Abstract

Recently, financial service systems have had essential impacts on public policies, the economic performance of firms, and all forms of industry and commerce. These systems play an important role in determining whether a society (which includes a wide range of members, from governmental institutions to individual consumers) has been successfully considered an environmentally sustainable path. The literature shows that the people who work in the financial sector are mostly unaware of the pressure and rationale behind sustainable development and its bearing on their work; however, those who work in the relevant research and policy areas generally ignore the vitality of the role of the financial sector in such a development. The study of interval-valued Pythagorean fuzzy sets (IVPFSs) indicates an urge for a decision approach to implementing the available information for rational decisions properly. Inspired by the advantage of IVPFSs, an extended decision methodology called the IVPF rank-sum weighting method (RSWM)-double normalization-based multi-aggregation (DNMA) is discussed. In this line, the IVPF-RSWM is applied to find the subjective weights of digital transformation challenges of sustainable financial service systems (SFSS), and the DNMA framework is developed to obtain the preferences of SFSSs in the banking sector. A case study to assess the main digital transformation challenges in SFSSs of the banking sector is undertaken. Further, comparison and sensitivity investigations are taken to illustrate the advantage of the presented approach.

Keywords: Digital transformation, Sustainable financial services, Sustainable development, DNMA, Interval-valued Pythagorean fuzzy sets, Rank-sum method

Introduction

Climate change has many economic implications that could result in a great transformation in financial services (Bopp, 2020). Indeed, this phenomenon is at the top of the business agenda among numerous issues that are critical to the financial industry. By considering the association between the financial sector and “sustainable development (SD),” at least three significant aspects must be taken into account. First, the financial sector can affect the environmental and sustainability aspects of the clients, e.g., projects, debtors, and investees (Thompson & Cowton, 2004; Weber, 2014), which is considered the indirect influence of this sector on sustainable development. Evidently, the indirect influences of finance are of high importance as access to capital is generally a key premise for being successful in business. Then, in a lot of ways, regulations related to environmental issues have influenced and still affect the financial sector (Weber et al., 2010). For example, environmental regulations in regard to the pollution of water, soil, and air have affected the ways environmental risks were managed in credit risk management during the 1990s (Boyer & Laffont, 1997). The numerous opportunities and risks associated with sustainability (for instance, alleviation of poverty and climate change) have increased and are still arising, which need to be addressed well by the financial sector (Richardson, 2009). On the other hand, it should be noted that the financial sector has often been reactive rather than proactive regarding such sustainability challenges. Third, the pressures exerted by stakeholders with a focus on SD affect the reputational risks of financial institutions (Evangelinos & Nikolaou, 2009) and their financial performance (Scholtens & Zhou, 2008).

The field of “information systems (ISs)” has created the analytical/theoretical frameworks addressing the transformational impacts that may be exerted due to diffusing, integrating, and implementing the “information technologies (ITs)” on intricate business ecosystems (Hirschheim and Klein, 2012; Werth et al., 2020). From the primary computer systems to the latest “digital technologies (DTLs),” e.g., “social, mobile, analytics, cloud and internet of things (SMACIT)” technologies (Sebastian et al., 2020), the promptness and degree of technological innovations have set the pace of “digital transformation (DT)” in services and industrial sectors. They have led to scientific discourse in the domain of business and IS research (Kutzner et al., 2018). Digital transformation was described by Vial (2019) as a process through which DTLs cause some disruptions triggering strategic responses from the companies seeking to adjust their paths for value creation and, at the same time, managing the structural changes and organizational obstacles influencing both positive and negative concerns of such transformational process. Accordingly, the disruptive impacts resulting from digital transformation could be taken into account as the direct consequence of the second-order technological disruptions induced by the aggregated effects of multiple digital innovations upon economic, social, and political norms (Schuelke-Leech, 2018). Technologically, digital innovation could appear in the form of novel digitalized products or service innovations, business or technical process enhancements, innovative digitally driven business models, and digital business strategies that are based on the latest paradigms of value creation (Hess et al., 2020). Due to the high significance of the influence of digital transformation on companies, societies, and industries, in the past decade, it has attracted lots of attention from scholars working in different fields. Some prominent examples in this regard are sustainability (Feroz et al., 2021; Pamucar et al., 2022), COVID-19 (Iivari et al., 2020) and healthcare (Kraus et al., 2021), supply chain finance (Henriette et al., 2015; Kamaci and Petchimuthu, 2022; Mahmoudi et al., 2022), strategy and organizational change (Hanelt et al., 2021; Khan et al., 2021), and IT (Papagiannidis et al., 2020).

Various researchers in the management domain have investigated the challenges the industry incumbents face when innovating their businesses (Eklund & Kapoor, 2019). In particular, the industry of financial services is currently experiencing a fundamental transformation. The formerly stable market reveals extraordinary competitive dynamics, regulatory changes, and non-/near- banks as asymmetric competitors in the digital technologies era. Practitioners mention a disruptive change that is able to lower the significance of conventional financial service providers. This has been recently exemplified by (Dehnert, 2020), who focused on future industry perspectives in regard to profitability measures. The study of (Chiorazzo et al., 2018) was concentrated on the digital transformation of incumbent financial service providers that had three criteria: high market power, revenue streams from conventional services, and physical branches (Chiorazzo et al., 2018). Insurance firms and incumbent banks have significant roles in the sustainable development of society. Such importance is due to the fact that there are numerous significant economic functions, e.g., the promotion of saving and wealth formation and the credit supply to the economy.

Financial service providers are traditionally concerned about B2C retail businesses with four main product types, i.e., payment, financing, investment, and insurance (Alt & Reinhold, 2012), with two key subsectors, i.e., banking and insurance. The former involves transferring, accumulating, increasing savings, and providing capital, while the latter primarily implies transferring and managing the risks. From the traditional perspective, financial services are the least interesting products, making it difficult to differentiate among them. On the other hand, digitalization makes customer orientation a key aspect of the competition (Bons et al., 2012). New digitally enabled competitors position themselves with various digital products that are standardized and easy to handle. With a decrease in switching costs, consumers will be able to select from among the offers given by both conventional and new financial service providers for their accounts, loans, payments, investments, mortgages, or insurance products, which questions their former robust, trust-based relationship with their financial service providers (Pousttchi & Dehnert, 2018).

The ICT has enabled the “digital transformation (DT)” of financial services as well as the development of Fintech, which have resulted in not only the enhancement of the resources available in service systems (for instance, resource “density”) but also their transferability. This has led to novel technology-empowered value co-creation processes (Breidbach & Maglio, 2016). Owing to the recent developments in technology, the prevalent effects of ICT on financial services are no more surprising, and the investigation of the ICT implications in services represents more broadly a key service research priority (Ostrom et al., 2010, 2015). On the other hand, the current contributions in the service research discipline have been questioned due to the fact that they could not offer deep insight into the emergent digital service innovations (Lusch & Nambisan, 2015) in general, and also they could not offer a deep understanding about Fintech as an evolving service context, in particular (Breidbach & Ranjan, 2017). For example, Bharadwaj (2000) stated that companies with high levels of IT capabilities could perform better than the control sample of companies regarding various profit- and cost-based performance measures. However, Chae et al. (2014) stated that there is not any considerable association between IT capabilities and such measures. For example, Aral and Weill (2007) maintained that the total IT investment of a company is not associated with PERF; though, investments in definite IT assets consistent with their strategic purposes are able to explain the performance differences. It should be noted that the findings of more recently conducted studies have suggested that digital transformation mediates the relationships between PERF and IT investments (Nwankpa & Roumani, 2016). Particularly, findings of some studies showed that DT largely and positively affects different factors such as FSP PERF in the long term (Scott et al., 2017), organizational agility (Ravichandran, 2018), and productivity (Bertoni & Croce, 2011). In another study, DeYoung et al. (2007) showed that DT has a positive association with community bank profitability. A recurrent finding indicates that specific configurations are vital to PERF (Ray et al., 2005). Such a gap in the knowledge is partially due to the fact that ICT and service research have been carried out conventionally in disciplinary silos (Brust et al., 2017), which is further amplified due to the high speed of the emergence of innovative innovation, disruptive technologies (Christensen, 2006).

Because of the impreciseness of knowledge, the vagueness of human beings’ minds, time limitations, and the absence of required information, the assessment, and ranking of suitable DT challenges in “sustainable financial service systems (SFSSs)” of the banking sector is an important and uncertain “multi-criteri decision making (MCDM)” issue faced by the hospitals and medical centers. To the best of our knowledge, no researcher has yet proposed an integrated “rank-sum weighting method (RSWM)” and “double normalization-based multiple aggregation (DNMA)” method under the “interval-valued Pythagorean fuzzy sets (IVPFSs)” environment in order to assess the DT challenges that arise in SFSSs of the banking sector. The IVPFSs are more capable compared to “intuitionistic fuzzy sets (IFSs),” “interval-valued intuitionistic fuzzy sets (IVIFSs),” and “Pythgorean fuzzy sets (PFSs)” in managing the vagueness and inaccuracy observed in many actual MCDM problems. This motivates to consider the IVPFSs context for the assessment of DT challenges in SFSSs of the banking sector. Moreover, the literature lacks research studies on SFSS from theoretical, managerial, and societal perspectives, and no study has yet systematically identified the research challenges related to this domain. In the present paper, we consider filling this gap by defining a clear agenda for service research with the aim of examining the DT challenges of SFSSs. Therefore, the present research attempts to determine the key challenges that may arise with the DT of sustainable financial services, discuss and compare the empirical findings reported in the literature, and define a plan for future service researchers. First, it provides a realistic contribution by identifying 18 key challenges related to the DT of financial services. This new conceptualization of challenges related to sustainable financial service systems (SFSSs) has contributed to the current discourse in regard to the role of ICT in financial services in general and the influence of DT upon these services in particular. In this study, we have developed the DNMA approach to select the most appropriate DT challenges in SFSSs of the banking sector alternative with IVPF information. Furthermore, this research discusses the integration of the RSWM and DNMA methods over IVPFSs. The contributions of the paper are given by.

We identified the main challenges to implementing DT in SFSSs using a survey study based on “decision experts (DEs)” and a current literature review.

To develop a comprehensive framework to evaluate DT challenges in SFSSs of the banking sector.

To analyze and evaluate the DT challenges in SFSSs of the banking sector using an extended IVPF-RSWM-DNMA approach.

The rank-sum weighting method (RSWM) is applied to evaluate the significance/weight value of different DT challenges in SFSSs of the banking sector.

To evaluate and rank the sustainable financial service systems (SFSS) of the banking sectors, the DNMA method is extended to IVPFSs.

The rest of the work is prepared as follows: Sect. 2 confers the review of the financial services industry and digital transformation in sustainable development. Section 3 presents the elementary notions and novel IVPF-RSWM-DNMA method. Section 4 demonstrates the developed framework by a case study of DT challenges in sustainable financial service systems of the banking sector. It also illustrates the comparative discussion with extant models and sensitivity investigation with different utility parameter values. Section 5 concludes and recommends further research of the study.

Literature review

The financial services industry and sustainable development

It is not easy to achieve commercial success within the current extremely competitive setting of the financial services sector (Asif & Sargeant, 2000). The last bastion of competitive advantage is effectively meeting the consumers’ requirements. A growing realization indicates that the most important point in the development of sustainable competitive advantage is becoming customer driven (Bennett, 1992). Those companies that succeed in the provision of quality services for their customers are considered the companies with a great opportunity for gaining success in such a competitive market. In modern societies, banks and insurance firms typically provide financial services (Dehnert, 2020). Both above-noted sectors share a number of functional similarities, which involves the risk transformation function. To start with, banks resolve various risk proclivities of debtors and investors in the credit and investment function, although the insurance business model involves identifying and calculating risk and balancing in underwriting procedures. Next, due to the maturity transformation function, banks are capable of reconciling various maturity interests of creditors/debtors, while specific insurance firms carry out savings and deposit businesses as well, e.g., life insurers. Finally, the customer service function distributes complex financial products through customer advisory services.

Within the financial sector, the first activities are mostly focused on managing the internal environment (Jeucken & Bouma, 1999). The undertakings to decrease the direct environmental effects lead to a number of positive public reputations (Babiak & Trendafilova, 2011); although the most important connection between sustainable development and the financial division is indirect, it is through lending or investing in insurance, or project finance (Scholtens, 2008). As a result, as a subsequent step, this sector gets focused on the management of environmental risks in their business through the integration of the assessment of sustainability risks into their credit risk management procedures (Evangelinos & Nikolaou, 2009).

Environmental risks and regulations considerably affect the risk of a credit portfolio of a bank; thus, they need to be perfectly managed (Weber et al., 2008). This is also the case for insurance since this sector also requires managing environmental risks. After the advent of “socially responsible investment (SRI)” products and services, financial institutions started to affect SD over their core business (Cerin & Scholtens, 2011). While on the one hand, environmental insurance is necessary (Weber et al., 2014), on the other hand, the market for environmental liability insurance is comparatively risky since environmental regulations suffer typically from uncertainty (Abraham, 1988). As it is widely acknowledged, in comparison with banks, insurance is more susceptible to environmental risks, although the influence of the insurance sector on SD is still rather indirect. It delivers insurance for its clients’ projects; however, banks directly affect SD (Scholtens, 2011). Insurance has a limited opportunity to affect its clients’ sustainability performance.

Recently, digital transformation has attracted much attention from scholars working in different domains such as marketing, business, management, ITs, and ISs. The growth in “information and communication technologies (ICTs)” has greatly affected companies and organizations. The changes that occurred to conventional business ecosystems have led to the creation of novel business environments termed generally as “digital business ecosystems.” Changes that occurred to business ecosystems have influenced the strategic decisions of organizations, which are generally made in relation to both external and internal environments. The frequency and size of such changes have caused the concept of change to be of higher meaningfulness (Emre & Ayberk, 2020). The quick growth of technology and various changes to current global markets have magnified a novel cooperative adaptation process. Such DT and the use of innovative technologies have raised many questions in regard to the changes that conventional firms, management practices, and strategies required to use to give suitable responses to them (Hess et al., 2016). Such response includes the formation of novel business models and/or enhancements to the currently used business models using digital technologies (Stjepi et al., 2020).

Financial service providers must focus on several daily challenges during their business activities. In recent years, several studies have been carried out with a focus on digital transformation and the subsequent risks from both practical and theoretical perspectives (Bohnert et al., 2019). There is a robust connection between the respective firms and their customers on the basis of trust and long-term connections; this is the case for both banking and insurance sectors (Boot, 2000; Csiszar & Heidrich, 2006). Moreover, the financial market has encountered fundamental innovations mostly due to the quick enhancements in technical possibilities and delivery networks (Bömer & Maxin, 2018). Several innovative technologies such as “big data analytics (BDA),” Robo-advisory, and “artificial intelligence (AI)” provide novel opportunities for firms to give support to their current business processes and customers. Such technologies can create/enhance novel financial services to meet the changes occurring in consumers’ needs (Keller et al., 2018). However, digital advances have fostered sales of financial services via digital channels (for instance, online platforms); they have provided challenges and opportunities to both firms and consumers. Nowadays, new competitors are moving continuously into the market. Through innovative business models, InsurTechs, FinTechs, or global Internet giants such as Facebook, Google, and Amazon (also termed BigTechs) have threatened incumbent firms (Arner et al., 2016), which show different reactions toward such new competitors.

In comparison with other industrial sectors, the financial sector is less exposed to stakeholders’ pressures (Qian et al., 2020) or the regulations about community, environment, or labor issues (Ertugrul & Hegde, 2009). However, numerous companies in the financial sector are on the radar of nongovernment institutions over financing projects or borrowers with businesses that can damage SD and the natural environment (Noor & Syumanda, 2006).

The financial sector primarily consists of insurance, banking, and asset management; banking and asset management are typically offered jointly. Various conventional products offered by insurances and banks have complementary and substitutive characteristics (Liu & Lee, 2019). In spite of the obvious converging impacts between insurances and banks, Beltratti and Corvino (2008) highlighted the fundamental differences that exist between the two business models. These differences are mainly connected to demography (for instance, sales channels, regulations, and accounting), the scale of operations, and the liability structure. Such differences form the relevance and speed of their digital transformations in the financial sector. Currently, the literature consists of a few studies systematically analyzing the impacts on the processes and the influence of leveraging digital technologies in this sector. The study of (Cziesla, 2014) is one of the few integrative studies on this issue, which performed a meta-analysis of the extant literature that is relevant to digital transformation.

The financial market exerts a governing impact upon the whole economy, society, and sustainable development through its activities (Choi & Wang, 2009). The financial market plays an intermediate role in distributing capital into various sectors, markets, projects, and regions; this market might prefer to be concentrated on financial derivatives. The consequence of the robust impacts of the financial industry upon society and the economy was observed in the last financial crisis. During this crisis (at least one of the key reasons), academic studies were focused on the influences of the financial sector on societies and sustainability practices. In this context, “sustainability” is generally described as a development that satisfies the present generation’s requirements without compromising the future generations’ requirements (Brundtland, 1987). Sustainability is characterized not only by this intergenerational aspect but also by intra-generational equity between north and south (Barkemeyer et al., 2014) and by taking into account both societal and environmental aspects of development (Vifell & Soneryd, 2012).

Digital transformation in the sustainable financial services sector

The sector of financial services, as mentioned earlier, comprises different main components, i.e., banking asset management. DT greatly impacts financial services since digital technologies have changed businesses in three dimensions: value creation, value proposition, and customer interaction (Pousttchi & Gleiss, 2019). The “value creation model (VCM)” shows how DT affects the way the products/services in the financial services sector are created (Pousttchi et al., 2019). It necessitates some essential processes for the execution of various business functions, e.g., maturity, risk, or information transformation. Scientific studies have classified the empirical elements of the business models influenced by DT from a variety of perspectives, such as customer orientation (Gimpel et al., 2018).

The all-inclusive concept of DT encompasses technologies as well as organizational and strategic changes (Diener & Špaček, 2021). Such transformation is due to the growth of technology, the advent of innovative business models, and alterations to customers’ expectations (Omar, 2016). Nowadays, a number of definitions of “digitalization” are generally acknowledged. This term is a complex issue encompassing a number of areas such as shifts in thinking, alterations to leadership, technology adoption, resources digitalization, and innovation acceptance (Francis et al., 2018). Note that there is a difference between “digitalization” and “digitization.” While the former addresses the influences of digital technologies on the organization, the latter signifies the shift from analogous solutions to digital solutions. In fact, digitalization refers to organizational revitalization by means of ICT (Hensmans, 2020).

A set of barriers seems to block the DT, hindering or destroying the whole process. Nevertheless, DT can resolve the challenges and problems the banks presently face. The principal practices of DT, e.g., digital trends, leadership, digital strategies, DT skills, “digital technologies (DTLs) adoption, and a “customer-centric approach (CCA),” are the influences that are noted to endure on digital maturity levels (Lotriet & Kokotwane Dltshego, 2020). The term “digital transformation (DT)” is often misunderstood as simply deploying state-of-the-art ICT. Technological investment entails some risks and requires understanding the relationships between technological and organizational culture and institutional modifications within some definite boundaries of regulatory procedures. DT should not be understood as a definite, simple, and/or predictable process. Rather, this process could be disruptive or transformative, with irreversible effects on associated organizational outcomes in relation to technical capabilities and behaviors (Krasonikolakis et al., 2020).

Digitalization has made important contributions to the sustainable development objectives of the United Nations. Only the transformation of prevailing businesses could help to solve the economic and environmental challenges of the future in a sustainable way (Bican & Brem, 2020). Digital transformation generates novel social groups—partly human, semi-human, or nonhuman. Some of these groups already exist, and some could be predicted to exist soon because of the latest advances in fields such as software engineering, brain wearables, and robotics. The growth of our dependency on digital services and tools could bring about a number of challenges to both organizations and human beings (Fekete & Rhyner, 2020). According to Forcadell et al. (2020), digitalization may cause some challenges that can hamper its potential benefits and compromise its survival. This is why corporate sustainability plays a noteworthy role in putting digitalization into effect. This can compensate for the disadvantages of digitalization. Particularly, integrating digitalization with corporate sustainability could help to transform the organizational nature of banks by simultaneously narrowing their boundaries and expanding their scope. El Hilali et al. (2020) called for further attention to imaginable ways to achieve sustainability in the course of DT. Based on their findings, firms can achieve sustainability by effectively considering the customers, data processing, and innovation. However, they did not prove the considerable role of competition in the enhancement of the firms’ commitment to sustainability. It was also endorsed partly in the study of Ordieres-Meré et al. (2020), where they showed the positive impacts of knowledge creation that could be facilitated by directly or indirectly applying digitalization. Technology has been found a factor capable of disrupting the financial industry, solving friction points for customers and businesses, and injecting more resilience and sustainability into the overall business. In addition, sustainable financial technology could have a great contribution to the stability of the financial system (Moro-Visconti et al., 2020). According to above discussions and current literature review, to evaluate the DT in SFSSs, 18 challenges are identified, i.e., understanding of the customers through big financial data (c1), knowledge for open data for value co-creation (c2), understanding changing role of traditional financial intermediaries (c3), integrating the multi-platform services (c4), improving platform orchestration (c5), investigate the platforms and markets (c6), managing the experience and quality of digital financial services (c7), knowledge for new value creating resource configurations (c8), understanding hybrid business models (c9), facilitating the co-creation of value without intermediaries (c10), understanding value co-creation with cryptocurrencies (c11), adaptable infrastructure of financial services for cryptocurrencies (c12), regulating value co-creation without intermediaries (c13), rules and regulations of financial institutions (c14), managing the deregulation of financial service systems (c15), designing customer-centric fintech services (c16), designing communities of practice (c17) and developing support systems (c18).

Research methodology

To address the concerns explained above, the “Pythagorean fuzzy sets (PFSs)” theory was proposed by Yager (2014) for the purpose of handling the uncertain or vague information that needs to be dealt with when solving an MCDM problem. Yager (2014) demonstrated the case where decision experts determine the value to which alternative Ri meets the attribute Cj is , and the value to which alternative Ri invalidates the attribute Cj is In such a situation, we note that and as a result, “intuitionistic fuzzy sets (IFSs)” are not able to solve the problem. As this condition could be tackled systematically by PFSs. Accordingly, PFSs can model various MCDM problems that are not solvable with the help of IFSs. To choose a suitable conversion method and upgrade the “agriculture residues-to-energy (ARE)” sectors, Rani et al. (2021) combined PFSs and “weighted discrimination-based approximation (WDBA)” with a new approach. Mishra et al. (2022a) presented an “ additive ratio assessment (ARAS)” model on PFSs for handling the sustainable biomass crop assessment problem. Further, the PFSs were generalized by Peng and Yang (2016) to “interval-valued Pythagorean fuzzy sets (IVPFSs).” An IVPFS, as an extended model of PFS and “interval-valued intuitionistic fuzzy set (IVIFS)” (Mishra et al., 2022b), could be more widely utilized to MCDM problems, including the selection of sustainable suppliers and evaluation of products. An innovative method, termed as “IVPF-stepwise weight ratio assessment (SWARA)-multi-objective optimization by ratio analysis with full multiplicative form (MULTIMOORA),” was introduced by He et al. (2021) for investigating the present status of “sustainable community-based tourism (SCBT)” in the context of Indian Himalayan area. Al-Barakati et al. (2022) gave the “weighted aggregated sum product assessment (WASPAS)” model based on similarity measure for ranking the “renewable energy sources (RESs)” on IVPFSs. Mishra et al. (2022c) discussed the IVPF “complex proportional assessment (COPRAS)” model for treating the “waste-to-energy (WTE)” methods for “municipal solid waste (MSW)” treatment. First, we present the concepts of the PFSs and IVPFSs. Second, we discuss an integrated approach called “IVPF-RSWM-DNMA” for treating MCDM problems.

Preliminaries

Some concepts of PFSs and IVPFSs are as follows:

Definition 1 (Yager, 2014)

A PFS on discourse set is defined by

| 1 |

where and are the “belongingness degree (BD)” and “non-belongingness degree (NBD)” of to respectively, with the condition Next, the hesitancy degree is given as

Definition 2 (Zhang, 2016)

An “interval-valued Pythagorean fuzzy set (IVPFS)” on Z is defined as

| 2 |

where and

Here, and imply the interval-valued BD and NBD of an element to respectively. The particular cases of IVPFS are:

-

(i)

An IVPFS is changed to an IVIFS if

-

(ii)

An IVPFS is reduced to a PFS if and

The function means the IPF-hesitancy index of to where and Generally, an “interval-valued Pythagorean fuzzy number (IVPFN)” is given as which fulfills

Definition 3 (Zhang, 2016)

Let and be the IVPFNs. Then, some operations are given by

Definition 4 (Peng & Yang, 2016)

Consider be an IVPFN. Then, the score and accuracy values on IVPFN are given as

| 3 |

| 4 |

Definition 5 (Peng & Yang, 2016)

Let and be two IVPFNs, then the discrimination between and is given as

| 5 |

An extended IVPF-RSWM-DNMA methodology

The complicated modern world increasingly generates many problems that could be classified under the MCDM problems, whose solutions encourage scholars to develop many MCDM methods. The outranking approaches are generally confined to handling a large number of DEs and criteria. Nevertheless, the utility-based models only use a single normalization process for the non-dimensionalization of the assessment ratings over different criteria. In this regard, the use of an extant normalization technique can bias the results in cases where there is an improper normalization tool. To address this concern, Liao and Wu (2020) suggested a utility degree-based framework called the “double normalization-based multi-aggregation (DNMA)” appropriately combining the benefits of various normalization processes and aggregation ratings. In DNMA, the final integration function extensively takes into consideration the “subordinate utility degrees (SUDs)” and the ranks of alternatives; this way, it can offer highly reliable ranking results. Wu and Liao (2019) carried out comparative analyses between DNMA and other existing representative utility value-based methods. Wang and Rani (2021) discussed the DNMA approach on IFSs for the assessing the “sustainability risk factors (SRFs)” in “supply chain management (SCM).” Recently, Saha et al. (2022) presented the q-ROF “full consistency method (FUCOM)” DNMA tool to treat with the HCWTT assessment. Hezam et al. (2022) gave an MCDM methodology by combining “method based on the removal effects of criteria (MEREC)-rank sum (RS)-DNMA” approach with IFSs and applied to evaluate the “alternative fuel vehicles (AFVs)” problem. In this way, the RSWM is discussed to find the subjective weights of challenegs. Though, this is the first study that implemented the RSWM on IVPFSs. From the literature, there has been no study that incorporated the RSWM and the DNMA methods in IVPFSs setting to analyze and assess the challenges of implementing DT in sustainable financial service systems. This study proposes an extended method termed as “IVPF-RSWM-DNMA” by integrating the RSWM and the DNMA methods.

The steps for the IVPF-RSWM-DNMA method are (see Fig. 1):

Fig. 1.

Flowchart of developed IVPF-RSWM-DNMA model

Step 1: Obtain the “IVPF-decision matrix (IVPF-DM).”

For the MCDM process, consider a set of alternatives over the set of criteria The “decision expert (DE)” provides his/her assessments of options over attribute in term of “linguistic decision matrix (LDM).”

Step 2: Estimate the DEs’ weights.

Consider a set of DEs with important weight The DE’s weight is obtained as “linguistic values (LVs)” and presented by IVPFNs. Let be IVPFN of kth DE. Therefore, the weight is obtained as

| 6 |

where, and

Step 3: Obtain the “aggregated-IVPF-DM (AIVPF-DM).”

Let be the “linguistic decision matrix (LDM)” of expert. To combine all the distinct LDMs, we use the “averaging aggregation operator” and create an AIVPF-DM where such that

| 7 |

Step 4: Determine the criteria weights by RSWM.

The subjective weighting procedure allows showing the opinions and assessment ratings of DEs. The procedure of MCDM and the DEs’ opinion of each option over different criteria play important roles in choosing the best option for the given problem. In this regard, the DE provides their subjective rating (Hezam et al., 2022; Stillwell et al., 1981). Now, the RSWM supports the DE in giving their assessment ranking for considered criteria. The expression for obtaining the weight is

| 8 |

where rjmeans the rank of each attribute, j = 1, 2, 3, …, n.

Step 5: Obtain of the “normalized AIVPF-DM (N-AIVPF-DM).”

First, the linear normalization uses the principle with the maximum-minimum to generate the N-AIVPF-DM as follows:

where

| 9 |

Next, the vector normalization is used to generate the N-AIVPF-DM

where

| 10 |

| 11 |

| 12 |

Step 6: Apply the “subordinate aggregation models (SAMs).”

Here, we present various SAMs using the abovementioned normalization processes.

Step 6.1: Use the “complete compensatory method (CCM).”

The first model is applied with the “interval-valued Pythagorean fuzzy weighted averaging (IVPFWA) operator” as follows:

| 13 |

The options are prioritized with the score values of and we find the rank

Step 6.2: Use the “un-compensatory method (UCM).”

The second model is used with the IVPFWA-based maximum operator, given by

| 14 |

The options is prioritized with the score values and we find the rank

Step 6.3: Use the “incomplete compensatory method (ICM).”

The third model is applied with the vector normalization and the “interval-valued Pythagorean fuzzy weighted geometric (IVPFWG) operator” as

| 15 |

The options is prioritized with the score values and we find the rank

Step 7: Find the “subordinate utility degrees (SUDs).”

The abovementioned three models as represented as CCM UCM and ICM Each alternative has considered two aspects: the “SUDs” and the rankings over each attribute Thus, we obtain two “decision matrices (DMs),” the SUD-DM and the rankings-DM

To maintain the innovativeness of the SUDs the normalized values of SUDs are obtained as

| 16 |

Where

Step 8: Assess the “overall utility degree (OUD).”

A coefficient is assumed to present the impact of the SUDs and the rankings of options. Here, we assume The OUD of each alternative is defined by

| 17 |

where and are the weight values of the models with Here, the weight and are obtained using the developed IVPF-RSWM method. Finally, the preference set is found by the OUDs

Results and discussion

Case study

In this study, to identify and evaluate the main digital transformation challenges in the financial service sector, this study conducted a survey approach using the current literature review and interviews with experts. To do so, in the first stage, to identify the main digital transformation challenges, a comprehensive list including 29 challenges is collected from current literature. In the next stage, this list of challenges is presented in the questionnaire format and sent to 30 experts in digitalization and finance who work in different universities using their academic emails. To identify these 30 experts, we have searched through the published papers in the areas of digital transformation, digitalization, and financial service in Google Scholar. Before sending the questionnaire to those experts, we invited them to the participants by their email; from these 30 experts, 22 of them accepted our invitations to participate in our survey study. In the next stage, we sent the questionnaire in a word file format with blank space to provide their opinions. After three weeks, we sent the reminders to those experts to provide their feedback; therefore, after a few days, we received 16 questionnaires that experts completed and provided their feedback. We repeated this reminder after another two weeks, and finally, we could collect 22 questionnaires. In the primary questionnaire, we identified 29 digital transformation challenges; after analyzing all questionnaires, we selected 18 digital transformation challenges. In the next round of our survey approach and to evaluate these selected challenges, we have conducted the second round of invitations. In this round of data collection, we have invited experts from industry and academic who are experts in financial and digital transformation with several years of experience. The main industry experts work in IT, financial, accounting, and computing areas from five bank financial sectors. At this stage, we have invited four experts from industry and four experts from academics. To collect the data for evaluation and analysis, we conducted in-person interviews with these experts; although we invited eight experts, only five agreed to collaborate with us to evaluate the questionnaires. In the next stage, we have implemented the new fuzzy decision methodology called the IVPF-RSWM-DNMA. In this approach, the IVPF-RSWM is applied to find the subjective criteria weights, and the DNMA framework is developed to obtain the preferences of SFSSs in the banking sector. Here, the presented method is applied as follows: From Eq. (6) and Table 1, the DEs’ weights are obtained and are given in Table 2. The DEs offer LDM and are given in Table 3. From Eq. (7) and Table 3, the AIVPF-DM is created and presented in Table 4.

Table 1.

Significance rating of alternatives in the form of LVs

| LVs | IVPFNs |

|---|---|

| Perfectly good (PG) | ([0.90, 0.95], [0.10, 0.15]) |

| Very good (VG) | ([0.80, 0.90], [0.20, 0.35]) |

| Good (G) | ([0.65, 0.80], [0.40, 0.50]) |

| Moderate good (MG) | ([0.50, 0.65], [0.50, 0.60]) |

| Fair (F) | ([0.40, 0.50], [0.60, 0.70]) |

| Moderate low (ML) | ([0.30, 0.40], [0.70, 0.80]) |

| Low (L) | ([0.20, 0.30], [0.80, 0.85]) |

| Very low (VL) | ([0.10, 0.20], [0.85, 0.90]) |

| Very very low (VVL) | ([0.05, 0.10], [0.90, 0.95]) |

Table 2.

Assessment of DE’s weight

| DEs | LTs | IVPFN | Weights |

|---|---|---|---|

| E1 | Good | ([0.65, 0.80], [0.40, 0.50]) | 0.2204 |

| E2 | Moderate Good | ([0.50, 0.65], [0.50, 0.60]) | 0.1500 |

| E3 | Fair | ([0.40, 0.50], [0.60, 0.70]) | 0.0922 |

| E4 | Very Good | ([0.90, 0.95], [0.10, 0.15]) | 0.3170 |

| E5 | Good | ([0.65, 0.80], [0.40, 0.50]) | 0.2204 |

Table 3.

LDM for the ratings of alternatives by DEs

| Challenges | |||||

|---|---|---|---|---|---|

| C1 | (F,MG,MG,F,ML) | (G,G,G,MG,F) | (MG,MG,F,ML,G) | (G,MG,F,F,F) | (F,G,MG,G,F) |

| C2 | (ML,L,F,ML,F) | (VL,VL,VL,ML,L) | (MG,F,MG,G,G) | (VG,MG,VG,G,F) | (F,G,F,MG,ML) |

| C3 | (G,VG,G,ML,G) | (VG,VG,VG,F,G) | (F,MG,F,G,ML) | (MG,G,F,ML,G) | (L,F,VL,G,G) |

| C4 | (L,VL,VL,G,G) | (L,ML,VL,F,F) | (L,ML,VL,ML,F) | (MG,ML,F,G,MG) | (G,PG,G,MG,F) |

| C5 | (MG,G,F,MG,ML) | (VG,G,VG,F,ML) | (G,VG,F,G,ML) | (VL,ML,L,MG,G) | (VG,F,G,G,MG) |

| C6 | (VG,VG,MG,L,F) | (G,VG,VG,F,F) | (F,MG,VL,ML,F) | (MG,ML,F,MG,F) | (L,ML,ML,MG,F) |

| C7 | (MG,L,F,ML,G) | (PG,G,MG,G,G) | (MG,F,VG,F,ML) | (PG,G,F,MG,G) | (ML,G,F,ML,VG) |

| C8 | (L,L,VL,ML,MG) | (L,VL,VL,ML,ML) | (ML,ML,F,G,MG) | (L,MG,F,MG,MG) | (ML,VL,F,ML,L) |

| C9 | (G,G,F,G,MG) | (ML,F,VL,L,VL) | (F,G,MG,G,F) | (F,VL,ML,VL,F) | (MG,G,G,L,ML) |

| C10 | (ML,L,F,L,F) | (ML,VL,ML,VL,F) | (G,ML,ML,F,MG) | (VL,VL,L,F,G) | (L,MG,ML,ML,F) |

| C11 | (MG,MG,F,G,G) | (F,G,G,PG,MG) | (VG,MG,F,MG,F) | (L,VL,ML,F,L) | (ML,VL,L,F,G) |

| C12 | (PG,G,F,F,F) | (MG,G,VG,G,F) | (F,VG,F,G,ML) | (G,ML,MG,G,VG) | (F,ML,MG,L,ML) |

| C13 | (VG,G,VG,F,F) | (G,PG,VG,F,MG) | (MG,ML,ML,F,G) | (MG,VG,F,L,ML) | (ML,ML,F,F,F) |

| C14 | (L,ML,VL,ML,F) | (L,L,ML,MG,G) | (G,F,L,MG,MG) | (ML,L,F,MG,MG) | (VG,MG,F,G,G) |

| C15 | (G,MG,F,MG,G) | (VG,G,MG,MG,F) | (ML,G,F,MG,G) | (VL,VL,L,ML,F) | (VG,F,ML,MG,F) |

| C16 | (L,VL,L,ML,ML) | (L,VL,VL,ML,F) | (G,VG,F,ML,F) | (ML,MG,F,G,MG) | (F,G,MG,F,G) |

| C17 | (ML,F,F,MG,ML) | (ML,ML,L,F,MG) | (ML,F,MG,G,MG) | (VG,MG,L,VL,F) | (PG,G,F,ML,L) |

| C18 | (VG,G,PG,MG,F) | (VG,G,VG,MG,F) | (F,L,F,MG,G) | (VG,L,F,F,F) | (VG,G,VG,G,G) |

Table 4.

The AIVPF-DM for options

| C1 | ([0.410, 0.527], [0.594, 0.694]) | ([0.564, 0.713], [0.469, 0.571]) | ([0.489, 0.632], [0.539, 0.640]) | ([0.490, 0.622], [0.534, 0.635]) | ([0.550, 0.693], [0.488, 0.590]) |

| C2 | ([0.325, 0.424], [0.681, 0.774]) | ([0.206, 0.301], [0.789, 0.856]) | ([0.581, 0.731], [0.456, 0.557]) | ([0.661, 0.792], [0.364, 0.495]) | ([0.469, 0.605], [0.551, 0.653]) |

| C3 | ([0.570, 0.705], [0.471, 0.592]) | ([0.691, 0.814], [0.330, 0.472]) | ([0.504, 0.643], [0.531, 0.633]) | ([0.518, 0.664], [0.521, 0.623]) | ([0.531, 0.678], [0.531, 0.624]) |

| C4 | ([0.514, 0.663], [0.559, 0.648]) | ([0.333, 0.431], [0.676, 0.763]) | ([0.297, 0.395], [0.709, 0.796]) | ([0.531, 0.679], [0.498, 0.600]) | ([0.651, 0.772], [0.381, 0.476]) |

| C5 | ([0.489, 0.634], [0.530, 0.631]) | ([0.616, 0.743], [0.414, 0.552]) | ([0.620, 0.760], [0.423, 0.542]) | ([0.455, 0.598], [0.588, 0.680]) | ([0.605, 0.783], [0.383, 0.506]) |

| C6 | ([0.605, 0.729], [0.430, 0.572]) | ([0.608, 0.737], [0.421, 0.550]) | ([0.374, 0.485], [0.633, 0.730]) | ([0.447, 0.581], [0.557, 0.657]) | ([0.386, 0.509], [0.626, 0.719]) |

| C7 | ([0.459, 0.598], [0.578, 0.675]) | ([0.733, 0.847], [0.301, 0.390]) | ([0.478, 0.600], [0.539, 0.654]) | ([0.701, 0.815], [0.328, 0.419]) | ([0.559, 0.687], [0.481, 0.614]) |

| C8 | ([0.355, 0.416], [0.582, 0.744]) | ([0.315, 0.432], [0.702, 0.783]) | ([0.501, 0.644], [0.537, 0.639]) | ([0.447, 0.588], [0.564, 0.657]) | ([0.273, 0.370], [0.732, 0.815]) |

| C9 | ([0.606, 0.757], [0.436, 0.537]) | ([0.606, 0.757], [0.436, 0.537]) | ([0.550, 0.693], [0.488, 0.590]) | ([0.294, 0.387], [0.716, 0.797]) | ([0.453, 0.595], [0.592, 0.683]) |

| C10 | ([0.300, 0.398], [0.710, 0.789]) | ([0.300, 0.398], [0.710, 0.789]) | ([0.481, 0.617], [0.547, 0.649]) | ([0.410, 0.537], [0.641, 0.726]) | ([0.348, 0.460], [0.663, 0.754]) |

| C11 | ([0.584, 0.736], [0.451, 0.552]) | ([0.730, 0.830], [0.296, 0.383]) | ([0.582, 0.714], [0.433, 0.559]) | ([0.283, 0.379], [0.728, 0.802]) | ([0.443, 0.553], [0.614, 0.708]) |

| C12 | ([0.654, 0.756], [0.380, 0.474]) | ([0.603, 0.746], [0.431, 0.542]) | ([0.576, 0.710], [0.463, 0.584]) | ([0.655, 0.793], [0.381, 0.504]) | ([0.327, 0.434], [0.684, 0.771]) |

| C13 | ([0.625, 0.750], [0.400, 0.536]) | ([0.665, 0.781], [0.364, 0.468]) | ([0.481, 0.617], [0.547, 0.649]) | ([0.484, 0.610], [0.554, 0.668]) | ([0.367, 0.467], [0.635, 0.735]) |

| C14 | ([0.297, 0.395], [0.709, 0.796]) | ([0.459, 0.602], [0.584, 0.673]) | ([0.513, 0.660], [0.511, 0.609]) | ([0.423, 0.559], [0.588, 0.683]) | ([0.663, 0.801], [0.369, 0.490]) |

| C15 | ([0.570, 0.710], [0.461, 0.562]) | ([0.609, 0.744], [0.411, 0.536]) | ([0.531, 0.679], [0.504, 0.606]) | ([0.270, 0.364], [0.736, 0.816]) | ([0.568, 0.696], [0.451, 0.579]) |

| C16 | ([0.251, 0.348], [0.751, 0.830]) | ([0.277, 0.372], [0.730, 0.810]) | ([0.549, 0.680], [0.489, 0.611]) | ([0.522, 0.668], [0.510, 0.612]) | ([0.526, 0.665], [0.508, 0.609]) |

| C17 | ([0.401, 0.524], [0.606, 0.707]) | ([0.382, 0.498], [0.627, 0.724]) | ([0.517, 0.662], [0.553, 0.654]) | ([0.519, 0.643], [0.526, 0.647]) | ([0.629, 0.732], [0.426, 0.516]) |

| C18 | ([0.668, 0.788], [0.355, 0.472]) | ([0.642, 0.773], [0.378, 0.510]) | ([0.489, 0.629], [0.541, 0.637]) | ([0.538, 0.655], [0.492, 0.619]) | ([0.708, 0.840], [0.322, 0.447]) |

From Eq. (10), we find the weight of each challenge to implement digital transformation in SFSSs in banking sectors in Table 5, and presented in Fig. 2.

Table 5.

Weights of challenges to implementing DT in SFSSs using RSWM

| Challenges | E1 | E2 | E3 | E4 | E5 | Aggregated IVPFNs | Crisp values | Rank of challenges | Weight |

|---|---|---|---|---|---|---|---|---|---|

| C1 | G | MG | ML | F | MG | ([0.434, 0.559], [0.569, 0.669]) | 0.432 | 9 | 0.0578 |

| C2 | ML | F | MG | L | F | ([0.343, 0.449], [0.669, 0.756]) | 0.325 | 14 | 0.0289 |

| C3 | ML | ML | L | F | VL | ([0.303, 0.399], [0.704, 0.791]) | 0.282 | 17 | 0.0116 |

| C4 | F | G | ML | F | F | ([0.410, 0.521], [0.592, 0.692]) | 0.402 | 10 | 0.0520 |

| C5 | VL | ML | L | ML | F | ([0.291, 0.387], [0.715, 0.802]) | 0.270 | 18 | 0.0058 |

| C6 | F | G | MG | F | ML | ([0.447, 0.572], [0.574, 0.676]) | 0.435 | 8 | 0.0636 |

| C7 | ML | F | G | L | F | ([0.372, 0.486], [0.655, 0.743]) | 0.348 | 11 | 0.0462 |

| C8 | MG | F | L | MG | F | ([0.447, 0.580], [0.559, 0.656]) | 0.449 | 7 | 0.0694 |

| C9 | ML | F | MG | ML | F | ([0.364, 0.471], [0.641, 0.741]) | 0.348 | 11 | 0.0462 |

| C10 | F | G | ML | F | MG | ([0.469, 0.599], [0.550, 0.651]) | 0.463 | 2 | 0.0983 |

| C11 | L | VL | MG | ML | F | ([0.316, 0.422], [0.696, 0.780]) | 0.296 | 16 | 0.0173 |

| C12 | ML | F | MG | L | F | ([0.343, 0.449], [0.669, 0.756]) | 0.325 | 14 | 0.0289 |

| C13 | G | ML | L | MG | ML | ([0.471, 0.614], [0.563, 0.662]) | 0.461 | 3 | 0.0925 |

| C14 | G | L | ML | MG | ML | ([0.468, 0.611], [0.567, 0.664]) | 0.457 | 4 | 0.0867 |

| C15 | MG | G | L | F | MG | ([0.485, 0.625], [0.535, 0.633]) | 0.485 | 1 | 0.1040 |

| C16 | ML | G | F | F | MG | ([0.460, 0.591], [0.561, 0.663]) | 0.452 | 5 | 0.0809 |

| C17 | ML | G | F | L | G | ([0.473, 0.614], [0.585, 0.677]) | 0.450 | 6 | 0.0751 |

| C18 | L | F | MG | ML | F | ([0.349, 0.456], [0.660, 0.751]) | 0.332 | 13 | 0.0289 |

Fig. 2.

Subjective weights of each challenge to implement digital transformation in SFSSs

According to the Eqs. (8)-(11) and Table 5, the linear N-AIVPF-DN and vector N-AIVPF-DM are created and given in Tables 6 and 7.

Table 6.

Linear N-AIVPF-DM for each option to implement DT in SFSSs

| R1 | R2 | R3 | R4 | R5 | |

|---|---|---|---|---|---|

| C1 | ([0.0997, 0.1697], [0.7430, 0.8123]) | ([0.1965, 0.3330], [0.6497, 0.7261]) | ([0.1444, 0.2525], [0.7026, 0.7756]) | ([0.1446, 0.2432], [0.6992, 0.7719]) | ([0.1855, 0.3115], [0.6644, 0.7400]) |

| C2 | ([0.0721, 0.1244], [0.7722, 0.8421]) | ([0.0288, 0.0618], [0.8525, 0.9009]) | ([0.2414, 0.4014], [0.5898, 0.6747]) | ([0.3205, 0.4854], [0.5073, 0.6235]) | ([0.1540, 0.2637], [0.6703, 0.7508]) |

| C3 | ([0.2412, 0.3827], [0.5892, 0.6925]) | ([0.3659, 0.5330], [0.4593, 0.5901]) | ([0.1856, 0.3129], [0.6414, 0.7255]) | ([0.1971, 0.3350], [0.6326, 0.7175]) | ([0.2074, 0.3514], [0.6411, 0.7182]) |

| C4 | ([0.1836, 0.3186], [0.6808, 0.7505]) | ([0.0750, 0.1270], [0.7714, 0.8360]) | ([0.0593, 0.1060], [0.7968, 0.8598]) | ([0.1967, 0.3359], [0.6307, 0.7130]) | ([0.3052, 0.4509], [0.5284, 0.6121]) |

| C5 | ([0.1617, 0.2815], [0.6641, 0.7433]) | ([0.2649, 0.4034], [0.5670, 0.6819]) | ([0.2684, 0.4264], [0.5749, 0.6742]) | ([0.1390, 0.2482], [0.7101, 0.7797]) | ([0.2547, 0.4570], [0.5392, 0.6449]) |

| C6 | ([0.2424, 0.3699], [0.5986, 0.7118]) | ([0.2451, 0.3786], [0.5903, 0.6947]) | ([0.0877, 0.1506], [0.7572, 0.8259]) | ([0.1270, 0.2213], [0.7002, 0.7747]) | ([0.0936, 0.1671], [0.7523, 0.8179]) |

| C7 | ([0.1632, 0.2832], [0.6617, 0.7436]) | ([0.4400, 0.6146], [0.4047, 0.4920]) | ([0.1777, 0.2858], [0.6277, 0.7260]) | ([0.3993, 0.5606], [0.4323, 0.5195]) | ([0.2456, 0.3822], [0.5767, 0.6924]) |

| C8 | ([0.0642, 0.0891], [0.7662, 0.8646]) | ([0.0503, 0.0969], [0.8399, 0.8865]) | ([0.1324, 0.2319], [0.7361, 0.8021]) | ([0.1039, 0.1887], [0.7543, 0.8133]) | ([0.0373, 0.0699], [0.8575, 0.9043]) |

| C9 | ([0.2450, 0.4071], [0.6002, 0.6821]) | ([0.2450, 0.4071], [0.6002, 0.6821]) | ([0.1986, 0.3315], [0.6433, 0.7226]) | ([0.0540, 0.0948], [0.8143, 0.8697]) | ([0.1320, 0.2356], [0.7244, 0.7910]) |

| C10 | ([0.0436, 0.0783], [0.8505, 0.8942]) | ([0.0436, 0.0783], [0.8505, 0.8942]) | ([0.1167, 0.2029], [0.7519, 0.8151]) | ([0.0832, 0.1486], [0.8104, 0.8596]) | ([0.0593, 0.1064], [0.8231, 0.8750]) |

| C11 | ([0.2681, 0.4412], [0.5516, 0.6413]) | ([0.4338, 0.5827], [0.4028, 0.4879]) | ([0.2660, 0.4127], [0.5347, 0.6477]) | ([0.0605, 0.1093], [0.7888, 0.8478]) | ([0.1504, 0.2385], [0.6948, 0.7723]) |

| C12 | ([0.3100, 0.4307], [0.5260, 0.6088]) | ([0.2597, 0.4181], [0.5715, 0.6659]) | ([0.2348, 0.3726], [0.5993, 0.6994]) | ([0.3112, 0.4828], [0.5267, 0.6345]) | ([0.0723, 0.1294], [0.7771, 0.8414]) |

| C13 | ([0.2842, 0.4277], [0.5392, 0.6564]) | ([0.3253, 0.4696], [0.5056, 0.5988]) | ([0.1624, 0.2765], [0.6656, 0.7469]) | ([0.1646, 0.2693], [0.6712, 0.7615]) | ([0.0930, 0.1528], [0.7362, 0.8127]) |

| C14 | ([0.0606, 0.1082], [0.7928, 0.8569]) | ([0.1475, 0.2625], [0.6954, 0.7654]) | ([0.1866, 0.3208], [0.6350, 0.7152]) | ([0.1251, 0.2235], [0.6980, 0.7729]) | ([0.3242, 0.4996], [0.5092, 0.6173]) |

| C15 | ([0.2151, 0.3510], [0.6200, 0.7005]) | ([0.2488, 0.3924], [0.5780, 0.6809]) | ([0.1849, 0.3168], [0.6554, 0.7342]) | ([0.0457, 0.0842], [0.8277, 0.8821]) | ([0.2137, 0.3356], [0.6117, 0.7140]) |

| C16 | ([0.0343, 0.0672], [0.8575, 0.9046]) | ([0.0420, 0.0772], [0.8445, 0.8929]) | ([0.1754, 0.2833], [0.6804, 0.7673]) | ([0.1569, 0.2727], [0.6964, 0.7680]) | ([0.1597, 0.2694], [0.6946, 0.7661]) |

| C17 | ([0.1030, 0.1806], [0.7327, 0.8063]) | ([0.0931, 0.1625], [0.7480, 0.8181]) | ([0.1756, 0.3012], [0.6925, 0.7683]) | ([0.1770, 0.2820], [0.6706, 0.7632]) | ([0.2685, 0.3797], [0.5882, 0.6631]) |

| C18 | ([0.3485, 0.5059], [0.4712, 0.5799]) | ([0.3200, 0.4833], [0.4936, 0.6137]) | ([0.1796, 0.3060], [0.6400, 0.7211]) | ([0.2193, 0.3346], [0.5974, 0.7057]) | ([0.3969, 0.5879], [0.4394, 0.5577]) |

Table 7.

Vector N-AIVPF-DM for each option to implement DT in SFSSs

| R1 | R2 | R3 | R4 | R5 | |

|---|---|---|---|---|---|

| C1 | ([0.2250, 0.2894], [0.3242, 0.3791]) | ([0.3097, 0.3913], [0.2563, 0.3114]) | ([0.2684, 0.3469], [0.2940, 0.3496]) | ([0.2686, 0.3412], [0.2915, 0.3467]) | ([0.3016, 0.3803], [0.2665, 0.3219]) |

| C2 | ([0.1893, 0.2470], [0.3385, 0.3851]) | ([0.1204, 0.1755], [0.3922, 0.4258]) | ([0.3386, 0.4262], [0.2267, 0.2769]) | ([0.3856, 0.4621], [0.1811, 0.2462]) | ([0.2737, 0.3528], [0.2742, 0.3246]) |

| C3 | ([0.2823, 0.3490], [0.2756, 0.3468]) | ([0.3420, 0.4028], [0.1932, 0.2761]) | ([0.2493, 0.3186], [0.3109, 0.3707]) | ([0.2565, 0.3287], [0.3049, 0.3648]) | ([0.2628, 0.3359], [0.3108, 0.3653]) |

| C4 | ([0.2963, 0.3825], [0.2837, 0.3286]) | ([0.1922, 0.2484], [0.3426, 0.3869]) | ([0.1713, 0.2276], [0.3598, 0.4036]) | ([0.3062, 0.3917], [0.2527, 0.3042]) | ([0.3752, 0.4452], [0.1934, 0.2415]) |

| C5 | ([0.2423, 0.3137], [0.3144, 0.3745]) | ([0.3051, 0.3677], [0.2459, 0.3276]) | ([0.3070, 0.3765], [0.2513, 0.3219]) | ([0.2254, 0.2962], [0.3488, 0.4033]) | ([0.2998, 0.3875], [0.2275, 0.3004]) |

| C6 | ([0.3420, 0.4121], [0.2275, 0.3025]) | ([0.3437, 0.4162], [0.2224, 0.2906]) | ([0.2114, 0.2741], [0.3348, 0.3862]) | ([0.2528, 0.3281], [0.2944, 0.3476]) | ([0.2182, 0.2879], [0.3312, 0.3800]) |

| C7 | ([0.2200, 0.2865], [0.3556, 0.4152]) | ([0.3512, 0.4061], [0.1851, 0.2399]) | ([0.2293, 0.2877], [0.3315, 0.4022]) | ([0.3361, 0.3907], [0.2020, 0.2579]) | ([0.2678, 0.3294], [0.2962, 0.3776]) |

| C8 | ([0.2506, 0.2933], [0.2702, 0.3453]) | ([0.2226, 0.3052], [0.3256, 0.3633]) | ([0.3533, 0.4546], [0.2490, 0.2965]) | ([0.3154, 0.4152], [0.2617, 0.3049]) | ([0.1924, 0.2611], [0.3396, 0.3782]) |

| C9 | ([0.3257, 0.4070], [0.2329, 0.2866]) | ([0.3257, 0.4070], [0.2329, 0.2866]) | ([0.2957, 0.3728], [0.2607, 0.3149]) | ([0.1580, 0.2080], [0.3823, 0.4255]) | ([0.2439, 0.3200], [0.3161, 0.3647]) |

| C10 | ([0.2178, 0.2889], [0.3201, 0.3558]) | ([0.2178, 0.2889], [0.3201, 0.3558]) | ([0.3488, 0.4480], [0.2467, 0.2925]) | ([0.2974, 0.3898], [0.2890, 0.3274]) | ([0.2527, 0.3340], [0.2987, 0.3399]) |

| C11 | ([0.3047, 0.3835], [0.2486, 0.3041]) | ([0.3806, 0.4330], [0.1632, 0.2109]) | ([0.3036, 0.3722], [0.2384, 0.3081]) | ([0.1475, 0.1975], [0.4012, 0.4418]) | ([0.2308, 0.2882], [0.3385, 0.3900]) |

| C12 | ([0.3226, 0.3729], [0.2246, 0.2799]) | ([0.2976, 0.3682], [0.2545, 0.3203]) | ([0.2840, 0.3502], [0.2734, 0.3449]) | ([0.3232, 0.3913], [0.2251, 0.2979]) | ([0.1611, 0.2140], [0.4041, 0.4554]) |

| C13 | ([0.3306, 0.3967], [0.2233, 0.2988]) | ([0.3516, 0.4128], [0.2030, 0.2608]) | ([0.2542, 0.3265], [0.3051, 0.3618]) | ([0.2558, 0.3225], [0.3089, 0.3724]) | ([0.1941, 0.2469], [0.3542, 0.4101]) |

| C14 | ([0.1691, 0.2246], [0.3663, 0.4109]) | ([0.2609, 0.3426], [0.3017, 0.3477]) | ([0.2920, 0.3756], [0.2638, 0.3145]) | ([0.2410, 0.3179], [0.3034, 0.3527]) | ([0.3774, 0.4556], [0.1903, 0.2530]) |

| C15 | ([0.3041, 0.3789], [0.2517, 0.3067]) | ([0.3252, 0.3973], [0.2246, 0.2929]) | ([0.2835, 0.3623], [0.2754, 0.3310]) | ([0.1442, 0.1945], [0.4020, 0.4456]) | ([0.3032, 0.3716], [0.2462, 0.3164]) |

| C16 | ([0.1555, 0.2160], [0.3616, 0.3993]) | ([0.1717, 0.2310], [0.3514, 0.3898]) | ([0.3405, 0.4214], [0.2351, 0.2941]) | ([0.3234, 0.4146], [0.2455, 0.2945]) | ([0.3261, 0.4124], [0.2443, 0.2932]) |

| C17 | ([0.2258, 0.2951], [0.3168, 0.3695]) | ([0.2150, 0.2808], [0.3275, 0.3783]) | ([0.2913, 0.3731], [0.2893, 0.3419]) | ([0.2924, 0.3623], [0.2747, 0.3383]) | ([0.3544, 0.4127], [0.2224, 0.2697]) |

| C18 | ([0.3101, 0.3661], [0.2299, 0.3060]) | ([0.2982, 0.3590], [0.2451, 0.3309]) | ([0.2269, 0.2920], [0.3506, 0.4132]) | ([0.2497, 0.3044], [0.3188, 0.4011]) | ([0.3290, 0.3900], [0.2088, 0.2900]) |

The SUDs of three models are obtained by Eq. (13)-Eq. (15) and are portrayed in Table 8. Then, corresponding to Eq. (16), the normalized SUDs are calculated with the rankings of alternatives and shown in Table 9.

Table 8.

The SUDs for each option to implement DT in SFSSs

| Option | CCM | UCM | ICM | |||

|---|---|---|---|---|---|---|

| R1 | ([0.182, 0.289], [0.686, 0.768]) | 0.264 | ([0.119, 0.146], [0.735, 0.779]) | 0.222 | ([0.263, 0.329], [0.288, 0.346]) | 0.494 |

| R2 | ([0.221, 0.341], [0.656, 0.737]) | 0.298 | ([0.119, 0.146], [0.735, 0.779]) | 0.222 | ([0.280, 0.348], [0.271, 0.326]) | 0.505 |

| R3 | ([0.167, 0.282], [0.682, 0.760]) | 0.266 | ([0.079, 0.102], [0.810, 0.855]) | 0.157 | ([0.289, 0.369], [0.281, 0.336]) | 0.507 |

| R4 | ([0.174, 0.279], [0.693, 0.770]) | 0.259 | ([0.113, 0.145], [0.725, 0.773]) | 0.228 | ([0.273, 0.347], [0.291, 0.345]) | 0.498 |

| R5 | ([0.203, 0.319], [0.664, 0.746]) | 0.286 | ([0.105, 0.133], [0.758, 0.802]) | 0.203 | ([0.288, 0.358], [0.273, 0.329]) | 0.507 |

Table 9.

Normalized SUDs and OUDs to implement DT in SFSSs

| Option | CCM | UCM | ICM | Final ranking | ||||

|---|---|---|---|---|---|---|---|---|

| R1 | 0.429 | 4 | 0.478 | 3.5 | 0.440 | 5 | 0.590 | 5 |

| R2 | 0.485 | 1 | 0.478 | 3.5 | 0.450 | 3 | 0.662 | 2 |

| R3 | 0.433 | 3 | 0.338 | 1 | 0.451 | 2 | 0.707 | 1 |

| R4 | 0.421 | 5 | 0.489 | 5 | 0.443 | 4 | 0.604 | 4 |

| R5 | 0.466 | 2 | 0.436 | 2 | 0.452 | 1 | 0.645 | 3 |

| Weight of aggregation model | ||||||||

From Eq. (17), the OUDs and the preference order of options are computed and mentioned in Table 9. Hence, the ranking of alternatives is and R3 is the best alternative.

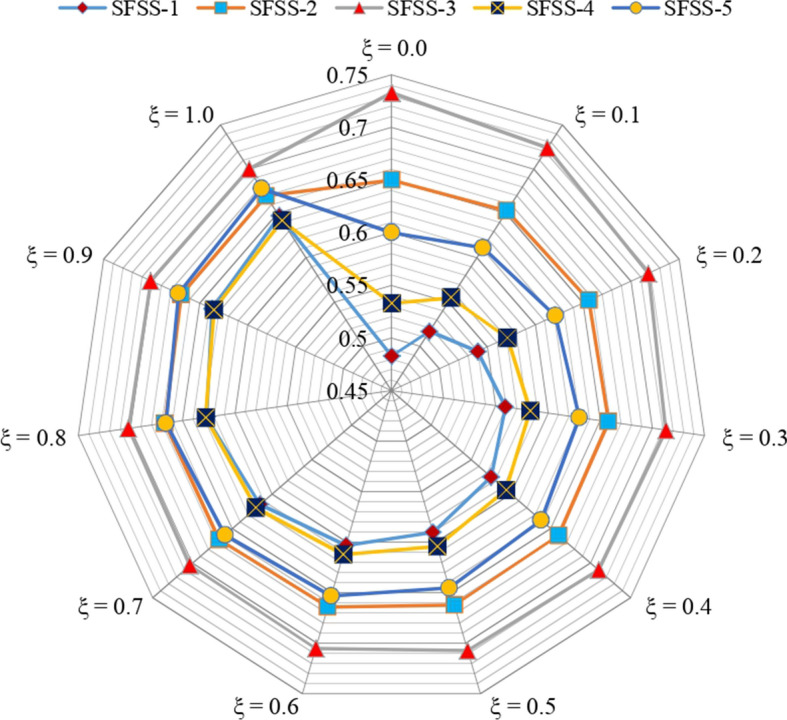

Sensitivity investigation

We present analysis with the coefficient values. The diverse values of is useful for evaluating the sensitivity of the presented approach by altering from the SUDs to the subordinate rankings. Furthermore, variation of is used to express the sensitivity of the presented approach to the distinction of weights of criteria.

Table 10 and Fig. 3 exemplify the assessment of the alternatives for diverse utility coefficeingt values. Thus, we get the same rankings for to and for to which shows that R3 is the optimal one for each value of while the R1 has the last rank for to and the R4 has the last rank for to Therefore, it is noticed that the proposed method holds adequate stability against the large range of parameter values.

Table 10.

Variation of OUDs with different values of

| R1 | R2 | R3 | R4 | R5 | |

|---|---|---|---|---|---|

| 0.0 | 0.483 | 0.650 | 0.733 | 0.533 | 0.600 |

| 0.1 | 0.517 | 0.653 | 0.724 | 0.555 | 0.611 |

| 0.2 | 0.540 | 0.656 | 0.718 | 0.571 | 0.621 |

| 0.3 | 0.559 | 0.658 | 0.713 | 0.583 | 0.630 |

| 0.4 | 0.575 | 0.660 | 0.710 | 0.594 | 0.638 |

| 0.5 | 0.590 | 0.662 | 0.707 | 0.604 | 0.645 |

| 0.6 | 0.603 | 0.664 | 0.705 | 0.612 | 0.653 |

| 0.7 | 0.615 | 0.666 | 0.703 | 0.620 | 0.659 |

| 0.8 | 0.627 | 0.667 | 0.702 | 0.628 | 0.666 |

| 0.9 | 0.637 | 0.669 | 0.701 | 0.635 | 0.672 |

| 1.0 | 0.647 | 0.670 | 0.700 | 0.642 | 0.678 |

Fig. 3.

Sensitivity of the with diverse utility parameter values

Comparison with existing methods

In what follows, we present a comparative study between the proposed and existing IVPF-TOPSIS model (Garg, 2017) for treating the MCDM problems under IVPFSs as follows:

Steps 1–4: Same as presented method.

Step 5: Calculate the discriminations of each alternative from “IVPF-ideal solution (IS)” and “IVPF-anti-ideal solution (AIS).”

Here, the BD and NBD of IVPF-IS are discussed as 1 and 0, and defined as Similarly, IVPF-A-IS is

To assess the option(s) we use the distance measure as

| 18 |

and

| 19 |

Step 6: Obtain “closeness index (CI).”

The CI of an option is defined by

| 20 |

Step 7: Determine the prioritization of alternatives.

From the we find the ranking order of options, and we get the optimal option.

Following the above steps, the IVPF-TOPSIS model is applied and discussed in Table 11.

Table 11.

Ranking of IVPF-TOPSIS for SFSS options

| Options | Ranking | |||

|---|---|---|---|---|

| R1 | 0.743 | 0.251 | 0.253 | 4 |

| R2 | 0.731 | 0.263 | 0.264 | 3 |

| R3 | 0.717 | 0.278 | 0.279 | 1 |

| R4 | 0.746 | 0.249 | 0.250 | 5 |

| R5 | 0.720 | 0.274 | 0.276 | 2 |

From Table 11, the most optimal SFSS option is R3, and the priority order obtained by the developed IVPF-RSWM-DNMA model shows conformity with the IVPF-TOPSIS model. By comparing with the IVPF-TOPSIS, we get the rank as Overall, the benefits of the IVPF-RSWM-DNMA framework with the extant model is presented as follows (see Fig. 4):

In the presented approach, the weights of DEs are computed by the weighting formula, resulting in a correct significance degree of DEs, unlike the arbitrary selection of attribute weight by DEs in Garg (2017).

The subjective weights of attributes in the proposed method are obtained by IVPF-RSWM, whereas in IVPF-TOPSIS, the criteria weights are chosen arbitrarily.

In Garg (2017), the distance is computed between the aggregated rankings and the IVPF-IS , and the IVPF-AIS to describe the CI of each option. The IVPF-IS and IVPF-AIS may be considered two standards against which the show of the options for each challenge could be assessed. Note that the two benchmarks mentioned above may not be attained fully in practice. On the other hand, it should be noted that the proposed IVPF-RSWM-DNMA uses strength points of various normalization procedures and models and can integrate all of them appropriately. Moreover, the OUD of the DNMA method broadly considers the SUDs and the ranks of options. Thus, the final ranking results from the suggested methodology could be highly reliable and more realistic as the DEs could know about the best and worst ratings of options on the defined challeneges and compare their performance.

Fig. 4.

The OUDs and CI of each SFSS option with different methods

Conclusions

Technological and digital innovation has significant strategic implications for companies by altering the competitive setting and the market dynamics in the financial sector. In addition, it is widely acknowledged that intensified competition and technological changes within a sector have the potential to give benefits to end customers through enhancing the quality of products and services and, at the same time, lowering their prices. DT should not be taken into account as a mere technological revolution; rather, it has the potential to drive the 3rd industrial revolution that concerns the growth of a novel ICT, where the augmented use of digital devices and platforms is transforming the ways consumers do banking, shift their market expectations, and also transform the model of financial intermediation. The contemporary digitization waves in the financial service systems of banks—especially in the case of payments—and the utilization of access and network technologies have led to the creation of different opportunities for novel entrants and challenges that banks to claim some market share, but also for established banks to reassess their positions within the market and the value they propose to their clients. In such a dynamic environment, banks are able to choose either to embrace changes by using the opportunities that technology offers through making interactions with the greater ecosystem of market participants and other service providers or to take a defensive position through being concentrating on the development of competitive solutions to all customer and product segments and putting limitations on access to their systems. Numerous researchers, policy makers, and practitioners have become interested in the digital transformation in banking, which causes us to think about what the banking sector could look like after the predicted digital transformation. Motivated by the above, this study targeted to recognize and evaluate the digital transformation challenges in sustainable financial service systems of the banking sector. To analyze, rank, and evaluate the digital transformation challenges in sustainable financial service systems of the banking sector, this study developed an integrated methodology for IVPFSs. In this regard, an extended approach termed as “IVPF-RSWM-DNMA” method is developed to evaluate the digital transformation challenges in sustainable financial service systems of the banking sector. To rank the digital transformation challenges in sustainable financial service systems of the banking sector, the IVPF-ranking sum weighting method (RSWM) is utilized to compute the preference order of different sustainable financial service systems in the banking sector DNMA method is used. A comparative study using the IVPF-TOPSIS method is conducted to validate the results from the suggested methodology. However, the presented IVIF-DNMA model has offered significant insights into the MCDM process but still has several limitations that permit advanced study and model improvement. The presented approach could be enhanced using the linguistic assessments of criteria with an aggregated decision matrix. Only subjective weight of attribute is used that determines from the IVIF-RS method and derived based on information provided by DEs.

In the future, this study could be carried out in the context of other countries, and results could be compared in a cross-national and cross-cultural perspective at a national or organizational level. In addition, future studies in this domain could compare our findings with those of other business sectors with high regulative pressures, for instance, the pharmaceutical industry. It will result in deeper insight into the incidences of and impacts on DT across nations and business sectors, leading to more detailed recommendations for practitioners. In the future, researchers could integrate various perspectives in a way to achieve an all-inclusive overview of the opinions and statements from a business perspective, which extends from the micro-level to the proposed approach. Performing real-time case studies of various financial service providers will provide insights into concrete digitization projects and result in the best-practice principles for the effective use of such projects.

Future studies can be focused upon the evaluation of the DT challenges identified in the present paper, and they can discuss priorities offered here and interdependencies with the use of various MCDM models such as “combinative distance-based assessment (CODAS),” “evaluation based on distance from average solution (EDAS),” “gained and lost dominance score (GLDS), “best worst method (BWM),” and other. In addition, future research can be focused on the identification and elimination the DT challenges of SFSS using the integrated models.

Availability of data and materials

Not applicable.

Declarations

Conflict of interest

The authors declare no competing interests.

Footnotes

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Contributor Information

Mohamadtaghi Rahimi, Email: mt_rahimi@alumni.iust.ac.ir.

Pranesh Kumar, Email: pranesh.kumar@unbc.ca.

Mahdieh Moazzamigodarzi, Email: moazzamig@unbc.ca.

Arunodaya Raj Mishra, Email: arunodaya87@outlook.com.

References

- Abraham KS. Environmental liability and the limits of insurance. Columbia Law Review. 1988;88:942–988. doi: 10.2307/1122695. [DOI] [Google Scholar]

- Alt R, Reinhold O. Social-Customer-Relationship-Management (Social-CRM) Wirtschaftsinformatik. 2012;54:281–286. doi: 10.1007/s11576-012-0330-6. [DOI] [Google Scholar]

- Al-Barakati A, Mishra AR, Mardani A, Rani P. An extended interval-valued Pythagorean fuzzy WASPAS method based 729 on new similarity measures to evaluate the renewable energy sources. Applied Soft Computing. 2022;120(108689):730. doi: 10.1016/j.asoc.2022.108689. [DOI] [Google Scholar]

- Aral S, Weill P. IT assets, organizational capabilities, and firm performance: How resource allocations and organizational differences explain performance variation. Organization Science. 2007;18:763–780. doi: 10.1287/orsc.1070.0306. [DOI] [Google Scholar]

- Arner, D.W., Barberis, J.N., Buckley, R.P. (2016) 150 years of Fintech: An evolutionary analysis. Jassa-the Finsia Journal of Applied Finance, 22.

- Asif S, Sargeant A. Modelling internal communications in the financial services sector. European Journal of Marketing. 2000;34:299–318. doi: 10.1108/03090560010311867. [DOI] [Google Scholar]

- Babiak K, Trendafilova S. CSR and environmental responsibility: Motives and pressures to adopt green management practices. Corporate Social Responsibility and Environmental Management. 2011;18:11–24. doi: 10.1002/csr.229. [DOI] [Google Scholar]

- Barkemeyer R, Holt D, Preuss L, Tsang S. What happened to the ‘development’ in sustainable development? Business guidelines two decades after brundtland. Sustainable Development. 2014;22:15–32. doi: 10.1002/sd.521. [DOI] [Google Scholar]

- Beltratti A, Corvino G. Why are insurance companies different? The limits of convergence among financial institutions. The Geneva Papers on Risk and Insurance - Issues and Practice. 2008;33:363–388. doi: 10.1057/gpp.2008.13. [DOI] [Google Scholar]

- Bennett R. Marketing and competitive advantage, How to satisfy the customer, profitably. Bank Marketing. 1992;24:36–38. [Google Scholar]

- Bertoni F, Croce A. The Productivity of European Life Insurers: Best-Practice Adoption vs. Innovation. The Geneva Papers on Risk and Insurance - Issues and Practice. 2011;36:165–185. doi: 10.1057/gpp.2011.1. [DOI] [Google Scholar]

- Bharadwaj AS. A resource-based perspective on information technology capability and firm performance: An empirical investigation. MIS Quarterly. 2000;24:169–196. doi: 10.2307/3250983. [DOI] [Google Scholar]

- Bican, P.M., Brem, A. (2020) Digital business model, digital transformation, digital entrepreneurship: Is there a sustainable “Digital”? 12, 5239.

- Bohnert A, Fritzsche A, Gregor S. Digital agendas in the insurance industry: The importance of comprehensive approaches†. The Geneva Papers on Risk and Insurance - Issues and Practice. 2019;44:1–19. doi: 10.1057/s41288-018-0109-0. [DOI] [Google Scholar]

- Bömer M, Maxin H. Why fintechs cooperate with banks—Evidence from germany. Zeitschrift Für Die Gesamte Versicherungswissenschaft. 2018;107:359–386. doi: 10.1007/s12297-018-0421-6. [DOI] [Google Scholar]

- Bons RWH, Alt R, Lee HG, Weber B. Banking in the Internet and mobile era. Electronic Markets. 2012;22:197–202. doi: 10.1007/s12525-012-0110-6. [DOI] [Google Scholar]

- Boot AWA. Relationship banking: what do we know? Journal of Financial Intermediation. 2000;9:7–25. doi: 10.1006/jfin.2000.0282. [DOI] [Google Scholar]

- Bopp RE. Climate change and reputation in the financial services sector. In: Walker T, Gramlich D, Bitar M, Fardnia P, editors. Ecological, societal, and technological risks and the financial sector. Springer International Publishing; 2020. pp. 225–242. [Google Scholar]

- Boyer M, Laffont J-J. Environmental risks and bank liability. European Economic Review. 1997;41:1427–1459. doi: 10.1016/S0014-2921(96)00034-7. [DOI] [Google Scholar]

- Breidbach CF, Maglio PP. Technology-enabled value co-creation: An empirical analysis of actors, resources, and practices. Industrial Marketing Management. 2016;56:73–85. doi: 10.1016/j.indmarman.2016.03.011. [DOI] [Google Scholar]

- Breidbach, C.F., Ranjan, S., (2017) How do fintech service platforms facilitate value co-creation? An analysis of twitter data, ICIS.

- Brundtland GH. Our common future—Call for action. Environmental Conservation. 1987;14:291–294. doi: 10.1017/S0376892900016805. [DOI] [Google Scholar]

- Brust, L., Breidbach, C.F., Antons, D., Salge, T.-O., (2017) Service-dominant logic and information systems research: a review and analysis using topic modeling. In: Thirty Eighth International Conference on Information Systems, South Korea 2017.

- Cerin P, Scholtens B. Linking responsible investments to societal influence: Motives, assessments and risks. Sustainable Development. 2011;19:71–76. doi: 10.1002/sd.508. [DOI] [Google Scholar]

- Chiorazzo V, D'Apice V, DeYoung R, Morelli P. Is the traditional banking model a survivor? Journal of Banking and Finance. 2018;97:238–256. doi: 10.1016/j.jbankfin.2018.10.008. [DOI] [Google Scholar]

- Choi J, Wang H. Stakeholder Relations and the Persistence of Corporate Financial Performance. Strategic Management Journal. 2009;30:895–907. doi: 10.1002/smj.759. [DOI] [Google Scholar]

- Christensen CM. The Ongoing process of building a theory of disruption. Journal of Product Innovation Management. 2006;23:39–55. doi: 10.1111/j.1540-5885.2005.00180.x. [DOI] [Google Scholar]

- Csiszar E, Heidrich GW. the question of reputational risk: Perspectives from an industry. The Geneva Papers on Risk and Insurance—Issues and Practice. 2006;31:382–394. doi: 10.1057/palgrave.gpp.2510096. [DOI] [Google Scholar]

- Cziesla, T., (2014) A Literature Review on Digital Transformation in the Financial Service Industry, Bled eConference, p. 18.

- Dehnert M. Sustaining the current or pursuing the new: Incumbent digital transformation strategies in the financial service industry. Business Research. 2020;13:1071–1113. doi: 10.1007/s40685-020-00136-8. [DOI] [Google Scholar]

- DeYoung R, Lang WW, Nolle DL. How the Internet affects output and performance at community banks. Journal of Banking & Finance. 2007;31:1033–1060. doi: 10.1016/j.jbankfin.2006.10.003. [DOI] [Google Scholar]

- Diener F, Špaček M. Digital Transformation in Banking: A Managerial Perspective on Barriers to Change. 2021;13:2032. [Google Scholar]

- Eklund J, Kapoor R. Pursuing the new while sustaining the current: incumbent strategies and firm value during the nascent period of industry change. Organization Science. 2019;30:383–404. doi: 10.1287/orsc.2018.1229. [DOI] [Google Scholar]

- El Hilali W, El Manouar A, Janati Idrissi MA. Reaching sustainability during a digital transformation: A PLS approach. International Journal of Innovation Science. 2020;12:52–79. doi: 10.1108/IJIS-08-2019-0083. [DOI] [Google Scholar]

- Emre, T., Ayberk, S., (2020) The effects of digital transformation on organizations. In: Umit, H. (Ed.), Handbook of Research on Strategic Fit and Design in Business Ecosystems. IGI Global, Hershey, PA, USA, pp. 259–288.

- Ertugrul M, Hegde S. Corporate Governance Ratings and Firm Performance. Financial Management. 2009;38:139–160. doi: 10.1111/j.1755-053X.2009.01031.x. [DOI] [Google Scholar]

- Evangelinos KI, Nikolaou IE. Environmental accounting and the banking sector: A framework for measuring environmental-financial risks. International Journal of Services Sciences. 2009;2:366–380. doi: 10.1504/IJSSCI.2009.026547. [DOI] [Google Scholar]

- Fekete, A., Rhyner, J. (2020) Sustainable digital transformation of disaster risk—Integrating new types of digital social vulnerability and interdependencies with critical infrastructure. 12, 9324.

- Feroz AK, Zo H, Chiravuri A. Digital transformation and environmental sustainability: A review and research agenda. Sustainability. 2021;13(3):1530. doi: 10.3390/su13031530. [DOI] [Google Scholar]

- Forcadell FJ, Aracil E, Ubeda F. Using reputation for corporate sustainability to tackle banks digitalization challenges. Business Strategy and the Environment. 2020;29:2181–2193. doi: 10.1002/bse.2494. [DOI] [Google Scholar]

- Francis BB, Hasan I, Küllü AM, Zhou M. Should banks diversify or focus? Know thyself: The role of abilities. Economic Systems. 2018;42:106–118. doi: 10.1016/j.ecosys.2017.12.001. [DOI] [Google Scholar]

- Gimpel H, Rau D, Röglinger M. Understanding FinTech start-ups—A taxonomy of consumer-oriented service offerings. Electronic Markets. 2018;28:245–264. doi: 10.1007/s12525-017-0275-0. [DOI] [Google Scholar]

- Garg H. A novel improved accuracy function for interval valued Pythagorean fuzzy sets and its applications in the decision making process. International Journal of Intelligent Systems. 2017;32:1247–1260. doi: 10.1002/int.21898. [DOI] [Google Scholar]

- Hanelt A, Bohnsack R, Marz D, Antunes Marante C. A systematic review of the literature on digital transformation: Insights and implications for strategy and organizational change. Journal of Management Studies. 2021;58:1159–1197. doi: 10.1111/joms.12639. [DOI] [Google Scholar]

- He J, Huang Z, Mishra AR, Alrasheedi M. Developing a new framework for conceptualizing the emerging sustainable community-based tourism using an extended interval-valued Pythagorean fuzzy SWARA-MULTIMOORA. Technological Forecasting and Social Change. 2021 doi: 10.1016/j.techfore.2021.120955. [DOI] [Google Scholar]

- Hezam IM, Mishra AR, Rani P, Cavallaro F, Saha A, Ali J, Strielkowski W, Štreimikienė D. A hybrid intuitionistic fuzzy-MEREC-RS-DNMA method for assessing the alternative fuel vehicles with sustainability perspectives. Sustainability. 2022;14:5463. doi: 10.3390/su14095463. [DOI] [Google Scholar]