Abstract

This research examined the effect of religiosity and attitude on tax compliant intention, moderated by The utilization of e-Filing. This research was analytical research with a quantitative approach. Data analysis used the measurement model Structural Equation Model (SEM) with the WarpPLS approach because the model used moderating variables where the WarpPLS approach is very well used in a model like this. The analysis tools use WarpPLS 6.0 Software. Large taxpayers are generally in the form of agencies and individuals, so the population of this study was companies that are in the Directorate General of Taxation of Large Taxpayers Jakarta, Large Tax Service Offices 1 and 2, totaling 529 companies. Religiosity (X1) and attitude (X2) significantly influence tax compliant intention (Y1). The utilization of e-Filing showed a significant moderating effect on the research model. The novelties that can be found in this study include the development of the Theory of Planned Behavior from the basic theory proposed by Ajzen (1991) by involving other variables that affect taxpayer compliance behavior, namely the religiosity of taxpayers. The development of concepts or models of Theory of Planned Behavior (TPB) in tax involves the variables of religiosity, attitude, tax compliant intention, and the utilization of the e-Filing system. In addition, it involves the utilization of the e-Filing variable as a moderating variable.

Keywords: Religiosity, The utilization of e-Filing, Tax compliant intention, Moderating variable

Introduction

Over the years, our country has not been able to achieve the maximum tax revenue target. Various government policies and facilities are implemented to improve taxpayer compliance in terms of paying and reporting their tax obligations. Taxpayer compliance is still a very complex problem and affects almost all countries. So far, there are major aspects that influence, namely aspects of the taxpayer's self and aspects of the tax apparatus. Aspects of the taxpayer's self-include demographics, family factors, cultural factors, religious factors, social and environmental factors, and other personal factors (motivation and belief). Aspects of the tax apparatus include tax authorities, tax administration systems, service tax officials, and tax audit steps. This problem needs to be addressed wisely and wisely by the government because it is not easy to raise awareness and willingness to pay and report taxes.

The current COVID-19 pandemic, which cannot be ascertained when it will end, certainly affects the realization of tax revenues in 2020. Unstable economic conditions affect many aspects. The social and psychological aspects of society are also influential, such as there is still a sense of fear of the dangers of COVID-19, confusion about the future, confusion about finding alternative income, hopelessness, and helplessness in life. Although this condition may occur in a short period, it affects a person's mental attitude, including the willingness and awareness of paying taxes. Changes in policy by both the government and company leaders are also affected by this pandemic. Therefore, it is very necessary to conduct research related to tax compliance in Indonesia.

In general provisions and taxation procedures, there are three tax collection systems, namely the self-assessment system, the official assessment system, and the withholding assessment system. Indonesia adheres to a self-assessment taxation system, which is a system where taxpayers are entrusted with calculating the amount of tax owed themselves, calculating the amount of tax that has been deducted by other parties, paying taxes that must be paid, and reporting to the Tax Office by the provisions stipulated in the Tax Offices. A self-assessment system is a tax collection system that gives taxpayers the authority to determine the amount of tax owed annually following the applicable tax laws and regulations (Resmi, 2016). The government expected that this system can give maximum trust to the public to increase the awareness and participation of taxpayers in complying with tax obligations. The self-assessment system calculation system allows the potential for taxpayers not to carry out their tax obligations properly due to negligence, intentional or ignorance of their tax responsibilities. One aspect that becomes the supervision of the tax authorities in the self-assessment system is the Surat Pemberitahuan Tahunan (SPT) reporting.

Initially, Surat Pemberitahuan Tahunan (SPT) was submitted by the Taxpayer to the Directorate General of Taxes through the Tax Service Office manually. This means that the SPT is submitted in hardcopy (paper form) which has been provided by the Tax Service Office. However, along with the development of technology, especially in terms of the computerization of the internet world, the Directorate General of Taxes has adopted a new technological innovation to serve as a service tool that makes it easier for taxpayers to fulfill their tax obligations.

One form of internet-based tax services is the application of the e-Filing system, namely the delivery of Periodic SPT and Annual SPT in the form of electronic forms in computer media. This SPT is not in paper form but in the form of an electronic form that is transferred or submitted to the Directorate General of Taxes through the Tax Service Office with an integrated and real-time process. The submission of SPT by e-Filing is an effort by the Directorate General of Taxes to provide convenient services for taxpayers in reporting the amount of tax that must be paid. e-Filing is a method of submitting SPT reports electronically or online through the website (DGT Online) or other official electronic filing channels regulated by the government. At least, there are several reasons why taxpayers should use e-Filing. Provisions regarding e-Filing are regulated in the Directorate General of Taxes Regulation Number PER-03/PJ/2015. With e-Filing or online tax reporting, it is expected to reduce the queue at the Tax Service Office (KPP) which is always crowded with people who want to fulfill their obligations to take care of taxation.

The background of the implementation of e-Filing is a transformation of the tax administration system in Indonesia. Previously, the tax reporting process was carried out in a way that taxpayers had to always come to the tax office, but not anymore. In addition, the tax reporting process before the e-Filing was certainly very different and faced many obstacles such as:

Before the implementation of e-Filing, DGT had a fairly large administrative burden to receive, process, and archive SPT throughout the year.

The costs required for the process of receiving, processing, and filing manual tax returns are very long and take a long time.

In the prediction of individual behavior, it is called the theory of planned behavior, which is an extension of the theory of rational behavior. The concepts of intention and action are generally studied in the theory of rational action first introduced by Fishbein and Eisen in 1975. Within the framework of rational action theory, behavioral intentions largely determine behavior and facts, and are two additional function variables that are subjective attitudes and norms. In the TPB model (Ajzen 1991), behavioral intent is an intermediate variable in behavior. In other words, an individual’s behavior is usually based on their intention to act. The intention to use technical services is an awareness of the customer's ability to use these services (Nguyen, 2020). Also, even if the audience is the same, not everyone will have the same attitude, so each person's circumstances, experiences, information and needs may be different. Everyone has an attitude that defines it, one of which is a religious character (Wibowo & Masitoh, 2018; Rahman et al., 2015; Graafland, 2017).

Several recent studies have demonstrated the importance of religious values in human resource management and organizational behavior in organizations. Several studies have found that organizational change can be achieved through the application of religious values in the workplace (Konz & Ryan, 1999; Fery, 2003; French & Bell, 2001). Religion according to Johnson et al. (2001) examines people's levels of commitment to religion and beliefs and applies its teachings to ensure that individuals' attitudes and behaviors reflect those commitments. Mohdali (2013) argues that the role of religious values can promote good behavior by encouraging positive behavior and reducing negative behavior for compliance behavior. This study aims to determine whether religiosity and attitudes affect taxpayer compliance behavior in fulfilling the provisions of tax laws. Religiosity and attitudes are some of the potential elements to explain tax compliance behavior beginning with the emergence of several studies such as Welch et al. (2005), Stack & Kposowa (CR444), Alabede et al. (2011), and Jayawardane & Low (2016) which emphasize the importance of religiosity and attitudes in tax compliance.

In the context of tax compliance, intent means that an individual taxpayer wants to be tax compliant. The decision is a taxpayer's personal decision to comply with tax laws and regulations. Several studies using the theory of planned behavior show that intentions influence behavior. According to a study by Bobek and Hatfield (2003), behavioral intention has a positive and meaningful effect on behavior. Some of the innovations found in this study are based on the basic theory proposed by Ajzen (1991), systematically based on other variables that influence taxpayer behavior, namely the taxpayer's religion, the development of behavioral theory. Therefore, this study also aims to elucidate whether the use of electronic SPT (especially e-Filing) affects the relationship between religiosity toward tax intention and taxpayer's attitude.

Literature review

Attitude

Based on the explanation above, one of the factors forming compliance is an attitude, in this study what is meant is the attitude of the taxpayer. Jalaluddin (1996) defines attitude as the tendency to act, perceive, and think, in dealing with objects, ideas, situations, or values. Attitude is not behavior but a tendency to behave in a certain way toward the object of attitude. The object of attitude may be an object, person, place, idea or situation, or group. An attitude is a form of evaluation or reaction to one's feelings, whether it is a feeling of support or not supporting an object to be addressed. Ajzen (2005) also argues that behavioral attitudes are determined by beliefs about behavioral consequences, that is, behavioral beliefs. According to Hariyono (2021), the patterns of community attitudes, behavioral patterns and cultural values that parents teach their children are the basis for further behavioral development. Understanding attitudes was also conveyed by Salrito and Eco (2009). Attitude is the process by which people evaluate an object. Attitudes are a set of beliefs and emotions associated with a particular subject and tendencies to influence that subject in a particular way (Calhoun, 2006). Attitude is a term that reflects a person's pleasure, discomfort, or neutrality toward something. Fishbein and Eisen suggest that there are two groups of attitude formation: behavioral beliefs and behavioral belief judgments. According to some opinions, an attitude can be said to be a response or reaction in the form of an evaluation that occurs in an individual to an object. Attitude can also be interpreted as an expression of concern for the environment. The process of forming an attitude is a process in which an object exists around a person, creates a stimulus that affects the person's senses, and processes the information received about the object in the brain to trigger a reaction. Jayawardane and Low (2016) conducted a study to evaluate and identify the most influential factors that reduce taxpayer compliance and to establish a relationship between attitudes and compliance behavior. The results of this study indicate that the attitude of taxpayers equally affects taxpayer compliance in Sri Lanka.

Then, Onu (2016) conducted a study to measure taxpayer attitudes and then discussed the evidence to support the relationship between attitude and compliance behavior. The results of this study can be concluded that attitude has the potential to be a useful tool for understanding tax behavior and also for improving attitudes.

Religiosity

Religiosity is the breadth of knowledge, the strength of his faith, the power of worship and enforcement of its rules, and the depth of gratitude for the religion he adheres to (Nashori & Mucharaman, 2002). Religiosity is the power of relationships and belief in religion (Raja in Susanti, 2016). Religion is a complex integration of knowledge, emotions, and religious activity. According to Johnson (2016), religiosity is viewed as the degree to which an individual feels committed to his or her religion and beliefs and applies its teachings so that an individual's attitudes and behaviors reflect that commitment. The religious nature of this study shows taxpayers' appreciation and attitude toward life based on their religious values. These assessments are reflected in the honest conduct of the tax. Religiosity refers to cognitions (religious knowledge and beliefs) that generally influence what we do with our emotional and emotional attachment to religion and behavior, such as reading scriptures, attending places of worship, and praying (Elci et al. 2011). Glock and Stark (1965) states that religiosity has 5 important aspects in evaluating religiosity: belief, religious practice (consciousness), judgment, knowledge (intellectual), and practice.

Torgler (2006) states that the religiosity of a religious organization will increase tax morale. In addition, Utama and Wahyudi (2016) in a study that aims to obtain empirical evidence that religiosity affects taxpayer compliance. By using taxpayer respondents residing in the DKI Jakarta Province, the total population or individual taxpayers in all Regional Offices within the DKI Jakarta Province is 3120584 Taxpayers. The research sample size is considered adequate with several 150 to 200. The results show that there is evidence that religiosity has a significant effect on voluntary tax compliance.

The utilization of e-Filing

Based on Law No. 28 of 2007, tax is defined as mandatory state taxation owned by individuals or legal entities, which can be taxed without receiving direct consideration. Tax is the transfer of wealth from the public to the state treasury to fund daily expenses, with the excess going into public savings, the main source of public investment to be devoted (Soemitro, 2013). By the provisions of the following laws and regulations, the General SPT report (SPT) of past performance can be submitted directly to the Directorate General of Taxes or sent by registered post. This system requires taxpayers to come directly to the tax office. The system also requires a lot of staff, takes up a lot of space, and slows down service due to the manual delivery process. Also, spelling errors are more common. For this reason, every tax office needs a faster and more accurate management and maintenance system. The culmination occurred on January 24, 2005, when the Indonesian President, along with the National Tax Service, launched a declaration product or electronic filing system at the Blue House. In a nutshell, e-Filing is the implementation of e-Government in tax administration, specifically SPT reporting to support the existing tax system. This means increasing tax compliance, simplifying tax filing and reducing tax errors. The DGT has two methods of reporting SPTs electronically: electronic filings and electronic forms, which are available on the DGT's official website. However, the most widely used by taxpayers is e-Filing.

e-Filing is an SPT reporting system using internet facilities without going through other parties and without any costs, which is made to make it easier for taxpayers in making and submitting SPT reports so that it becomes faster and cheaper. With e-Filing, taxpayers no longer need to wait in long queues at drop box locations or the Tax Service Office (KPP). This means that reporting taxes with e-Filing saves time and money because there is no need to spend money.

e-Filing itself is carried out online and in real-time, which means that if the taxpayer is to report his annual tax return, the device used must always be connected to the internet network known online. So, if there is an error or error in the network, the taxpayer must repeat the initial step. e-Filing can make the SPT submission process that is more practical, minimal in cost and time, and makes it easier for taxpayers. Because DGT emphasizes technology-based innovation toward a more “lean” tax administration process. With the presence of an online SPT reporting system, it can provide various benefits for taxpayers and the SPT submission process itself, including:

Can simplify the process of recording SPT data in the DGT database. If previously data recording was done manually and spent a lot of time, now with an online tax reporting system, of course, it can save time.

It can reduce the direct meeting of the Taxpayer with the tax officer. Taxpayers no longer have to always come to the KPP, especially taxpayers who live in big cities, who need more time on the road because of traffic jams.

In addition, e-Filing can reduce the impact of queues and the volume of work in the SPT receipt process. The existence of this online SPT report aims to reduce the number of taxpayers who come to the Tax Office so that there are no longer long queues.

Can reduce the volume of physical files or tax documents. The use of an online system will of course reduce the use of paper or documents that taxpayers need to carry. In addition, it can also reduce the risk of lost and damaged documents when stored.

Tax compliance intention

Tax compliance can be defined as an act in which a taxpayer fulfills all tax obligations and exercises the right to pay taxes. There are two types of regulatory compliance: formal compliance and material compliance. Material compliance is the taxpayer’s action to effectively implement all material taxation provisions in accordance with the spirit and content of the tax law. Formal compliance is the act by which a taxpayer seeks to formally fulfill their tax obligations in accordance with the formal provisions of tax law (Cahyonowati, 2011).

One indicator of formal tax compliance is the submission of tax reports through a tax return (SPT). The number of registered taxpayers in 2018 was 38,651,881 with 17,653,963 taxpayers required to submit SPT. Meanwhile, the number of individual taxpayers who reported the 2017 Annual SPT was 10,589,648. That is way, the compliance ratio of the individual SPT in 2018 is only 63.9 percent. The total number of taxpayers who have submitted SPT is equivalent to 70.15 percent of the target of 15.58 million reporting in 2018. Taxpayers registered in 2020 will be 46.38 million and will increase to 49.82 million in 2021 (Pajak.go.id, 2018; Bisnis.com, 2021). Oktaviani et al. (2017) stipulate that an understanding of tax laws is a tax obligation principle so that taxpayers can fulfill their tax obligations. According to Minister of Finance Regulation No 192/PMK.03/2007, an eligible taxpayer is a taxpayer appointed by the Secretary of State as a taxpayer who meets certain criteria. Measuring compliance intent variables requires two approaches: trends and compliance decisions. In tax compliance, intent refers to the taxpayer's will to determine whether or not to comply with the tax. However, not all taxpayer defaults are due to default. The complexity of tax law usually determines the occurrence of tax violations in many places, so unintended or unintended factors can lead to tax evasions.

Dewi & Noviari (2018) state that two factors influence taxpayer compliance, namely external factors and internal factors. Taxpayer compliance is influenced by internal factors if the individual feels that compliance with the obligation to pay taxes is under the individual's control or comes from internal factors such as personality traits, awareness, and abilities. Meanwhile, external factors are factors that affect taxpayer compliance which is influenced from outside the individual/organization, for example, equipment or social influences from other people, meaning that individuals will be forced to behave because of the situation (Manuaba & Gayatri, 2017). The modern taxation system can be classified as an external factor that influences taxpayers to carry out their taxation (Ameur & Tkiouat, 2016).

From the literature above, we can construct the hypothesis below:

H1

Religiosity significantly affects attitudes.

H2

Religiosity significantly affects tax compliant intention.

H3

Attitude significantly affects tax compliant intention.

H4

The utilization of e-Filing as the mediating variable strengthens the effect of religiosity on tax compliant intention.

H5

The utilization of e-Filing as the mediating variable strengthens the effect of attitudes on tax compliant intention.

Research methods

This study used quantitative approaches and used a questionnaire (primary data). The data were analyzed by Structural Equation Model (SEM) with the WarpPLS approach because the model used moderating variables, whereas the WarpPLS approach is very well used in a model with mediating variables. The analysis tools use WarpPLS 6.0 Software (Rinaldo Fernandes et al. 2014; Sumardi & Fernandes 2018; Fernandes & Solimun 2017).

The population of this study was companies that are in the Directorate General of Taxation of Large Taxpayers Jakarta, namely Tax Service Office for Large Taxpayers Category I (One) and Tax Service Office for Large Taxpayers Category II (Two) in a total of 529 companies. The Tax Service Office for Large Taxpayers is divided into 4, and each takes care of different administrations. Here is the explanation:

The Tax Service Office for Large Taxpayers Category I plays a role in administering large taxpayers from the mining sector and mining support services, banking, and financial services.

The Tax Service Office for Large Taxpayers Category II plays a role in administering large taxpayers from the industrial, trade, and service sectors.

The Tax Service Office for Large Category III Taxpayers plays a role in administering taxpayers who are state/state-owned enterprises in the industrial and trade sectors.

The Tax Service Office for Large Taxpayers Category IV plays a role in administering taxpayers from state/state-owned companies in the service sector and large individual taxpayers.

The sample units were chosen, namely Tax Service Office for Large Taxpayers Category I (One) and Tax Service Office for Large Taxpayers Category II (Two), because they are relatively free private companies. The selection of organizations or companies for large taxpayers are the organizations or companies that registered with large KPP WP Category I and Large KPP WP Category II within the Regional Office of the Directorate General of Taxes for Large Taxpayers. This is because both categories consist of private companies that have unlimited choices of corporate actions compared to state-owned companies to maximize corporate profits. The perception held by respondents within the scope of this company may be more varied regarding the understanding of the measured research variables, especially on compliance in paying taxes. On the other hand, Large Taxpayers registered with Large KPP WP Category III and Large KPP WP Category IV include state-owned companies whose corporate action activities are limited and have been regulated by law, so in this case, they are not the object of research because relatively more obedient in paying taxes. The limitation of this study is that it only examines corporate taxpayers included in Categories I and II because this study wants to know the tax compliance of a company/organization. Tax compliance from a company/organization is more attractive than tax compliance from individuals because it contributes more to state tax revenues. The sampling technique used in this study was simple random sampling with sample size was 155 large taxpayers (agencies) in Jakarta. The choice of Jakarta as the research location is because the companies that fall into categories I and II are located in the province of Jakarta only (Fig. 1).

Fig. 1.

Conceptual Framework

Results

The questionnaire is a technique of collecting data from several people or respondents through a set of questions to be answered. By providing the list of questions, the answers obtained are then collected as data. Later, the data are processed and concluded as research results. Some experts have their definition of what a questionnaire is. For example, Narbuko and Achmadi (2015) say that the notion of a questionnaire is a list of a series of questions related to a problem or field to be studied. For studies using quantitative techniques, the quality of data collection is primarily determined by the quality of the equipment or data collection tools used. Research equipment (a questionnaire in the context of this investigation) is considered high quality and may be considered if its effectiveness and reliability have been demonstrated. The validity and reliability of the equipment must be verified, as well as adapted to the type of equipment used in the study. The results of the research instrument validity test are presented in Table 1.

Table 1.

Validity test

| Variable | Indicator | Correlation | Alpha-Cronbach | Result |

|---|---|---|---|---|

| Religiosity (X1) | Faith (ideological) (X1.1) | 0.882 | 0.709 | Valid and Reliable |

| Religious Practices (X1.2) | 0.861 | Valid and Reliable | ||

| Appreciation (X1.3) | 0.776 | Valid and Reliable | ||

| Knowledge (intellectual) (X1.4) | 0.687 | Valid and Reliable | ||

| Practice (Consequences) (X1.5) | 0.987 | Valid and Reliable | ||

| Attitude (X2) | Behavioral Belief (X2.1) | 0.876 | 0.700 | Valid and Reliable |

| Evaluation of Behavioral Belief (X2.2) | 0.731 | Valid and Reliable | ||

| The utilization of e-Filing (X3) | Frequency of Use (X3.1) | 0.801 | 0.800 | Valid and Reliable |

| The simplicity of the System (X3.2) | 0.731 | Valid and Reliable | ||

| Comprehensive Security (X3.3) | 0.661 | Valid and Reliable | ||

| Tax compliant intention (Y1) | Personal Tendency to Behave (Y1.1) | 0.897 | 0.800 | Valid and Reliable |

| The decision to Be Compliant (Y1.2) | 0.774 | Valid and Reliable |

Source: Research Data (2020)

Table 1 shows the corrected item correlation values in the questionnaire for all indicators and items with a value of 0.3 or higher (Solimun et al, 2017). So we can conclude that they are all valid. The next step is to test the reliability of the device. A device is declared reliable if the Cronbach Alpha value is > 0.6 (Solimun et al, 2017). The results of the reliability test of the research instrument showed that the Cronbach's Alpha value of the four research variables was 0.6 or higher. From these results, it can be concluded that religiosity (X1), attitude (X2), use of e-Filing (X3), and intention to pay taxes (Y1) are reasonable and reliable.

The measurement model (the measurement loading value, and the p-value of each indicator for each variable) is shown in Table 2.

Table 2.

Measurement Model

| Variable | Indicator | Loading | p-value |

|---|---|---|---|

| Religiosity (X1) | Belief (ideological) (X1.1) | 0.501 | < 0.001 |

| Religious Practices (X1.2) | 0.500 | < 0.001 | |

| Appreciation (X1.3) | 0.561 | < 0.001 | |

| Knowledge (intellectual) (X1.4) | 0.652 | < 0.001 | |

| Practice (Consequences) (X1.5) | 0.661 | < 0.001 | |

| Attitude (X2) | Behavioral Belief (X2.1) | 0.675 | < 0.001 |

| Evaluation of Behavioral Belief (X2.2) | 0.675 | < 0.001 | |

| The utilization of e-Filing (X3) | Frequency of Use (X3.1) | 0.583 | < 0.001 |

| The simplicity of the System (X3.2) | 0.564 | < 0.001 | |

| Comprehensive Security (X3.3) | 0.679 | < 0.001 | |

| Tax compliant intention | |||

| (Y1) | Personal Tendency to Behave (Y1.1) | 0.513 | < 0.001 |

| The decision to Be Compliant (Y1.2) | 0.513 | < 0.001 |

Source: Research Data (2020)

Based on Table 2, it can be concluded that all these latent variables are appropriate and have good indicators. It can also be used to determine the most dominant indicator (with the highest loading value) contributing to latent composition. The best indicator of religiosity (X1) is belief (ideological) (X1.1). The best indicators (X2) for attitude formation are behavioral beliefs (X2.1) and behavioral belief evaluation (X2.2). The dominant indicator constituting The utilization of e-Filing (X3) is comprehensive security (X3.3). Taxpayer intent (Y1) has the indicators with the highest load factors: personal behavioral tendencies (Y1.1) and obedience decisions (Y2.2).

The second step in the WarpPLS study is to measure the internal model, i.e., the structural model. Structural models represent relationships between study variables. Coefficients in structural models describe the magnitude of the relationship between one variable and another. If the p-value is less than 0.1, the effect of one variable on the other is significant. WarpPLS has two effects: direct effect and indirect effect. Table 3 shows the results of the direct impact test and Table 5 shows the results of the indirect test. For the results of the direct effect test, Table 3 given below.

Table 3.

Result of Estimation and Testing of the Direct Effect

| Relations between variables | Hypothesis | Path coefficient | P-value | Conclusion |

|---|---|---|---|---|

| Religiosity → Attitude | H1 | 0.342 | 0,002 | Significant |

| Religiosity → Tax compliant intention | H2 | 0.267 | < 0,001 | Significant |

| Attitude → Tax compliant intention | H3 | 0.199 | 0,001 | Significant |

| Mediating Variable: The Utilization of e-Filing | ||||

| Religiosity → Tax compliant intention | H4 | 0.251 | 0.063 | Significant |

| Attitude → Tax compliant intention | H5 | 0.188 | 0.072 | Significant |

Source: Research Data (2020)

Table 4 presents the results of the following inner model testing, we can inform that:

There is a significant direct effect of religiosity on attitude (path coefficient of 0.342 and a p-value of 0.002 (less than 0.1)). Considering that the path coefficient is positive, it can be concluded that the higher the religiosity, the attitude will also increase. Based on the concept of Graafland (2017), the factors that are considered to influence attitudes are personality traits, individual circumstances, experience, information, and spiritual needs, namely the traits of religiosity. According to Johnson et al (2001), religion is seen as the extent to which people apply their teachings to make commitments to their religion and beliefs and to ensure that individual attitudes and behaviors reflect that commitment. Several studies have shown that the application of religious values in the workplace can bring about organizational change (Konz & Ryan, 1999; French & Bell, 2001). One of the important aspects of changing an organization is the religious values of its employees. Several studies have shown that religiosity has a positive effect on attitudes toward work (McClelland, 1961; Simmons, 2005; Weaver & Agle, 2002). According to Johnson et al (2001), religion is seen as the extent to which people attach themselves to their religion and beliefs and apply their teachings so that their relationships reflect that commitment. Based on the results, this research was supported/in line with the previous research from McClelland (1961), Simmons (2005), and Weaver & Agle (2002) that shows the positive and significant effect of the relationship between religiosity and attitude.

There is a significant direct effect of religiosity on tax compliant intention (path coefficient of 0.267 and p-value < 0.001 (less than 0.1)). Considering that the path coefficient is positive, it can be concluded that the higher the religiosity, the higher the intention to comply with taxes. In general, whatever religion a person adheres to always teaches and encourages a person to always act positively and prevent negative behavior. With religion, religiosity is formed through strong and positive religious teachings and values which then influence the ethical behavior of people in the social environment, one of which is tax compliance. Damayanti (2018) argues that the religiosity of taxpayers can strengthen their willingness to comply with tax regulations. Every religion teaches its followers to act honestly and comply with all national legal obligations, namely the state’s obligation to pay and report taxes honestly and correctly. Wahyudi’s (2016) and Purwadi & Setiawan’s (2019) studies also show that taxpayer compliance is influenced by religiosity. People who are of higher religion will be more willing and motivated to fulfill their tax obligations. Based on the results, this research was supported/in line with the previous research from Wahyudi (2016) and Purwadi & Setiawan (2019) that shows the positive and significant effect on the relationship between religiosity and tax compliant intention.

There is a significant direct effect of attitude on tax compliant intention (path coefficient of 0.199 and a p-value of 0.001 (less than 0.1)). Considering that the path coefficient is positive, it can be concluded that the higher the altitude, the higher the intention to comply with taxes will be. Alabade et al. (2011) said that the attitude of taxpayers toward tax avoidance is positively related to compliance behavior. In addition, this study shows that the taxpayer's risk appetite has a strong negative to moderate effect on the relationship between tax avoidance attitudes and compliance behavior. The results of this study are by the research concept of Alabede et al. (2011), where attitude has a positive effect on taxpayer compliance in Indonesia. This study shows that attitudes affect Indonesia's intention to comply with tax regulations. Based on the results, this research was supported/in line with the previous research from Alabede et al. (2011) that shows the positive and significant effect on the relationship between attitude and tax compliant intention.

Table 4.

Research Model Quality Index

| Quality index | Statistics-value | Criteria | Conclusion |

|---|---|---|---|

| Average path coefficient (APC) |

0.177 (P = 0.011) |

Significant if p < 0.1 |

Significant |

| Average R-Squared (ARS) |

0.167 (P = 0.01) |

Significant if p < 0.1 |

Significant |

| Average adjusted R-Squared (AARS) |

0.155 (P = 0.02) |

Significant if p < 0.1 | Significant |

| Average block VIF (AVIF) | 1.176 |

Accept if ≤ 5 Ideal if ≤ 3.3 |

Ideal |

| Average full collinearity VIF (AFVIF) | 1.189 |

Accept if ≤ 5 Ideal if ≤ 3.3 |

Ideal |

| Tenenhaus Gof (Gof) | 0.288 |

Small ≥ 0.1 Medium ≥ 0.25 Large ≥ 0.36 |

Medium |

| Sympson’s paradox ratio (SPR) | 1.000 |

Accept if ≥ 0.7 Ideal if = 1 |

Ideal |

| R-Squared contribution ratio (RSCR) | 1.000 |

Accept if ≥ 0.9 Ideal if = 1 |

Ideal |

| Statistical suppression ratio (SSR) | 1.000 | Accept if ≥ 0.7 | Accept |

| Nonlinear bivariate causality direction ratio (NLBCDR) | 1.000 | Accept if ≥ 0.7 | Accept |

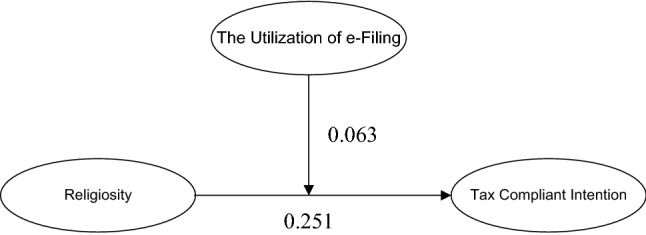

Moderation effect of the utilization of e-Filing on the relationship between religiosity and tax compliant intention

The SEM-WarpPLS analysis results obtained a moderation coefficient is 0.251 and a p-value of 0.063. With α = 10%, since the p-value is < 0.1; the utilization of e-Filing is a moderation variable on the relationship between religiosity and tax compliant intention, and there is a significant positive direct effect on the relationship between religiosity and tax compliant intention (Fig. 2).

Fig. 2.

Moderation Effect of the Utilization of e-Filing on the Relationship between Religiosity and Tax Compliant Intention.

Source Research Data (2020)

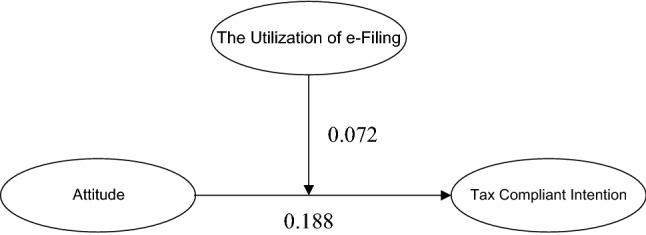

Moderation effect of the utilization of e-Filing on the relationship between attitudes and tax compliant intention

The SEM-WarpPLS analysis results obtained a moderation coefficient is 0.188 and a p-value of 0.072. With α = 10%, since the p-value is < 0.1, the utilization of e-Filing is a moderation variable on the relationship between attitude and tax compliant intention and there is a significant positive direct effect on the relationship between attitude and tax compliant intention (Fig. 3).

Fig. 3.

Moderation Effect of the Utilization of e-Filing on the Relationship between Attitudes and Tax Compliant Intention.

Source Research Data (2020)

The results regarding the effect of utilization of e-Filing in moderating the relationship between attitudes and tax compliant intention and religiosity on tax compliant intention in this study have not been specifically described in previous studies, so this study reveals something new. The Goodness of Fit Criteria of the model can be seen in Table 4.

The feasibility of the model can also be analyzed by calculating the coefficient of determination expressed by R-Square (R2). R-Square is a measure of how well the research model can explain the behavior of the research object (system) being studied. R2 > 0 indicates the model has predictive relevance. R22can be used in this study to see how much variability in the data can explain the model. A predictive relevance value of 0.537 indicates that 53.7% of the diversity of data that can be explained by the model can be explained by the model, i.e., the information contained in 53.7% of the data can be explained by the model. The remaining 46.3% is explained by other variables (not included in the model) and errors. Thus, the structural model that has been formed is appropriate.

Discussion

Based on results, religiosity (X1) and attitude (X2) are known to have a positive and significant effect on the intention to pay (Y1). Several recent studies have demonstrated the importance of religious values in the management of organizational human resources and organizational behavior. Several studies have shown that the application of religious values in the workplace can lead to organizational change (Konz & Ryan, 1999; French & Bell, 2001; Fery, 2003). One of the key aspects that transforms an organization is the religious values of its employees. Several studies have shown that religion has a positive effect on attitudes toward work (McClelland, 1961; Weaver & Agle, 2002; Simmons, 2005). Based on the results of this study, this study supplemented the previous studies of Vahyudi (2016) and Purwadi and Setiawan (2019) and found that it had a positive and significant effect on the relationship between religion and tax payment intention. As a supporter of religious values, Indonesia must have a very strong ethical or moral base to avoid behavior that is detrimental to society as a whole. Various empirical studies show that the realization of religious values can play a role in organizational change.

Religion is usually described as emotional attachment to a religion or behavior and cognitions (religious knowledge, religious beliefs) that influence emotions (Elci, 2007). Religion by Johnson et al. (2001) takes into account the degree to which people are committed to their religion and beliefs and applies their teachings in a way that reflects their attitudes and behaviors. Worthington et al. (2010) Religion or religious commitment is referred to as “the extent to which an individual maintains and applies his or her religious values, beliefs and practices to his or her daily life”. Religion or religious devotion can be divided into two types of devotion. Individual religion stems from individual beliefs and attitudes, and interpersonal religious devotion stems from individual participation in community life or religious groups. Mohdali (2013) argues that the role of religious values is to encourage positive behavior by encouraging good behavior by approving behavior and preventing negative behavior. Religion can be a factor in increasing community self-control and playing an active role in preventing deviant behavior (Purnamasari & Amaliah, 2015). Understanding current taxpayer compliance behavior is not easy. The main challenge is to find the underlying theory of predictable taxpayer compliance so that voluntary compliance of taxpayers can be expected in a dynamic environment (Yusoff and Mohd 2017). This is the problem facing the IRS. In other words, guidance, advice, service and supervision functions well, but the level of tax compliance is not. Many factors lead to tax violations, and achieving full tax compliance is not easy.

Smulders et al. (2015) explains that tax compliance incurs these costs, which affects tax compliance and contributing behavior. Attitudes play an important role in explaining a person's behavior in games, but many other factors influence behavior, including personal background and motivation. Common environmental factors also influence attitudes and behaviors. Attitude behavior is defined as the evaluation of an individual's likes or dislikes of behavior. The higher the score, the more intentions are formed (Byabashija & Katono, 2011) so that the attitudes displayed by individuals can determine their behavior (Nkundabanyanga et al., 2017; Night & Bananuka, 2019; Chong et al., 2018). Economic growth improves the quality of life when people increase their income and spend on positive businesses (Oh & Park, 2020).

Also, attitude (X2) is known to have a positive and significant effect on intention to pay (Y1). This means that an increase in attitude (X2) leads to an increase in taxpayer intent (Y1). Based on the results, this study is consistent/supported with previous work by Alabede et al. (2011) show a positive and significant effect on the relationship between attitude and tax intention. This study is guided by the results of Ajzen's (1991) research on the Theory of Planned Behavior (TPB) which explains that behavior arises because of an intention to behave. Behavioral intentions are influenced by 3 components, namely attitudes, subjective norms, and perceived behavioral control. Ajzen (1991) stated that the more positive the attitude toward behavior, the stronger a person's intention to bring out the behavior. A positive attitude of taxpayers toward taxes will make the behavior obedient toward taxes higher, and it is stated that the more positive the attitude toward behavior, the stronger a person's intention to bring up this behavior.

In addition, the use of electronic filing has a positive and important effect on strengthening the relationship between religion and willingness to comply with taxes, and between attitudes and willingness to comply with taxes. According to TranNam (2015), there are three main models of tax compliance: the avoidance model, tax psychology, and behavioral economics. The traditional prevention model usually emphasizes mandatory costs. The psychological tax model emphasizes the spontaneous nature of prevention and education. Although the behavioral economic model emphasizes compliance by examining the behavior of taxpayers. The state has launched a "e-Filing" initiative to facilitate taxpayer tax filings, primarily based on taxpayer education and behavior. This will automatically facilitate an increase in state tax rates and an increase in tax revenue. The results of research on the effectiveness of using e-Filing in mitigating the relationship between religion and tax attitudes and tax intentions in this study have not been specifically explained in previous studies. Therefore, this survey reveals something new and is a novelty of our survey.

The Directorate General of Taxes (DGT) has introduced a program for submitting Annual Income Tax Returns (SPT) through an electronic application known as e-Filing since 2004. This step follows several countries that are classified as developed which have introduced e-Filing first. Learning from their experiences, DGT sees that in addition to providing benefits for taxpayers and tax authorities, the use of e-Filing is also environmentally friendly (go green). From the taxpayer's perspective, reporting using e-Filing provides flexibility regarding time and place. Taxpayers can use the e-Filing application at any time, no longer limited to working days and hours, because e-Filing can still be accessed on holidays and after working hours. Taxpayers also no longer need to queue and spend valuable time at the Tax Service Office just waiting for the receipt of the Annual SPT.

In addition, e-Filing also provides convenience for taxpayers in filling out their Annual Income Tax Returns. Taxpayers no longer need to be confused about filling out the Annual Income Tax Return, because they will be guided by this application wizard. Taxpayers only need to answer questions that appear on the computer or tablet screen they are using. However, taxpayers who are accustomed to filling out forms can still use them.

For DGT itself, the use of the e-Filing application can increase the efficiency of using the budget. The budget for procurement and file maintenance can be reduced, as will the budget for printing the Annual SPT form. In addition, in terms of human resources, DGT can maximize existing employees to improve other services, explore tax potential and carry out law enforcement in the field of taxation. When using this application, taxpayers no longer need to use paper in compiling their annual income tax return. Thus, the use of e-Filing simultaneously increases the efficiency of paper use when compared to when the taxpayer reports his annual income tax return manually. Data for 2012 show that the DGT received 9.48 million Annual Tax Returns. On average, one Annual SPT requires 4 (four) pieces of paper, so the number of papers used to report the Annual Income Tax Return reaches nearly 38 million pieces. As is known, paper is made from tree trunks. Reducing paper usage means participating in making the earth greener.

In this study the indicators are used to refer to individuals rather than organizational characteristics, this is because in this study it is assumed that the directors/financial managers who act as respondents in this study can reflect the organizations that they represent. Therefore, in this study, the characteristics of individual representatives of the organization under study become a reflection of the organization as a whole. This can also be used as a research limitation, so that in future research it may be possible to provide several respondents in 1 organization so that in 1 organization several people are represented.

Conclusion

Based on the results of empirical analysis, it can be concluded that there is a significant and positive effect between religion and intention to comply with taxes. There is an important and positive influence between attitude and intention of tax compliance. In addition, the use of e-Filing as a moderating variable to improve the relationship between religion and attitudes toward tax compliance has positive but significant benefits. Based on the survey results above, it can be said that the results of this survey are more comprehensive than previous surveys regarding the use of electronic filing for religion, attitudes, and taxation. The results of this study can make an important theoretical contribution to the development of scientific knowledge.

The contribution of this research to the development of science is the result of research to test and refine the theory developed in this research and is also the consistency of the results of previous research. The results of this study indicate that religion is the dominant factor influencing the intention to pay taxes. However, the way knowledge management is implemented requires not only being shaped by it but also the appropriate attitude. The simplicity of the system in the electronic filing system should be a major challenge for advances in knowledge management practices and improvements in tax law.

Declarations

Conflict of interest

Authors declare that there is no conflict of interests.

Footnotes

The original online version of this article was revised: Three references “(Rinaldo Fernandes et al. (2014); Sumardi & Fernandes (2018); Fernandes & Solimun (2017)” have been missed to insert in the reference list. Missing references have been added in the reference list.

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Change history

8/28/2022

A Correction to this paper has been published: 10.1057/s41264-022-00177-6

Contributor Information

Kadarisman Hidayat, Email: kadarisman.ub@gmail.com.

Mekar Satria Utama, Email: mekarsatria08.fia@gmail.com.

Umar Nimran, Email: umar.nimran.ub@gmail.com.

Arik Prasetya, Email: prasetyaarik2@gmail.com.

References

- Ajzen I. The theory of planned behavior. Organizational Behavior and Human Decision Processes. 1991;50(2):179–211. doi: 10.1016/0749-5978(91)90020-T. [DOI] [Google Scholar]

- Ajzen, I. (2005). Attitudes, personality, and behavior. UK: McGraw-Hill Education.

- Ajzen I, Fishbein M. A Bayesian analysis of attribution processes. Psychological Bulletin. 1975;82(2):261. doi: 10.1037/h0076477. [DOI] [Google Scholar]

- Alabede JO, Ariffin ZZ, Idris KM. Individual taxpayers attitude and compliance behavior in Nigeria: The moderating role of financial condition and risk preference. Journal of Accounting and Taxation. 2011;3(3):91–104. [Google Scholar]

- Ameur F, Tkiouat M. A Contribution of Expected Utility Theory in Taxpayers’ Behavior Modeling. International Journal of Economics and Financial Issues. 2016;6(3):1217–1224. [Google Scholar]

- Bobek DD, Hatfield RC. An investigation of the theory of planned behavior and the role of moral obligation in tax compliance. Behavioral Research in Accounting. 2003;15(1):13–38. doi: 10.2308/bria.2003.15.1.13. [DOI] [Google Scholar]

- Byabashaija W, Katono I. The impact of college entrepreneurial education on entrepreneurial attitudes and intention to start a business in Uganda. Journal of Developmental Entrepreneurship. 2011;16(01):127–144. doi: 10.1142/S1084946711001768. [DOI] [Google Scholar]

- Calhoun, C. (2006). The University and the Public Good. Thesis Eleven. 84: 7–43. 10.1177/0725513606060516.

- Cahyonowati, N. (2011). Model moral dan kepatuhan perpajakan: wajib pajak orang pribadi. Jurnal Akuntansi Dan Auditing Indonesia, 15(2).

- Chong ZR, Zhao J, Chan JHR, Yin Z, Linga P. Effect of horizontal wellbore on the production behavior from marine hydrate-bearing sediment. Applied Energy. 2018;214:117–130. doi: 10.1016/j.apenergy.2018.01.072. [DOI] [Google Scholar]

- Damayanti, T. W. (2018). Tax Compliance: Between Intrinsic Religiosity and Extrinsic Religiosity. Journal of Economics, Business & Accountancy Ventura (JEBAV), Vol 21(No.1), 41–49

- Dewi NLPP, Noviari N. Pengaruh ukuran perusahaan, leverage, profitabilitas dan corporate social responsibility terhadap penghindaran pajak (tax avoidance) Sumber. 2016;1(166):20. [Google Scholar]

- Elci, M. (2007). Effect of manifest needs, religiosity and selected demographics on hard working: An empirical investigation in Turkey. Journal of International Business Research, 6 (2): 97.

- Elçi, M., Sener, İ., & Alpkan, L. (2011). The Impact of Morality and Religiosity of Employees on Their Hardworking Behavior. Procedia-Social and Behavioral Sciences, 24: 1367–1377.

- Fernandes, A.A.R. and Solimun. (2017). Moderating effects orientation and innovation strategy on the effect of uncertainty on the performance of business environment. International Journal of Law and Management, 59(6): 1211–1219. 10.1108/IJLMA-10-2016-0088

- Fery YA. Differentiating visual and kinesthetic imagery in mental practice. Canadian Journal of Experimental Psychology/revue Canadienne De Psychologie Expérimentale. 2003;57(1):1–10. doi: 10.1037/h0087408. [DOI] [PubMed] [Google Scholar]

- French, W. L., & Bell, C. H. (2001). Organization development: behavioral science interventions for organization improvement (No. HD38 F69). New Jersey: Prentice-Hall.

- Glock C, Stark R. Is there American Protestantism? New Jersey: Transaction; 1965. [Google Scholar]

- Graafland, J. (2017). Religiosity, attitude, and the demand for socially responsible products. Journal of Business Ethics, 144 (1): 121–138.

- Hariyono, H. (2021). Do Economic Attitudes Drive Employee Productivity? Lesson from Indonesia. The Journal of Asian Finance, Economics, and Business, 8(1), 1009–1016. 10.13106/jafeb.2021.vol8.no1.1009

- Jalaluddin. R. (1996). Psikologi Komunikasi. Jakarta: Remaja Rosdakarya.

- Jayawardane, D., & Low, K. (2016). Taxpayer attitude and tax compliance decision in SriLanka. International Journal of Arts and Commerce, 5 (2): 124.

- Johnson BR, Jang SJ, Larson DB, De Li S. Does adolescent religious commitment matter? A reexamination of the effects of religiosity on delinquency. Journal of Research in Crime and Delinquency. 2001;38(1):22–44. doi: 10.1177/0022427801038001002. [DOI] [Google Scholar]

- Konz GN, Ryan FX. Maintaining an organizational spirituality: No easy task. Journal of Organizational Change Management. 1999;12(3):200–210. doi: 10.1108/09534819910273865. [DOI] [Google Scholar]

- Manuaba IACA, Gayatri. Pengaruh Pengetahuan Pemahaman Peraturan Pajak, Pelayanan Fiskus, Persepsi Efektivitas Sistem Perpajakan Terhadap Kemauan Membayar Pajak. E-Jurnal Akuntansi. 2017;19(2):1259–1289. [Google Scholar]

- McClelland, D. C. (1961). Achieving society (No. 15). Simon and Schuster.

- Mohdali, N. R. (2013). The influence of religiosity on tax compliance in Malaysia (Doctoral dissertation, Curtin University).

- Narbuko, C. & Achmadi, A. (2015). Metodologi Penelitian. Bumi Aksara. Jakarta.

- Nashori, F. N., & Mucharam, R. D. (2002). Mengembangkan kreativitas dalam perspektif psikologi islam. Penerbit Menara Kudus. Kudus.

- Nguyen, O. T. (2020). Factors affecting the intention to use digital banking in Vietnam. The Journal of Asian Finance, Economics, and Business, 7(3), 303–310. 10.13106/jafeb.2020.vol7.no3.303

- Night S, Bananuka J. The mediating role of adoption of an electronic tax system in the relationship between attitude towards electronic tax system and tax compliance. Journal of Economics, Finance and Administrative Science. 2019;25(49):73–88. doi: 10.1108/JEFAS-07-2018-0066. [DOI] [Google Scholar]

- Nkundabanyanga, S. K., Mvura, P., Nyamuyonjo, D., Opiso, J., & Nakabuye, Z. (2017). Tax compliance in a developing country: Understanding taxpayers’ compliance decision by their perceptions. Journal of Economic Studies 44(6): 931–957.

- Oh, A. H., & Park, H. Y. (2020). The Effect of Airline's Professional Models on Brand Loyalty: Focusing on Mediating Effect of Brand Attitude. The Journal of Asian Finance, Economics, and Business, 7(5), 155–166. 10.13106/jafeb.2020.vol7.no5.155

- Oktaviani, R. M., Hardiningsih, P., & Srimindari, C. (2017). Kepatuhan Wajib Pajak Memediasi Determinan Penerimaan Pajak Penghasilan. Journal Akuntansi, 21(2): 318–335.

- Purnamasari P, Amaliah I. Fraud prevention: Relevance to religiosity and spirituality in the workplace. Procedia-Social and Behavioral Sciences. 2015;211:827–835. doi: 10.1016/j.sbspro.2015.11.109. [DOI] [Google Scholar]

- Purwadi, M. O. D., & Setiawan, P. E. (2019). Pengaruh Religiusitas , Pelayanan Fiskus dan Sanksi Pajak pada Kepatuhan Wajib Pajak Orang Pribadi. E-JA: E Jurnal Akuntansi, 2110–2125

- Rahman A, Asrarhaghighi E, Ab Rahman S. Consumers and Halal cosmetic products: Knowledge, religiosity, attitude, and intention. Journal of Islamic Marketing. 2015;6(1):148–163. doi: 10.1108/JIMA-09-2013-0068. [DOI] [Google Scholar]

- Resmi, S. (2016). Perpajakan: Teori dan Kasus (Edisi 9 Buku 1). Jakarta: Salemba Empat.

- Rinaldo Fernandes, A. A., Budiantara, I. N., Otok, B. W., Suhartono. (2014). Reproducing kernel Hilbert space for penalized regression multi-predictors: case in longitudinal data. International Journal of Mathematical Analysis, 8(40): 1951–1961. 10.12988/ijma.2014.47212

- Simmons WP, Parsons S. Beliefs in conspiracy theories among African Americans: A comparison of elites and masses. Social Science Quarterly. 2005;86(3):582–598. doi: 10.1111/j.0038-4941.2005.00319.x. [DOI] [Google Scholar]

- Smulders, S., Stiglingh, M., Franzsen, R., & Fletcher, L. (2015). Determinants of internal tax compliance costs: Evidence from South Africa. Journal of Economic and Financial Sciences, 9 (3): 714–729

- Soemitro, R. (2013). Perpajakan Teori dan Kasus. Jakarta: Gramedia.

- Solimun., Fernandes, A.A.R., & Nurjannah. Multivariate Statistical Method: Structural Equation Modeling Based on WarpPLS. Malang: UB Press; 2017. [Google Scholar]

- Stack, S., & Kposowa, A. (2006). The Effect of Religiosity on Tax Fraud Acceptability: A Cross-National Analysis. Journal for The Scientific Study of Religion - 45. 10.1111/j.1468-5906.2006.00310.x [DOI] [PubMed]

- Sumardi, and Fernandes, A.A.R. (2018). The mediating effect of service quality and organizational commitment on the effect of management process alignment on higher education performance in Makassar, Indonesia. Journal of Organizational Change Management, 31(2): 410–425. 10.1108/JOCM-11-2016-0247

- Yusoff, S. N., & Mohd, S. (2017). How Well-Informed Are Taxpayers On Their Income Tax Payment?. Journal of Global Business and Social Entrepreneurship (GBSE), 3(9).

- Wahyudi. Pengaruh Religiusitas terhadap Perilaku Kepatuhan Wajib Pajak Orang Pribadi di Provinsi DKI Jakarta. Jurnal Lingkar Widyaiswara. 2016 doi: 10.1016/S0040-4020(00)00446-4. [DOI] [Google Scholar]

- Weaver GR, Agle BR. Religiosity and ethical behavior in organizations: A symbolic interactionist perspective. Academy of Management Review. 2002;27(1):77–97. doi: 10.5465/amr.2002.5922390. [DOI] [Google Scholar]

- Wibowo, H. A., & Masitoh, M. R. (2018). Measuring religiosity and its effects on attitude and intention to wear a hijab: Revalidating the scale In Increasing Management Relevance and Competitiveness (pp. 237–240). CRC Press.

- Worthington EL, Greer CL, Hook J, Davis D, Gartner AL, Jennings li, D. J., Norton, L., Van Tongeren, D. R., Greer, T. W., & Toussaint, L. Forgiveness and spirituality in the organizational life: Theory, the status of research, and new ideas for discovery. Journal of Management Spirituality & Religion. 2010;7(2):119–134. doi: 10.1080/14766081003765273. [DOI] [Google Scholar]

Website

- Bisnis.com. (2021). Sri Mulyani Bandingkan Kondisi Wajib Pajak Saat jadi Menkeu pada 2005 dan Masa Kini. https://ekonomi.bisnis.com/read/20210628/259/1410786/sri-mulyani-bandingkan-kondisi-wajib-pajak-saat-jadi-menkeu-pada-2005-dan-masa-kini. Accessed in May 12nd 2022

- Pajak.go.id. (2018). https://www.pajak.go.id/sites/default/files/2019-05/LAKIN DJP 2018. pdf. Accessed on May 12nd 2022