Summary

Dramatic reductions in solar, wind, and battery storage costs create new opportunities to reduce emissions and costs in China’s electricity sector, beyond current policy goals. This study examines the cost, reliability, emissions, public health, and employment implications of increasing the share of non-fossil fuel (“carbon free”) electricity generation in China to 80% by 2035. The analysis uses state-of-the-art modeling with high resolution load, wind, and solar inputs. The study finds that achieving an 80% carbon-free electricity system in China by 2035 could reduce wholesale electricity costs, relative to a current policy baseline, while maintaining high levels of reliability, reducing deaths from air pollution, and increasing employment. In our 80% scenario, wind and solar generation capacity reach 3 TW and battery storage capacity reaches 0.4 TW by 2035, implying a rapid scale up in these resources that will require changes in policy targets, markets and regulation, and land use policies.

Subject areas: Energy management, Energy Modelling, Energy policy, Energy resources, Energy sustainability

Graphical abstract

Highlights

-

•

China could reach 80% carbon-free electricity by 2035 at 6% lower cost

-

•

China’s power grids can be reliably operated with a high level of non-fossil generation

-

•

Exceeding existing non-fossil goals can reduce additional emission and health impacts

-

•

Job gains in clean energy more than offset those lost in coal-related industries

Energy management; Energy Modeling; Energy policy; Energy resources; Energy sustainability.

Introduction

The electricity sector will play a pivotal role in meeting China’s environmental goals, including both carbon neutrality and air quality goals. Increases in non-fossil generation, combined with electrification in the transportation, industrial, and building sectors, can generate significant reductions in emissions. Many recent modeling studies have evaluated deep decarbonization scenarios for China’s energy system, with emphasis on 2050. Earlier energy system modeling studies evaluated transitions needed to achieve 1.5 and 2C scenarios for China, including for the power sector, out to 2050 (Institute of Climate Change and Sustainable Development (ICCSD), Tsinghua University, 2020; Jiang et al., 2018). Zhang and Chen (2022) used Monte Carlo analysis to analyze numerous sectoral decarbonization pathways, including for power, to highlight uncertainties. For the power sector specifically, Kahrl et al., (2020c) modeled the resource portfolios and economic and institutional implications for eliminating coal power generation by 2040 and 2050. Zhuo et al., (2022) modeled specific climate mitigation target scenarios for China’s power system to assess the associated renewable development costs, power system security constraints and grid expansion investments and found 19.9% increase in electricity supply costs by 2050 to achieve carbon neutrality.

Few power system modeling studies have focused on the technical potential and socioeconomic implications of more ambitious renewable deployment in the near-term, i.e., 2030 to 2035, to accelerate China’s broader energy transition. Previous analysis has shown that 62% of non-fossil generation could be achieved by 2030 cost-effectively but did not consider the latest renewable energy cost trends or offshore wind resources for China (He et al., 2020). Chen et al. (2020) analyzed the investment and operation costs for national and provincial planning with the target of realizing 80% renewable energy penetration in 2030, 2040, and 2050, along with other scenarios to explore the potential for hydrogen, electrification, storage and charging and other variables impacting the power system. They find only 40% renewable adoption is cost-effective in 2030, and 80% is cost-effective in 2050, but did not consider the latest ambitious pumped hydro storage targets announced by China.

This article aims to build on existing research to examine the technical and operational feasibility, economic impacts, and socioeconomic implications of increasing the share of non-fossil fuel electricity generation in China to 80% of total generation by 2035 (see Table 1). The analysis uses state-of-the-art modeling tools, detailed load, wind, and solar profiles for China, and recent projections for wind, solar, and electricity storage costs in China (see Figure 12, Figure 13, Figure 14).

Table 1.

Description of scenarios

| Current Policy Scenario | Clean Energy Scenario | |

|---|---|---|

| Coal generation capacity additions | 150 GW of new net coal generation is forced into the model | No new net coal generation is forced into the model |

| Wind and solar generation capacity additions | Annual wind and solar generation capacity additions are limited to policy targets (1,200 GW total wind and solar capacity by 2030) | Annual wind and solar generation capacity additions decided by model to meet 80% clean electricity by 2035 |

| Non-fossil generation share | Least-cost optimization, subject to limits on non-fossil generation additions | 46% in 2025; 65% in 2030; 80% in 2035 |

Figure 12.

Baseline year (2020) Generation Resources and Transmission Network used in the model Scenario

Figure 13.

National electricity demand projection used in this study, relative to other recent Studies

Sources: Jiang et al. (2018); Institute of Climate Change Sustainable Development (2020); IEA (2020); SGERI (2020); China National Renewable Energy Centre of Energy Research Institute of China (2020); China Electricity Council (2021a); Fu et al. (2020).

Figure 14.

Technology Cost Inputs for Offshore Wind, Onshore Wind, Solar PV, and Battery Storage (4-h), See also Table S4

Source: Data are from Bloomberg New Energy Finance BNEF, 2020, converted using current exchange rate of 6.34 yuan/USD.

The article aims to inform discussion around three key questions: Is a 80% non-fossil electricity system technically and operationally feasible for China by 2035? What are the economic impacts of this transition on wholesale electricity costs and broader socio-economic impacts? What would it take for China to achieve this more ambitious clean power system transition through policy changes?

To understand the magnitude of broader socioeconomic benefits, this paper also includes analyses of emissions and health impacts. Increases in the share of non-fossil generation will offset coal generation, creating employment in the manufacturing and construction sectors to expand non-fossil generation but leading to a decline in employment in coal mining and other sectors with links to the coal industry. To understand the magnitude of these competing impacts, this study also includes an employment analysis, using an input-output modeling framework and national macroeconomic data for China. Section Results describes two categories of results: (1) Changes in generation and transmission, and (2) cost, investment, emissions, reliability, health impacts, and employment impacts. Section Conclusions and discussion summarizes key conclusions from the study, provides discussion on policy changes needed to overcome barriers for a more ambitious clean power system, and outlines study limitations and areas for future research.

Results

The results are organized into two categories. The first (Section Generation and transmission) includes generation mix, generation capacity mix, generation capacity additions, transmission capacity, and coal plant operations. The second (Section Cost, reliability, emissions, and employment) includes wholesale cost, total investment, emission reductions, reliability, health impacts, and employment. Results for the sensitivity analyses are integrated into these sections.

Generation and transmission

Generation mix

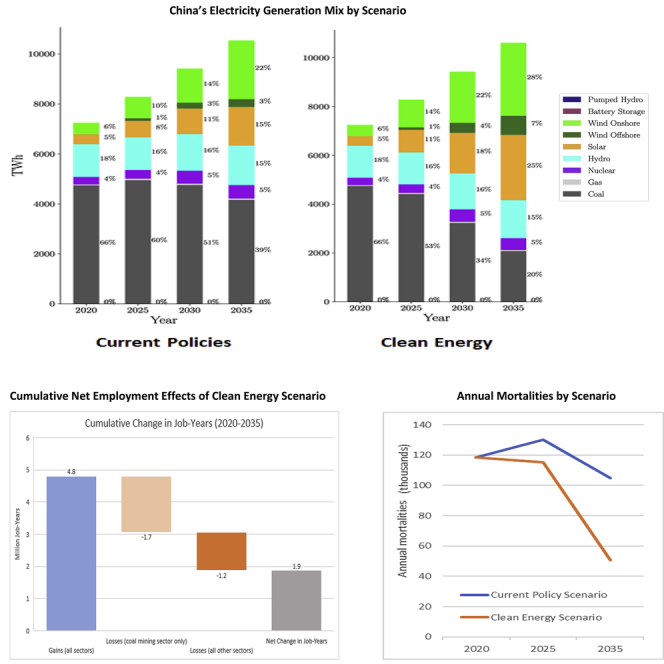

In the Current Policy scenario, non-fossil generation increases from 34% of total generation in 2020 to 60% in 2035, accounting for all new generation and reducing coal generation by about 12% relative to 2020 levels (Figure 1A). The Current Policy is consistent with the National Energy Administration’s (NEA’s) Energy Production and Consumption Revolution Strategy, which calls for non-fossil generation to reach 50% of total generation nationwide by 2030 (NEA, 2016a). In the Clean Energy scenario, non-fossil generation reaches 80% in 2035, reducing coal generation by 56% relative to 2020 levels. The incremental increase in non-fossil energy in the Clean Energy scenario, relative to the Current Policy scenario, is supplied by expanding onshore wind (47% of increased non-fossil generation), offshore wind (12%), and solar PV (42%) generation (Figure 1A).

Figure 1.

Electricity generation and capacity mixes in the Current Policy and Clean Energy cases

(A) Electricity Generation Mix.

(B) Capacity Mix.

Capacity mix

In the Current Policy scenario, all new generation capacity additions are non-fossil resources, aside from the 150 GW of coal generation under construction (Figure 1B). The model is able to build additional coal generation in the Current Policy scenario but chooses not to. This suggests that, with the inputs and assumptions used in this study, a combination of wind, solar, and electricity storage is lower cost than coal for meeting growth in electricity demand. This outcome is consistent with current government policy. Wind and solar generation capacity reach 1,273 GW in 2030 in the Current Policy scenario, in line with the government’s 1,200 GW target for 2030 (NEA, 2021a), and increases to 1,933 GW in 2035. Declining costs lead to rapid increases in battery storage capacity in the Current Policy scenario, with a total of 98 GW by 2025, 225 GW by 2030, and 244 GW by 2035.

In the Clean Energy scenario, wind and solar generation and battery storage capacity increase more rapidly than in the Current Policy scenario (Figure 1B). Divergence between the two scenarios begins in 2020–2025. In the Clean Energy scenario, wind and solar generation and battery storage capacity reach 1,153 and 155 GW by 2025, relative to 873 and 98 GW in the Current Policy scenario. Wind and solar generation capacity grow further to 1,993 GW by 2030 and 3,069 GW by 2035 in the Clean Energy scenario, significantly higher than current policy targets. Battery storage grows to 356 and 414 GW in 2030 and 2035, respectively.

Generation capacity additions

In the Current Policy scenario, limits on annual wind and solar generation capacity additions are binding and the model limits annual additions of both resources to 68, 80, and 134 GW per year in 2021–2025, 2026–2030, and 2031–2035 (Figure 2). These rates are conservative; China added 120 GW of wind and solar in 2020 (China Electricity Council, 2021b). In the Clean Energy scenario, where annual wind and solar additions are driven by economics, wind and solar generation reach an average of 124, 168, and 215 GW per year in the three model periods. Rates of battery additions in both the Current Policy and Clean Energy scenarios are an order of magnitude larger than historical rates.

Figure 2.

Annual capacity additions for wind and solar and battery storage

Transmission capacity

In the Current Policy and Clean Energy scenarios, the model does not build any new interregional capacity or new interprovincial transmission capacity from 2020 to 2025, which suggests that all cost-effective capacity had already been built by 2020. Interprovincial transmission capacity additions and investment from 2025 to 2035 are only marginally (∼3%) higher in the Clean Energy scenario (Figure 3). There are three main reasons for this result: (1) Given the deep reductions in installed costs for solar PV and onshore wind, the model can cost-effectively build these resources closer to load centers instead of importing from the highest resource quality regions via long distance transmission lines; (2) low-cost grid-scale storage obviates a large part of the new transmission investments needed for grid balancing; and, (3) electricity demand growth between 2020 and 2035 requires a large increase in baseline transmission investment in the Current Policy scenario, which means that the incremental transmission investment needed in the Clean Energy scenario, relative to the Current Policy scenario, is lower.

Figure 3.

Interprovincial and interregional transmission capacity (left panel) and annualized costs for new transmission (right panel)

Coal plant operations

Coal power plant operations change significantly in the Current Policy and Clean Energy scenarios, with steep declines in annual operating hours for most coal generators and increases in the variance of annual operating hours in both scenarios. Average annual operating hours for coal plants fall from 4,526 h per year (52% annual capacity factor) in 2020 to 3,469 (40%) h per year in 2035 in the Current Policy scenario and 1,986 (23%) h per year in 2035 in the Clean Energy scenario. Although some coal power plants continue to provide base load support, most of the coal capacity operations shift from an annual base load to seasonal, particularly during low-RE/high demand seasons and many coal power plants may not dispatch at all. For example, in the Clean Energy Case, about 450 GW of coal power plants are never required to be dispatched in an average year, whereas less than 100 GW of coal power plants (mostly with the lowest variable cost) operate at near-base load with >60% annual capacity factor, and 500 GW operate primarily during high demand months like July/August or December/January, implying an annual capacity factor of 30%. All coal power plants still meet their technical operational constraints such as technical minimum levels, minimum up or down times, maximum ramp rates etc.

Figure 4 shows the change in annual capacity factors for individual coal units in the Clean Energy scenario, illustrating the high variance in capacity factors among coal units and the overall decline in capacity factors by 2035.

Figure 4.

Annual Capacity Factors for Coal Generators

Note: Each dot represents the capacity factor of an individual coal unit.

Cost, reliability, emissions, and employment

Wholesale cost

Average wholesale costs (average wholesale costs are total wholesale costs divided by total generation. Here, wholesale costs include installed capacity, fixed O&M, fuel costs for generation, storage, and installed capacity costs for interprovincial and interregional transmission) are 6% lower in the Clean Energy scenario than in the Current Policy scenario in 2035, because the incremental annualized cost of additional investments in wind, solar, batteries, and transmission in the Clean Energy scenario (497 billion yuan per year) is less than the sum of incremental cost savings from coal and natural gas fuel (426 billion yuan per year) and additional investments in coal generation (95 billion yuan per year) in the Current Policy scenario (Figure 5). Lower average wholesale costs in the Clean Energy scenario suggest that the limits on annual wind and solar generation capacity additions in the Current Policy scenario are below levels that are cost-effective.

Figure 5.

Average wholesale costs

Total investment

Total cumulative investment in the Clean Energy scenario is somewhat higher (516 billion yuan, 17%) than in the Current Policy scenario in 2025, but by 2035 the difference in cumulative investment between the two scenarios grows to nearly 4 trillion yuan (40%) (Figure 6). As discussed above, this large increase in investment is essentially financed using coal fuel cost savings.

Box: Offshore wind sensitivity.

China has significant, high-quality offshore wind resources along its eastern coast. The offshore wind sensitivity (see Section 2.4 for a description) allows these resources to be rapidly developed. In this sensitivity, we relax limits on annual capacity additions for offshore wind, which allows additional offshore wind to displace onshore wind and solar generation. The share of offshore wind in the generation mix increases from 7 to 15% in 2035, whereas the shares of onshore wind and solar fall from 28 to 23% and 25–23%, respectively. Total offshore wind generation capacity increases from 170 to 400 GW, corresponding to annual deployment of 20 GW per year from 2025 to 2030 and 56 GW per year from 2030 to 2035 (Figure 7).

Figure 7.

Average annual capacity additions under clean energy scenario and offshore wind sensitivity scenario

In 2035, wholesale costs in the offshore wind sensitivity (322 yuan/MWh) are similar to those in the Clean Energy scenario base case (318 yuan/MWh), and lower than in the Current Policy scenario (327 yuan/MWh). Total generation and transmission investment in the offshore wind sensitivity is comparable to the Clean Energy scenario base case. The results suggest that offshore wind could be an important resource for China’s energy system by reducing the need to develop higher-cost (lower resource quality) onshore wind and solar generation resources to meet energy and environmental policy goals.

Note: Offshore wind costs include grid interconnection and other incremental transmission costs.

Figure 6.

Cumulative New Capital Investment for Generation and Transmission

Note: Investment in each year is total cumulative, rather than annualized, investment.

Emission reductions and health benefits

In the Current Policy scenario, CO2, SO2, and NOX emissions intensity (emissions per kWh generated) falls significantly, though absolute emissions increase in the short run and fall only by 12% from 2020 levels by 2035 due to electricity demand growth (Figure 8A). In the Clean Energy scenario, CO2 emissions intensity falls by 70% from 2020 levels, to 0.16 tCO2/MWh, and absolute emissions fall by 50% (by 1,660 MtCO2) by 2035 (Figure 8A). SO2 and NOX emission intensities are also much lower in the Clean Energy Scenario.

Figure 8.

Emissions Reductions and Health Impacts

CO2, SO2, and NOX Emissions Intensities (A). Annual Mortalities and Map of Avoided Deaths (B). Note: The map on the right of Panel B shows annual avoided premature deaths associated with power plant emissions under the Clean Energy scenario, compared to the Current Policy scenario.

Lower emissions from coal-fired generation lead to a significant reduction in mortality, with annual deaths related to electricity generation falling by approximately 50% in the Clean Energy scenario, relative to the Current Policy scenario, in 2035. As Figure 8B illustrates, reductions in the intensity of mortality (deaths per 1,000 km2) are evenly distributed across China.

Reliability/coal retirements

In the coal retirement sensitivity, 30-year lifetimes reduce the coal capacity to about 800 GW by 2035 — a reduction of about 250–300 GW. We find that the electricity system is able to meet demand plus a 10% operating reserve margin during the highest summer and winter net load weeks even with lower coal generation capacity, as reservoir hydropower, gas generation, and storage energy make up the capacity shortfall from retired coal generation (Figure 9).

Figure 9.

National system dispatch in the highest net load week in summer (2035), with coal retirements

Reliability/supply and demand shocks

During the highest net load hour of the 35-year wind and solar data, wind and solar generation fall by 162 GW relative to our base weather year (2018) wind and solar generation profiles. During the highest net load week in summer, aggregate national renewable energy generation drops by 12% relative to our base year (Figure 10A); during the highest net load week in winter, it drops by 14% relative to our base weather year (Figure 10B). Because of the regional diversity and resource diversity, the reduction in national aggregate renewable generation availability across the 35 weather years is limited to 12%–14% during peak load periods(within a province or at an individual site level, the inter-annual variation in renewable generation would be higher than the national aggregate number).

Figure 10.

National system dispatch results for highest net load weeks under system shocks

National system dispatch in the highest net load week in summer (2035), using 35 years of weather data (A). National system dispatch in the highest net load week in winter (2035), using 35 years of weather data (B). National system dispatch in the highest net load week in summer (2035), with a 10% demand shock (C). National system dispatch in the highest net load week in winter (2035), with a 10% demand shock (D).

Other sources of capacity and energy must replace this shortfall. In the dispatch simulation, wind and solar generation are replaced by coal and gas generation. With a 10% demand shock (increase), peak demand increases to nearly 2,000 GW, but the system still has adequate resources to meet demand in the highest summer and winter net load weeks (Figures 10C and 10D).

Employment

Increases in non-fossil generation in the Clean Energy scenario lead to significant shifts in expenditures within the electricity sector, in particular from spending on coal fuel to construction and manufacturing spending on wind, solar, and energy storage installations. This shift in expenditures leads to changes in employment, with lower spending on coal fuel leading to reduced employment concentrated in the coal mining sector, and higher spending on construction and manufacturing leading to higher net employment.

We estimate that the lower spending on coal generation leads to a total of 1.7 million cumulative coal mining job-years lost from 2020 to 2035. Other (non-coal) sectors experience a loss of 1.2 million job-years in aggregate over the same period. In contrast, higher spending on wind, solar, and energy storage leads to a total gain of 4.8 million cumulative job-years from 2020 to 2035, for a net increase of 1.9 million job-years (Figure 11). These results are highly sensitive to assumptions about the labor productivity growth rate in each sector, particularly in the coal mining sector. Removing productivity growth rates from the calculation results in a net gain of 4.3 million job-years by 2035.

Figure 11.

Cumulative net employment effects of clean energy scenario

The net employment effects of the shift from fossil to non-fossil generation are relatively small, both in absolute terms and relative to the size of China’s labor force. However, because changes in employment will be uneven both across provinces and across time, managing the macroeconomic impacts of the transition from fossil to non-fossil generation will likely require careful policy support.

Conclusions and discussion

Sustained declines in costs for wind, solar, and electricity storage technologies create new opportunities to lower wholesale costs and reduce emissions in China’s electricity sector. The results of this study suggest that expanding the share of non-fossil electricity generation from around 60%, under current policies (Current Policy scenario), to 80% (Clean Energy scenario) by 2035 is technically and operationally feasible. In addition, a more ambitious and faster transition to a clean power system would lower wholesale electricity costs and support the Chinese government’s goals for carbon neutrality and air quality. Transitioning to an electricity system with 80% non-fossil generation would require overcoming barriers to the development and integration of wind generation, solar generation, and energy storage.

This final section summarizes the study’s key conclusions, provides recommendations for changes in policy and regulation based on the results, and outlines priorities for future research identified through this study.

Key conclusions

The analysis in this study supports five key conclusions.

Declining wind, solar, and electricity storage costs are changing the economics of China’s electricity sector

The Current Policy and Clean Energy scenarios illustrate emerging changes in the economics of China’s electricity sector. In both scenarios, the lowest cost resources for meeting growth in electricity demand are a combination of wind, solar, and battery storage. This result suggests that a combination of these resources is lower cost than building new coal generation.

In the Clean Energy scenario, adding additional wind, solar, and energy storage cost-effectively reduces generation from existing coal plants because the incremental cost of additional wind, solar, storage, and transmission is lower than the fuel cost savings from reduced coal plant operations. This result suggests that, in the Clean Energy scenario, it is lower cost to build new wind generation, solar generation, and some battery storage than to continue to operate existing coal plants.

China’s electricity system can be reliably operated with high levels of non-fossil generation

The reliability sensitivity showed that China’s electricity system could maintain high standards of reliability with an 80% non-fossil generation mix that includes 60% wind and solar generation in 2035. With higher levels of wind, solar, hydropower, and electricity storage, reliability concerns will shift from capacity adequacy to capacity and energy adequacy. However, even during prolonged periods of low wind and solar generation and unanticipated load increases, China’s electricity system would be able to maintain adequate capacity and energy. New coal generation is not needed to ensure resource adequacy.

The two key enabling conditions for ensuring reliability with high levels of renewable generation are: (1) a robust approach for optimizing the operation of electricity storage facilities, to ensure that individual storage operations support the reliability of the electricity system as a whole; and, (2) regionally and nationally coordinated operations, to ensure that provinces and regions that are short power can seamlessly import from neighboring provinces and regions on shorter and longer timescales.

Exceeding existing goals for non-fossil generation would deliver additional emission reduction and health and employment benefits

Increasing the share of non-fossil generation to 80% would support significant additional reductions in CO2 emissions and health costs and mortality related to poor air quality. Emission reductions and health benefits would be greater than the estimates in this study due to electrification. For instance, transportation electrification, combined with an accelerated shift to non-fossil generation, will reduce both vehicle tailpipe and power plant emissions. The combination of electrification and accelerated deployment of non-fossil generation would thus be a powerful tool to hasten progress toward China’s environmental goals.

Reductions in coal generation would lead to continued reductions in employment in the coal mining industry, but these losses would be offset by increases in employment driven by investment in wind, solar, hydropower, nuclear, and batteries. Lower wholesale electricity costs, if translated into the prices that retail customers pay, would also drive increases in employment. The challenge for policymakers in China will be to manage the transition in employment and tax revenues from an electricity sector dependent on coal to one dependent on non-fossil resources, without undermining the economics of new non-fossil generation.

Reaching cost-effective levels of non-fossil generation will require overcoming barriers to wind, solar, and storage development and integration

The Clean Energy scenario involves the development of wind, solar, and storage on an unprecedented scale. Wind and solar generation reach a combined 1,153 GW in 2025, close to the current 2030 target (1,200 GW), and grow further to nearly 2,000 GW in 2030 and just over 3,000 GW in 2035. Battery storage grows from MW scale in 2020 to 100-GW scale by 2025.

For wind, solar, and electricity storage to be developed and integrated into the electricity system on this scale, barriers to scaling will need to be overcome. The scenarios in this study provide a useful analogy for what overcoming barriers entails. In the Current Policy scenario, annual solar and wind generation capacity additions (GW/yr) are constrained to historical levels. As in the Clean Energy scenario, where these constraints are relaxed, overcoming barriers to scaling will mean finding ways to enable more rapid development and integration of wind, solar, and storage than has occurred historically. The most important barriers are around regulation and markets, electricity system operations, and land use. Section 5.2 discusses these barriers in greater detail.

The shift to a low-cost renewables pathway can accelerate in the next five years

The share of non-fossil generation in the Current Policy and Clean Energy scenarios begins to diverge in the 2020–2025 time period, suggesting that policy and regulatory changes to accelerate non-fossil deployment should begin in the 14th five-year planning period (2021–2025), rather than later. In particular, whereas there already may be momentum behind accelerated expansion of wind and solar generation, a near-term priority would be to lower barriers to the rapid expansion of battery storage.

Policy needs and implications for reaching 80% by 2035

Priority areas for reducing barriers to rapid wind, solar, and storage deployment for achieving 80% non-fossil power generation by 2035 include policy targets, markets and regulation, and land availability and use. Changes in these three areas would facilitate the shift from renewable energy as a peripheral resource to the backbone resource in China’s electricity system.

Targets for generation capacity and the share of non-fossil generation have historically played an important role in providing China’s electricity industry with guidance on the direction of national policy. There is no indication that policy targets will not continue to play this role in the future.

Increase 2030 targets for non-fossil generation and renewable generation capacity, and consider adding storage targets

The results of this study suggest that increasing the 2030 target for non-fossil generation from 50% to as much as 65% and the 2030 target for wind and solar generation capacity from 1,200 GW to around 2,000 GW could lead to significant additional CO2 emission reductions and health benefits at low or even negative cost, while positioning China to mostly decarbonize its electricity sector throughout the 2030s and enhance energy security.

In 2021, the NEA increased its target for pumped hydropower to 120 GW by 2030 (NEA, 2021b). China’s Action Plan for Carbon Dioxide Peaking Before 2030 set a target of 30 GW or more for new types of energy storage by 2025 (The State Council of the People’s Republic of China, 2021). Developing explicit, longer-term targets for electricity storage could provide helpful signals to storage manufacturers and the electricity industry on the expected pace and scale of electricity storage capacity and integration needs.

Set targets for the share of non-fossil generation capacity for 2035

China does not yet have non-fossil generation and wind, solar, hydro, and nuclear generation capacity targets for 2035. Adoption of 2035 targets could also provide helpful long-term signals to manufacturers, the electricity industry, and provincial and local governments on the expected pace and scale of change.

Changes in regulation that mainstream and create stable business models for wind, solar, and storage in electricity resource procurement and markets will be important to reduce barriers to more rapid deployment of these resources. Mainstreaming involves progress through a series of interrelated reforms that are already underway.

Consolidate approaches to renewable energy procurement and focus on participation in forward contract markets

The first of these reforms is in resource procurement. Currently, renewable generation in China is bought and paid for through a combination of several feed-in tariff and market-based procurement mechanisms, many of which result in excessive losses and unpredictable revenues for renewable generators (Yong, 2022). In addition, these mechanisms do not enable direct wholesale competition between renewable generation and thermal generation.

To address this problem, the different approaches to procuring renewable generation can be jettisoned in favor of a single approach — procurement through forward contract markets. Under this approach, renewable generation competes directly with thermal generation for forward contracts with industrial and grid company buyers. This approach is consistent with the intent of electricity market reforms in 2015 and the direction of renewable energy procurement guarantee policies in China (National Energy Administration, 2015, NEA, 2016b).

To level the playing field for different kinds of resources, forward contract markets can be extended (e.g., longer-term contracting, more tailored contracts) to allow for more frequent and flexible trading by buyers and sellers, while continuing to have shorter-term (e.g., monthly) auctions. Recent experience in the US illustrates that renewable generation can directly compete with thermal generation in forward procurement (Kahrl, 2021a). Spot markets will help to support participation by renewable generation in forward markets, by reducing the perceived need for physical delivery of contracted generation.

Continue progress in developing electricity spot markets and support their evolution into regional markets

For renewable generation to participate in forward markets on a larger scale, it will be important to resolve issues around imbalance costs. Imbalance costs include the difference in energy between what a seller generates and a buyer consumes, differences in locational costs due to congestion, and the costs imposed on the electricity system due to wind and solar forecast error. Real-time energy spot markets provide a natural mechanism for addressing these costs, allowing sellers and buyers to pay spot market prices to settle imbalances and to determine in their contracts which party will take on the risk for imbalance costs. The US experience has been that which entity is best positioned to manage this risk will depend on buyer and seller size, balance sheets, and sophistication.

China has several provincial spot market pilots underway. Most of these pilots feature some form of nodal pricing, 15-min dispatch and settlement, and some pilot provinces have allowed participation by renewable generation. These spot markets continue to be in trial operation mode, however, and will need continued development of market designs and regulation to support their more formal implementation. Formal implementation of these spot markets will be an important complement to forward markets. As spot markets in China mature, shifting to 5-min dispatch and settlement will help to level the playing field for wind and solar generation by reducing imbalance charges related to forecast error.

Several areas of work are needed to complement spot energy market development. They include: 1) developing system operator-run ancillary services (AS) markets that procure frequency regulation reserves and operating reserves through competitive mechanisms, paid for by loads rather than generators; 2) continuing to shift forward contracts to contracts for differences (CfDs) to enable greater real-time operational flexibility; and, 3) developing new financial products that allow market participants to hedge longer-term risk.

Lastly, spot market development will need mechanisms that facilitate greater coordination in markets and operations between provinces and regions, ideally through a single regional market operated by a regional system operator. The National Development and Reform Commission and National Energy Administration (2021) Rules for Interprovincial Spot Market Transactions (省间电力现货交易规则) provide a framework for coordinating among interprovincial spot markets, in which provincial markets incorporate export supply and import demand curves from other provincial markets, inclusive of transmission charges (National Development and Reform Commission and National Energy Administration, 2021). However, the US experience has been that a single regional system operator can better manage reliability, support more efficient dispatch and avoid inefficient dispatch due to high transmission charges, and coordinate regional resource adequacy and transmission investment relative to multiple coordinated spot markets or bilateral coordination among utilities (PJM (2019) and Midcontinent Independent System Operator (2021)).

Strengthen the renewable quota and green certificate system

Even if new wind and solar generation are low cost, these cost advantages may not be reflected in forward or spot markets in the nearer term, where markets need more time to develop and buyers and sellers lack experience with market mechanisms. For instance, imbalance charges for renewable generators may be excessively high as day-ahead and real-time energy markets take shape. China also has more than 500 GW of existing wind and solar generation that may have higher costs and would need some form of out-of-market support mechanism in the transition to a more market-oriented approach for procurement of renewable generation.

In the near term, strengthening the existing renewable quota and green certificate system could help to provide support for existing renewable generators and continue to drive the market for renewable energy. The most important areas to strengthen are: to tie the quotas more closely to policy targets, clarify responsibility for meeting the quotas, and enforce the quotas (Yong, 2022). If renewable generators are participating in forward markets, it will be most effective and efficient if the quota system is implemented on market buyers (industrial customers and grid companies), with penalties for non-compliance that exceed the premiums in renewable certificates.

Develop market participation models for electricity storage

This study projects that battery storage will be cost-effective on a hundred-GW scale by 2025, but to our knowledge China does not yet have stable mechanisms to procure or operate battery storage. Thus, there is a gap between the large-scale potential for electricity storage in China’s electricity system and the mechanisms that would allow it to be developed and integrated on this scale.

Electricity storage can provide an array of services: firm capacity, energy arbitrage, congestion management, regulation and operating reserves, and distribution and transmission cost savings. Storage, and particularly battery storage, can be located almost anywhere in the electricity system — at a generation facility, behind the customer meter, on the high voltage transmission system, on the sub-transmission system, or on the distribution system. Models like the one used in this study often only capture part of the value provided by storage and provide limited insight on where storage should be optimally located, for instance at a solar facility, directly connected to the transmission system, or at an industrial facility. Market pricing can help to better value storage and determine where it should be optimally sited.

Allowing electricity storage to participate in forward and spot markets can help create stable business models for electricity storage, giving buyers and sellers the flexibility to determine how storage is best used based on services provided, where it is best sited, and who should own it. This would enable multiple revenue and ownership models for storage. The US electricity markets can provide a useful reference on rules for energy storage participation in spot markets.

Integrate distributed energy resources into wholesale markets

Distributed energy resources (DERs), including distributed generation, distributed electricity storage, and demand response (DR), can provide an important source of energy and flexibility to complement bulk system resources. DR has long been a focus area for policy in China, and recent policies have sought to encourage distributed generation and storage. To maximize the larger value of DERs, the operation of these resources will need to be integrated into wholesale markets. There are multiple potential strategies for doing so, including tariffs that reflect market prices or direct participation of DERs in wholesale markets. DER integration into wholesale markets is an ongoing area of innovation and market reform in the US (ESIG, 2022).

Develop resource adequacy processes and mechanisms

Ensuring long-term resource adequacy in China’s electricity system, as it undergoes transitions to markets and to new resources, will likely require more systematic and formal resource adequacy processes. Such processes would identify levels of firm capacity needed to meet a reliability target, include mechanisms that encourage adequate levels of investment in firm capacity, facilitate an efficient and fair allocation of the costs of those investments, and incentivize the real-time availability and performance of resources that are counted toward firm capacity. The US electricity markets have multiple approaches to resource adequacy that can be a useful reference for China (Kahrl et al. (2021b)).

The importance of resource adequacy mechanisms increases with rising levels of renewable generation and storage. High levels of wind and solar generation will tend to depress energy market prices, which implies that generation and electricity storage needed for reliability will need to increasingly rely on scarcity pricing to recover their fixed costs. Research in the US suggests that a variety of existing approaches can ensure resource adequacy and revenue sufficiency for generators under higher renewable penetrations, though they will require continued enhancements, including: better accounting for the firm capacity value of renewable generation and storage; improved scarcity pricing and market price formation; improved generator and storage availability and performance; and, more responsive demand (Levin and Botterud, 2015; Frew et al., 2016; Wolak 2020; Ela et al., 2021).

Terawatt-scale development of wind and solar generation will require a significant amount of land, on the order of millions to tens of millions of hectares. Ensuring that adequate land is available at an economic cost, and that wind and solar development do not conflict with national and local land conservation priorities, requires greater attention to the land use implications of wind and solar development.

Prioritize land use efficiency

Technological improvements have significantly reduced the land footprint of onshore wind and utility-scale solar PV over the past decade through increased power (MW/ha) and energy (MWh/ha) densities ( Bolinger and Bolinger (2021);Department of Energy, 2021). In the US, improvements in both technologies were driven by incentives to increase energy generation (MWh) and capacity factors (annual operating hours). In China, as wind and solar become a more important part of the electricity system, government policy should also shift from an emphasis on installed capacity to an emphasis on energy generation from these resources, which will also help to encourage innovation that supports efficient land use. The renewable quota system is a step in this direction.

Offshore wind and distributed solar PV can also help to reduce the land use impacts of terawatt-scale wind and solar development. Electricity market designs, policies and tariffs for distributed generation, land prices, and transmission availability will all play important roles in determining the balance among onshore versus offshore wind, utility-scale and distributed solar, and local generation versus imports in China’s coastal provinces. This suggests the need for coordination among land use priorities, electricity resource planning, and transmission planning

Integrate wind and solar development into land use and conservation planning

Renewable developers will need clear guidance from government agencies to direct them toward project sites that do not conflict with conservation and agricultural land use priorities. Integrated land use planning can be an important source of transparent, rigorous guidance. In the US, tools for integrated land use planning have improved significantly over the past decade and could provide a helpful reference for China. https://www.nature.org/en-us/about-us/where-we-work/united-states/california/stories-in-california/clean-energy/

Study limitations and future areas of research

This study focuses on the cost, reliability, emissions, public health, and employment implications of increasing the share of non-fossil fuel (“carbon free”) electricity generation in China to 80% by 2035. As such, we have not fully explored the implications of full-decarbonization of China’s power system in the longer term. For example, as the power system approaches net-zero emissions, long-duration energy storage technologies and hydrogen, and negative emission technologies such as bio-energy with carbon-capture and storage (BECC) are likely to play important roles. Similarly, we have not examined the role of demand-side flexibility in the current analysis or smart charging of electric vehicles. These topics warrant additional research.

Although we assess an operationally feasible least cost pathway for China’s power system using spatially and temporally resolved load and generation data, further work is needed to advance our understanding of other facets of a power system with high RE penetration. First, this report primarily focuses on renewable-specific technology pathways and does not explore the full portfolio of clean technologies that could contribute to future electricity supply. Second, issues such as loss of load probability, system inertia, and alternating-current transmission flows need further assessment. Options to address these issues have been identified elsewhere (for example, Denholm et al., 2020). Second, our assessment does not fully address the operational impacts of day-ahead/intra-day forecast errors in RE and load. However, several studies have shown that with state-of-the-art forecasting techniques, the impact of such forecast errors appears to be small (for example, Hodge et al., 2015; Brancucci Martinez-Anido et al., 2016).

Although this analysis does not attempt a full power-system reliability assessment, we perform scenario and sensitivity analysis to ensure that demand is met in all periods, including during extreme weather events and periods of low renewable energy generation. This modeling approach provides confidence that integrating over 3000 GW of renewable energy into the grid is techno-economically feasible by 2035. This is critical, because power sector decarbonization can be the catalyst for decarbonization across all economic sectors via electrification of vehicles, buildings, and industry. Owing to the global nature of renewable energy and battery markets, our study indicates the possibility that cost-effective decarbonization can be a near-term reality.

Finally, although this report describes the system characteristics needed to accommodate high levels of renewable generation, it does not address the institutional, market, and regulatory changes that are needed to facilitate such a transformation.

In addition, this study does not explore the details of how new institutions would be developed to support a high renewable electricity system in China. These institutions cover several areas that warrant new research. Key questions for each area for future research are described below.

Electricity demand forecasting

How can long-term electricity forecasts used in infrastructure planning and policy modeling account for the impacts of electrification and demand flexibility on load shapes? Would demand flexibility reduce the need for energy storage? How can uncertainty in electricity demand be best captured in planning and policy studies?

Resource adequacy planning

Which entities should be responsible for long-term planning to ensure that there are adequate resources in the electricity system to meet reliability targets? How should wind, solar, and storage be credited toward resource adequacy? How should resource adequacy mechanisms be designed and enforced? Should resource adequacy be regional or national? How should resource adequacy mechanisms be integrated with spot markets?

Electricity storage policy strategy

What are the ownership, business, and operational models that will be most appropriate to China’s electricity system? What mix of policies and markets can help to rapidly increase the scale of electricity storage?

Offshore wind policy strategy

What technologies, ownership and business models, and approaches to transmission interconnection are most appropriate to China’s offshore wind industry? What mix of policies and markets can help to rapidly increase the scale of offshore wind manufacturing and deployment?

Transition pathways for regional wholesale electricity markets

How can China’s emerging electricity spot markets be consolidated into regional markets? How can China overcome the political challenges to forming regional electricity markets that have frustrated progress toward regional markets in the US?

Emission allowance markets and renewable quota implementation and harmonization

In the nearer term, how can the implementation of China’s cap-and-trade system, along with its emissions allowance trading, and China’s renewable quota system be strengthened? In the longer term, how can these two systems be harmonized to ensure that they remain effective to support national goals and provide consistent incentives?

Integrated land use planning

How can land use planning ensure efficient and fair access to land for wind and solar developers, while minimizing the impacts of wind and solar development on conservation goals and the agricultural sector?

STAR★Methods

Key resources table

| REAGENT or RESOURCE | SOURCE | IDENTIFIER |

|---|---|---|

| Deposited data | ||

| Cost projections for wind, solar and battery technologies | BloombergNEF | https://about.bnef.com/ |

| Data generated for this paper | This paper (supplemental information) | N/A |

| Note: The complete data set could be found upon request. | ||

| Software and algorithms | ||

| Plexos | Energy Exemplar | https://www.energyexemplar.com/plexos |

| Intervention Model for Air Pollution (InMAP) | Spatial Model | http://spatialmodel.com/inmap/ |

| China’s Energy Policy Simulator | Energy Innovation | https://china.energypolicy.solutions/docs/ |

Resource availability

Lead contact

Further information and requests should be directed to the lead contact and corresponding author, Jiang Lin (j_lin@lbl.gov).

Materials availability

The study did not generate new materials.

Method details

Model and scenarios detail

This study draws on intensive scenario building, data development, and power system modeling using detailed, best-available data inputs and state-of-the-art modeling tools. This section provides an overview of scenarios, key inputs and assumptions, modeling tools and approach, and sensitivity analyses, as well as detailed descriptions of methods for the modeling and the development of hourly load, wind, and solar profiles.

Scenarios

The analysis examines two core scenarios: a Current Policy scenario, which is consistent with current policies and technology cost trends in China; and, a Clean Energy scenario, in which 80% of China’s electricity is generated using non-fossil fuel resources in 2035. Sensitivity analyses explore variations on the Clean Energy scenario.

The Current Policy and Clean Energy scenarios differ in three assumptions (Table 1). First, in the Current Policy scenario, we force a net 150 GW of coal generation additions into the model, based on plants currently under construction and some retirement of existing generation.(Based on existing policies and planned coal projects, we include a net 150 GW of new coal generation capacity through 2030. This is consistent with estimated net new additions of 158 GW through 2030 without additional measures from Cui et al. (2022)) In the Clean Energy scenario, we do not force this net 150 GW of coal generation into the model. In both scenarios, the model can build new coal generation as part of least-cost capacity expansion.

Second, the Current Policy scenario assumes that the amount of new wind and solar generation that can be added in any given year is limited in each model year to meet and not exceed the current policy targets and their implied trajectories in 2035. In the Clean Energy scenario, these limits are relaxed and new wind and solar generation capacity additions are instead driven by annual targets for non-fossil generation. Lastly, in the Current Policy scenario, the amount of total non-fossil generation is calculated through least-cost optimization in the model, subject to limits on wind and solar capacity additions based on current renewable policy targets and policy targets for nuclear power and hydropower. In the Clean Energy scenario, the model builds non-fossil generation to meet the following non-fossil generation targets: 46% in 2025, 65% in 2030, and 80% in 2035.

Modeling tools and approach

The state-of-the-art methodology for studies that assess the impacts of high renewable energy penetration on electric power systems is to use capacity-expansion and production cost models. For this study, we use PLEXOS, an industry standard capacity expansion and production cost model, to assess:

-

●

the least-cost (“optimal”) generation mix and inter-provincial transmission investments between 2020 and 2035;

-

●

that meet regional electric power demand requirements, based on grid reliability (reserve) requirements, technology resource constraints, and policy constraints.

The study focuses on model years 2025, 2030, and 2035. For each year, we simulate hourly economic dispatch using the PLEXOS production cost model to ensure that the grid can run reliably for all 8,760 hours in the year, including the hours when the system is most constrained.

PLEXOS uses deterministic or stochastic, mixed-integer optimization to minimize the cost of meeting load given physical (e.g., generator capacities, ramp rates, transmission limits) and economic (e.g., fuel prices, start-up costs, import/export limits) grid parameters. Moreover, PLEXOS simulates unit commitment and actual energy dispatch for each hour (at 1-minute intervals) of a given period. As a transparent model, PLEXOS makes available to the user the entire mathematical problem formulation. The model minimizes total generation cost (fixed plus variable costs) for the entire system, including existing and new generation capacity and transmission networks. We assess the optimal resource mix under a range of scenarios examining deployment rates, coal plant retirements, demand growth, electricity market design, demand response, and supply chain challenges.

Our representation of China’s electricity system in PLEXOS included a detailed rendering of generation resources, generation constraints, unit commitment, and interprovincial and interregional transmission constraints. Figure 12 shows the location of transmission and generation capacity in the Clean Energy scenario, illustrating the level of spatial detail included in the model. We represent the Chinese electricity grid using 32 interconnected nodes, connected using 182 inter-provincial transmission corridors. We assume that the electricity system is balanced and reserves are managed at a regional grid scale, enabling efficient resource sharing among provinces.(The model includes six regional grids: Northwest (Xinjiang, Gansu, Qinghai, Ningxia, Shaanxi, Tibet), Northeast (Liaoning, Jilin, Heilongjiang, East Inner Mongolia), North (Beijing, Tianjin, Hebei, Shanxi, Shandong, West Inner Mongolia), Central (Hubei, Hunan, Jiangxi, Henan, Sichuan, Chongqing), East (Shanghai, Jiangsu, Zhejiang, Fujian, and Anhui), and South (Guangdong, Guangxi, Guizhou, Hainan, Yunnan)).

Figure S1 depicts our overall method and the various data components.

Operational parameters

Operational parameters such as ramp rates, technical minimum levels, auxiliary consumption, minimum up and down times, etc. have been taken from the actual data used in previous China and U.S. studies, regulatory norms, and expert/industry consultations. They are summarized in Table S1.

Heat rates

We use actual heat rate data for every power plant using several sources such as Global Energy Monitor, the World Resources Institute’s Global Power Plant database, SWITCH-China model industry/expert consultations, and previous literature. We model the heat rate as a function of generator loading, meaning that as the power generation from a unit drops, the heat rate will increase. Figure S2 shows the heat rate function used for a new 660 MW supercritical power plant. At loading level of 50%, the heat rate increases by over 5% of the design heat rate at rated capacity.

The study’s health and employment impact analyses were conducted using outputs from the PLEXOS modeling. The health analysis used an adapted reduced-form air quality model, InMAP (Intervention Model for Air Pollution). The employment analysis used Energy Innovation’s China Energy Policy Simulator (EPS), an open-source model that includes an input-output (I-O) framework and uses China’s national income accounts and labor statistics.(EPS is an open-source system dynamics computer model developed to inform policymakers and regulators about which climate and energy policies will reduce greenhouse gas emissions most effectively and with the most beneficial financial and public health outcomes. To calculate employment impacts, we used the model outputs from the two scenarios as inputs into the EPS jobs module alongside data on employment, wages, and labor productivity growth rate in China. The module then calculates relative employment impacts of the two scenarios via an input-output macroeconomic model by determining the impact of policies on individual industries, sorted by International Standard Industrial Classification (ISIC) codes. Full documentation of the mechanics of EPS’s jobs module is available online. See Energy Innovation (2022).) The model measures differences in employment between the Current Policy scenario and the Clean Energy Scenario, calculated in job-years, or one year of employment.

Health impact modeling

A reduced-form air quality model, InMAP-China, and a concentration-response function developed for China are used to quantify the premature deaths caused by ambient PM2.5 concentrations associated with those power plants’ emissions (SO2, NOx, and PM2.5 emissions) in China (Wu et al., 2021; Yin et al., 2017). We respectively calculate the annual average capacity factor of coal and natural gas-fired power plants in each region and estimate the annual emissions from each power plant based on the average capacity factor and emission rates from Yang et al. (2019).

We quantify the premature deaths caused by all sector emissions except for the power sector emissions as the baseline and then quantify the total mortalities from all sectors including the power sector emissions under all proposed scenarios. Therefore, the differences between the baseline and the all-sector mortalities are the premature deaths caused by power plant emissions in China. Population increase is not considered in this analysis and all mortality changes are caused by emission changes.

Table S2 shows that the Clean Energy scenario can help reduce negative health impacts associated with power plant emissions by more than 50% in 2035 due to less generation from the burning of fossil fuels. Figure S3 shows that PM concentrations drop significantly in northern and eastern China under the Clean Energy Scenario in 2035. Due to the high population density, regions like Beijing, Hebei, and Jiangsu enjoy dramatic health benefits from the Clean Energy scenario.

Employment impact modeling

Changes in clean energy deployment and spending

We used output data on clean energy technology deployment and demand from the capacity expansion model and a customized version of the China Energy Policy Simulator (China EPS) to estimate employment impacts. To do so, we hard coded the outputs from the capacity expansion modeling into the input-output model embedded in the China EPS. Impacts are expressed as a difference between the Current Policy and Clean Energy scenarios, not an absolute change from 2020-2030, isolating the impact of an 80% clean electricity policy on employment.

Input-output modeling

Estimates of labor impacts from clean energy policies in China are made using an embedded input-output (IO) macroeconomic model in the China EPS. The IO model receives data from other parts of the model on changes in cash flows for capital, fuel, maintenance, labor, etc and flows these through a typical IO model structure to estimate changes in direct, indirect, and induced economic impacts. Macroeconomic feedbacks are accounted for on a single year delay. More information on the IO model embedded in the EPS can be found online here: https://us.energypolicy.solutions/docs/io-model.html.

Key parameters

The IO model is populated with publicly available data, much of which comes from the Organisation for Economic Co-operation and Development (OECD). Key input data include business-as-usual employment, output, and value added, estimates of the Domestic Leontief Inverse Matrix (which relates outputs from an industry to the inputs required to produce output and is used to estimate indirect effects), and labor productivity growth rates. Labor productivity in particular has a very strong effect on the magnitude of employment impacts, and several scenarios were assessed for this modeling.

Labor productivity growth rate estimates

We evaluated three different scenarios for labor productivity growth in China in this analysis:

-

●

Holding constant productivity at today’s levels (Zero Future Growth Scenario)

-

●

Continued growth in productivity based on the greatest amount of historical data dating back to 2000, while looking at manufacturing as a whole (Maximum Historical Growth Scenario)

-

●

Continued growth in productivity based on the greatest amount of historical data dating back to 2000 but looking at individual industries within the manufacturing sector (Maximum Growth with Manufacturing Industries Scenario)

The employment results in the main text of this report represent this final scenario, and use both the sector-by-sector labor productivity growth rate index based on historical data shown in Figure S4, with the manufacturing broken down by industry as shown in Figure S5.

In the Zero Future Growth Scenario, we assumed no incremental productivity growth beyond today’s productivity. This scenario should be viewed as an upper bound on potential employment impacts, because future labor productivity gains (or losses) are not accounted for, and changes in spending therefore yield larger changes in employment than in other scenarios. There is a net gain of 4.3 million job-years in this scenario, with 13.1 million job-years gained overall sectors, 5.3 million job-years lost in the coal mining sector, and 3.4 million job-years lost in all other sectors combined, as shown in Figure S6.

In the Maximum Historical Growth Scenario set, we relied on as many years of data as possible back to 2000 to produce future growth estimates. There is a net gain of 1.2 million job-years in this scenario, with 4.1 million job-years gained overall sectors, 1.7 million job-years lost in the coal mining sector, and 1.1 million job-years lost in all other sectors combined, as shown in Figure S7.

In the Maximum Growth with Manufacturing Industries Scenario, used in the main text of this report, we similarly relied on as many years of data as possible but used growth rates for individual manufacturing industries as available, as seen in Figure S5. There is considerable differentiation among industries, which is reflected in this dataset.

Electricity demand

Growth in China’s electricity demand over the next 15 years is highly uncertain. It will depend on the structure and pace of economic growth and the pace of electrification in the transportation, industry, and buildings sectors. In this study, we based our electricity demand projections on the 1.5°C scenario in Tsinghua University’s 2020Low Carbon Development Strategy and Transition Roadmaps Study, which captures expected changes in China’s electricity demand needed to meet a global 1.5°C warming target (Institute of Climate Change Sustainable Development, 2020). Figure 13 (See also Table S3) shows electricity demand projections used in this study relative to projections in other recent studies.

Drawing on publicly available provincial electricity demand data, we converted national annual electricity demand into 31 provincial hourly load shapes, which matches the hourly timescale used in the PLEXOS modeling. Our approach assumed that provincial system load factors decline over time, resulting in a national coincident peak demand (1,992 GW in 2035) that grows just over 1.5 times faster than energy demand during the next 15 years. (System load factor is the ratio between average and peak electricity demand. Declines in system load factor are consistent with reductions in the share of industrial electricity demand, which is consistent with recent trends in China. For capacity expansion, the modeling assumes a 15% planning reserve margin. The analysis does not attempt to incorporate changes in load shapes that would result from electrification or more responsive demand; this is an important area for future research).

Provincial hourly load shapes

Hourly electricity demand data is not publicly available in China. To generate hourly provincial load shapes, we used publicly available data and an algorithm that disaggregates national electricity demand into hourly load profiles by province. These data include:

-

·

National long-term load forecasts, based on policy and academic studies;

-

·

Provincial shares of national electricity demand, based on a historical base year (2019);

-

·

Monthly provincial generation shares, based on a historical base year (2019);

-

·

Typical weekday and weekend/holiday load shapes by province, based on data from the NDRC.

Our disaggregation algorithm has four main steps.

Step 1: Disaggregate a national annual electricity demand forecast into provincial annual electricity demand forecasts

First, we disaggregate a national annual electricity demand (TWh/yr) forecast into provincial energy demands (PLiy for province i) by multiplying a national load forecast in year y (NLy) by forecasted provincial shares of national demand in year y (αyi)

The national electricity demand forecast, and by extension provincial forecasts, are for total electricity demand, including transmission and distribution losses, generator own-use, and behind-the-meter generation.

To be consistent with the level of expected electricity demand required to meet longer-term GHG emission reduction goals in China, we use as our base forecast the electricity demand projections from the 1.5°C scenario in the Institute of Climate Change and Sustainable Development’s (ICCSD’s) 2020 Low Carbon Development Strategy and Transition Roadmaps Study, with linear interpolation to fill in missing years. Table S3 shows the ICCSD forecast relative to other projections of long-term electricity demand in China.

Provincial shares of national electricity demand will change over time, as a result of changes in population and economic structure. Changes in economic structure are difficult to account for; we are not aware of any long-term forecasts of provincial GDP in China that have sectoral detail. Longer-term provincial population forecasts are more widely available.

To forecast αyi, we multiply base year provincial per capita electricity consumption (ECi) by long-term provincial population (PPyi) forecasts from Chen et al. (2020) (SSP2 scenario), and then calculate αyi by dividing values for each province by the sum of all provinces.

As Table S4 shows for 2035, changes in provincial shares of national electricity demand change only slightly relative to 2019.

Step 2: Disaggregate provincial annual electricity demand forecasts into provincial monthly electricity demand forecasts

We disaggregate annual provincial electricity demand (PLyi) into monthly provincial demand (PLmyi) using historical (2019) shares of monthly demand (βmi)

where

Data (2019) for βmi are from the Statistical Yearbook series.

Step 3: Disaggregate provincial monthly electricity demand forecasts into provincial hourly electricity demand forecasts

We disaggregate provincial monthly electricity demand to provincial hourly demand using typical weekday and weekend/holiday load shapes by province, published by National Development and Reform Commission and National Energy Administration (2021). This disaggregation involves two sub-steps: (1) calculating daily electricity demand for weekdays and weekends/holidays in each month; and, (2) multiplying daily electricity demand by normalized hourly load shapes.

We estimate provincial daily electricity demand for weekends/holidays (WEmyi) and weekdays (WDmyi) using the ratio of weekday and weekend/holiday consumption (θi for province i) from the NDRC load shapes and the number of weekends/holidays (DE) and weekdays (DD) in each month. For weekends, daily electricity demand is

where

The value of θi is estimated from the daily totals of the NDRC typical weekday and weekend/holiday load shapes.

For weekdays, daily electricity demand is then:

For each hour on weekdays and weekends/holidays, we calculate electricity demand using daily weekday and weekend/holiday loads and normalized shapes based on the NDRC load shapes. For each weekday, the hourly load shape (PLWDhmyi) is

where the normalized load shape coefficients (φWDhi) are calculated using the NDRC typical weekday load shapes (LNWDhi)

For each weekend/holiday, the hourly load shape (PLWEhmyi) is similarly:

Each weekday and weekend/holiday in a given month will thus have the same hourly values. We calculate annual hourly load shapes for each province by matching these hourly values to weekdays and weekends/holidays in each month in a given future model year (2025, 2030, 2035). We adjust holiday dates to match the future year.

Step 4: Adjust provincial hourly electricity demand forecasts to match a peak demand forecast

The provincial hourly electricity demand forecasts that result from steps 1–3 will be consistent with forecasted energy (TWh) demand but will generally not match peak (GW) demand. To reconcile the provincial hourly electricity demand forecasts with peak demand, we use a novel adjustment technique that scales the highest demand hour in a load duration curve (LDC) to match peak demand and pivots the rest of the LDC to ensure that the total area under the LDC matches total annual electricity (energy) demand.

To obtain the final LDC (FLhy), the initial LDC in hour h (ILhy) is adjusted by a peak adjustment factor (ωy in year y) and a scaling factor (γy):

where ωy is the ratio between a peak load estimate based on a target system load factor (SLFy in year y) and the maximum value implied by the provincial load shapes above (max[PLhmyi])

The scaling factor is:

The NDRC load shape data also includes a highest load and lowest load day, though it is not clear what these data represent; for instance, are they total electricity generation, inclusive of transmission and distribution losses, generator own use, and behind-the-meter generation (全社会用电量) or are they only end-use consumption? To ensure consistency, we use the maximum value in our load shapes in 2019 as a base year peak demand value and increase peak demand over time by using an algorithm for system load factor (SLF) declines.

Our algorithm for SLF declines assumes that provincial SLFs decline by 10% by 2025, 15% by 2030, and 20% by 2035, relative to the implied peak in the hourly load shape (PLWDhmyi). We use 50% as an SLF floor for all provinces. These assumptions lead to a roughly 20% decline in the average national SLF by 2035. Table S5 shows estimated SLFs provincial and national SLFs in 2035 and, for reference, 2019.

Technology and fuel costs

The PLEXOS model requires extensive resource cost inputs, among which the most important are wind, solar, and battery storage technology costs and coal fuel costs.(We included several technologies in the capacity expansion analysis: coal generation, gas generation, large-scale hydro generation, nuclear generation, solar generation, onshore and offshore wind, 2/4/8-hour battery storage, and pumped hydropower storage. For simplicity, the analysis does not include biomass generation, concentrated solar power (CSP), or geothermal. These resources have challenges around cost-effectiveness and scalability.) The analysis used projections of installed costs and fixed operations and maintenance (O&M) costs for onshore wind, offshore wind, solar PV, and 4-hour battery storage in China from Bloomberg New Energy Finance (BNEF), shown in Figure 14 (See also Table S6). The model also considers 2-hour and 8-hour duration battery storage; cost declines for these technologies are similar to those for the 4-hour battery shown in Figure 14. In cost and technology inputs, we do not make an explicit distinction between distribution- and transmission-connected resources. (Because we do not model intra-provincial transmission, from the perspective of the model, distribution- and transmission-connected resources look the same from an operational perspective. We did not have sufficient detail on land costs and incremental distribution and transmission costs to more meaningfully assess the tradeoffs between utility-scale and distributed resources.).

Longer-term coal price trends in China are highly uncertain. Coal prices rose to record levels in 2021 but are expected to moderate over time. Lower coal demand, consistent with national policy and the results of this study, would tend to decrease prices, but lower prices would tend to reduce supply, keeping prices closer to marginal production and transport costs. In this study, we assume that provincial thermal coal prices remain constant in real 2019 yuan terms over the study horizon, which means that coal prices increase at the rate of inflation.

The Current Policy and Clean Energy scenarios use the same technology cost and fuel cost assumptions. Table S7 provides assumptions on conventional technology (coal, nuclear, natural gas, and hydro) capital and fixed O&M costs, which have been taken from multiple sources including Bloomberg, He et al. (2020), and industry consultations.

New investments

PLEXOS outputs total capital investment in new generation and transmission assets starting in 2020. We annualize the investment costs by using a real weighted average cost of capital (WACC) of 5% and technology-specific assumptions for economic lifetimes (see Table S8). PLEXOS also outputs the total operations and maintenance (O&M) costs (fixed and variable) and fuel costs of the existing as well as new generation capacity.

Existing assets

PLEXOS does not report the investment cost of generation capacity built before 2020, which we estimate exogenously. First, we assess the undepreciated value of generation assets built before 2020, using data from the WRI global power plant database for plant level commissioning dates. For conventional as well as renewable technologies, we use the capital cost assumptions, shown previously, to assess the total value of each generating plant during the commissioning year. We then apply a straight line depreciation method to estimate the remaining economic value for every generation plant, assuming an economic life of 30 years for all technologies except batteries. For batteries, we use an economic life of 15 years. We use the average WACC of 5% (real), to annualize these costs of the existing capacity and then add them to our total costs.

Fuel prices

In case of coal, we use province level monthly average coal prices delivered at power plants in the year 2019 (Figure S8). In order to be conservative, we assume that coal prices remain the same in real 2019 terms through 2035. In case of gas, we assume a flat price of $8/GJ between 2020 through 2035 based on the actual 2019 prices.

Solar and wind profiles

For this study, we estimated wind and solar resource potential and developed detailed solar and wind profiles for each province in China, using a two-part approach. First, we estimate the resource potential, or the maximum solar and wind capacity that can be installed in a province. We use average annual capacity factors from Global Wind and Solar Atlas and multiple exclusion criteria to estimate this potential. Exclusion criteria include elevation, slope, landcover, and ocean depth. Second, we develop detailed hourly generation profiles, using meteorological data from reanalysis datasets and simulating site level wind and solar generation using NREL’s System advisor Model (SAM). Wind and solar farms can be designed in SAM and hourly generation can be estimated by passing meteorological data through it. We then use an aggregation algorithm to combine hourly generation from multiple sites in a province and create a representative province wind and solar resource profile.

Resource potential

Solar