Abstract

Purpose

Oncology drugs are often approved for multiple indications, for which their clinical benefit varies. Aligning a single price to this differing value remains a challenge. This study examines the clinical and economic value, price, and reimbursement of multi-indication cancer drugs across seven countries, representing different approaches to value assessment, pricing, and coverage decisions: the USA, Germany, France, England, Canada, Australia, and Scotland.

Methods

Twenty-five multi-indication cancer drugs across 100 indications were identified with US Food and Drug Administration (FDA) approval between 2009 and 2019. For each indication data on Health Technology Assessment (HTA) recommendations, disease prevalence, and drug prices were obtained. Quality-adjusted life years (QALYs) gained, disease prevalence, list prices, and HTA outcomes were then compared across indications and regions.

Results

First approved indications provide a higher clinical benefit whilst targeting a smaller patient group than indication extensions. Quality-adjusted life year gains were higher for first (0.99, 95% CI 0.05–3.25) compared to second (0.51, 95% CI 0.02–1.63, p < 0.001) and third (0.58, 95% CI 0.05–2.07, p < 0.01) approved indications. Disease prevalence per 100,000 inhabitants was 20.7 (95% CI 0.2–63.3) for first compared to 27.1 (95% CI 1.5–109.6, p = 0.907) for second and 128.3 (95% CI 3.1–720.1, p < 0.001) for third approved indications. With each approved indication drug prices declined in Germany and France, remained constant in the UK, Canada, and Australia, whilst they increased in the USA. Negative HTA outcomes, clinical restrictions, and managed entry agreements (MEAs) were more frequently observed for indication extensions.

Conclusions

Results suggest that indication development is prioritised according to clinical value and disease prevalence. Countries employ different mechanisms to account for each indication’s differential benefit, e.g., weighted-average prices (Germany, France, Australia), differential discounts (England, Scotland), clinical restrictions, and MEAs (England, Scotland, Australia, Canada). Value-based indication-specific pricing can help to align the benefit and price for multi-indication cancer drugs.

Supplementary Information

The online version contains supplementary material available at 10.1007/s40258-022-00737-w.

Key Points for Decision Makers

| Results demonstrate that manufacturers maximise revenues by sequencing indication launches to set the highest possible drug price: cancer drugs are first launched for rare diseases that offer significant QALY gains and then extended to indications that deliver lower QALY gains to more eligible patients. |

| In theory, “pure” value-based indication-specific pricing - one price per indication - could help to align the clinical benefit and price for multi-indication cancer drugs. |

| In practice, countries employ a variety of methods, such as weighted-average prices, indication-specific discounts, clinical restrictions, and MEAs, to reflect each indication’s differential value. |

Introduction

Over the past 20 years, cancer treatment has rapidly evolved through new immuno-therapies and targeted drugs [1]. Due to their mode-of-action, these novel drugs are often effective for multiple cancer types (indications). In 2018, 75% of oncology drugs have been approved for multiple indications [2]. The relative value a drug delivers across indications may vary substantially given different standards of care and levels of unmet need [3]. Additionally, multi-indication drugs offer dynamic efficiency gains for patients and manufacturers as lengthy and costly research and pre-clinical testing efforts only occur once per drug. Expanding drugs to new indications increases revenues, profits, returns, and valuations for manufacturers [4, 5]. However, pricing and reimbursement mechanisms have not evolved at the same pace as pharmaceutical development, intensifying concerns about the affordability of new drugs. The rise of combination and pan-tumour treatments further increases pressure to innovate pricing models.

Economic Incentives Under Current Drug Pricing Policies

The most prevalent drug pricing model, i.e. “single (lowest) price mechanisms” with “one price for one drug”, decouples price and value of multi-indication drugs. Under a single price policy, manufacturers may be incentivised to prioritise, delay, withhold, or brand certain indications in order to achieve the highest possible price and profit [6, 7]. Theory suggests that manufacturers first launch drugs for indications with high clinical benefit and strong clinical evidence among small population groups (Fig. 1A). Based on this strong clinical evidence, manufacturers can demand the maximum list price for multi-indication drugs, which minimally impacts healthcare budgets due to a small population target group. Thereafter, manufacturers aim to expand drugs to indications in a larger patient population with lower clinical benefit. Subsequently, single drug pricing policies may cause manufacturers to withhold or withdraw indications due to potential off-label usage or price deteriorations of previously launched indications.

Fig. 1.

Indication launch decisions under single-price policies: A theory and B evidence. A shows the differential value and number of patients for a given drug per indication. Indication development follows the natural order A, B, C, then D - priced at then . Theory suggests that manufacturers may be incentivised to sequence and withhold indications according to clinical value and number of patients to extract the highest possible prices ( and ) under a single pricing mechanism [6, 7, 12]. B illustrates evidence from a sample of 25 multi-indication cancer drugs. This evidence suggests that launch sequences are indeed prioritized by number of patients (measured by disease prevalence [23]) and clinical value (measured by incremental QALYs extracted from health technology assessment reports). Indications offering marginal incremental QALYs for a small population group are not launched. QALY quality-adjusted life year. Source(s) [6, 7, 12, 23]

Indication-Specific Pricing

Indication-specific pricing (ISP), also referred to as indication-based pricing (IBP) or multi-indication pricing (MIP), is a differential pricing method that distinctly prices a drug according to the additional value it delivers for each indication [8]. Thereby, ISP restores the price-value link [9]. There is an ongoing theoretical debate about the pros and cons of ISP [7, 10, 11]. The primary benefits of ISP are rationalising drug prices, increasing transparency, granting timely access to medicines for patients, and encouraging the dynamic launch of indications by reducing research and development (R&D) risks for manufacturers. Therefore, ISP could serve all parties, by expanding access to patients, containing payers’ costs through additional consumer surplus, and increasing revenues for manufacturers. In contrast, Chandra and Garthwaite noted that under ISP consumer surplus distribution may favour manufacturers and thus increase payers' budget impact at least in the short term [12]. Although scholars recognise this risk, they argued that increased competition resulting from the dynamic launch of new indications will drive down prices and payers’ budget impact in the long term [6, 7, 10, 11, 13].

Indication-specific pricing is of special interest for marketing authorisation (MA) and health technology assessment (HTA) agencies as the rise of multi-indication oncology drugs with differential value and cost characteristics is not yet reflected in most rigid regulatory processes. Indication-specific marketing approval is crucial to account for varying safety and efficacy profiles. More importantly, HTA agencies must address fluctuating efficiency, effectiveness, and affordability on an indication level. Drug pricing ought to adjust for differential value with distinct pricing mechanisms to re-establish efficiency and affordability. Therefore, governments and insurers face several policy dilemmas concerning how to reflect indications’ differential value in already strictly defined reimbursement systems. Monitoring at an indication level, complex distribution systems, high administrative costs, fierce opposition of key stakeholders, legal barriers, and privacy concerns are the main hurdles to implement ISP [7, 14, 15]. Countries attempted to address challenges of multi-indication pricing through indirect ISP methods, such as differential discounts, weighted-average prices, clinical restrictions, as well as financial and outcome-based managed entry agreements (MEAs) [6, 15–17].

Study Objectives

A variety of studies theoretically analyse and review multi-indication drugs regarding economic frameworks [6, 9, 11, 12, 17], healthcare evaluations [3, 16, 18, 19], implementation feasibility across countries [7, 10, 13–15, 20–22], or single case studies [8, 19]. Yet, there remains a lack of evidence examining launch decisions and timely patient access under different pricing policies. This paper examines the value and pricing of multi-indication cancer drugs across seven countries: England, Scotland, France, Germany, Canada, Australia, and the USA. There are two main objectives:

First, to analyse clinical and economic value alongside target population size per indication. Consequently, incremental cost-effectiveness ratios (ICERs), incremental quality-adjusted life years (QALYs) and life years (LYs) gained, and disease prevalence are explored across first, second, subsequent, and not launched indications.

Second, to examine reimbursement and drug pricing of multi-indication drugs across nations. The progression of list prices and HTA reimbursement decisions alongside the use of clinical restriction and MEA is analysed by indication sequence.

Data and Methods

Sample Selection

US Food and Drug Administration drug approvals from January 1st, 2009, to January 1st, 2019, were screened to identify 99 drugs with multiple indications. Twenty-five of these multi-indication drugs were selected for further analyses (Fig. 2). Selection was based on two prioritisation criteria. First, the sample focused on oncology drugs to ensure comparability of clinical trial data. Second, only drugs with at least two monotherapy treatments were prioritised to exclude confounding effects of combination treatments. For selected molecules, all indications were factored into the analysis (including combination therapies and non-oncology indications).

Fig. 2.

Flow diagram of multi-indication drugs included in the analysis, 2009–2019. CADTH Canadian Agency for Drugs and Technologies in Health, EMA European Medicines Agency, FDA US Food & Drug Administration, G-BA Federal joint Committee (“Gemeinsamer Bundesausschuss”), HAS Haute Autorité de Santé, HC Health Canada, NICE National Institute of Health and Care Excellence, PBAC Pharmaceutical Benefits Advisory Committee, SMC Scottish Medicines Consortium, TGA Therapeutic Goods Administration

Data Sources

Data for these 25 multi-indication cancer drugs were collected in seven countries: England, Scotland, France, Germany, Canada, Australia, and the USA. Public availability of regulatory documents (HTA reports) and language (English, French, German) were the criteria for country selection. For all 25 products, HTA data were collected from the respective agency website until July 1st, 2020 (Supplement 1, Table e1).

Furthermore, indications were matched on a country basis with their disease prevalence published by the Global Burden of Disease Study in 2017 [23]. Monthly drug price data were collected from the IQVIA sales database for the UK (England and Scotland), France, Germany, Canada, and the USA. Data on drug prices were not available for Australia.

Collected Variables

The following variables were extracted from HTA reports (Supplement 1, Table e2 and e3): (1) submission, (2) outcome, (3) approval date, (4) economic (financial and outcome-based) restrictions, (5) clinical (population and dosing) restrictions, (6) incremental QALYs gained, (7) incremental LYs gained, and (8) ICER. Health technology assessment outcomes were classified as positive (list or list with condition) or negative (do not list). Given the lack of a formal HTA process in the USA, data on QALYs, LYs, and ICERs were retrieved from a peer-reviewed literature search covering the PubMed database during July 2020 of economic evaluations for all included indications.

Statistical Analyses

A launched indication was defined as an indication with both regulatory approval and an available HTA reimbursement decision in the specific jurisdiction. In the USA, a launch was defined solely based on the regulatory FDA approval due to the absence of a HTA agency. We coded the indication launch sequence as first, second, subsequent, and not launched according to the HTA approval date in each country.

QALY, LY, Disease Prevalence, and ICER by Indication Launch Sequence

In order to measure the clinical and economic benefit each indication offers, we compared incremental QALY and LY gains as well as the ICER across indication launches and countries. Similarly, the patient population - measured by disease prevalence - that stands to benefit was then compared across indication launches. Outliers with a disease prevalence beyond 1 per 100 inhabitants resulting from non-cancer indications were excluded from the analysis. Therefore, dimethyl fumarate and aflibercept were excluded due to their indication approvals for psoriasis and diabetic retinopathy, respectively. We finally mapped incremental QALYs gained over disease prevalence for first, second, third, and not launched indications to visualise results.

List Prices, HTA Outcomes, and HTA Restrictions by Indication Launch Sequence

First, we compared the list price progression of new indication launches within countries. Therefore, the average change in list prices from first to second and first to third indication was calculated. Subsequently, list prices per country were converted to US dollars and then compared to UK prices. This comparison was selected because UK list prices remain largely constant over time unless price changes are mandated through the VPAS (former Pharmaceutical Price Regulation Scheme [PPRS]) and are not affected by patient access schemes (PAS), which, in the majority of cases, result in a confidential discount.

Second, the average percentage of positive recommendations was compared across new indication launches. Similarly, the average number of positive recommendations with clinical and economic restrictions was then calculated per country.

Statistical Methods

After data were extracted and stored in Microsoft EXCEL, analyses were performed with STATA SE Version 15.1. Numerical data were expressed as means and frequencies. p values were calculated based on ANOVA with Dunnett’s-test, Students’ t tests, and χ2-tests. A two-tailed probability value below 0.05 was considered significant.

Results

Twenty-five drugs with a total of 100 indications were included in the final analysis (Supplement 1, Table e4). In total, 91.0% of collected indications treated oncologic diseases with 70.0% solid and 21.0% haematologic cancer treatments (Supplement 1, Table e5). Some cancer drugs were also approved for non-cancer indications, e.g. aflibercept or nintedanib. In line with prior sample selection, 82.0% of indications were monotherapy treatments. In total, 62.0% of indications were launched as 2nd-, 3rd-, or 4th-line treatments, while 38.0% were launched as 1st-line treatments. The total number of indication launches varied significantly across countries. Most indication launches were observed in the USA (N = 96), followed by Germany (N = 80), France (N = 78), Scotland (N = 68), England (N = 67), Australia (N = 63), and Canada (N = 57) (Supplement 1, Table e6).

Quality-Adjusted Life Years, LY, Disease Prevalence, and ICER by Indication Launch Sequence

Data on QALYs and LYs gained were only reported for a subset of indications. Data on ICERs were available in England (N = 51), Scotland (N = 56), France (N = 27), Canada (N = 30), and the USA (N = 41). Disease prevalence rates, ICERs, incremental QALYs and LYs gained varied significantly across indication sequence (Fig. 3).

Fig. 3.

Indication characteristics by launch sequence. Average incremental QALYs gained (A), incremental LYs gained (B), disease prevalence (C), and ICERs (D) are compared across indication launch sequence. p values presented on the error bars compare the first to second, first to third, and first to not launch indications. p values on top of the graphs compare launched to not launched indications. p values calculated based on ANOVA with Dunnett’s-test and Student’s t test: *p < 0.05, **p < 0.01, ***p < 0.001. Bars show 95% confidence intervals. ICER incremental cost-effectiveness ratio, LY life year, QALY quality-adjusted life year

Average incremental QALYs and LYs gained decreased with the launch of new indications (Fig. 3A, B). Quality-adjusted life-year gains were higher for first (0.99, 95% CI 0.05–3.25) compared to second (0.51, 95% CI 0.02–1.63, p < 0.001) and third (0.58, 95% CI 0.05–2.07, p < 0.01) launched indications. Similarly, LYs gained were 1.73 (95% CI 0.08–5.39) for first, 0.94 (95% CI 0.11–3.47, p < 0.01) for second, and 0.96 (95% CI 0.21–3.58, p < 0.05) for third launched indications. On average, launched indications provided a gain of 0.78 QALYs (95% CI 0.02–2.26) and 1.30 LYs (95% CI 0.11–3.61), while not launched indications increased QALYs by 0.39 (95% CI 0.01–1.24, p < 0.001) and LYs by 0.68 (95% CI 0.13–2.87, p < 0.05).

The average disease prevalence rate increased with the launch of new indications (Fig. 3C). Disease prevalence (per 100,000) was 20.7 (95% CI 0.2–63.3) for first compared to 27.1 (95% CI 1.5–109.6, p = 0.907) for second and 128.3 (95% CI 3.1–720.1, p < 0.001) for third launched indications. Disease prevalence did not differ between launched (121.2, 95% CI 0.4–558.0) and not launched (94.4, 95% CI 1.3–151.2, p = 0.538) indications.

The average ICER increased with indication sequence in France, Canada, and the USA, yet not England and Scotland (Fig. 3D). Average ICERs increased from first versus second versus third launched indications in France (EUR 90,416 vs 84,983 vs 136,763, p = 0.180), Canada (CAD 112,859 vs 150,386 vs 181,054, p = 0.390), and the USA (USD 188,382 vs 513,249 vs 515,144, p = 0.250). In England (GBP 49,248 vs 52,761, p = 0.192) and Scotland (GBP 45,694 vs 39,440, p = 0.142) ICERs were similar for first and third launched indications.

Mapping incremental QALYs gained and disease prevalence per indication sequence yields the graph shown in Fig. 1B. In summary, drugs are first launched in indications with high clinical benefit and a low disease prevalence. However, indication extensions target larger patient populations whilst providing a comparatively lower clinical benefit.

Drug Prices, HTA Outcomes, and HTA Restrictions by Indication Launch Sequence

Drug prices progressed differently across countries throughout the launch of new indications (Fig. 4A). Prices declined in Germany and France, did not change in the UK and Canada, and rose in the USA. In Germany, prices declined by − 16.6% (p < 0.001) for second, − 32.1% (p < 0.001) for third and − 42.7% (p < 0.001) for fourth relative to first indications. The price decline was more gradual in France with respective decreases of − 7.7% (p < 0.01), − 14.1% (p < 0.001), and − 17.0% (p < 0.01). Conversely, prices increased by + 23.9% (p < 0.05), + 22.5% (p = 0.110), and + 27.9% (p = 0.064) in the USA.

Fig. 4.

Change in drug list prices by indication launch sequence. A illustrates the percentage change of list prices from first to second, first to third, and first to fourth launched indication according to health technology assessment approval date in the UK, France, Germany, Canada, and the USA. B presents list prices relative to UK values for first, second, and subsequently launched indications. Bars show 95% confidence intervals. p values: *p < 0.05, **p < 0.01, ***p < 0.001

Relative to UK list price levels, prices in Germany were + 15.0% (p < 0.05) higher for first, equal for second (p = 0.649), and − 9.2% (p < 0.05) lower for subsequent indications (Fig. 4B). A similar, not significant, price evolution can be observed in France. Throughout the entire indication sequence, prices in the USA were at least 68.9% higher compared to the UK (p < 0.01).

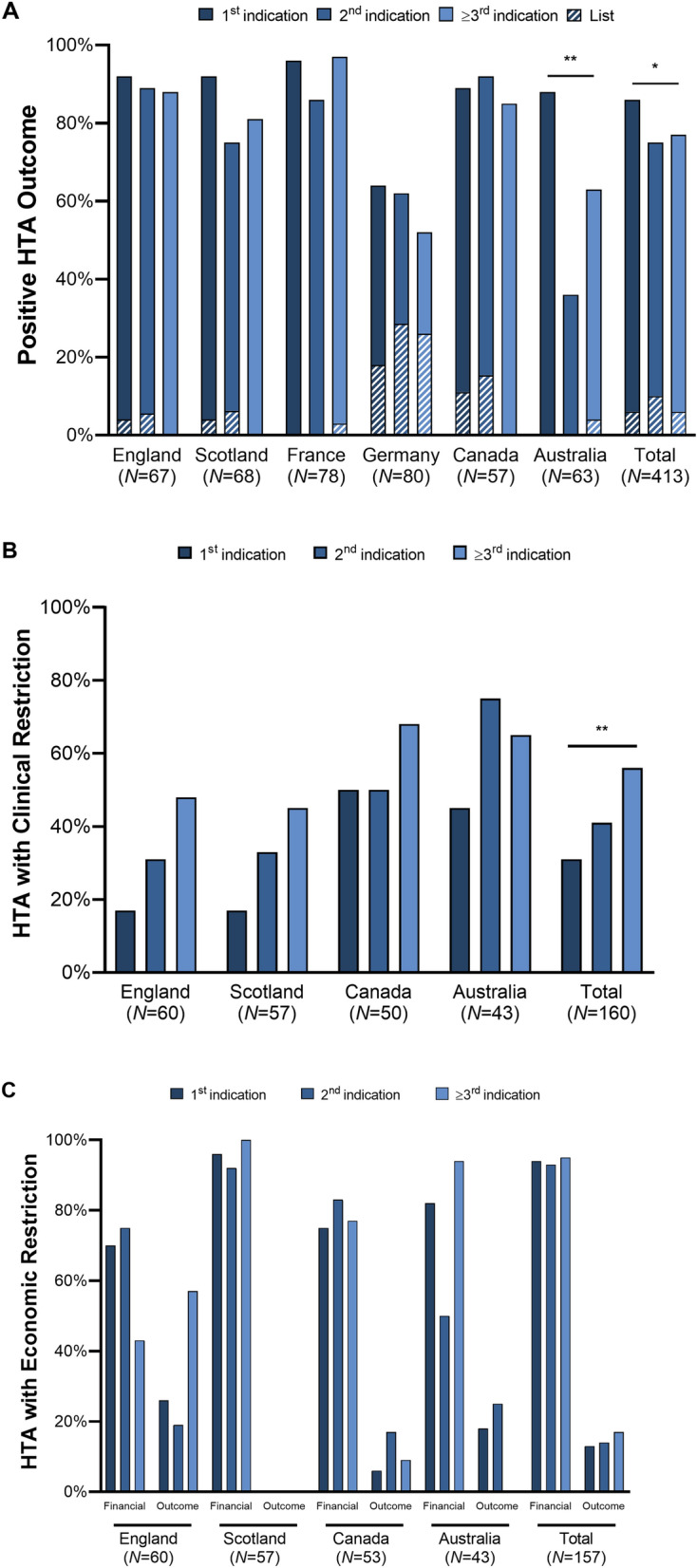

Overall, HTA outcomes varied across nations (Fig. 5A). On an aggregate level, first indications (86.4%) more frequently received a positive HTA recommendation, than second (75.0%) and subsequent (77.0%) launches (χ2(2,N=412) = 6.23, p < 0.05). Clinical restrictions and MEAs were only observed in England, Scotland, Canada, and Australia (Fig. 5B). Overall, 31.0% of first, 40.9% of second, and 56.1% of subsequent indications had clinical restrictions (χ2(2, N=210) = 10.80, p < 0.01). This trend proved only significant on an aggregate level due to small sample sizes. Financial and/or outcomes-based MEAs were implemented across the study countries, but data is only available in England, Scotland, Australia, and Canada. No significant trend across indication launches could be observed (Fig. 5C). Our study results are presented for each country in Supplement 2.

Fig. 5.

HTA outcomes by indication launch sequence. A presents the percentage of positive HTA outcomes across countries. Positive outcomes include “list” and “list with condition”. B shows the percentage of decisions with clinical restrictions in England, Scotland, Canada, and Australia. No restrictions were found in France and Germany. C displays financial and outcome-based managed entry agreements for England, Scotland, Canada, and Australia. Indication launch sequence was determined according to HTA approval date. p values calculated based on χ2-tests: *p < 0.05, **p < 0.01, ***p < 0.001. HTA health technology assessment

Discussion

This study analysed the clinical value, disease prevalence, and pricing of multi-indication cancer drugs alongside reimbursement and coverage decisions. We find that drugs provided varying value to patients and payers across indications. Although countries employ indirect ISP, such as weighted-average prices, differential discounts, or MEAs, indication development is prioritised according to clinical value and disease prevalence. Besides drug pricing policies, several factors throughout the indication discovery, development, and approval process incentivise this observed launch sequence. From a pharmaceutical policy perspective, a pure ISP mechanism - one price per indication - could help to better align the incentives, clinical value, and price of multi-indication drugs.

Current Pricing Policies for Multi-indication Drugs

In theory, weighted-average drug prices and differential discounts should adequately capture each indication’s differential value [10]. Weighted-average prices are calculated according to each indication’s value and/or (forecasted or actual) sales volume [10, 11]. Differential discounts on a drug’s list price are negotiated for each newly launched indication [10, 11]. In theory, both mechanisms should reduce the incentive to sequence indication launches [10].

In practice, we observed that indications are sequenced according to clinical value and disease prevalence across all countries, no matter if weighted-average pricing or differential discounts are present. Incremental QALYs and LYs gained were significantly lower for subsequently launched indications, whilst disease prevalence increased with each new indication. Therefore, Fig. 1B, which maps incremental QALYs and disease prevalence by indication sequence, closely resembles theoretical concepts, as portrayed in Fig. 1A, proposed by several authors [6, 7, 12]. Even under weighted-average pricing and differential discounts, there remains an incentive to first launch drugs in high-value indications with a small patient population. First, no upward revisions took place in countries that employ weighted-average pricing. Therefore, manufacturers are motivated to increase revenues and profits by anchoring drug prices to the indication with the highest value. Accordingly, differential discounts can be applied when low-value indications are launched, whilst a differential premium for high-value indications is yet to be witnessed. Second, drug prices are subject to external reference pricing (ERP) systems around the globe, thereby motivating manufacturers to first launch the highest value indication, which can set the maximum possible price in the USA, Germany, and the UK [24, 25]. These countries, alongside others implementing minimal price controls, are then used as a reference to price drugs elsewhere. In Sect. 4.2, we discuss additional factors beyond drug pricing, which could influence the observed launch sequence.

In line with theory, Germany and France - countries with weighted-average pricing - accounted for the lower clinical benefit and higher patient population by significantly reducing drugs’ list prices with each new indication. In contrast, prices remained constant in countries employing differential discounts, e.g. England, Canada, Australia, and Scotland. Although discounts could not be observed as they are not disclosed, the use of clinical restrictions and MEAs increased with each new indication in England, Canada, Australia, and Scotland. Clinical restrictions limit prescription to subpopulations of subsequently launched indications. Within an indication, HTA agencies aim to identify patients who stand to benefit most, e.g. patients with metastatic cancer, to increase incremental QALYs gained and thereby improve ICERs [26]. Similarly, financial and outcome-based MEAs are employed to reduce uncertainty while ensuring access to medicines [27, 28]. In conclusion, HTA organisations more frequently used restrictions or MEAs to ensure that multi-indication drugs' value is aligned to the prices paid for the medicines, when list prices do not account for varying indication value. To date none of these differential pricing policies are implemented in the USA, although several insurers initiated ISP schemes for single drugs of unknown magnitude and benefit [11].

Coherent with previous cost-effectiveness studies [3, 16, 18, 19], ICERs increased with new indications in some countries, e.g. USA and Canada. This is a result of decreasing efficacy and increasing (or flat) prices of subsequent indications. In contrast, no significant trend could be observed in countries such as England, Scotland, and France. In these countries, an indication-specific HTA process, which then informs the negotiation of weighted-average prices or differential discounts, could help to control the price of and expenditure on multi-indication drugs.

However, results demonstrate that certain low-value indications are not launched, even in countries employing weighted-average pricing of differential discounts. Especially countries with smaller populations and therefore small potential markets experienced fewer launches, e.g. Scotland, Australia, Canada. Additionally, launched indications provided a higher clinical benefit in terms of QALYs and LYs, but did not exhibit any differences in disease prevalence. All this suggests that there is little economic incentive for manufacturers to launch indications in regions with smaller patient populations. Even under a weighted-pricing mechanism, the launch of low-value indications would have an adverse effect on list prices (and potentially profits). These findings matched previous conceptual frameworks [6, 13, 29].

The downside of weighted-average pricing and differential discounts is that both require the ex-ante estimation or ex-post tracking of use per indication. The consideration of competition and its impact on other drugs’ sales volume and market share further complicates weighted-average pricing. Similarly, there is a substantial administrative cost associated with designing, negotiating, and monitoring MEAs.

Indication Discovery, Development, Approval, and Pricing

The indication launch sequence observed in our study is not solely a reflection of pricing and reimbursement policies. The discovery, development, regulatory approval, and launch of new indications is a lengthy process with multiple facets and decision points. First, scientists aim to research and develop drugs for diseases with unmet medical needs, e.g. severe diseases with few therapeutic alternatives and a low prevalence [30]. There is a more pressing need and consequently a larger potential for patients’ health benefits in such indications. Furthermore, scientists leverage new technologies, including next-generation sequencing, high throughput screening, or machine learning, to quickly test hypotheses and identify optimal patient populations (and indications) for a drug [31, 32]. Discovering platform technologies, such as targeted therapies or immuno-therapies, which can be used across multiple diseases, are especially desired and valued by investors [1, 4, 5].

The clinical development of targeted and personalised therapies has also been shaped by recent innovations in clinical trial design. “Master protocols” have been introduced to provide a more efficient and ethical way of conducting trials [33]. Basket, umbrella, and platform trials, which study multiple diseases, treatments, or a combination of both, have increased in popularity, especially for Phase 1 or 2 trials [34]. These new trial designs offer manufacturers an earlier opportunity to identify and select patient populations that benefit most from investigational new drugs [33, 34]. Combined with new biomarker technologies such as liquid biopsies [35], innovative trial designs permit personalised treatment strategies, resulting in narrower drug indications, ultimately leading to an increase in the total number of indications.

The US Congress has kept pace with these developments in drug discovery and development by introducing special FDA review processes, such as the breakthrough therapy designation [36]. These special approval pathways permit the FDA to allocate resources to indications with unmet medical needs. Michaeli et al. found that apart from uniform drug prices, special regulatory review pathways from the FDA, EMA, HC, and TGA incentivise manufacturers to prioritise monotherapy indications in rare diseases with high unmet needs [37]. Arguably the indication development and approval process in the USA could have the largest effect on the observed launch sequence given that it is the single largest market for prescription drugs.

In conclusion, recent technological advances enabled, whilst regulatory processes further incentivised the prioritisation of indications for patients with unmet medical needs.

Innovation and Patent Protection of Multi-indication Drugs

The observation that multiple indications with diverging innovativeness are approved at different dates is highly relevant from a legal perspective. Manufacturers usually apply for patents to protect their novel therapeutic invention with an innovative mechanism-of-action, manufacturing process, drug target, or method-of-use from competition for a time period of up to 25 years. Whilst this process provides manufacturers with several years of sales exclusivity, drugs with multiple indications only capture the full period of exclusivity for the first yet not the later approved indications. To ensure that generic competitors may enter the market for first launched indications according to the Hatch-Waxman Act (Pub.L. No. 98-417), generics may carve-out indications without patent protection with “skinny labels”, whereby follow-on drug manufacturers seek approval for some but not all of the indications for which the branded originator drugs has been approved [38, 39]. Whilst Walsh et al. correctly recognise that several barriers prevent skinny labels to enter the market [38, 39], the innovativeness of on-patent indications must be fully protected. Recent examples of Amarin’s icosapent ethyl (Vascepa®) or GlaxoSmithKline’s carvedilol (Coreg®) showed that skinny labels often exceed the generic’s approved indication by willingly or unwillingly encouraging prescription for on-patent indications [40, 41]. In this context, indication-specific tracking of drug use does not only provide the foundation for a more sophisticated pricing mechanism, but also helps to enforce indication-specific method-of-use patents.

The Way Forward

Further research is necessary to investigate the effects of current pricing mechanism on multi-indication non-cancer drugs. A similar analysis of countries employing a different mix of drug pricing policies, such as Italy and Spain, is of interest. It is furthermore warranted to compare the clinical benefit (e.g. overall survival or progression-free survival) and quality of clinical evidence (e.g. phase of clinical trial, number of enrolled patients) across indications. One of the key advantages of indication extensions relates to shorter development cost and time; however, the extent to which this translates to faster patient access to new therapeutic options should be explored in future studies. Further including indications through clinical trial registries that never received regulatory approval creates a more holistic perspective on the development process of multi-indication drugs. A more in-depth analysis on the effectiveness of weighted-average prices, MEAs, and differential discounts to control pharmaceutical expenditure is necessary. Reimbursement policies and net list prices are subject to further scrutiny. The effect of pricing policies on the demand side, e.g. usage and prescription, is of special interest for dispensers, prescribers, and patients.

Limitations

Our analysis has some limitations. First, the study only permits conclusions for multi-indication cancer drugs, due to the sample selection. Second, the presence of combination therapies (18% of indications) may bias results, e.g., partially cause the increased ICERs for subsequentially launched indications. Third, reforms and updates of HTA processes throughout the study period limit conclusions. In Germany, no HTA reports were available before the introduction of the current HTA system (AMNOG) in 2011 [42]. In England, reforms of NICE approval timelines along with the Cancer Drug Fund (CDF), require all HTA submissions to be processed within 90 days of EMA approval [43]. Introduction of the CDF may impact launch decisions, HTA outcomes, list prices, and economic and clinical restrictions. Data on QALYs, LYs, ICERs, and list prices were only available for a subset of the sample. Observable list prices are subject to further negotiations resulting in discounted, unobservable net prices. Cross-sectional prevalence data were extracted for 2017 and only matched to indications on a disease level, which does not account for age-specific prevalence rates, cancer subtypes, and different lines of therapies. The definition of indication launches may be debated as indications may already be marketed in certain countries, e.g. Germany, prior to the formal HTA decision. The impact of negative HTA outcomes furthermore varies across jurisdictions. Whilst drugs with negative outcomes are not reimbursed in the UK, they may be reimbursed in Germany (for a lower price). This study does not permit an isolated evaluation of pricing mechanisms for multi-indication drugs. All implemented policies are subject to further regional specificities, such as regulatory process, HTA assessments, and social, economic, and demographic settings [44].

Conclusion

Cancer drugs are increasingly approved for multiple indications of varying clinical benefit. Aligning a single price to this differing value remains a challenge. We examined the clinical value, price, reimbursement, and coverage decisions of multi-indication drugs across seven countries. In our sample of 25 cancer drugs with 100 indications, drugs were first launched for rare diseases that offer significant QALY gains and were subsequently extended to indications that deliver lower QALY gains to eligible patient populations. This launch sequence could be influenced by multiple factors throughout the discovery, development, approval, and pricing process. Scientists aim to address decision-makers’ revealed preference and discover drugs for diseases with unmet medical needs, the FDA and other regulatory agencies provide incentives for orphan indications, whilst manufacturers seek to set the highest possible price (attained in indications with high QALYs gained) and thereby maximise revenue and profit streams. Countries employ “indirect” ISP to account for each indication’s differential benefit, notably weighted-average prices (Germany, France, Australia), differential discounts (England, Scotland), clinical restrictions, and MEAs (England, Scotland, Australia, Canada). In this context, a “pure” value-based indication-specific pricing policy, which assigns one price to each indication, should be explored to better align the incentives, clinical benefit, and cost for multi-indication cancer drugs. ISP could help to contain payers’ costs and increase patient benefit. However, monitoring at an indication level, complex distribution systems, high administrative costs, opposition by key stakeholders, legal barriers, and privacy concerns challenge the feasibility of ISP. Nonetheless, an indication-specific tracking of drug use does not only provide the foundation for a more sophisticated pricing mechanism, but could also help to enforce indication-specific method-of-use patents.

Supplementary Information

Below is the link to the electronic supplementary material.

Acknowledgements

We are grateful to comments and suggestions received by the editor of the journal and the anonymous referees. We are also grateful to Aurelio Miracolo for his excellent research assistance.

Funding

Open Access funding enabled and organized by Projekt DEAL.

Declarations

Funding

Novartis Pharmaceuticals Corporation, an affiliate of Novartis AG, provided access to the IQVIA sales database.

Disclosure statement

Not applicable.

Data availability

All data generated or analysed during this study are included in this published article and its supplementary files.

Ethical standards

Not applicable.

Conflict of interest

The authors declare no conflict of interest.

Author contributions

DM: conceptualization, data collection, statistical analysis, visualization, writing, editing. MM: conceptualization, supervision, data collection, statistical validation, editing, review. PK: conceptualization, supervision, review.

Consent to participate

Not applicable.

Consent for publication (from patients/participants)

Not applicable.

Code availability

Not applicable.

Contributor Information

Daniel Tobias Michaeli, Email: danielmichaeli@yahoo.com.

Panos Kanavos, Email: p.g.kanavos@lse.ac.uk.

References

- 1.Finn OJ. Cancer immunology. N Engl J Med. 2008;358:2704–2715. doi: 10.1056/NEJMra072739. [DOI] [PubMed] [Google Scholar]

- 2.IQVIA. Global Oncology Trends 2018: Innovation, Expansion and Disruption; 2018.

- 3.Hui L, von Keudell G, Wang R, Zeidan AM, Gore SD, Ma X, Davidoff AJ, Huntington SF. Cost-effectiveness analysis of consolidation with brentuximab vedotin for high-risk Hodgkin lymphoma after autologous stem cell transplantation. Cancer. 2017;123:3763–3771. doi: 10.1002/cncr.30818. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 4.Michaeli DT, Yagmur HB, Achmadeev T, Michaeli T. Valuation and returns of drug development companies: lessons for bioentrepreneurs and investors. Ther Innov Regul Sci. 2022;56:313–322. doi: 10.1007/s43441-021-00364-y. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 5.Michaeli DT, Yagmur HB, Achmadeev T, Michaeli T. Value drivers of development stage biopharma companies. Eur J Health Econ. 2022 doi: 10.1007/s10198-021-01427-5. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 6.Cole A, Towse A, Lorgelly P, Sullivan R. Economics of innovative payment models compared with single pricing of pharmaceuticals. London: Office of Health Economics; 2018. [Google Scholar]

- 7.Mestre-Ferrandiz J, Towse A, Dellamano R, Pistollato M. Multi-indication pricing: pros, cons and applicability to the UK. London: Office of Health Economics; 2015.

- 8.Bach PB. Indication-specific pricing for cancer drugs. JAMA. 2014;312:1629–1630. doi: 10.1001/jama.2014.13235. [DOI] [PubMed] [Google Scholar]

- 9.Pearson SD, Dreitlein WB, Henshall C, Towse A. Indication-specific pricing of pharmaceuticals in the US healthcare system. J Comp Eff Res. 2017;6:397–404. doi: 10.2217/cer-2017-0018. [DOI] [PubMed] [Google Scholar]

- 10.Campillo-Artero C, Puig-Junoy J, Segú-Tolsa JL, Trapero-Bertran M. Price models for multi-indication drugs: a systematic review. Appl Health Econ Health Policy. 2020;18:47–56. doi: 10.1007/s40258-019-00517-z. [DOI] [PubMed] [Google Scholar]

- 11.Preckler V, Espín J. The role of indication-based pricing in future pricing and reimbursement policies: a systematic review. Value Health. 2022;25:666–675. doi: 10.1016/j.jval.2021.11.1376. [DOI] [PubMed] [Google Scholar]

- 12.Chandra A, Garthwaite C. The economics of indication-based drug pricing. N Engl J Med. 2017;377:103–106. doi: 10.1056/NEJMp1705035. [DOI] [PubMed] [Google Scholar]

- 13.Mestre-Ferrandiz J, Zozaya N, Alcalá B, Hidalgo-Vega Á. Multi-indication pricing: nice in theory but can it work in practice? Pharmacoeconomics. 2018;36:1407–1420. doi: 10.1007/s40273-018-0716-4. [DOI] [PubMed] [Google Scholar]

- 14.Flume M, Bardou M, Capri S, Sola-Morales O, Cunningham D, Levin L-A, Touchot N, Payers’ Insight. Feasibility and attractiveness of indication value-based pricing in key EU countries. J Mark Access Health Policy. 2016;4. 10.3402/jmahp.v4.30970. [DOI] [PMC free article] [PubMed]

- 15.Towse A, Cole A, Zamora B. The debate on indication-based pricing in the U.S. and five major European countries. London: Office of Health Economics; 2018. [Google Scholar]

- 16.Yeung K, Li M, Carlson JJ. Using performance-based risk-sharing arrangements to address uncertainty in indication-based pricing. J Manag Care Spec Pharm. 2017;23:1010–1015. doi: 10.18553/jmcp.2017.23.10.1010. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 17.Cole A, Neri M, Cookson G. Expert consensus programme: payment models for multiindication therapies. London: Office of Health Economics; 2021. [Google Scholar]

- 18.Persson U, Norlin JM. Multi-indication and combination pricing and reimbursement of pharmaceuticals: opportunities for improved health care through faster uptake of new innovations. Appl Health Econ Health Policy. 2018;16:157–165. doi: 10.1007/s40258-018-0377-7. [DOI] [PubMed] [Google Scholar]

- 19.Garrison LP, Veenstra DL. The economic value of innovative treatments over the product life cycle: the case of targeted trastuzumab therapy for breast cancer. Value Health. 2009;12:1118–1123. doi: 10.1111/j.1524-4733.2009.00572.x. [DOI] [PubMed] [Google Scholar]

- 20.Meher BR, Padhy BM. Indication-specific pricing of drugs: a utopian idea, a pragmatic proposition or unrealistic in economically constrained settings? Trop Doct. 2020;50:157–159. doi: 10.1177/0049475520903644. [DOI] [PubMed] [Google Scholar]

- 21.Neri M, Towse A, Garau M. Multi-indication pricing (MIP): practical solutions and steps to move forward. London: Office of Health Economics; 2018. [Google Scholar]

- 22.Mills M, Miracolo A, Michaeli D, Kanavos P. PNS73 payer perspectives on pricing of MULTI-indication products. Value Health. 2020;23:S655. doi: 10.1016/j.jval.2020.08.1517. [DOI] [Google Scholar]

- 23.Abate KH, Abay SM, Abbafati C, et al. Global, regional, and national incidence, prevalence, and years lived with disability for 354 diseases and injuries for 195 countries and territories, 1990–2017: a systematic analysis for the Global Burden of Disease Study 2017. Lancet. 2018;392:1789–1858. doi: 10.1016/S0140-6736(18)32279-7. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 24.Kanavos P, Fontrier A-M, Gill J, Efthymiadou O, Boekstein N. The impact of external reference pricing within and across countries. London: London School of Economics and Political Sciences; 2017. [Google Scholar]

- 25.Kanavos P, Fontrier A-M, Gill J, Efthymiadou O. Does external reference pricing deliver what it promises? Evidence on its impact at national level. Eur J Health Econ HEPAC Health Econ Prev Care. 2020;21:129–151. doi: 10.1007/s10198-019-01116-4. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 26.Kanavos P, Visintin E, Gentilini A. Algorithms and heuristics of health technology assessments: a post hoc analysis of the factors associated with HTA outcomes for new drugs across eight OECD countries. 2022. [DOI] [PubMed]

- 27.Ferrario A, Kanavos P. Dealing with uncertainty and high prices of new medicines: a comparative analysis of the use of managed entry agreements in Belgium, England, the Netherlands and Sweden. Soc Sci Med. 2015;124:39–47. doi: 10.1016/j.socscimed.2014.11.003. [DOI] [PubMed] [Google Scholar]

- 28.Kanavos P, Ferrario A. Managed entry agreements for pharmaceuticals: the European experience. Brussels: EMiNet; 2013. [Google Scholar]

- 29.Kanavos P, Vandoros S, Irwin R, Nicod E, Casson M. Differences in costs of and access to pharmaceutical products in the EU. Brussels: European Parliament; 2011. [Google Scholar]

- 30.Vreman RA, Heikkinen I, Schuurman A, Sapede C, Garcia JL, Hedberg N, Athanasiou D, Grueger J, Leufkens HGM, Goettsch WG. Unmet medical need: an introduction to definitions and stakeholder perceptions. Value Health. 2019;22:1275–1282. doi: 10.1016/j.jval.2019.07.007. [DOI] [PubMed] [Google Scholar]

- 31.Adams DR, Eng CM. Next-generation sequencing to diagnose suspected genetic disorders. N Engl J Med. 2018;379:1353–1362. doi: 10.1056/NEJMra1711801. [DOI] [PubMed] [Google Scholar]

- 32.Vamathevan J, Clark D, Czodrowski P, et al. Applications of machine learning in drug discovery and development. Nat Rev Drug Discov. 2019;18:463–477. doi: 10.1038/s41573-019-0024-5. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 33.Woodcock J, LaVange LM. Master protocols to study multiple therapies, multiple diseases, or both. N Engl J Med. 2017;377:62–70. doi: 10.1056/NEJMra1510062. [DOI] [PubMed] [Google Scholar]

- 34.Park JJH, Siden E, Zoratti MJ, Dron L, Harari O, Singer J, Lester RT, Thorlund K, Mills EJ. Systematic review of basket trials, umbrella trials, and platform trials: a landscape analysis of master protocols. Trials. 2019;20:572. doi: 10.1186/s13063-019-3664-1. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 35.Ignatiadis M, Sledge GW, Jeffrey SS. Liquid biopsy enters the clinic—implementation issues and future challenges. Nat Rev Clin Oncol. 2021;18:297–312. doi: 10.1038/s41571-020-00457-x. [DOI] [PubMed] [Google Scholar]

- 36.Darrow JJ, Avorn J, Kesselheim AS. The FDA breakthrough-drug designation—four years of experience. N Engl J Med. 2018;378:1444–1453. doi: 10.1056/NEJMhpr1713338. [DOI] [PubMed] [Google Scholar]

- 37.Michaeli DT, Mills M, Michaeli T, Miracolo A, Kanavos P. Initial and supplementary indication approval of new targeted cancer drugs by the FDA, EMA, Health Canada, and TGA. Investig New Drugs. 2022 doi: 10.1007/s10637-022-01227-5. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 38.Walsh BS, Sarpatwari A, Rome BN, Kesselheim AS. Frequency of first generic drug approvals with “skinny labels” in the United States. JAMA Intern Med. 2021;181:995–997. doi: 10.1001/jamainternmed.2021.0484. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 39.Walsh BS, Bloomfield D, Kesselheim AS. A court decision on “skinny labeling”: another challenge for less expensive drugs. JAMA. 2021;326:1371–1372. doi: 10.1001/jama.2021.0006. [DOI] [PubMed] [Google Scholar]

- 40.US Dist Lexis 144792. Amarin Pharma, Inc v Hikma Pharmaceuticals USA Inc; 2021.

- 41.US App Lexis 23173. GlaxoSmithKline LLC v Teva Pharmaceuticals USA, Inc; 2021.

- 42.Ruof J, Schwartz FW, Schulenburg J-M, Dintsios C-M. Early benefit assessment (EBA) in Germany: analysing decisions 18 months after introducing the new AMNOG legislation. Eur J Health Econ. 2014;15:577–589. doi: 10.1007/s10198-013-0495-y. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 43.Macaulay R, Dave K, Walsh SC. The impact of cancer drugs fund reforms on reimbursement of oncology drugs in the UK. Value Health. 2017;20:A461. doi: 10.1016/j.jval.2017.08.354. [DOI] [Google Scholar]

- 44.Angelis A, Lange A, Kanavos P. Using health technology assessment to assess the value of new medicines: results of a systematic review and expert consultation across eight European countries. Eur J Health Econ. 2018;19:123–152. doi: 10.1007/s10198-017-0871-0. [DOI] [PMC free article] [PubMed] [Google Scholar]

Associated Data

This section collects any data citations, data availability statements, or supplementary materials included in this article.

Supplementary Materials

Data Availability Statement

All data generated or analysed during this study are included in this published article and its supplementary files.