrupted time series regression analyses to estimate the impact of new nablab beers on the volume of subsequent purchases of same-branded higher-strength beers.

Data source

The data source is Kantar Worldpanel’s (KWP) household shopping panel for the years 2015–2018. KWP comprises  30,000 British households at any one time, recruited via stratified sampling, with targets set for region, household size, age of main shopper and occupational group, (National Readership Survey 2019) which we have described in more detail elsewhere (O’Donnell et al., 2019; Anderson et al., 2021a). The same households provide longitudinal data over time; for the years 2015–2018, the average time between the first and last recorded alcohol purchase was just under 16 months per household. Households provide demographic information when joining the panel (age of the main shopper, number of adults in the household, income and social class), followed by annual updates. Households record all off-trade alcohol purchases, including alcohol-free products from all store types, including internet shopping, which is brought back into the home, using barcode scanners.

30,000 British households at any one time, recruited via stratified sampling, with targets set for region, household size, age of main shopper and occupational group, (National Readership Survey 2019) which we have described in more detail elsewhere (O’Donnell et al., 2019; Anderson et al., 2021a). The same households provide longitudinal data over time; for the years 2015–2018, the average time between the first and last recorded alcohol purchase was just under 16 months per household. Households provide demographic information when joining the panel (age of the main shopper, number of adults in the household, income and social class), followed by annual updates. Households record all off-trade alcohol purchases, including alcohol-free products from all store types, including internet shopping, which is brought back into the home, using barcode scanners.

Alcohol purchases are recorded daily. For each individual purchase, the data include the type and volume of the purchase using 19 drink categories, including the brand and the ABV. The volume purchased was combined with ABV to calculate the grams of alcohol purchased. We classified households by a range of socio-demographic groups (see Supplementary Table 1, page 1).

Inclusion criteria for analysis

Our inclusion criteria for analysis were a nablab product that: (i) was newly introduced to Great Britain during 2015–2018; (ii) had a name that clearly indicated low- or alcohol-free content (e.g. light or alcohol-free) and (iii), had a parent product or products with an ABV greater than 3.5%, with a similar name and that was available for purchase throughout 2015–2018, both prior and subsequent to the launch of the new nablab beer. Out of 43 potential nablab products, six (14%) met the inclusion criteria. Based on household purchases, five were released during the first quarter of 2017, and the sixth during the last quarter of 2017. Two products, which were analysed separately, had the same parent product. One other product had three parent products (i.e. the same first generic name, and specific second names), which were treated as one parent product.

We set the day of introduction for each new nablab product (as identified by household purchases) as Day 1, our definition of the event (introduction of nablab product), with days across all six products before and after Day 1 ranging from day minus 771 to day plus 414 (for a day numbered <1, no nablab product had been introduced and thus bought; for a day numbered greater than zero, at least one nablab product had been bought). These were our study days, which, because they were recalculated for each nablab product dependent on the exact day of the first recorded purchase of the product, included different days of the week and different seasons of the year on any one study day. For the main analyses, we treated the purchase of any of the six nablab products as a purchase of one product, whose volumes were summed. We did the same for the parent products. For the parent product that was related to two nablab products, we took half the sum of the parent product related to each nablab product.

We classified individual households as follows:

▪ Nablab-plus: bought at least one new nablab beer for a study day numbered greater than zero

▪ Nablab-minus: did not buy any new nablab beer for study day numbered greater than zero

▪ Parent-plus: bought at least one parent higher-strength beer before the introduction of the new nablab beers (i.e. during a study day numbered <1)

▪ Parent-minus: did not buy any parent higher-strength beer before the introduction of the new nablab beers (i.e. during a study day numbered <1)

Statistical analyses

Generalized linear model to estimate likelihood and volume of purchases

Analysed at the level of each household and across the six nablab products treated as one product, we used a generalized linear model with a binomial distribution and log-link function to estimate the ORs (and 95% confidence intervals (CI)) for:

Parent-minus/nablab-plus making at least one subsequent purchase (since the introduction of the nablab) of a parent product compared with parent-minus/nablab-minus to answer question 1, to what extent does the introduction of nablab beers act as gateways by increasing the likelihood of subsequent purchases of same branded higher-strength beers and

Parent-plus making at least one purchase of a new nablab product compared with parent-minus to answer question 2, to what extent does the previous purchase of higher-strength beers affect the likelihood of purchasing newly introduced same branded nablab beers.

The regression equation is:

▪ Purchase (dichotomized yes/no) = intercept + predictor (dichotomized yes/no) + error.

We repeated the generalized linear model to investigate changes in volumes of purchases as opposed to likelihood of making a purchase, with the following regression equation (for details, see Supplement pages 2–4 and Supplementary Figs 1–4):

▪ Log natural (volume of purchase) = intercept + predictor (yes/no) + error.

We undertook additional analyses to consider switching form a higher-strength product to a different branded nablab product (see Supplement, page 5).

As sensitivity analysis for the generalized linear model, we repeated the models for question 2 by removing each one of the nablab products in turn, starting with the latest introduced product down to the earliest product. That is, the repeated models included, respectively, five, four, three, two and one nablab products to see if the model holds up, irrespective of any one nablab.

Interrupted time series analysis to estimate impact on purchase volume

Analysed at the level of each study day, we used interrupted time series analysis (Beard et al., 2019) to estimate the associated impact of the introduction of all six new nablab products, treated together as one product, representing the ‘event’, the independent variable, on the volume of subsequent purchases of all parent products, the dependent variable. We prepared the dependent variable to be consistent and comparable with other publications that have analysed the same data set (e.g. O’Donnell et al., 2019; Anderson et al., 2020; Anderson et al., 2021a; Anderson et al., 2021b; Jane Llopis et al., 2021), by averaging the volume of beer purchases in millilitres by study day (as defined above) across all households, with the average being the mean of the sum of the volume of purchases per adult per individual household for any day of purchase. The interrupted time series tested for level and persistent changes due to the event, the introduction of the new nablab products. The event variable was entered as a dummy variable coded with 0 for each day before the event and with 1 for each day from the event forward. We used a generalized linear model, with the regression equation:

▪ Volume of purchase of parent product = intercept + time + event + error,

where time is the days before and after the event, with the event the dummy-coded variable for the introduction of the new nablab products. For details, see Supplement pages 6–7 and Supplementary Figs 5 and 6.

As our measure is based on the volume of purchase for each individual household for any day of purchase, we checked for the stability of frequency of purchases over time and for any differences in frequency between parent products and new nablab products. For details, see Supplement pages 8–9 and Supplementary Figs 7–10.

To consider if household characteristics affected the results of the interrupted time series analysis, based on the recommendation of Beard et al. (2019), we first converted the dependent variable (volume of purchase of the parent product) into z-scores, so that the coefficients are comparable in terms of standard deviations (relative changes), rather than original volumes (absolute changes). We undertook the interrupted time series analysis as above for all six new nablab products combined, separately for each of the household socio-demographic groups (as defined in Supplementary Table 1, page 1), plotting standardized coefficients and 95% CI.

As sensitivity analysis for the interrupted time series analyses, we repeated the interrupted time series models by removing one of the nablab products in turn, starting with the latest introduced product down to the earliest product. That is the repeated models included, respectively, five, four, three, two and one nablab products.

To consider stability of changes at the level of the individual household, we analysed parent-plus/nablab-plus households, plotting over time, the ratio of (volume of purchases of new nablab beer) divided by (volume of purchases of new nablab beer plus volume of purchases of parent beer). For details, see Supplement, page 10.

All analyses were performed with SPSSv26 (IBM Corp 2019).

RESULTS

Beer purchasing behaviours of 64,280 households were analysed. Of these, 6770 households (10.5%) made 17,842 separate purchases of at least one parent beer before the introduction of any new nablab beer. At least one new nablab beer was purchased by 2469 households (3.8%), with 5439 separate purchases. Following the time of the introduction of any new nablab beer, 6091 (9.5%) households made 14,709 separate purchases of at least one parent beer. The six nablab products (14% of the 43 newly introduced nablab products, as assessed by household purchases) were responsible for 45.4% of the volume of all newly introduced nablab purchases since their release. The eight parent products (2 nablab products had 1 parent product and 1 nablab product had 3 parent products), representing 0.42% of all different beer brands (total number = 1905) with an ABV > 3.5% on the market (as assessed by the household purchases) were responsible for 7.0% of the volume of all beer purchased with an ABV >3.5%. The frequency of purchases remained stable over time and did not differ between parent and nablab products (see Supplementary Fig. 11, and page 11).

Impact of nablab beer on subsequent purchase of parent beer (question 1)

Based on the generalized linear model to estimate ORs, and for parent-minus households, the likelihood of making at least one subsequent purchase of any parent beer after the introduction of any new nablab beer was 0.320 (95% CI = 0.282–0.363) for nablab-plus compared with nablab-minus households. In volume terms, and for parent-minus households that subsequently purchased a parent beer after the time of introduction of any new nablab beer, nablab-plus households bought half (0.502, 95% CI = 0.410–0.614) as much new parent beer as nablab-minus households.

Figure 1 plots the time series of the volume of purchases of parent and nablab products following the introduction of the nablab beers. For parent-plus households, the launch of all new nablab beers was associated with a reduction in subsequent purchases of parent beers of 48.5 ml (95% CI = 45.3–45.7) per adult per household per day, for days in which a purchase was made (from 215.3 ml, 95% CI = 213.6–216.9–166.8 ml, 95% CI = 164.5–169.2), a 22.5% reduction (95% CI = 22.0–23.0). On the other side, since their introduction, new nablab purchases averaged 34.6 ml per adult per household per day for days in which a purchase was made (95% CI = 34.4–34.8).

Fig. 1.

Volume (ml) of parent and nablab beers purchased per adult per household per day of purchase by study days before and after introduction of nablab (vertical line).

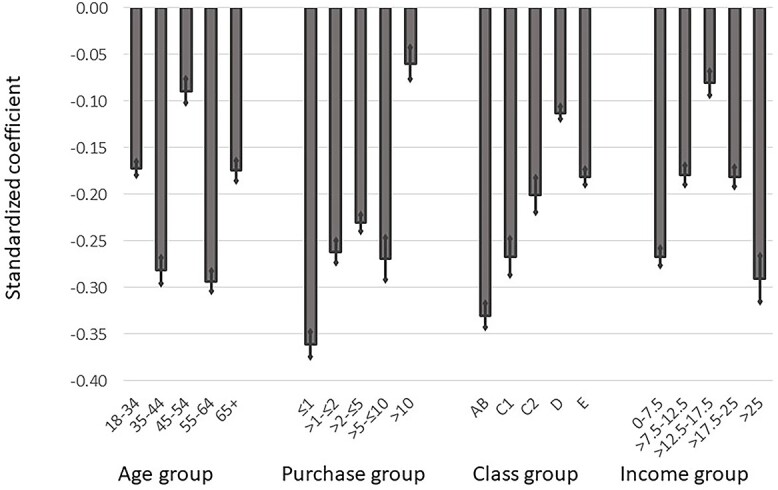

Reductions in subsequent purchases of the parent beers occurred across all household characteristic groups, not related to household age or income group, but were greater amongst the lower purchasing households and in the ‘higher’ social class groupings, Fig. 2.

Fig. 2.

Standardized coefficient of change in volume of purchases of parent product following introduction of new nablab product for parent-plus households, by household characteristics.

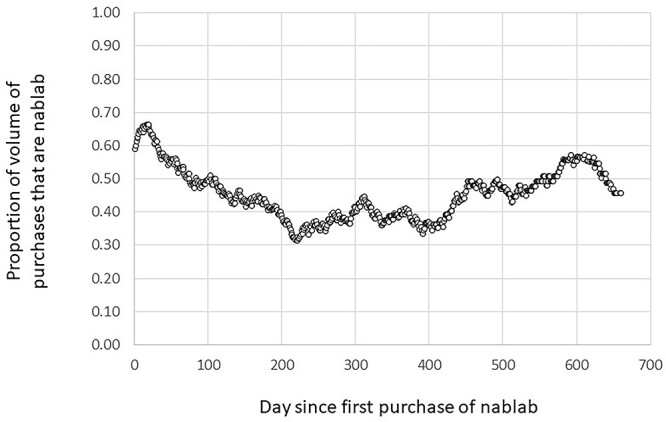

Figure 3 plots, at the level of each individual household, the proportion of the volume of all parent plus nablab beer purchases that were nablab purchases by day since the first day of a nablab purchase. There was a dip for the first 200 days, which then recovered, with a nonsignificant regression coefficient of the proportion across all study days of −1.9−5 (95% CI = −5.0−5 to 1.3−5).

Fig. 3.

Proportion of volume of purchases that are nablab by day since first purchase of nablab. The horizontal axis plots the day since the first purchase of a new nablab product, and the vertical axis the proportion of the volume of all beer purchases that were nablab purchases by day. Both axes were calculated separately for each household for each of the six new nablab products, then averaged across each household for each product, and then averaged across each product.

Impact of parent beer on purchase of new nablab beer (question 2)

Based on the generalized linear model to estimate ORs, parent-plus households were 2.16 times more likely to buy any new nablab beer (95% CI = 1.95–2.40) than parent-minus households. Of those that bought a new nablab beer, parent-plus households, bought, in volume terms 15.2% more volume of nablab beer (95% CI = 12.2–18.2) than parent-minus. For the no-alcohol beer that had a previously launched sibling low-alcohol beer, both the parent beer (OR = 1.43, 95% CI = 1.09–1.87) and the sibling beer (OR = 5.37, 95% CI = 3.95–7.30) increased the likelihood of purchase of the nablab beer, with the sibling beer having the greater impact.

For each individual nablab beer, the likelihood of purchase was increased by previously purchasing the same-branded parent beer, Supplementary Table 2, page 12. There was some evidence for shifting from other higher-strength branded beers for two of the nablab beers (for nablab beer 1, from parent beers 4 and 6 and for nablab beer 3, from parent beer 6), but not for the other four.

Adding the four groups of household characteristics (age of the main shopper, usual purchase group (grams of alcohol), social class, and household income) to the model found that, compared with parent-minus households, parent-plus households were more likely to buy the new nablab beer when they were younger, generally purchased more alcohol of any type, were more likely to be in a higher social class group and had a higher income, Table 1.

Table 1.

Impact of household characteristics on extra likelihood of purchasing nablab beer

| Compared with parent-minus households, impact of household characteristics on likelihood of purchasing nablab beer for parent-plus households | ||||

|---|---|---|---|---|

| Moving across age divisions from youngest (18–34 years) to oldest (65+ years) | Moving across purchase divisions from lowest (<1 g alcohol) to highest (>10 g alcohol) | Moving across household income divisions from lowest (≤£7500 per year) to highest (>25,000 per year) | Moving across social class divisions from AB (‘higher’) to E (‘lower’) | |

| Odds ratio (95% CI) for moving from one division to next across the five divisions | 0.950 (0.914–0.988) |

1.122 (1.083–1.162) |

1.094 (1.053–1.138) |

0.956 (0.911–1.002) |

Sensitivity analyses

Table 2 lists the ORs (and 95% CI) from the generalized linear model for parent-plus households buying a new nablab beer compared with parent-minus households, by the number of nablab beers included in the model. The ORs tended to get larger, the smaller the number of products considered. Table 2 also lists the reductions in the volume of subsequent purchases of the parent beers associated with the launch of the new nablab beers for parent-plus households from the interrupted time series analyses, by the number of nablab beers included in the model. Associated reductions in the volumes purchased were present in all models, although, inevitably became smaller as fewer products were included in the models.

Table 2.

Sensitivity analysis.

| Number of nablab products included in the models | ORs (95% CI) for parent-plus households buying a new nablab beer compared with parent-minus households | Reductions in the volume (ml per adult per household per day of purchase, 95% CI) of subsequent purchases of the parent beers associated with the launch of the new nablab beers for parent-plus households |

|---|---|---|

| 6 | 2.16 (1.95–2.40) | 48.5 (45.3–45.7) |

| 5 | 2.09 (1.86–2.34) | 49.9 (47.0–52.8) |

| 4 | 2.19 (1.95–2.47) | 45.6 (42.8–48.4) |

| 3 | 2.48 (2.16–2.84) | 31.7 (29.2–34.2) |

| 2 | 2.56 (2.23–2.95) | 29.7 (27.5–32.0) |

| 1 | 2.71 (2.34–3.15) | 23.3 (21.1–25.9) |

Number of products included in the models dropped from 6 to 1, by, at each step removing the latest introduced product.

DISCUSSION

Principal findings

In relation to our first question, using British household purchase data for 2015–2018, we found that parent-minus/nablab-plus households were less than one-third as likely to go on and newly buy a same-branded parent beer compared with parent-minus/nablab-minus households. Furthermore, when parent-minus/nablab-plus households did subsequently buy a same-branded parent product, they bought half as much volume as parent-minus/nablab-minus households. This suggests that the introduction of new nablab beers did not act as gateways increasing the purchases of same-branded higher-strength products.

For parent-plus/nablab-plus households, the introduction of the new same-branded nablab beer was associated with decreased purchases of the parent beer by, on average, 48 ml per adult per household per day of purchase. Sensitivity analyses found that associated decreases in purchases were present irrespective of the number of nablab products included in the model (between 1 and 6), although inevitably, became smaller, as fewer nablab products were included in the model (Table 2).

The decreased purchases of the same-branded parent beer did not differ by age or household income but tended to be greater in typically lower alcohol purchasing households (expressed in grams) and in higher socio-economic status groups. At the individual household level, there was stability in the purchases of new nablab products over time (at least, for over 22 months, as far as our data allowed us to analyse), meaning there was no evidence of reverting to buying a higher-strength parent beer (Fig. 3).

In relation to our second question, we found that parent-plus households were more than twice as likely to purchase a newly introduced same-branded nablab beer, and, if buying such a nablab beer, bought 15% more volume compared with parent-minus households. Sensitivity analyses found that the increased likelihood was present irrespective of the number of nablab products included in the model, generally becoming greater the fewer nablab products included in the model (Table 2). This pattern of purchase of higher-strength brands increasing the likelihood of later purchase of nablab beers held for each individual nablab beer (Supplementary Table 2). For two of the nablab beers, there was some evidence of switching from other different branded parent beers (Supplementary Table 2). Households that bought the new nablab beers tended to be younger, generally purchasing more alcohol, and of a higher social class with higher average incomes than households that had never bought the new nablab beers (Fig. 2).

Comparison with other studies

We are not aware of any similar studies that investigate beer branding effects on purchase or consumption of no- or low-alcohol beers, using such a large data set. The only studies that we are aware of are qualitative studies exploring consumers’ attitudes to and views on the introduction of nablab beers, rather than their purchase or consumption behaviour. Our results are, however, consistent with the findings of such studies, which demonstrate that brand loyalty, brand image and product familiarity are important predictors of beer purchases (Chrysochou, 2014; Giacalone et al., 2015; Cardello et al., 2016; Betancur et al., 2020). Although consumption of nablab beers is often viewed by drinkers as a substitute for higher-strength beers (Silva et al., 2016), it appears that nablab beers may be deemed more acceptable to buy and drink if there is a recognizable higher-strength (branded) beer. This could be a quality-assurance issue or may reflect how drinkers want to be seen by others (Silva et al., 2016). In absolute terms, it is important to point out, though, that nablab beers remain a minority interest and seem to be one for affluent and higher social status groups (Anderson et al., 2021b).

Strengths and limitations of study

Our study has a number of strengths. First, it uses a large commercial market-research data set with relatively large numbers of households and purchases across each new nablab and parent beer for the time periods before and after the introduction of the new nablab beer (covering 2–3 years before the introduction of the new beer, and 1–2 years subsequent to the introduction of the new beer). Second, although relying on compliance at the household level, purchase data based on product bar codes, and verified via digital receipts, is, of itself, objective. In general, attrition rates and fatigue in recording over time are low and seem better with Kantar scanner-based data (Leicester and Oldfield, 2009), that also provides more detailed product descriptions and less under reporting (Griffith and O’Connell, 2009), than with data from other regular in-person surveys.

Our study, though, also has a number of limitations. Although quality control and compliance are regularly monitored by Kantar, the data have some shortcomings. Alcohol purchases have been among the most underreported categories in the panel data (Leicester, 2012), which might reflect the method of recording purchases if not all items purchased are taken home and scanned. Although most primary shopping is done by women, secondary top-up shopping, which is more likely done by men, may be less well recorded (Leicester, 2012).

Before considering any policy implications, our analyses have a number of important caveats. First, we only consider off-trade beer purchases that are a little over half of all beer purchases (Giles and Robinson, 2019). Second, we only capture household purchases made by adults, aged 18 plus years, meaning we were unable to assess the impact of introducing nablab beers on the purchasing behaviour of underage drinkers. Third, the market penetration of low- and no-alcohol products is very small – for the time period of our study, out of the volume of all beer purchased, only 4.9% had an ABV > 0.0% and ≤ 3.5%, and only 1.5% had an ABV of 0.0% (Jane Llopis et al., 2021). Third, due to our inclusion criteria to study brand impact on purchases of nablab products, we were only able to consider six new nablab products and their parent products, even though the nablab products, representing 14% of all possible different products at the time of study, accounted for 45% of the volume all no- and low-alcohol beer purchased; the parent products, representing 0.4% of all possible products, accounted for 7% of the volume of all beer purchased with an ABV > 3.5%. Elsewhere we have shown that the combined introduction of 46 new nablab products and the reformulation of 33 beer products to contain less alcohol were associated with relative reductions in household purchases of grams of alcohol within beer of between 7.1% and 10.2%; and purchases of grams of alcohol as a whole of between 2.6% and 3.9% (Anderson et al. 2019), and that for every 10 ml absolute increase in household purchases of zero-alcohol beer, purchases of grams of all alcohol contained within beer dropped by 1.1% (Anderson et al., 2022). Nevertheless, we should be cautious in recommending any policy implications (Anderson et al., 2021c).

Conclusions and policy implications

Bearing in mind the above caveats, our data have shown that purchases of new no- and low-alcohol beers do not appear to act as gateways for increased purchases of same-branded higher-strength beers. However, our data cannot say much about switching to other alcohol products including other beer products. Conversely, previous purchases of higher-strength beers appear to increase the likelihood of purchasing same-branded no- and low-alcohol beers.

Elsewhere, we have shown that the introduction of new nablab beers in the British market is associated with households buying less grams of alcohol (Anderson et al., 2020). A key policy question is how to encourage further shifts from higher-strength beers to nablab beers, and in particular to no-alcohol beers, which would lead to greater reductions in consumption of grams of alcohol than similar volume shifts to low-alcohol beers.

The most direct policy measure to influence the extent to which lower-strength beers are selected versus higher-strength beers seems to be via pricing and taxation. For example, minimum unit prices introduced in devolved administrations in Great Britain have encouraged shifts in purchases from higher- to lower-strength alcohol products (Jane Llopis et al., 2021; Anderson et al. 2021). For taxation, alcohol volumetric taxes calculate tax rates according to the volume of pure alcohol in a beverage and can thus provide consumers with an incentive to select lower-strength beers, as has been modelled in Canada, with likely beneficial impact (Stockwell et al., 2020). Australia has had a sliding scale of taxation for beer for many years with higher tax rates for higher-strength beers that have encouraged uptake of low-alcohol beers (Stockwell and Crosbie, 2001).

As a policy limitation, we could not address the question of the extent to which newly introduced nablab beers could act as gateways to purchase and consumption of higher-strength beers by under-age drinkers (Miller et al., 2021), as the panel data were restricted to household purchases by adults, with purchases of alcohol by under 18-year-olds illegal in Great Britain. Likewise, we were unable to assess the extent to which any such impacts on under-age drinkers could be compounded by advertising of alcohol-free products strongly linked by ‘brand’ to parent products, which might promote addition to, rather than substitution of, higher-strength products (Vasiljevic et al., 2018), or might circumvent advertising regulations (Ross et al., 2014; Kaewpramkusol et al., 2019). These questions require urgent study. Although waiting for the results of such studies, known policies should continue to be implemented to delay the onset of drinking and to reduce the amount drunk by children and adolescents, guided, for example, by WHO’s SAFER initiative (WHO, 2020b).

AUTHORS’ CONTRIBUTIONS

E.J-L. conceptualized the paper and undertook the analyses. All the authors refined the various versions of the full paper and approved the final manuscript. The corresponding author attests that all listed authors meet authorship criteria and that no others meeting the criteria have been omitted. P.A. and A.O.D. are the guarantors of the data.

Supplementary Material

ACKNOWLEDGEMENTS

Professor Kaner, supported by a National Institute for Health Research (NIHR) Senior Investigator award, is Director of the NIHR Applied Research Collaboration, North East and North Cumbria. Dr O’Donnell is a National Institute for Health Research (NIHR) Advanced Fellow. The views expressed in this article are those of the authors and not necessarily those of NIHR, or the Department for Health and Social Care. We thank Kantar Worldpanel for providing the raw data and reviewing the method description as it describes the data collection. Kantar Worldpanel provided the raw data to Newcastle University under a direct contract, in which it is stated that Kantar Worldpanel collected and owned the data as part of its business activities and provided the data to Newcastle University, which requested access to the anonymized data for the purpose of analysing the potential impact of changes in the alcohol content of beers on overall alcohol consumption and on alcohol-related harm, taking into account relevant socio-demographic factors and product price. Kantar Worldpanel received reimbursement from AB InBev to cover the costs of the data. Kantar WordPanel has similar commercial relationships with other customers who pay to have data collected on food and non-food items available for sale in supermarkets and other retail outlets covered by the WorldPanel. Kantar Worldpanel and no other entity had any role in the study design, data analysis, data interpretation or writing of the manuscript.

Contributor Information

Eva Jané Llopis, ESADE Business School, Ramon Llull University, Barcelona 08034, Spain; Faculty of Health, Medicine and Life Sciences, Maastricht University, Maastricht, 6200 MD, Netherlands; Institute for Mental Health Policy Research, Centre for Addiction and Mental Health, 33 Ursula Franklin Street, Toronto, ON M5S 2S1, Canada.

Amy O’Donnell, Population Health Sciences Institute, Newcastle University, Baddiley-Clark Building, Newcastle upon Tyne NE2 4AX, UK.

Eileen Kaner, Population Health Sciences Institute, Newcastle University, Baddiley-Clark Building, Newcastle upon Tyne NE2 4AX, UK.

Peter Anderson, Faculty of Health, Medicine and Life Sciences, Maastricht University, Maastricht, 6200 MD, Netherlands; Population Health Sciences Institute, Newcastle University, Baddiley-Clark Building, Newcastle upon Tyne NE2 4AX, UK.

ETHICAL APPROVAL

Not required.

DATA SHARING

Kantar Worldpanel data cannot be shared due to licensing restrictions.

FUNDING

No funding was received in support of this study.

CONFLICT OF INTEREST STATEMENT

E.J.L., A.O.’D. and E.K. declare no competing interests and declare no financial relationships with any organizations that might have an interest in the submitted work in the previous 3 years. Within the previous 5 years, P.A. has received financial support from AB InBev Foundation outside the submitted work. All authors have completed the ICMJE uniform disclosure form at www.icmje.org/coi_disclosure.pdf and declare no support from any organization for the submitted work; all authors declare no other relationships or activities that could appear to have influenced the submitted work.

References

- Albers AB, DeJong W, Naimi TSet al. (2014) The relationship between alcohol price and brand choice among underage drinkers: are the most popular alcoholic brands consumed by youth the cheapest? Subst Use Misuse 49:1833–43. 10.3109/10826084.2014.935790. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Anderson P, Jané Llopis E, O’Donnell Aet al. (2020) Impact of low and no alcohol beers on purchases of alcohol: interrupted time series analysis of British household shopping data, 2015–2018. BMJ Open 10:e036371. 10.1136/bmjopen-2019-036371. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Anderson P, O’Donnell A, Kaner Eet al. (2021a) Impact of minimum unit pricing on alcohol purchases in Scotland and Wales: controlled interrupted time series analyses. Lancet Public Health 6:e557–65. 10.1016/S2468-2667(21)00052-9. [DOI] [PubMed] [Google Scholar]

- Anderson P, O’Donnell A, Kokole Det al. (2021b) Is buying and drinking zero and low alcohol beer a higher socio-economic phenomenon? Analysis of British survey data, 2015–2018 and household purchase data 2015–2020. Int J Environ Res Public Health 18:10347. 10.3390/ijerph181910347. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Anderson P, Kokole D, Llopis E. (2021c) Production, consumption, and potential public health impact of low- and no-alcohol products: results of a scoping review. Nutrients 13:3153. 10.3390/nu13093153. https://www.mdpi.com/2072-6643/13/9/3153. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Anderson P, O’Donnell A, Jané Llopis Eet al. (2022) The impact of lower-strength alcohol products on alcohol purchases: ARIMA analyses based on 4 million purchases by 69,803 households, 2015-2019. J Public Health 1–11. 10.1093/pubmed/fdac052. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Beard E, Marsden J, Brown Jet al. (2019) Understanding and using time series analyses in addiction research. Addiction 114:1866–84. 10.1111/add.14643Epub 2019 Jul 9. PMID: 31058392. [DOI] [PubMed] [Google Scholar]

- Betancur MI, Motoki K, Spence Cet al. (2020) Factors influencing the choice of beer: a review. Food Research International, 109367 ISSN 0963-9969. 137. 10.1016/j.foodres.2020.109367. [DOI] [PubMed] [Google Scholar]

- Burton R, Henn C, Lavoie Det al. (2017) A rapid evidence review of the effectiveness and cost-effectiveness of alcohol control policies: an English perspective. Lancet 389:1558–80. [DOI] [PubMed] [Google Scholar]

- Calvo Porral C, Levy-Mangin J-P. (2015) Global brands or local heroes? Evidence from the Spanish beer market. Br Food J 117:565–87. 10.1108/BFJ-07-2013-0174. [DOI] [Google Scholar]

- Capitello R, Todirica Ioana Claudia. 20212 – Understanding the behavior of beer consumers. In Capitello Roberta, Maehle Natalia (eds). In Woodhead Publishing Series in Consumer Sci & Strat Market, Case Studies in the Beer Sector. Sawston, Cambridge, England: Woodhead Publishing, 15–36, ISBN 9780128177341, 10.1016/B978-0-12-817734-1.00002-1. [DOI] [Google Scholar]

- Cardello AV, Pineau B, Paisley AGet al. (2016) Cognitive and emotional differentiators for beer: an exploratory study focusing on “uniqueness”. Food Qual Prefer 54:23–38. [Google Scholar]

- Chrysochou P. (2014) Drink to get drunk or stay healthy? Exploring consumers’ perceptions, motives and preferences for light beer. Food Qual Prefer 31:156–63ISSN 0950-3293. 10.1016/j.foodqual.2013.08.006. [DOI] [Google Scholar]

- European Commission . (2019) Service contract for the provision of 2019 – support to member states in studies and capacity building activities to reduce alcohol related harm. European Commission, Consumers, Health, Agriculture and Food Executive Agency, Ref Ares 7816625 – 19/12/2019. [Google Scholar]

- Giacalone D, Frost MB, Bredie WLPet al. (2015) Situational appropriateness of beer is influenced by product familiarity. Food Qual Prefer 39:16–27. [Google Scholar]

- Giles L, Robinson M. (2019.) Monitoring and evaluating Scotland’s alcohol strategy: monitoring report Edinburgh: NHS health Scotland. http://www.healthscotland.scot/publications/mesas-monitoring-report-2019 (Accessed 1 April 2022).

- Griffith R, O’Connell M. (2009) The use of scanner data for research into nutrition. Fiscal Stud 30:339–65. [Google Scholar]

- IBM Corp. Released 2019 . IBM SPSS Statistics for Windows, Version 26.0. Armonk, NY: IBM Corp. [Google Scholar]

- Jané Llopis E, O'Donnell A, Anderson P. (2021) Impact of price promotion, price, and minimum unit price on household purchases of low and no alcohol beers and ciders: descriptive analyses and interrupted time series analysis of purchase data from 70, 303 British households, 2015–2018 and first half of 2020. Soc Sci Med 270:113690, ISSN 0277-9536. 10.1016/j.socscimed.2021.113690. http://www.sciencedirect.com/science/article/pii/S0277953621000228. [DOI] [PubMed] [Google Scholar]

- Kaewpramkusol R, Senior K, Nanthamongkolchai Set al. (2019) Brand advertising and brand sharing of alcoholic and non-alcoholic products, and the effects on young Thai people's attitudes towards alcohol use: a qualitative focus group study. Drug Alcohol Rev 38:284–93. 10.1111/dar.12910Epub 2019 Feb 10. PMID: 30740803. [DOI] [PubMed] [Google Scholar]

- Leicester A. (2012) How might in-home scanner technology be used in budget surveys? IFS Working Paper W12/01 https://ifs.org.uk/publications/6035 (Accessed 1 April 2022). [Google Scholar]

- Leicester A, Oldfield Z. (2009) Using scanner technology to collect expenditure data. Fiscal Stud 30:309–37. [Google Scholar]

- Llopis EJ, O’Donnell A, Anderson P. (2021) Impact of price promotion, price, and minimum unit price on household purchases of low and no alcohol beers and ciders: descriptive analyses and interrupted time series analysis of purchase data from 70, 303 British households, 2015–2018 and first half of 2020. Soc Sci Med 270:113690. [DOI] [PubMed] [Google Scholar]

- Miller M, Pettigrew S, Wright CJC. (2022) Zero-alcohol beverages: harm-minimisation tool or gateway drink? Drug Alcohol Rev 41:546–549. 10.1111/dar.13359Epub ahead of print. PMID: 34370881. [DOI] [PubMed] [Google Scholar]

- National Readership Survey . Social class London: National Readership Survey; 2019[cited 10 July 2019]. http://www.nrs.co.uk/nrs-print/lifestyle-and-classification-data/social-grade/ (Accessed 1 April 2022).

- O’Donnell A, Anderson P, Jane-Llopis Eet al. (2019) Immediate impact of minimum unit pricing on alcohol purchases in Scotland: controlled interrupted time series analysis for 2015-18. Br Med J 366:l5274. 10.1136/bmj.l5274. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Rehm J, Roerecke M. (2013) Reduction of drinking in problem drinkers and all-cause mortality. Alcohol Alcohol 48:509–13. [DOI] [PubMed] [Google Scholar]

- Rehm J, Lachenmeier DW, Jané-Llopis Eet al. (2016) On the evidence base of reducing ethanol content in beverages to reduce the harmful use of alcohol. Lancet Gastroenterol Hepatol 1:78–83. [DOI] [PubMed] [Google Scholar]

- Ross CS, Maple E, Siegel Met al. (2014) The relationship between brand-specific alcohol advertising on television and brand-specific consumption among underage youth. Alcohol Clin Exp Res 38:2234–42. 10.1111/acer.12488Epub 2014 Jul 1. PMID: 24986257; PMCID: PMC4146644. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Salantă LC, Coldea TE, Ignat MVet al. (2020) Non-alcoholic and craft beer production and challenges. Processes 8:1382. 10.3390/pr8111382. [DOI] [Google Scholar]

- Siegel M, DeJong W, Naimi TSet al. (2011) Alcohol brand preferences of underage youth: results from a pilot survey among a national sample. Subst Abus 32:191–201. 10.1080/08897077.2011.601250PMID: 22014249; PMCID: PMC3202336. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Silva AP, Jager G, Bommel Ret al. (2016) Functional or emotional? How Dutch and Portuguese conceptualise beer, wine and non-alcoholic beer consumption. Food Qual Prefer 49:54–65ISSN 0950-3293. 10.1016/j.foodqual.2015.11.007. [DOI] [Google Scholar]

- Stockwell TR, Crosbie D. (2001) Supply and demand for alcohol in Australia: relationships between industry structures, regulation and the marketplace. Int J Drug Policy 12:139–52. [DOI] [PubMed] [Google Scholar]

- Stockwell T, Churchill S, Sherk Aet al. (2020) How many alcohol attributable deaths and hospital admissions could be prevented by alternative pricing and taxation policies? Modelling impacts on alcohol consumption, revenues and related harms in Canada. Health Promot Chronic Dis Preven Can . 10.24095/hpcdp.40.5/6.04. [DOI] [PMC free article] [PubMed] [Google Scholar]

- UK Government . (2019) Advancing our health: prevention in the 2020s – consultation document. https://www.gov.uk/government/consultations/advancing-our-health-prevention-in-the-2020s/advancing-our-health-prevention-in-the-2020s-consultation-document (Accessed 1 April 2022).

- Vasiljevic M, Coulter L, Petticrew Met al. (2018) Marketing messages accompanying online selling of low/er and regular strength wine and beer products in the UK: a content analysis. BMC Public Health 18:147. 10.1186/s12889-018-5040-6. [DOI] [PMC free article] [PubMed] [Google Scholar]

- WHO . (2020a) Global status report on alcohol and health 2018. https://apps.who.int/iris/bitstream/handle/10665/274603/9789241565639-eng.pdf?ua=1&ua=1 (Accessed 1 April 2022).

- WHO . (2020b) Geneva, Switzerland. World Health Organization. SAFER, Alcohol Control Initiative, 2020. https://www.who.int/substance_abuse/safer/en/ (Accessed 1 April 2022). [Google Scholar]

- Wood AM, Kaptoge S, Butterworth ASet al. (2018) Risk thresholds for alcohol consumption: combined analysis of individual-participant data for 599 912 current drinkers in 83 prospective studies. The Lancet 391:1513–23. [DOI] [PMC free article] [PubMed] [Google Scholar]

Associated Data

This section collects any data citations, data availability statements, or supplementary materials included in this article.