Abstract

Solar PV has seen a spectacular market development in recent years and has become a cost competitive source of electricity in many parts of the world. Yet, prospective observations show that the coronavirus pandemic could impact renewable energy projects, especially in the distributed market. Tracking and attributing the economic footprint of COVID-19 lockdowns in the photovoltaic sector poses a significant research challenge. Based on millions of financial transaction records and 44 thousand photovoltaic installation records, we tracked the spatio-temporal sale network of the distributed photovoltaic market and explored the extent of market slowdown. We found that a two-month lockdown duration can be assessed as a high-risk threshold value. When the lockdown duration exceeds the threshold value, the monthly value-added loss reaches 67.7%, and emission reduction capacity is cut by 64.2% over the whole year. We show that risks of a slowdown in PV deployment due to COVID-19 lockdowns can be mitigated by comprehensive incentive strategies for the distributed PV market amid market uncertainties.

Keywords: COVID-19, Distributed PV market, Transaction, Economy slowdown

Abbreviations: PV, photovoltaic; COVID-19, corona virus disease found in 2019; METI, Ministry of Economy, Transaction and Industry; GHI, Daily global horizon; LER, Loss in potential emission reduction capacity; PFRC, Proportion of PV companies under Risk of Collapse; PRSW, Risk of Suspension of Work; LRER, Loss rate in potential emission reduction capacity

1. Introduction

A great deal of direct and indirect evidence has revealed the fact that the global coronavirus pandemic has cut emissions in recent months, as world-wide cities went on lockdown and the crisis squeezed national and international economic transactions [1], [2], [3]. By this token, could we assume that this pandemic crisis—which has caused hundreds of thousands of deaths [4]—will help to mitigate climate change? Unfortunately, many environmental scientists and economists have already given a negative prediction on this question [5]. Manzanedo et al. [6] explained that with pandemic of COVID-19 all over the world, the climate management will be more and more difficult, where in [7], Oldekop et al. expressed a similar idea. One key contributing factor is, with economic downturn [8], customers would tend to slow down capital intensive renewable energy projects [9], especially in the distributed photovoltaic (PV) market, despite of their long-term benefits [10], [11], [12], [13]. Solar PV has long been thought as an effective and promising technology as a substitutive for electricity generation of traditional fossil fuel [14], [15]. The popularity of solar PV is essential for the mitigation of climate change [16]. However, existing conventional electricity generation assets might receive higher priority as they put less short-term stress on the economy [17], [18], [19], [20]. Since one-fifth of all renewable capacity deployed globally consists of individuals and small-to-medium-sized enterprises installing solar PV panels on their roofs or business sites [10], [21], this market slowdown in the distributed PV sector would bring considerable negative impacts on clean energy transformation progress [22] and even overall employment [23]. The unemployment brought by COVID-19 is an important factor of consumption behaviors of solar PV as many families turned to increase the proportion of purchase on daily products rather than other things [24].

In light of these problems, it is necessary to dissect the economic footprint of the COVID-19 pandemic in the distributed PV market, so as to help governments devise suitable economic rescue packages for renewable energy industries and emission reduction strategies. Earlier studies on economic analysis of the PV sector mainly focused on an in-depth interpretation of costs and benefits based on limited data [25], [26], [27], [28]. There are rare evidence and studies that discover the impact of the COVID-19 pandemic on solar PV market and its chain effect in the energy sector. It is important to further reveal research gaps in our understanding of the business networks of the PV sector, in order to further analyze the propagation of economic impacts on the distributed PV sector in this extreme situation. Deep insights into these impacts is the key to strengthening the resilience of future energy supply systems [29], [30], [31] and improving future utility solar power policy [32], [33], [34], [35], [36], [37].

Here, we explore the patterns of market slowdown in the distributed PV sector brought by COVID-19 lockdowns. We focus mainly on three key questions: (1) What is the economic footprint of COVID-19 lockdowns on new investments in distributed PV; (2) What is the loss in emission reduction capacity caused by investment slowdown in distributed PV products; (3) How can investments in the distributed PV be incentivized to achieve environmental targets. Based on data fusion of 1.66 million financial transaction records and 44,374 distributed PV installation records in 2018, we elaborately simulated how a lockdown would cause a market slowdown in Japan's distributed PV sector. Finally, we offer an assessment of a comprehensive incentive strategy to support the resilience of the distributed PV market, which might help guide governments in designing robust recovery policies.

2. Related works

PV power has long been acknowledged as a promising renewable energy technology. A lot of scholars contributed to study the PV market from different aspects. They respectively did the analysis from costs and benefits, the supply-chain, and policy impacts.

Some studies focused on costs and benefits of PV market development. Zahedi [38] pointed out that the major factors impeding the PV market development include high initial costs, lack of skilled manpower, lack of good quality data and social acceptance. The main factors favoring PV market development in remote areas including the high costs of conventional energy sources; the loss of a scale-economy effect, price of fuel, fuel transportation and spare part supplies. Using solar PV production information in conjunction with wholesale price data, Borenstein [39] estimated the market value and cost of power from solar PV. Gan and Li [40] analyze the relationship between the declines in PV module costs and cumulative production, silicon prices, supply–demand imbalance and the presence of lower-cost Chinese products in the global PV market. Botelho, Lourenço-Gomes [41] surveyed residents’ preferences toward the cost and benefit of PV.

As for the supply-chain, the related studies mainly focus on the macro aspect of the whole supply-chain of PV market. Marsillac [42] built a framework of the PV market supply chain and compared the critical components of the PV supply chain. Davies and Joglekar [43] quantify the value of modularity and integration of PV supply chain. Guo, Lin [44] tracing carbon emissions from the photovoltaic supply chain with life cycle method. Chen and Su [45] studied the business dynamics of the multiple PV supply chain and gave quantitative analytical results that provide appropriate business strategic directions for the enterprises. Utilizing a two-phase approach based on DEA and the robust optimization models, Dehghani, Jabalameli [46] designed and planed a solar photovoltaic supply chain in an uncertain environment. Based on multiple cases, Besiou and Van Wassenhove [47] analyzed the closed-loop PV supply chains involving key stakeholders in the design, production, collection, and recovery of PV panels. Wang, Yuan [48] conducted 249 observations of 75 solar PV companies in the whole supply-chain from 2005 to 2012 to investigate how the supply side would be influenced by government aid such as bank loans and direct subsidies.

The impacts of policies on the PV market also gained considerable attention by researchers. By summarizing local activities related to solar in 151 localities, Doris, Booth [49] discussed how the policies within jurisdiction as well as local policies interact to contribute to national PV market developments. Moosavian, Rahim [50] compared the energy policies of 7 countries. Flexible retail financing terms, renewable portfolio standards, incentives, subsidies, and tax exemptions are contributed to increase of PV market. Grau, Huo [51] did a survey for the photovoltaic industry and policy in Germany and China and discussed the synergies. Policy on PV market and the mechanisms in German, Japan and China are discussed by Yu, Popiolek [52]. Haley and Schuler [53] discuss how the uncertainty of government policy on solar PV shape firms’ market and nonmarket strategies. Zhi, Sun [54] examined the evolution of China’s PV policies. They found that China’s PV policies are gradually changing from production supply prioritization to demand-side policy domination. Using a hybrid energy agent-based model, Al Irsyad, Halog [55] simulated the impacts of financing support policies towards PV market in Indonesia. Ahmad, Tahar [56] utilized a system dynamics model to investigate the impact of feed-in tariff policy in promoting solar photovoltaic investments in Malaysia.

Existing researches mainly based the statistical data from the official section, reviews from the government documents or survey data of a limited scale. The results of the existing researches are general. As far as we know, few studies tracked economic performance and energy effect of PV market by utilizing big data which provided a more comprehensive understanding toward the whole market. Besides, there are rare evidence and studies that discover the impact of the COVID-19 pandemic on the solar PV market and its chain effect in the energy sector. Filling the gaps of existing literature, the contributions of this work are shown as followings:

-

(1)

We explore the patterns of market slowdown in the distributed PV sector brought by COVID-19 lockdowns;

-

(2)

We utilized massive of big data including 1.66 million financial transaction records and 44,374 distributed PV installation records in 2018 to track the spatio-temporal sale network of the distributed photovoltaic market;

-

(3)

Different from the previous general results, we apply data fusion method to give more detailed results;

-

(4)

We assess the comprehensive incentive strategy to support the resilience of the distributed PV market.

3. Mechanism of modeling COVID-19 market slowdown

Confronted with this severe pandemic, national governments have been compelled to respond with drastic measures including “lockdowns” so as to mitigate the coronavirus spread. However, due to the uncertainties of the pandemic situation, governments might be forced to extend the duration of lockdowns. Therefore, over a relatively long period of time, a part of markets, especially high-risk service industries, would be mandatorily shut down. Then, due to demand contraction in these service industries, upstream industries (e.g. manufacturing) would be subsequently affected. Due to the propagation of impacts, these mandatory closures and declines in demand would directly lead to a reduction of the whole industry, which would force more industries to stop certain components of services or production. Consequently, residents gradually face the risk of suspension from work and decreased income. This in turn would cause a decline in spending power, and negative feedback to consumption. For the distributed PV sector, the effects of COVID-19 lockdown manifest themselves in two aspects: 1. The implementation of lockdown policy mandatorily stops parts of services of distributed PV intermediators, e.g. installation, rental. This impact would slow down parts of distributed PV markets directly. 2. Due to declining industry profits and income levels in the residential sector, end-consumers of distributed PV may choose to postpone or even terminate their installation plans. Additionally, the market slowdown in the distributed PV sector undoubtedly causes a loss in emission reduction capacity potentially jeopardizing the attainment of internationally agreed climate mitigation targets. In light of this complexity, the government needs to devise a comprehensive recovery strategy for the distributed PV sector. However, facing the huge uncertainties in market response, it is difficult to make appropriate policy decisions.

In this study, we tracked the propagation of the economic impact of the COVID-19 crisis on the distributed PV market, and further estimated the market slowdown in the distributed PV sector and loss in emission reduction capacity. the mechanism of the COVID-19 market slowdown modeling is shown in Fig. 1 . The framework’s input included 1.66 million financial transaction records, 302,845 firms’ information (location, industry, capital, number of employees, etc.), 44,374 newly distributed PV installation records (location and capacity), and authoritative information on lockdown measures and residential consumption attitudes, covering the entire country of Japan. The entire simulation process was conducted in three hypothetical scenarios assuming one-, two- and three-month-long lockdowns. These simulations will help guide policies addressing the direct adverse effects of the crisis. Additionally, we also investigated policy strategies during the recovery period characterized by exacerbated market uncertainties. We propose a novel analytical framework to study policy impacts under COVID-19 market conditions (see Experimental procedures). Based on the transaction data, we tracked the business networks of all industries. According to the official lockdown measure information, we could simulate the shutdown of specific services under COVID-19 policy and trace the propagation of the economic impacts of all relevant industries. Based on the company level information dataset, we tracked the employment situation and evaluated the changes in the regional income level. Then, by combing survey data on residential consumption attitudes, we can estimate the demand reduction in the distributed PV market, and the corresponding market slowdown of the distributed PV sector. We computed the loss in potential emission reduction volume caused by the distributed PV market slowdown based on the potential power production and the local emission factor of electricity generation. In the end, we helped the government to devise recovery incentive strategies for the distributed PV sector.

Fig. 1.

Mechanism of the COVID-19 market slowdown modeling. The arrows represent the propagation and causal chains of the economic impact. The colors of the arrows vary according to different data sources and methods. The orange panes illustrate the data sources and how the data were utilized in this research. The grey panes show the specific impacts on each component of the distributed PV market under the COVID-19 lockdown policy. The green panes represent the scenarios we set to give a comprehensive analysis of different situations. In this model, the input datasets are official lockdown measure information, financial transaction data, company information data, survey data of residential consumption attitude, regional weather data, and PV installation data. (For interpretation of the references to color in this figure legend, the reader is referred to the web version of this article.)

4. Methods

4.1. Data description

We took the data in 2018 as the baseline of our study. The official lockdown measure information was found from the official statements issued by Japan Broadcasting Corporation. The record data of distributed PV installation was found from the announcements by The Ministry of Economy, Transaction and Industry (METI), Japan, which include the purchaser location (firm location), installation location and PV capacity; Additionally, over 1.66 million transaction records covering various attributes of companies(capital, number of employees, address, etc.) as well as transaction information between the companies (transaction item, estimated transaction amounts, etc.) from across Japan were used in this study. The data is held by the private Corporate Credit Research Teikoku Databank Ltd.. The transaction values were estimated in a joint study between Teikoku Databank Ltd. and Takayasu Laboratory of the Tokyo Institute of Technology.[57] Each transaction record includes the information of both sides of the transaction, transaction item category, transaction time and transaction amount. According to the transaction items, there are 8760 distributed PV product transactions. The company information dataset includes 302,845 firms and all of them could be matched with the transaction record data. For each company, the dataset also includes their location, industry category, capital, number of employees, etc. These firms are classified into 89 industries. As for the distributed PV sector, there are 1814 firms in total. The average wage information of each industry is open data from a career research company, Mynavi Corporation. The consumption structure information of different demographic groups is from the Survey of Family Statistics and Consumption by the Statistics Bureau of the Ministry of Public Affairs, Japan. The survey results are from about 30,000 households. The consumption attitudes on distributed PV products is open survey data from a research company, MyVoice. The survey results are from 10,852 respondents from different demographic groups. The emission factors of electricity generation are from the official report of each regional electricity company in Japan. Daily global horizon (GHI) values in kWh/m2 of 1741 administrative regions in Japan are extracted from solar radiation database Metronome (Version 7.1).

4.2. Framework of methodology

Fig. 2 shows the framework of our methodology. The blue boxes show the input data. The green boxes display the sub-methods. The details of each sub-method are explained in the Experimental procedures section. The orange boxes describe the result that could be obtained from the input data and methods. The black arrows show the data stream. The red arrows mean extracting data of the distributed PV sector from the result set of the whole industry. The blue arrows mean visualizing the data. The orange circles represent the assumptions in this framework and blue ones represent the scenarios set in this analysis.

Fig. 2.

Framework of methodology.

Firstly, based on the official policy information and firm information dataset, we set the initial operating state of each firm at the beginning of lockdown. Then based on the transaction data, we developed an agent-based input–output model for tracking the propagation of the economic impacts caused by the operating state changes and updated the operating state of each firm. With this result, we evaluated the state of suspension of work of each firm, based on the capital and employee information and then assess its impacts on the local resident income level. Based on the survey data of the consumption attitude of each region, we reconstructed the resident consumption structure under the decreases in local income level, and took the result into the agent-based input–output model to simulate the market negative feedback mechanism. According to the simulated lockdown duration, we did certain times of iteration. Then we extracted the result of distributed PV firms to analyze the impacts of lockdown policy on the PV sector from the aspects of sales, demand, firms, and employees (as shown in Fig. 3 ). Finally, based on the factors of electricity generation and daily radiation values of 1741 administrative regions in Japan, we estimated the loss in potential emission reduction capacity (as shown in Fig. 4 ), and made a comprehensive incentive strategy for the government to mitigate the loss (as shown in Fig. 5 ).

Fig. 3.

Tracking propagation of the economic impact of lockdown.

Fig. 4.

Sales network of the distributed PV market and spatial distribution of newly installed distributed PV in Japan in 2018. a. Sales network of the distributed PV sector: There are three layers in the sales network. The first layer represents the distributed PV manufacturers, the second layer shows the distributed PV intermediators (wholesalers, installers, retailers, and leasers), and the third layer shows the two types of end-consumers. C represents the customers of PV intermediators. D represents direct customers of PV manufacturers. b. Spatial distribution of newly installed distributed PV. The position of the point shows the location of the installation. The deep color refers to the installation of solar PV with high capacity, while shallow color refers to the installation of low-capacity solar PV. The size of the point indicates the number of installations, where bigger refers to more, and smaller refers to fewer. (For interpretation of the references to color in this figure legend, the reader is referred to the web version of this article.)

Fig. 5.

Market slowdown caused by COVID-19 lockdown in the distributed PV sector. On April 8, 2020, Japan declared a state of emergency in response to the coronavirus pandemic, which led to the near-total closures of schools, universities, and colleges, as well as mandatory shutdowns of high-risk service industries. Due to the uncertainties of the pandemic situation, the duration of the lockdown has been forced to extend. Based on this real case, we simulated how the lockdown policy would impact on the distributed PV market. a. The economic footprint of the lockdown policies on distributed PV manufacturers, with different implementation durations. Here, we focus on the detailed value-added losses contributed by different types of end-customers. b. Here, we focused on the demand losses from different end-customers. c. The Proportion of PV firms (including manufacturers and intermediators) under Risk of Collapse (PFRC) (see Experimental procedures). d. The Proportion of employees in the distributed PV sector under Risk of Suspension of Work (PRSW) (see Experimental procedures).

There are five key assumptions supporting the framework (their order is the same as the order number in the orange circle):

-

1.

Although we took mass and fine-grained datasets to support our result, the sample size still cannot reach to the real order of magnitude, which is scarcely possible to get, especially to the transaction data and detailed firm information data. Here, we assumed that our datasets are an unbiased sampling set from real-size data. Additionally, there is also much evidence can support this assumption. For example, the National Survey Report of PV Power Applications in Japan-2018 figured out that household PV took about 78.96% (estimated value) of the whole new installation capacity of decentralized PV[58]. While from our data, we assessed the value is 75.97%, which is very close to the official estimate.

-

2.

The Japanese government issued detailed lockdown measures to different industries. Here, we assumed that every firm will strictly follow the lockdown measure. Once the firms shut down following the policy, the employees of the firms will be suspended from work. Based on this assumption, we assessed the initial operating state of each firm at the beginning of lockdown. Although from the economic report, Japan's economy has suffered certain damages before the lockdown policy [59], since in this paper, we mainly focused on the impacts of COVID-19 lockdown on the distributed photovoltaic market, we did not take the previous damages into the iteration.

-

3.

For businesses that are allowed to operate normally during the lockdown, when a certain rate of sales reduction occurs, we assume that a corresponding ratio of employment in this firm would face the risk of suspension of work, and with the same ratio reduction in their salary (however, according to the labor law, the salary reduce rate cannot be higher than 40%). Based on the average wage and the employee proportion suspended from work of each industry and in each region, we evaluated the decrease degree in regional income level. Although the different firms may have different ways to cope with the sales reduction situation, in the context of the whole industry, we believe that our assumption can better describe the macro impacts of market slowdowns.

-

4.

Although the lockdown policy, to some extent, limits people from leaving homes and restricted on economic activities, many authoritative surveys also show that the sales volume of online shopping has been increasing during the lockdown period [24]. It is hard to say how much the physical limitation impacts consumption capacity, especially to the non-service industries. However, we are convinced that the income level is the key factor to shape the individual consumption structure. Here, we assume that to the businesses that are mandatorily closed, the resident consumption volume is 0. To the businesses that are allowed to operate normally during the lockdown, the shrinkage of resident consumption is related to income decrease.

-

5.

In this paper, we took 2018 as the baseline year. We assume that the potential capacity of newly distributed PV installation in 2020 will be the same as in 2018, so as for measuring the loss rate in potential emission reduction capacity in 2020.

In this paper, we also set several scenarios to describe the uncertainties of the future pandemic situation and market response (their order is the same as the order number in the blue circle):

-

1.

Due to the uncontrolled pandemic situation, many countries have extended their lockdown duration. From the macro statistics, the duration is usually within the range of one to three months. In light of this fact, we set three scenarios of one-, two-, and three-month lockdown, to comprehensively analyze the market slowdown situation.

-

2.

According to the prediction result from the Japan Research Institute report, the recovery duration may take a similar length with the lockdown. However, the government will effort to make a strong V-shaped economic recovery. Therefore, here, we set four scenarios which are immediate recover, recovery with one, two, and three months.

-

3.

To achieve the renewable growth target, the government needs to issue incentive policies for distributed PV market after lockdown. Considering the complex uncertainties of market response and the government's financial capacity, it is hard to set certain scenarios to predict future situations. Here, we develop a comprehensive incentive strategy for the distributed PV market considering the market response uncertainties. The government can dynamically adjust the incentive plan under the detailed guidelines of our results to achieve recovery targets.

4.3. Tracking propagation of the economic impact of lockdown

Here, we proposed an agent-based input–output model to track the propagation of the economic impact of lockdown, as shown in Fig. S2. We took each firm as an agent of this model (we also regard the resident customers of each firm as a “firm”). The input of the model includes the closure measures and initial consumption reduction of all industries. The model has a two-step iterative procedure as follows:

Transaction volume shrinkage. According to the model input, we computed the change of scale for each firm, and estimated the shrinkage in transactions between firms and customers, which is formulated as

| (1) |

where are the 0 to 1 values representing the scale of firm and (we use to represent the resident customers of each firm); is the amount of transactions between them before the iteration, and is the decreased transaction volume.

Firm scale shrinkage. In return, the scale of firm is recalculated according to the decreased revenue, which is formulated as

| (2) |

where is the shrunken scale of firm . When the firm-scale is lower than a certain threshold (a value with a mean of 0.2 and a variance of 0.05, this value being estimated based on macroeconomic statistics) in each simulation, it will be regarded as facing risk of bankruptcy, and all the transactions involved will no longer be included in the next iteration. After each iteration, the model will output the changes of firm scale and gross revenue and expenditure of each industry.

Tracking shrinkage of resident consumption Based on the results of the propagation of the economic impact of lockdown, we detected the scale shrinkage of each firm. With the scale shrinkage rate of each firm, we assumed the same ratio of employee will face risk of suspension of work, , and with the same ratio reduction in their salary (however, according to the labor law, the salary reduce rate cannot be higher than 40%). Based on the average wage of each industry,, we calculated the average salary of the employee of firm i, :

| (3) |

| (4) |

| (5) |

Then we could update the income level of each administrative region , . based on the survey results of consumption structure in different income-level groups, we reconstructed the consumption structure of each region and figured out the resident consumption reduction on each industry's product. Finally, we could estimate out the of the resident customers, and take this into the iteration process of tracking the propagation of the economic impact of lockdown. When the iteration time excesses the time threshold , we output the result.

| (6) |

| (7) |

For PV products, we looked at the survey data of consumption attitudes on distributed PV products from MyVoice. For other industries’ products, we took consumption structure information from the Statistics Bureau of the Ministry of Public Affairs.

4.4. Estimating loss in potential emission reduction capacity

We focused on the potential power production of the loss in distributed PV demand, and multiplied it with the local emission factor of electricity generation to measure the loss in potential emission reduction capacity (LER) caused by the distributed PV market slowdown, which is defined as

| (8) |

Accordingly, the loss rate in potential emission reduction capacity (LRER) is defined as

| (9) |

where is the accumulated output of the loss in distributed PV capacity before day in administrative region , kWh. is the emission factor of electricity generation in region , kg/kWh. is the accumulated output of all expected newly-distributed PV volume before day in administrative region , kWh.

For predict the PV system energy yield, firstly, we estimate the distance between the arrays to get the actual area required to deploy a single PV panel. Then the potential capacity of PV system can be calculated. Finally, the PV output is calculated in combination with local distance data. The formulas used are as follows:

| (10) |

| (11) |

| (12) |

where is the distance of adjacent arrays, m. is the width of panels, m. is the tilt angle of panels and is the latitude of the place where the PV system is sited. is the length of the PV panel, m. is the available area for PV deployment, m2.is the maximum Power at STC. Here we set as 365 W. is local horizontal irradiance, kWh/m2; is the standard test condition of PVs, 1000 W/m2; is the capacity of installed PV system, kW; is the overall Performance coefficient, Here we set as 0.78.

The location of the sited PV is the key to evaluate the output. However, the location of the purchaser (firm) and installation location in a transaction may not be in the same administrative region. Here, based on the statistical data of PV installations, we reconstructed the spatial sales network of the distributed PV market.

5. Result analysis

5.1. Sales network of distributed PV sector

From the company data and financial transaction data, we tracked the sales network of the distributed PV market across all of Japan, as shown in Fig. 4a. The PV manufacturers provide direct selling services to downstream markets, mainly including households (comprising 26.77% of total sales volume), manufacturing industries (17.61%). Additionally, there are also four kinds of intermediators between the PV manufacturers and the downstream markets, which are distributed PV wholesalers, installers, retailers, and leasers. The market share of each intermediator is 36.12%, 10.00%, 2.46%, and 1.33%, respectively. Through these intermediators, PV products are transferred to third-level customers, which are mainly contained within households. Overall, in the context of end-customers, the major end-customers of distributed PV products are households (total shares 75.97%) and manufacturers who own large-area land properties (total shares 17.88%) like warehouses and factories.

Additionally, we also found the distribution of the installation location of distributed PV has strong relations with economic development. Fig. 4b shows the spatial distribution of newly installed distributed PV across Japan. Most solar PVs are installed in areas that are south of the Kanto area, including Okinawa. This is mainly because the intensity of sunshine is much stronger in the south, and the time period of high intensity is longer in these areas. Also, installations south of mountain ranges outnumber those to the north, because irradiation on the southern side is stronger. These areas are more suitable for installing distributed PV. Here, we highlight four regions with a high density of installation: the Tokyo area, Nagoya area, Osaka-Kobe area, and Kagoshima-Miyazaki area. We found that although city center areas have high population and energy demand, new installations in urban areas are relatively low. On the contrary, installations in suburban areas is very high. This indicates that the distributed PV market in the urban areas is near saturation. However, due to economic spread effects, suburban areas develop quickly and are the biggest distributed PV market. With the lockdown, the output of service industries, which is mainly in city centers, suddenly reduces. This causes cascading effects on upstream industries, which would be mainly located in the nearby suburban areas, which in turn reduces the income-level of local people. In consequence, new investment in distributed PV in these major markets would be slowed down.

5.2. Market slowdown in distributed PV sector

Impacted by the economic downturn caused by the COVID-19 crisis, residential income level, upstream industry production, and infrastructure development will generally tend towards contraction. Moreover, this contraction will gradually expand with increased duration of the country’s lockdown. As a consequence, the impacted end-customers would tend to reduce their investment in distributed PV, and shift towards purchasing necessities. Here, we explored the economic footprint of COIVD-19 in the distributed PV sector in four aspects—sales, demand, firms, and employees—and four proposed respective indicators, which are value-added loss of the whole sector (including manufacturers and intermediators), market demand loss, Proportion of PV companies under Risk of Collapse (PFRC), and Proportion of employees in the PV sector under Risk of Suspension of Work (PRSW).

Based on our simulations, we found severe potential damage in the distributed PV market during the lockdown period. Fig. 5a displays the change in value-added loss as lockdown duration is extended, showing a steep increasing trend. Impacted by the one-month-long lockdown, the value-added loss is 8.06% in the entire distributed PV sector. When the lockdown duration is extended to three months, the monthly value-added loss would reach 67.69%—including 45.22% from manufacturers, 16.33% from wholesalers, and 4.52% from installers. Under the one-month to three-month lockdown policies, the demand loss from end-customers boosts from 9.49% to 78.69%. At the beginning of the lockdown, due to the mandatory closure of stores and the decline in purchasing power, service and manufacturing industries are the first to be affected by the COVID-19 lockdown and slow down their new investment in PV products. Consequently, as shown in Fig. 5b, the demand loss brought by the one-month lockdown is mainly from the manufacturing industries. Service industries also contribute about 1.20%, even they only share a small part of the end-customer group. As lockdown duration is extended, the propagation of economic impacts finally reaches to households by causing unemployment and income decline. As a result, the household demand loss for PV products increases sharply to 57.00% when the country goes to a three-month lockdown. Regarding PV firms, we predicted a high risk of massive collapse after a three-month lockdown (Fig. 5c). Additionally, about 81% of employees in the PV sector will face the risk of suspension of work (Fig. 5d). This kind of damage could be far-reaching and difficult to recover, across the entire PV sector. Compared with the first two lockdown scenarios, the increases in PFRC and PRSW in the three-month lockdown are extremely rapid. These results indicate that the two-month lockdown duration would be a high-risk threshold value of market slowdown in the distributed PV sector.

5.3. Loss in potential emission reduction capacity

The above results show that, as some environmental scientists and economists have worried, the distributed PV sector would face a dramatic slowdown in installation activity due to lockdown measures. The contraction of PV demand will undoubtedly create a considerable shock to renewable the energy transformation. Compared to the expected reduction emission capacity under normal conditions, we focused on the potential power production of the loss in distributed PV demand and the local emission factor of electricity generation to measure the loss rate in potential emission reduction capacity (LRER) caused by the distributed PV market slowdown (see Experimental procedures).

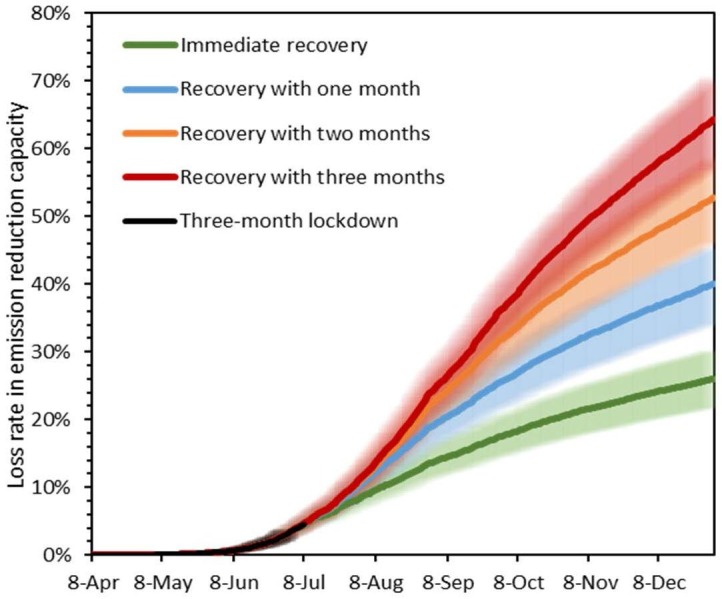

Here, we focused on the lockdown policy lasting three months, and estimated the LRER in four scenarios of the economic recovery process with different duration spans back to the normal level (Fig. 6 ). When looking at the whole year, the early-year market slowdown in the distributed PV sector will cause a large amount of indirect emissions. The value of year-end indirect emissions shows exponential growth as recovery duration spans are extended. To be specific, if the economy recovers immediately after the lockdown policy, which is the most optimistic hypothesis, the lockdown would cause 26.0% LRER at the end of 2020. In one- and two-month recovery scenarios, the LRER at the end of the year is about 40.0% and 52.7%, respectively. If the recovery process prolongs to three months, the LRER will increase to 64.2%, which is approximately 2.5 times compared to immediate recovery. This high proportion value indicates that more than half of emission reduction efforts by planned new-sited distributed PVs will be devoured by COVID-19 lockdown. These results reveal that in addition to the COVID-19 lockdown’s effects on the national economy, the lockdown would also have far-reaching negative impact on the reduction strategy roadmap.

Fig. 6.

Loss rate in emission reduction capacity caused by COVID-19 lockdown in the distributed PV sector. Here, we set four scenarios of the recovery process with different duration spans after a three-month lockdown: Immediate recovery, recovery within one month, two months, and three months. The economic recovery simulation is a reversion process of the lockdown economic damage simulation. Each curve shows one LRER in 2020 in one scenario and its corresponding confidence interval.

5.4. Incentive strategies for distributed PV market

In the context market complexities associated with the lock-down shock, incentive policies should ideally to incentivize in the distributed PV market to minimize the LRER. However, the policy mixes of the incentive strategy are various, since the government could adjust the policy intensity ratio of each month, and it is hard to assess the feasibility of the proposed solutions. To this end, we focused on the incentive strategies to help the government to achieve the targets to reduce LRER to 15% and 10% within two or three recovery months. We exhaustively listed all the policy mixes in the period of recovery which could help to achieve the targets (see Fig. 7 ). Firstly, we focused on an extremely unbalanced case where the government invests all subsidies into the market during the first recovery month to boost the distributed PV consumption to a high level, while, during the other recovery months, the government tries to maintain the reference level of consumption. In this case, the consumption increasing rate in the first recovery month should be boosted to 34% and 52% respectively to achieve the decrease target of the LRER to 15% and 10%. In case the government only invests in the third recovery month, which means the government delays market recovery, the consumption increasing rate in the third recovery month should be increased to 49% and 75% respectively (see Fig. 7b and d). The results show that the later incentive policies are implemented, the greater the pressure on consumption increasing rate in the recovery month. The results reveal the key recovery time node, and the urgency to formulate corresponding incentive policies for the PV sector.

Fig. 7.

Incentive policy mix sets for distributed PV market. The X-axis of Figures represents the number of policy mix. The Y-axis represents the required consumption increase rate for distributed PV market under different expected LRERs in the recovery month. Different color represents different recovery month. Every policy mix contains two (Fig. 5a, c) or three (Fig. 5b, d) points. For example, in Fig. 5a, No. 21 policy mix contains two points. The values in X-axis coordinate are 20% (red) and 14% (blue), which means to achieve the target, in the first recovery month, the government should increase the consumption rate by 20%, and 14% in the second recovery month. The color dot lines represent the maximum value of each recovery month in the policy mix set, which happens only when just one recovery month undertakes task in increasing the consumption rate. a. Incentive policy mix set aiming to decrease LRER to 15% with two months. b. Incentive policy mix set aiming to decrease LRER to 15% with three months. c. Incentive policy mix set aiming to decrease LRER to 10% with two months. d. Incentive policy mix set aiming to decrease LRER to 10% with three months. (For interpretation of the references to color in this figure legend, the reader is referred to the web version of this article.)

In addition, the proposed method can help the government to dynamically adjust the policy mix coping with the uncertainties of market response. For example, if the government expects to reduce the LRER to 15% by only implementing the policy in the first recovery month, from the strategy chart we would suggest that the required CIR should be 34%. However, due to the uncertainties of market response, the government may just achieve, for example, 20% of CIR. Based on the strategy chart, the policymaker can easily find out the other feasible policy mixes for the next two months under the constraint of 20% of CIR in the first recovery month, like a policy mix by 20% in the first recovery month and 14% in the second recovery month (Fig. 7a).

Following the above analysis, the suggestion of incentive strategies can be summarized as:

-

(1)

Formulate incentive policies as soon as possible.

The two-month lockdown duration would be a high-risk threshold value of market slowdown in the distributed PV sector. The later incentive policies are implemented, the more risks and losses the government has to bear. It is an urgent task to launch the incentive policies towards PV market.

-

(2)

The emphasis of the incentive policies is different in different stages.

As the main PV demand loss change from manufacturing industries loss to the household demand loss over time, PV incentive policies should gradually change from production supply prioritization to demand-side policy domination.

-

(3)

Adjust the incentive policies mix flexibly to cope with the uncertainties of market response

Considering the deep market uncertainties associated with such systemic risks as COVID-19, the policies should be flexible and adjustable for both manufacturers and consumers.

6. Conclusions

Environmental scientists and economists have argued that extreme crises, like this COVID-19 pandemic, could hinder the progress of renewable energy projects, especially in the distributed PV sector. However, these arguments have lacked comprehensive scientific evidence and quantitative assessment. Using a comprehensive compilation of datasets of Japan’s PV market, including 1.6 million financial transaction records and 44,374 newly-distributed PV installation records we tracked the spatio-temporal sales network of the distributed PV market, and explored the market slowdown in the distributed PV sector caused by the COVID-19 lockdown. From the results, we found severe damage in the distributed PV market during the lockdown period. Two-month lockdown duration would be a high-risk threshold value in the distributed PV sector. When the duration exceeds the threshold value, the monthly value-added loss reaches 67.69%, and demand shrinks by 78.69%. Additionally, 7.18% of distributed PV firms would face risk of collapse, and about 81% of employees in the PV sector would be suspended from work. Moreover, we pointed out the environmental impacts of the market slowdown in the distributed PV sector. Compared with the expected construction schedule of distributed PV, the market slowdown cuts as much as 64.2% of emission reduction potential over the whole year. These results indicate that in addition to the effect on the market, the lockdown would also have a far-reaching negative impact on the emission reduction strategy roadmap. Finally, we illustrate how the government could develop comprehensive incentive strategies for the distributed PV market considering the deep market uncertainties associated with such systemic risks as COVID-19. We assess the benefits of dynamically adjusting detailed guidelines of incentive plans aiming to achieve economic, social and environmental recovery targets.

With the support of reliable and fine-grained datasets and the proposed comprehensive analysis framework, we believe our proposed findings can offer fundamental support for guiding the government in designing economic, environmental, and social policies in the context of systemic risk management for the PV sector. Additionally, the proposed methods are not limited to the studied COVID-19 lockdown case, but rather are also practical for analyzing cases of potential future waves of COVID-19 and similar crises. This study is carried out as part of joint research with Teikoku Databank, Ltd. The authors would like to thank Teikoku Databank, Ltd. (TDB) for providing the inter-frm transaction big data.

CRediT authorship contribution statement

Haoran Zhang: Conceptualization, Methodology, Formal analysis. Jinyue Yan: Supervision. Qing Yu: Writing - original draft, Visualization. Michael Obersteiner: Supervision. Wenjing Li: Visualization. Jinyu Chen: Writing - original draft, Methodology. Qiong Zhang: Supervision. Mingkun Jiang: Supervision. Fredrik Wallin: Supervision. Xuan Song: Supervision. Jiang Wu: Supervision. Xin Wang: Supervision. Ryosuke Shibasaki: Supervision.

Declaration of Competing Interest

The authors declare that they have no known competing financial interests or personal relationships that could have appeared to influence the work reported in this paper.

References

- 1.Wang Y., Yuan Y., Wang Q., Liu C., Zhi Q., Cao J. Changes in air quality related to the control of coronavirus in China: implications for traffic and industrial emissions. Sci Total Environ. 2020:13. doi: 10.1016/j.scitotenv.2020.139133. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 2.Callaway E, Cyranoski D, Mallapaty S, Stoye E, Tollefson JJN. Coronavirus by the numbers. 2020;579:482. [DOI] [PubMed]

- 3.Huang X, Ding A, Gao J, Zheng B, Zhou D, Qi X, et al. Enhanced secondary pollution offset reduction of primary emissions during COVID-19 lockdown in China; 2020. [DOI] [PMC free article] [PubMed]

- 4.Organization WH, organization Wh. Coronavirus disease (COVID-2019) situation reports; 2020.

- 5.Temple JJMTR. Why the coronavirus outbreak is terrible news for climate change; 2020.

- 6.Manzanedo RD, Manning PJSotTE. COVID-19: Lessons for the climate change emergency. 2020;742:140563. [DOI] [PMC free article] [PubMed]

- 7.Oldekop JA, Horner R, Hulme D, Adhikari R, Agarwal B, Alford M, et al. COVID-19 and the case for global development. 2020;134:105044. [DOI] [PMC free article] [PubMed]

- 8.Duffin EJSR, April. Impact of the coronavirus pandemic on the global economy-statistics & facts. 2020;3:2020.

- 9.Gulseven O, Al Harmoodi F, Al Falasi M, ALshomali IJAaS. How the COVID-19 pandemic will affect the UN sustainable development goals? 2020.

- 10.IEA. Global Energy Review 2020; 2020.

- 11.Luthander R, Widén J, Nilsson D, Palm JJAe. Photovoltaic self-consumption in buildings: a review. 2015;142:80–94.

- 12.Wu Y, Wang J, Ji S, Song Z, Ke YJJoCP. Optimal investment selection of industrial and commercial rooftop distributed PV project based on combination weights and cloud-TODIM model from SMEs’ perspectives. 2019;234:534–48.

- 13.Xin-gang Z, Yi-min XJE. The economic performance of industrial and commercial rooftop photovoltaic in China. 2019;187:115961.

- 14.Tyagi V, Rahim NA, Rahim N, Jeyraj A, Selvaraj LJR, reviews se. Progress in solar PV technology: research and achievement. 2013;20:443-61.

- 15.Borenstein SJJotAoE, Economists R. Private net benefits of residential solar PV: the role of electricity tariffs, tax incentives, and rebates. 2017;4:S85–S122.

- 16.Creutzig F, Agoston P, Goldschmidt JC, Luderer G, Nemet G, Pietzcker RCJNE. The underestimated potential of solar energy to mitigate climate change. 2017;2:17140.

- 17.Nwokocha CO, Okoro UK, Usoh CIJRe. Photovoltaics in Nigeria–Awareness, attitude and expected benefit based on a qualitative survey across regions. 2018;116:176–82.

- 18.Zhang F, Deng H, Margolis R, Su JJEP. Analysis of distributed-generation photovoltaic deployment, installation time and cost, market barriers, and policies in China. 2015;81:43–55.

- 19.Garlet TB, Ribeiro JLD, de Souza Savian F, Siluk JCMJR, Reviews SE. Paths and barriers to the diffusion of distributed generation of photovoltaic energy in southern Brazil. 2019;111:157–69.

- 20.Rigo PD, Siluk JCM, Lacerda DP, Rosa CB, Rediske GJJoCP. Is the success of small-scale photovoltaic solar energy generation achievable in Brazil? 2019;240:118243.

- 21.Ballif C, Perret-Aebi L-E, Lufkin S, Rey EJNE. Integrated thinking for photovoltaics in buildings. 2018;3:438–42.

- 22.da Silva PP, Dantas G, Pereira GI, Câmara L, De Castro NJJR, Reviews SE. Photovoltaic distributed generation–An international review on diffusion, support policies, and electricity sector regulatory adaptation. 2019;103:30–9.

- 23.Engel H. How a post-pandemic stimulus can both create jobs and help the climate; 2020.

- 24.Baker S.R., Farrokhnia R.A., Meyer S., Pagel M., Yannelis C. How does household spending respond to an epidemic? consumption during the 2020 covid-19 pandemic. Natl Bureau Econ Res. 2020 [Google Scholar]

- 25.Yan J, Yang Y, Campana PE, He JJNE. City-level analysis of subsidy-free solar photovoltaic electricity price, profits and grid parity in China. 2019;4:709–17.

- 26.Zhengshan JY, Carpenter JV, Holman ZCJNE. Techno-economic viability of silicon-based tandem photovoltaic modules in the United States. 2018;3:747–53.

- 27.Lilliestam J, Melliger M, Ollier L, Schmidt TS, Steffen BJNE. Understanding and accounting for the effect of exchange rate fluctuations on global learning rates. 2020;5:71–8.

- 28.Xin-gang Z, Zhen WJR, Reviews SE. Technology, cost, economic performance of distributed photovoltaic industry in China. 2019;110:53–64.

- 29.Perera A, Nik VM, Chen D, Scartezzini J-L, Hong TJNE. Quantifying the impacts of climate change and extreme climate events on energy systems. 2020;5:150–9.

- 30.McCollum DL, Gambhir A, Rogelj J, Wilson CJNE. Energy modellers should explore extremes more systematically in scenarios. 2020;5:104–7.

- 31.Otto C, Piontek F, Kalkuhl M, Frieler KJNE. Event-based models to understand the scale of the impact of extremes. 2020;5:111–4.

- 32.Braunholtz-Speight T, Sharmina M, Manderson E, McLachlan C, Hannon M, Hardy J, et al. Price support allows communities to raise low-cost citizen finance for renewable energy projects. 2020;5:127–8.

- 33.Hidayatno A, Setiawan AD, Supartha IMW, Moeis AO, Rahman I, Widiono EJRE. Investigating policies on improving household rooftop photovoltaics adoption in Indonesia. 2020.

- 34.Pang Y, He Y, Cai HJJoCP. Business model of distributed photovoltaic energy integrating investment and consulting services in China. 2019;218:943–65.

- 35.Xu L, Zhang Q, Wang K, Shi XJAE. Subsidies, loans, and companies' performance: evidence from China's photovoltaic industry. 2020;260:114280.

- 36.Gao X, Rai VJEP. Local demand-pull policy and energy innovation: evidence from the solar photovoltaic market in China. 2019;128:364–76.

- 37.Programme UE. Emissions Gap Report 2019; 2019.

- 38.Zahedi A. The future of the photovoltaic market (demand side/supply side). Proceedings of the 33 intersociety energy conversion engineering conference; 1998.

- 39.Borenstein S. The market value and cost of solar photovoltaic electricity production; 2008.

- 40.Gan P.Y., Li Z. Quantitative study on long term global solar photovoltaic market. Renew Sustain Energy Rev. 2015;46:88–99. [Google Scholar]

- 41.Botelho A., Lourenço-Gomes L., Pinto L., Sousa S., Valente M. Accounting for local impacts of photovoltaic farms: the application of two stated preferences approaches to a case-study in Portugal. Energy Policy. 2017;109:191–198. [Google Scholar]

- 42.Marsillac E. Management of the photovoltaic supply chain. Int J Technol Policy Manage. 2012;12:195–211. [Google Scholar]

- 43.Davies J, Joglekar N. The market value of modularity and supply chain integration: theory and evidence from the solar photovoltaic industry. Boston U School of Management Research Paper; 2010.

- 44.Guo X., Lin K., Huang H., Li Y. Carbon footprint of the photovoltaic power supply chain in China. J Cleaner Prod. 2019;233:626–633. [Google Scholar]

- 45.Chen Z., Su S.-I.I. Multiple competing photovoltaic supply chains: modeling, analyses and policies. J Cleaner Prod. 2018;174:1274–1287. [Google Scholar]

- 46.Dehghani E., Jabalameli M.S., Jabbarzadeh A. Robust design and optimization of solar photovoltaic supply chain in an uncertain environment. Energy. 2018;142:139–156. [Google Scholar]

- 47.Besiou M., Van Wassenhove L.N. Closed-loop supply chains for photovoltaic panels: a case-based approach. J Ind Ecol. 2016;20:929–937. [Google Scholar]

- 48.Wang P., Yuan L., Kuah A.T. Can a fast-expanding market sustain with supply-side government aid? An investigation into the chinese solar photovoltaics industry. Thunderbird Int Bus Rev. 2017;59:103–114. [Google Scholar]

- 49.Doris E, Booth S, Chavez J, Krasko V, Stout S. Understanding the impacts of local policies on distributed photovoltaic market development. Energy Sustainability: American Society of Mechanical Engineers; 2014. p. V002T11A1.

- 50.Moosavian S., Rahim N., Selvaraj J., Solangi K. Energy policy to promote photovoltaic generation. Renew Sustain Energy Rev. 2013;25:44–58. [Google Scholar]

- 51.Grau T., Huo M., Neuhoff K. Survey of photovoltaic industry and policy in Germany and China. Energy policy. 2012;51:20–37. [Google Scholar]

- 52.Yu H.J.J., Popiolek N., Geoffron P. Solar photovoltaic energy policy and globalization: a multiperspective approach with case studies of Germany, Japan, and China. Prog Photovoltaics Res Appl. 2016;24:458–476. [Google Scholar]

- 53.Haley U.C., Schuler D.A. Government policy and firm strategy in the solar photovoltaic industry. California Manage Rev. 2011;54:17–38. [Google Scholar]

- 54.Zhi Q., Sun H., Li Y., Xu Y., Su J. China’s solar photovoltaic policy: an analysis based on policy instruments. Appl Energy. 2014;129:308–319. [Google Scholar]

- 55.Al Irsyad M.I., Halog A., Nepal R. Estimating the impacts of financing support policies towards photovoltaic market in Indonesia: a social-energy-economy-environment model simulation. J Environ Manage. 2019;230:464–473. doi: 10.1016/j.jenvman.2018.09.069. [DOI] [PubMed] [Google Scholar]

- 56.Ahmad S., Tahar R.M., Muhammad-Sukki F., Munir A.B., Rahim R.A. Role of feed-in tariff policy in promoting solar photovoltaic investments in Malaysia: a system dynamics approach. Energy. 2015;84:808–815. [Google Scholar]

- 57.Tamura Koutaro, et al. Diffusion-localization transition caused by nonlinear transport on complex networks. Scientific reports. 2018;8(5517) doi: 10.1038/s41598-018-23675-x. In this issue. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 58.Programme IPPS. National Survey Report of PV Power Applications in Japan – 2018; 2019.

- 59.center Mer. Japan Economic Outlook; 2020.