Abstract

U.S. young adults face the largest student loan burden in history, rising income inequality, and economic uncertainty. Personal debt and other financial stressors have been associated with problematic drinking and mental health symptoms. In this paper, we investigated whether student loan debt was more strongly linked to problem drinking and mental health symptoms among those in lower positions of socioeconomic status (SES) and those who perceived greater [in]stability in their SES (SES-instability). Using data from a larger study of college graduates, we investigated SES, SES-instability, student debt, and their 2-way interactions on problematic drinking and mental health symptoms. College graduates (N = 331), who were two years post-graduation, completed measures assessing student debt, perceived SES, SES-instability, problematic drinking, and mental health symptoms (depression, anxiety, and stress). The hypotheses and data analysis plan were registered prior to conducting analyses. The expected unique, positive associations of SES-instability with problematic drinking and mental health symptoms were supported. SES was uniquely linked with problematic drinking only and in the opposite direction as predicted. Student debt was uniquely and positively linked to stress only. The expected interactions were largely supported for SES-instability and student debt—i.e., the associations of student debt with problematic drinking, anxiety, and stress were stronger (more positive) for those with greater SES-instability. The expected interactions for SES and student debt were null. Though data are cross-sectional and come from an educationally-privileged group, study findings provide preliminary evidence of links between young adult student loan debt, greater SES-instability, and their drinking/mental health.

Keywords: problematic drinking, mental health, student loans, college students, depression, anxiety

1. Introduction

U.S. young adults face complex financial circumstances. They have lower economic mobility (Tankersley, 2016) and are pessimistic about their likelihood of being better off than their parents (Wieczner, 2016). These perceptions are widely shared— >70% of US adults think young adults have it harder than their parents’ generation to save for the future, pay for college, and buy a home (Sechopoulos, 2022). College graduates are among the most economically-privileged young adults but are not immune from financial stressors. Here, we focus on one of them—student loan debt—and investigate their associations with problematic drinking and mental health symptoms.

Total U.S. student loan debt is more than $1.70 trillion (Hanson, 2022) and is frequently described as a looming crisis (Scott-Clayton, 2018) or catastrophe (Griffin, Riley, 2018). Individuals with a Bachelor’s degree owe more (median of $25,000) in student loans than those with lower levels of educational attainment (Cilluffo, 2019), and the burden of student loans (i.e., less advantageous lending terms, higher debt, and more difficulty repaying loans) is typically heaviest on students who are the least advantaged–Black, Hispanic and Latino/a/x, female, first-generation, and/or low-income students, and single parents (Hanson, 2022). Student loans can have negative financial consequences (e.g., defaulting or being delinquent on repayments; delaying or being unable to achieve financial goals). Taken together, it is, perhaps, unsurprising that 52% of students with student loan debt report feeling it was not worth it (Hanson, 2022).

Student loan debt also negatively affects well-being and mental health, even after controlling for other types of debt, assets, income, and demographic factors (see Kim & Chatterjee, 2019). Though research on student loan debt and problematic drinking is relatively scant, one study found a positive relationship between medical students’ student loan debt and the likelihood of problematic alcohol use or alcohol dependence (Jackson et al., 2016). That student loan debt might “spillover” to affect well-being and mental health is consistent with a review’s findings of a positive relationship between personal unsecured debt (a category that includes student loans) and physical and mental health and problematic substance use (see Richardson et al., 2013). The review’s key conclusion is that personal debt is an important, overlooked factor concerning its potential impact on mental health and problematic substance use.

There is a sizeable literature on disparities in financial stressors, unemployment, poverty and their intersection with race, gender, and ethnicity, related to problematic drinking (Collins, 2016; Cook et al., 2020; Mossakowski, 2008; Mulia et al., 2014), but financial factors – especially student loan debt – and their links to problematic drinking and mental health have been understudied by addictive behaviors researchers and psychologists who have a primary focus on college student and young adult drinking (ourselves included). This gap is especially problematic given the US student debt crisis, rising income inequality, and ongoing financial uncertainty. Macroeconomic factors, such as changes in state unemployment rates, appear linked to increases in problematic drinking in individuals living in those states (Dávalos et al., 2012). Similarly, severe economic losses (e.g., losing a job or a house during the 2008-2009 recession) have been linked to increases in alcohol dependence and negative alcohol-related consequences (Mulia et al., 2014). Moreover, the length of economic hardship has been linked to drinking heavily and drinking heavily more frequently (Mossakowski, 2008). Taken together, these findings suggest that recent college graduates (who are likely to have grown up during the 2008-2009 recession) who have student loan debt might be at increased risk of problematic drinking. The literature on financial stressors and their relations to mental health symptoms suggests that a similar pattern would also be found for mental health (e.g., Frasquilho et al., 2015).

Studies also suggest the importance of perceptions about finances. For example, perceptions of financial strain are associated with problematic drinking during economic crises and downturns (Dávalos et al., 2012; Kalousova & Burgard, 2014). Relatedly, perceived (vs. “objective”) economic strain is associated with greater mental health symptoms (Selenko & Batinic, 2011). This pattern extends to perceived socioeconomic status (SES), with several studies indicating that perceptions of one’s SES predict health outcomes and well-being as well or better than “objective” indicators of one’s SES (Adler et al., 2000; Cook et al., 2020; Singh-Manoux et al., 2005).

Given the above, we investigated whether young adults’ student loan debt (for brevity, student debt), their perceived SES position (for brevity, SES) and the perceived instability of their SES position (for brevity, SES-instability) were associated with problematic drinking and mental health symptoms. We expected that student debt and SES-instability would be positively associated with problematic drinking and mental health symptoms, whereas SES would be negatively associated with problematic drinking and mental health symptoms. We further expected that SES and SES-instability would moderate the positive relationship between student debt and problematic drinking and mental health symptoms. Specifically, we expected that there would be a stronger, more positive relationship between student debt and drinking and mental health symptoms in individuals with a lower (vs. higher) SES and with more (vs. less) SES-instability.

Study hypotheses were evaluated with data from the final assessment of a 2.5-year longitudinal study of college seniors who reported drinking hazardously in the last six months prior to their graduation (Lindgren et al., 2022). The final assessment was completed approximately two years post-graduation in Fall 2019—prior to the onset of the global COVID-19 pandemic, the pause on U.S. federal student loan payments, and proposed student debt relief (Hanson, 2022). We aimed to describe the sample with respect to student debt, SES, SES-instability, problematic drinking, and mental health symptoms and evaluate the associations between student debt, SES, and SES-instability on problematic drinking and mental health symptoms, including the predicted two-way interactions described above. The three-way interaction (student debt * SES * SES-instability) was evaluated on an exploratory basis. Hypotheses and the data analysis plan were registered prior to conducting analyses (see https://osf.io/f4wrj).

2. Material and Methods

2.1. Participants

The final assessment of the larger study1 was completed by 346 college graduates from a large public university in the U.S. Pacific Northwest. Of those, 331 completed items regarding student loans (from family/friends and/or government or other sources) and, thus, comprised the sample for the current study. The sample was 60% female, 39% male, and 1% identified as gender-diverse. Mean age was 23.97 years (SD = 0.96). The majority identified as White/Caucasian (62%), 20% as Asian, 13% as more than one race, and 2% as American Indian/Alaska Native/Native American. Less than 2% identified as members of the following groups: Black/African American, unknown, or preferred not to answer. The majority (91%) identified as not Hispanic or Latino/a/x; 7% identified as Hispanic or Latino/a/x; and 2% reported their ethnicity as unknown.

2.2. Measures

Student debt items were from the National Longitudinal Study of Youth 1997 (NLSY97, U.S. Bureau of Labor Statistics, n.d.). Items are from the “Asset” questionnaire and have been part of the NLSY97 since Round 7/2005. The first queried whether participants “received loans from parents, other relatives, or friends to help them attend a school or college?” If participants responded yes, they were asked to report the “total amount you owe altogether on these educational loans from family members or friends.” They were also asked whether they “received government-subsidized or other types of loans to attend a school or college?” If yes, they were asked to report “the total amount you owe altogether on these types of education loans.” Despite potential concerns about the accuracy of self-reported debt, research indicates that self-reports and credit reports of student debt are very similar (Houle, 2014; Houle & Warner, 2017).

Perceived SES was assessed via The MacArthur Scale of Subjective Social Status (Singh-Manoux et al., 2005). It is a single item displaying a ladder with ten rungs and asks, “Think of the ladder as representing where people stand in the United States, where would you place yourself on this ladder?” (10 being the highest, 1 being the lowest). It has been validated for use as a proxy for socioeconomic status (Adler et al., 2000; Singh-Manoux et al., 2005). A second item was created for the current study to assess perceived SES-instability. It asks, “How stable is your position on this ladder?” and uses a 7-point Likert response scale ranging from −3 (Very Unstable) to +3 (Very Stable) and was reverse-coded to reflect the degree of SES-instability.

Monthly income was used as a covariate in analyses and was assessed via a single, open-ended question that asked, “What is your monthly income from monies you make from work after taxes, financial checks, government assistance, and/or parental support?”

Problematic drinking was assessed via the Alcohol Use Disorders Identification Test (AUDIT, Babor et al., 2001). The AUDIT is a 10-item measure assessing past year’s alcohol use, dependence, and alcohol-related problems. Responses range from 0 to 4 and are summed to create a total score; higher scores indicate greater AUD risk. Cronbach’s α for this sample = .77.

Mental health symptoms were assessed via the Depression Anxiety Stress Scale-21 (DASS-21) (Lovibond & Lovibond, 1996). The DASS-21 has 21 items comprising three subscales. It evaluates symptoms of depression, anxiety, and stress over the last month and has been validated for use in clinical and non-clinical samples (Antony et al., 1998). Response values range from 0 (Not at all) to 3 (Most of the time). Cronbach’s α’s for this sample were: depression = .923; anxiety = .802; and stress = .880.

2.3. Procedures

Study procedures were approved by the university’s institutional review board. All participants provided informed consent. Procedures for the larger study are described in Lindgren et al. (2022).2 Assessments were online and given at approximately 4-month intervals. Three accuracy check questions (e.g., “To answer this question correctly, you must answer ‘Strongly disagree’”) were interspersed throughout this assessment to evaluate whether participants were attentive and responding accurately; 100% of the current sample responded accurately to all three items. Participants were compensated $30 for assessment completion. Additional bonus compensation was possible and depended on participants’ history of completing prior assessments.

2.4. Data analytic plan

Primary analyses consisted of a series of hierarchical generalized linear models (Hardin & Hilbe, 2018; McCabe et al., 2021). Separate models were tested for the four outcomes (problematic drinking [AUDIT scores] and mental health symptoms [depression, anxiety, and stress subscale scores]). Student debt, SES, and SES-instability were entered in Step 1 to evaluate main effects. Two 2-way product terms were added in Step 2 (student debt* SES and student debt * SES-instability) to evaluate SES as a moderator of the association of student loan burden and the given outcome variable. The three-way product term (student debt * SES * SES-instability) was also added in Step 3 to evaluate the three-way interaction. The two-way product term between SES and SES-instability was added at this step so that all three constituent two-way products were included in testing the three-way product. We neglected to mention this in the pre-registration. Also, in the pre-registration, we indicated we would include main effects and two-way interactions in Step 1. In retrospect, we recognized that the main effects would be of interest and not easily interpretable unless we put the main effects in Step 1 and two-way products in Step 2. Results presented in the tables include tests of coefficients at the steps in which they were added. Main effects and lower-order interactions were included in the models with higher-order interactions but are not shown in the table for parsimony. Monthly income was included as a covariate based on a helpful suggestion from reviewers.

The appropriate distributions for all outcomes were evaluated in preliminary analyses. Model fit comparisons were based on BIC values where each outcome was examined as a function of the main effects, with distribution specified as Gaussian, Poisson, or negative binomial. For all outcomes, the negative binomial model provided the best fit.

Negative binomial models are nonlinear log-linked models that provide parameter estimates representing expected changes in the log-transformed outcome. For nonlinear models, the expected change in the effect of a focal variable (e.g., student debt) on the outcome (e.g., AUDIT) as a function of another variable (e.g., SES) is not constant but dependent upon the values of all predictors in the model. A significant product term on the log-transformed scale does not necessarily indicate a significant interaction for the outcome in its natural units, which is typically the question of primary interest (Kim & McCabe, 2022). For the interactions, we used a partial derivative framework to show the average marginal effect of student loans at specific values of SES instability and conducted tests of the second cross-partial derivative, which provides a direct test of the interaction (i.e., the average marginal effect of one variable as a function of another (Karaca-Mandic et al., 2012; Kim & McCabe, 2022; & McCabe et al., 2021) provide details about this approach).

3. Results

Overall, 44.7% of the sample reported having student debt, with 29.6% of the sample reporting having loans from government-subsidized or other sources, 4.2% reporting loans from relatives and/or friends, and 10% reporting having government-subsidized or other loans and having loans from relatives and/or friends. All participants (because of the larger study design) had at least a bachelor’s degree, and the observed rates for student debt were roughly equivalent to national statistics (i.e., 49% of those with a bachelor’s degree report having loans (Cilluffo, 2019)). Among the 148 participants who reported having student debt, the average total amount reported was $44,445 (SD=$46,841)—roughly equivalent with national statistics (i.e., average debt of $40,780, including private and governmental loans (Hanson, 2022). Table 1 reports descriptive statistics for student debt across the entire sample.

Table 1.

Descriptive statistics and bivariate correlations for all study variables.

| Mean | SD | 1 | 2 | 3 | 4 | 5 | 6 | 7 | |

|---|---|---|---|---|---|---|---|---|---|

| 1. Monthly Income $1000s | 3.49 | 2.83 | - | ||||||

| 2. Student Debt $1000s | 19.87 | 38.30 | −0.116* | - | |||||

| 3. SES | 6.39 | 1.56 | 0.222*** | −0.014 | - | ||||

| 4. SES-Instability | −1.72 | 1.29 | −0.240*** | 0.101 | −0.429*** | - | |||

| 5 . AUDIT | 8.18 | 4.85 | 0.035 | 0.177** | 0.156** | 0.080 | - | ||

| 6. Depression | 7.04 | 8.65 | −0.092 | 0.112* | −0.210*** | 0.375*** | 0.242*** | - | |

| 7. Anxiety | 4.85 | 5.82 | −0.077 | 0.211*** | −0.154** | 0.242*** | 0.303*** | 0.624*** | - |

| 8. Stress | 9.72 | 8.37 | −0.116* | 0.221*** | −0.198*** | 0.308*** | 0.257*** | 0.702*** | 0.742*** |

Note. N was 331 for all variables and correlations. SD = standard deviation. Monthly Income $1000s = amount of self-reported monthly post-tax income from all sources and was capped at $14,000 (4% of participants reported monthly income above $14,000). Student Debt $ 1000s = amount of self-reported student debt from all sources (i.e., from family/friends or government). SES = perceived socioeconomic status; higher values indicate perceiving self to have higher status position on the MacArthur Scale of Subjective Social Status. SES-instability = perceived instability in one’s status position; higher values indicate greater instability. AUDIT = scores on the Alcohol Use Disorder Identification Test; higher scores indicate greater AUD risk; and 51% of the sample had scores ≥ 8, which indicate risk for hazardous drinking. Depression, anxiety, and stress represents scores on the depression, anxiety, and stress subscales of the DASS-21; higher scores = greater symptom severity. When multiplied by two, subscale scores can used to identity levels of severity; 31% of the sample scored above the “normal” range for depression (≥10), 26% were above “normal” for anxiety (≥ 6), and 8% were above “normal” for stress (≥ 15).

p<.001.

p<.01.

p<.05.

Please see Table 1 for descriptive statistics and zero-order correlations among study variables. Of note, participants, on average, reported being on the sixth rung of the 10-rung SES ladder, and SES-instability level was, on average, between “a little” and “somewhat” stable. Table 1’s note provides detailed information about the sample’s risk/severity ranges with respect to AUDIT scores and DASS-21 subscales.

Given the large skew of loan amounts and that roughly 55% of participants reported no student debt, we stated in the pre-registration that we would use a dichotomous loan variable for primary analyses. In retrospect, a dichotomous variable for student debt seemed inadequate.3 It would not account for the potential effects of having greater (vs. smaller) amounts of debt. Thus, we constructed an ordinal variable with four categories (no loans, < $25K, >=$25K & <$50K, >=$50K & <$75K, and >=$75K) for use in analyses.

Tests of parameter estimates of hierarchical negative binomial models are provided in Table 2. Step 1 results were relatively consistent across all four outcomes. Student debt was positively and uniquely associated with stress but was not uniquely associated with AUDIT scores, depression, or anxiety. SES-instability was uniquely associated with all four outcomes. A one-unit increase in SES-instability was associated with increases of 8.6% in AUDIT, 33.4% in depression, 17.2% in anxiety, and 14.6% in stress scores. SES was not uniquely associated with depression, anxiety, or stress scores but was uniquely associated with AUDIT scores in the opposite direction as expected—each unit increase in SES was associated with a 9.2% increase in AUDIT scores.

Table 2.

Negative binomial regression results.

| DV | Step | Predictor | b | se | z | p | irr |

|---|---|---|---|---|---|---|---|

| AUDIT | Step 1 | Intercept | 1.618 | 0.159 | 10.20 | <0.001 | 5.042 |

| Monthly Income | 0.007 | 0.015 | 0.45 | 0.655 | 1.007 | ||

| Student Debt (SD) | 0.043 | 0.033 | 1.31 | 0.192 | 1.044 | ||

| SES | 0.088 | 0.027 | 3.30 | 0.001 | 1.092 | ||

| SES-instability | 0.083 | 0.031 | 2.65 | 0.008 | 1.087 | ||

|

| |||||||

| Step 2 | SD*SES | 0.025 | 0.019 | 1.33 | 0.184 | 1.025 | |

| SD*SES-instability | 0.098 | 0.018 | 5.34 | <0.001 | 1.103 | ||

|

| |||||||

| Step 3 | SES*SES-instability | −0.011 | 0.018 | −0.60 | 0.548 | 0.989 | |

| SD*SES*SES-instability | 0.004 | 0.009 | 0.40 | 0.686 | 1.004 | ||

|

| |||||||

| Depression | Step 1 | Intercept | 2.547 | 0.286 | 8.90 | <0.001 | 12.767 |

| Monthly Income | 0.007 | 0.032 | 0.21 | 0.832 | 1.007 | ||

| Student Debt (SD) | 0.022 | 0.064 | 0.34 | 0.731 | 1.022 | ||

| SES | −0.034 | 0.050 | −0.68 | 0.494 | 0.966 | ||

| SES-instability | 0.288 | 0.051 | 5.68 | <0.001 | 1.333 | ||

|

| |||||||

| Step 2 | SD*SES | −0.038 | 0.040 | −0.94 | 0.347 | 0.963 | |

| SD*SES-instability | 0.077 | 0.050 | 1.54 | 0.123 | 1.080 | ||

|

| |||||||

| Step 3 | SES*SES-instability | 0.006 | 0.033 | 0.17 | 0.863 | 1.006 | |

| SD*SES*SES-instability | 0.014 | 0.023 | 0.64 | 0.522 | 1.015 | ||

|

| |||||||

| Anxiety | Step 1 | Intercept | 2.107 | 0.282 | 7.48 | <0.001 | 8.226 |

| Monthly Income | −0.002 | 0.032 | −0.06 | 0.951 | 0.998 | ||

| Student Debt (SD) | 0.106 | 0.064 | 1.64 | 0.100 | 1.111 | ||

| SES | −0.059 | 0.050 | −1.18 | 0.240 | 0.943 | ||

| SES-instability | 0.159 | 0.055 | 2.88 | 0.004 | 1.172 | ||

|

| |||||||

| Step 2 | SD*SES | 0.011 | 0.040 | 0.27 | 0.790 | 1.011 | |

| SD*SES-instability | 0.121 | 0.047 | 2.61 | 0.009 | 1.129 | ||

|

| |||||||

| Step 3 | SES*SES-instability | −0.004 | 0.037 | −0.11 | 0.915 | 0.996 | |

| SD*SES*SES-instability | 0.033 | 0.020 | 1.62 | 0.106 | 1.033 | ||

|

| |||||||

| Stress | Step 1 | Intercept | 2.634 | 0.202 | 13.05 | <0.001 | 13.933 |

| Monthly Income | −0.011 | 0.023 | −0.50 | 0.618 | 0.989 | ||

| Student Debt (SD) | 0.111 | 0.046 | 2.39 | 0.017 | 1.117 | ||

| SES | −0.033 | 0.035 | −0.96 | 0.338 | 0.967 | ||

| SES-instability | 0.136 | 0.038 | 3.59 | <0.001 | 1.146 | ||

|

| |||||||

| Step 2 | SD*SES | −0.002 | 0.030 | −0.07 | 0.945 | 0.998 | |

| SD*SES-instability | 0.076 | 0.034 | 2.23 | 0.026 | 1.079 | ||

|

| |||||||

| Step 3 | SES*SES-instability | −0.025 | 0.025 | −1.02 | 0.306 | 0.975 | |

| SD*SES*SES-instability | 0.026 | 0.016 | 1.65 | 0.100 | 1.026 | ||

Note. N = 331. Monthly Income = amount of self-reported monthly post-tax income from all sources. Student debt = total self-reported student loan debt from all sources and was coded 0 (no loans), 1 (with loans < $25K), 2 (>=$25K & <$75K), and 3 >=$75K. SES = perceived socioeconomic status; higher values indicate perceiving self to have higher status position on the MacArthur Scale of Subjective Social Status. SES-instability = perceived instability in one’s status position; higher values indicate greater instability. AUDIT = scores on the Alcohol Use Disorder Identification Test; higher scores indicate greater AUD risk. Depression, anxiety, and stress represents scores on the depression, anxiety, and stress subscales of the DASS-21; higher scores = greater symptom severity. Significant effects are bolded.

Step 2 results revealed significant product terms for student debt * SES-instability for AUDIT, anxiety, and stress. Interactions associated with significant product terms were evaluated by examining whether the average marginal effect (AME) of student debt on outcomes varied as a function of SES-instability via tests of the second cross-partial derivatives (see Kim & McCabe, 2022). Please see Table 3 and Figure 1.

Table 3.

Average Marginal Effects (AME) of student loan debt in two-way interactions via tests of the second cross-partial derivatives.

| DV | Effect | ∂y∂x | SE | z | p | LCI | HCI |

|---|---|---|---|---|---|---|---|

| Audit | ∂/∂Studcnt Debt | 0.304 | 0.266 | 1.14 | 0.253 | −0.218 | 0.825 |

|

| |||||||

| @SESI=−3 | −0.706 | 0.335 | −2.11 | 0.035 | −1.363 | −0.049 | |

| @SESI=−2 | 0.039 | 0.266 | 0.14 | 0.885 | −0.482 | 0.559 | |

| @SESI=−1 | 0.869 | 0.268 | 3.24 | 0.001 | 0.344 | 1.394 | |

| @SESI= 0 | 1.820 | 0.352 | 5.17 | <0.001 | 1.13 | 2.51 | |

| @SESI= 1 | 2.942 | 0.521 | 5.65 | <0.001 | 1.922 | 3.963 | |

|

|

|||||||

| ∂^2/∂SI@ Student Debt | 0.855 | 0.163 | 5.25 | <0.001 | 0.536 | 1.175 | |

|

| |||||||

| Anxiety | ∂/∂ Student Debt | 0.685 | 0.359 | 1.91 | 0.057 | −0.019 | 1.389 |

| @SESI=−3 | −0.273 | 0.399 | −0.68 | 0.494 | −1.054 | 0.509 | |

| @SESI=−2 | 0.223 | 0.321 | 0.70 | 0.486 | −0.405 | 0.852 | |

| @SESI=−1 | 0.879 | 0.336 | 2.62 | 0.009 | 0.22 | 1.537 | |

| @SESI= 0 | 1.769 | 0.539 | 3.28 | 0.001 | 0.712 | 2.825 | |

| @SESI= 1 | 3.008 | 1.011 | 2.97 | 0.003 | 1.025 | 4.99 | |

|

|

|||||||

| ∂^2/∂SI@ Student Debt | 0.745 | 0.301 | 2.48 | 0.013 | 0.155 | 1.334 | |

|

| |||||||

| Stress | ∂/∂ Student Debt | 1.268 | 0.462 | 2.75 | 0.006 | 0.364 | 2.173 |

| @SESI=−3 | 0.036 | 0.567 | 0.06 | 0.949 | −1.076 | 1.148 | |

| @SESI=−2 | 0.725 | 0.461 | 1.57 | 0.116 | −0.179 | 1.628 | |

| @SESI=−1 | 1.621 | 0.487 | 3.33 | 0.001 | 0.665 | 2.576 | |

| @SESI= 0 | 2.790 | 0.774 | 3.60 | <0.001 | 1.273 | 4.308 | |

| @SESI= 1 | 4.323 | 1.349 | 3.21 | 0.001 | 1.68 | 6.966 | |

|

|

|||||||

| ∂^2/∂SI@ Student Debt | 0.948 | 0.374 | 2.53 | 0.011 | 0.214 | 1.681 | |

Note. N = 331. Student debt = total self reported student loan debt from all sources and was coded 0 (no loans), 1 (with loans < $25K), 2 ( >=$25K & <$75K), and 3 >=$75K. SESI= SES-instability = perceived instability in one’s SES; higher values indicate greater instability. AUDIT = scores on the Alcohol Use Disorder Identification Test; higher scores indicate greater AUD risk. Anxiety and stress represent scores on the anxiety and stress subscales of the DASS-21; higher scores = greater symptom severity. ∂y∂x = partial derivative (average marginal effect). Significant effects are bolded.

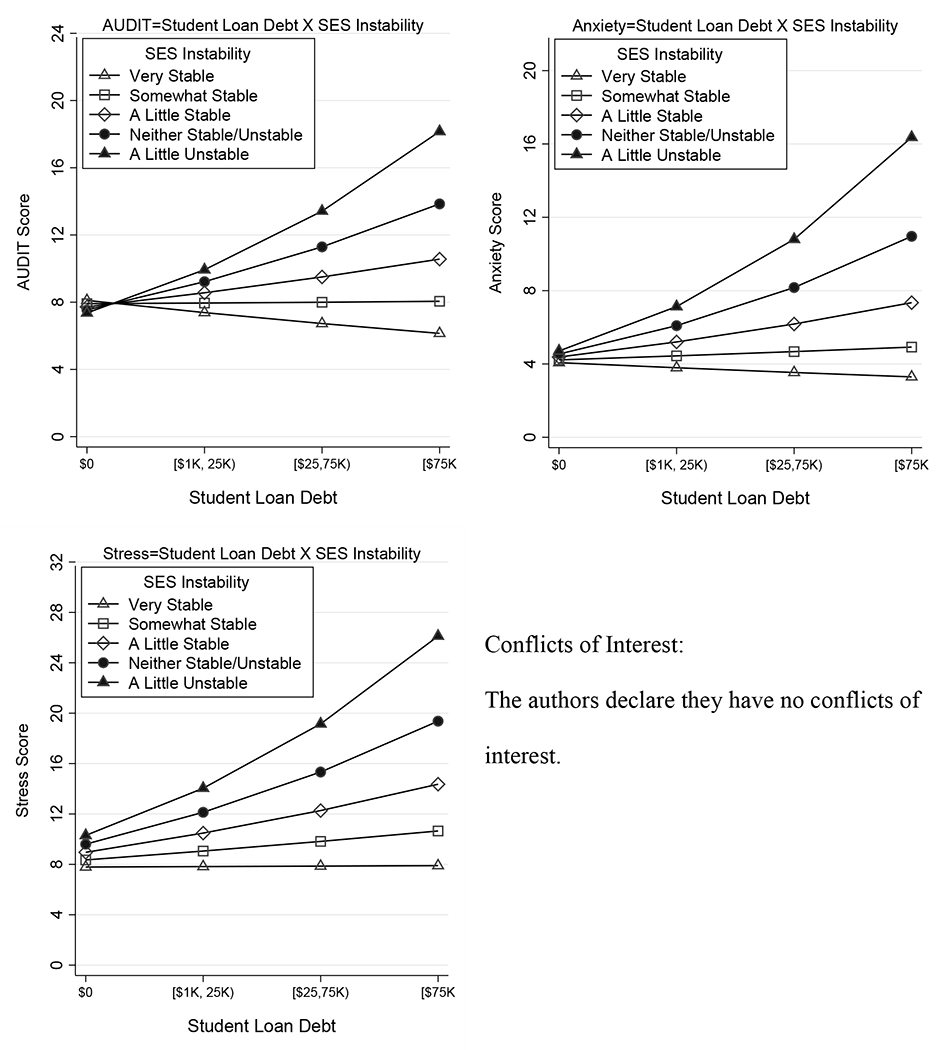

Figure 1.

Two-way interactions of student loan debt and SES-instability for AUDIT scores, anxiety, and stress.

Figure 1 (top right, top left, and bottom) shows the interactions between student debt and SES-instability in predicting AUDIT scores, anxiety, and stress, respectively. Average marginal effects of student loans on outcomes are presented for SES-instability values ranging from very stable (−3) to a little stable (1). Similar patterns were observed for all three interactions. For participants who felt their position was highly stable, student loan amount was either negatively or not significantly associated with outcomes. At increasing levels of SES-instability, the association between student loans and outcomes became increasingly and significantly positive. Furthermore, for all interactions, the average marginal effects at each value of SES-instability were significantly different from each other (p’s ranged between <0.001 and 0.020).

4. Discussion

We investigated the links between financial stressors—student debt, SES, and SES-instability—and problematic drinking and mental health symptoms in a U.S. young adult sample. SES-instability had a consistent link with problematic drinking and mental health symptoms: even after controlling for student debt, SES, and monthly income. SES, however, was only associated with problematic drinking and in the opposite direction as expected. That higher SES was associated with greater problematic drinking may reflect our SES variable (which provides a gestalt of SES vs. a fine-grained look) and the AUDIT (which includes items assessing quantity/frequency of consumption, dependence, and problems). Collins’s (2016) review indicates a positive association between some socioeconomic factors and the quantity/frequency of alcohol consumption.

Contrary to expectations, student debt was only associated with stress. The specificity of this relationship may reflect that student debt (like other debt) is commonly characterized as a stressor and that stressors, in and of themselves, do not necessarily lead to depression, anxiety, and problematic drinking. Further, this finding was qualified by the SES-instability by student debt interaction (observed for all outcomes but depression). Generally, having more student debt was linked to more problematic outcomes but only in specific circumstances—experiencing SES-instability. That this interaction was not observed for depression may reflect that rumination about the past is a key factor in depression (Nolen-Hoeksema, 1991), whereas SES-instability can be conceptualization as concern about one’s current and future circumstances. Finally, we note the null findings for the SES by student debt interaction. Though unexpected, they are consistent with findings that perceptions of financial strain are as or more important than objective indicators of financial strain (Dávalos et al., 2012; Kalousova & Burgard, 2014).

Ultimately, study findings indicate that the combination of student debt and SES-instability is risky for young adult college graduates, which has important implications for addictive behaviors research, interventions, and policies. Regarding the former, the current study’s limitations provide helpful guidance for a future research agenda. It is a secondary analysis of cross-sectional data from a larger study not designed for this purpose. The sample is educationally-privileged, majority white and non-Hispanic/Latino/a/x, and individuals had to meet criteria for hazardous drinking risk during their senior year of college. Student debt and SES were not assessed until the final assessment (approximately two years post-college), and those assessments, though validated (Adler et al., 2000; Bureau of Labor Statistics, 2019; Singh-Manoux et al., 2005), are self-reported and relatively high-level. The larger study did not assess key variables associated with greater student debt burden (i.e., first-generation college student, single parent, etc.), and the sample size, though >300, is not adequate to evaluate the characteristics we did assess (e.g., race, ethnicity). Longitudinal studies and natural experiments specifically designed with the goal of investigating student debt, problematic drinking, and mental health will be essential to determine the temporal relationship among these factors and to evaluate causality. Future studies should include secondary programs (whether college, community college, technical schools, or for-profit training programs) and include current students, graduates, and individuals who dropped out. Individuals whose alcohol consumption was lower or less problematic should be included to evaluate the potential impact of financial stressors over time. Finally, larger, more diverse samples and more fine-grained assessments will allow for a more nuanced investigation of student loans themselves (e.g., types, terms of loans), financial demographics (e.g., family or household income), and other financial stressors and a better understanding of their impact on particular groups (e.g., minoritized groups, first-generation college students, students who are parents).

Should findings replicate and extend more broadly to current and former students, assessing financial stressors will be important for intervention and policies. Doing so may help identify additional individuals at risk for problematic drinking and mental health concerns and suggest additional avenues to reduce those risks (i.e., resources for ameliorating student loan burden and/or financial stressors). Further, policies (e.g., the freeze on federal loans set to expire in December 2022; federal student debt relief) may function, unwittingly, as substance use and/or mental health interventions.

Highlights:

US young adults face a heavy student loan burden & socioeconomic instability

We tested if they were linked to problematic drinking & mental health symptoms

Positive links between instability and drinking, anxiety and stress were found

Relationships were stronger at higher levels of perceived socioeconomic instability

Acknowledgments

Funding was provided by National Institute on Alcohol Abuse and Alcoholism (NIAAA), Grant Number: R01 AA024732 (PI: Lindgren). NIAAA played no role in study design; the collection, analysis, and interpretation of data; the writing of this paper; or the decision to submit this paper for publication.

Footnotes

Publisher's Disclaimer: This is a PDF file of an unedited manuscript that has been accepted for publication. As a service to our customers we are providing this early version of the manuscript. The manuscript will undergo copyediting, typesetting, and review of the resulting proof before it is published in its final form. Please note that during the production process errors may be discovered which could affect the content, and all legal disclaimers that apply to the journal pertain.

Author CRediT statement

Kristen Lindgren: Conceptualization, Funding acquisition, Investigation, Methodology, Writing - original draft, Writing - review & editing. Ty Tristao: Data curation, Project administration, Writing - original draft. Clayton Neighbors: Conceptualization, Investigation, Formal analysis, Visualization, Roles/Writing - original draft, Writing - review & editing.

The demographic composition of the sample at the final assessment (specifically, gender, race, and ethnicity) was roughly equivalent to the sample at the baseline assessment. Final assessment completers (n = 346) and non-completers (n = 76) did not differ with respect to age (Z = −.53, p = 0.599), gender identity (Z = 0.68, p = 0.793), ethnicity (Z =−.34, p = 0.732), or race (χ2[df=3, N=407] = 2.83. p = 0.419). Detailed information about larger study, including demographics and retention over time, is provided in the study’s primary aims paper (Lindgren et al., 2022).

Eligibility criteria for the larger study included: expecting to graduate within the next six months, scoring ≥ 8 on the AUDIT, being between ages 18-25, and fluency in English.

We appreciate reviewers for raising this concern.

References

- Adler NE, Epel ES, Castellazzo G, & Ickovics JR (2000). Relationship of subjective and objective social status with psychological and physiological functioning: Preliminary data in healthy, White women. Health Psychology, 19(6), 586–592. 10.1037/0278-6133.19.6.586 [DOI] [PubMed] [Google Scholar]

- Antony MM, Bieling PJ, Cox BJ, Enns MW, & Swinson RP (1998). Psychometric properties of the 42-item and 21-item versions of the Depression Anxiety Stress Scales in clinical groups and a community sample. Psychological Assessment, 10(2), 176–181. 10.1037/1040-3590.10.2.176 [DOI] [Google Scholar]

- Babor TF, Higgins-Biddle JC, Saunders JB, & Monteiro MG (2001). The Alcohol-use disorders Identification Test (AUDIT): Guidelines for use in primary care (2nd ed.). World Health Organization, Department of Mental Health and Substance Dependence. [Google Scholar]

- Bureau of Labor Statistics, U. S. D. of L. (2019). U.S. National Longitudinal Survey of Youth 1979 cohort, 1979-2016 (rounds 1-27). Center for Human Resource Research (CHRR), The Ohio State University. [Google Scholar]

- Cilluffo A (2019). Five facts about student loans. http://www.pewresearch.org/fact-tank/2017/08/24/5-facts-about-student-loans/.

- Collins SE (2016). Associations Between Socioeconomic Factors and Alcohol Outcomes. Alcohol Research: Current Reviews, 38(1), 83–94. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Cook WK, Mulia N, & Li L (2020). Subjective Social Status and Financial Hardship: Associations of Alternative Indicators of Socioeconomic Status with Problem Drinking in Asian Americans and Latinos. Substance Use & Misuse, 55(8), 1246–1256. 10.1080/10826084.2020.1732423 [DOI] [PMC free article] [PubMed] [Google Scholar]

- Dávalos ME, Fang H, & French MT (2012). EASING THE PAIN OF AN ECONOMIC DOWNTURN: MACROECONOMIC CONDITIONS AND EXCESSIVE ALCOHOL CONSUMPTION: MACROECONOMIC CONDITIONS AND EXCESSIVE ALCOHOL CONSUMPTION. Health Economics, 21(11), 1318–1335. 10.1002/hec.1788 [DOI] [PMC free article] [PubMed] [Google Scholar]

- Frasquilho D, Matos MG, Salonna F, Guerreiro D, Storti CC, Gaspar T, & Caldas-de-Almeida JM (2015). Mental health outcomes in times of economic recession: A systematic literature review. BMC Public Health, 16(1), 115. 10.1186/s12889-016-2720-y [DOI] [PMC free article] [PubMed] [Google Scholar]

- Griffin Riley. (2018, October 17). U.S. Student Debt May Be a Crisis Now. Soon It Will Be a Catastrophe. Bloomberg. https://www.bloomberg.com/news/articles/2018-10-17/the-student-loan-debt-crisis-is-about-to-get-worse [Google Scholar]

- Hanson M (2022, October 26). Student Loan Debt Statistics. Education Data Initiative. https://educationdata.org/student-loan-debt-statistics [Google Scholar]

- Hardin JW, & Hilbe JM (2018). Generalized linear models and extensions (Fourth edition). Stata Press. [Google Scholar]

- Houle JN (2014). Disparities in Debt: Parents’ Socioeconomic Resources and Young Adult Student Loan Debt. Sociology of Education, 87(1), 53–69. 10.1177/0038040713512213 [DOI] [Google Scholar]

- Houle JN, & Warner C (2017). Into the Red and Back to the Nest? Student Debt, College Completion, and Returning to the Parental Home among Young Adults. Sociology of Education, 90(1), 89–108. 10.1177/0038040716685873 [DOI] [PMC free article] [PubMed] [Google Scholar]

- Jackson ER, Shanafelt TD, Hasan O, Satele DV, & Dyrbye LN (2016). Burnout and Alcohol Abuse/Dependence Among U.S. Medical Students. Academic Medicine, 91(9), 1251. 10.1097/ACM.0000000000001138 [DOI] [PubMed] [Google Scholar]

- Kalousova L, & Burgard SA (2014). Unemployment, measured and perceived decline of economic resources: Contrasting three measures of recessionary hardships and their implications for adopting negative health behaviors. Social Science & Medicine (1982), 106, 28–34. 10.1016/j.socscimed.2014.01.007 [DOI] [PubMed] [Google Scholar]

- Karaca-Mandic P, Norton EC, & Dowd B (2012). Interaction Terms in Nonlinear Models. Health Services Research, 47(1pt1), 255–274. 10.1111/j.1475-6773.2011.01314.x [DOI] [PMC free article] [PubMed] [Google Scholar]

- Kim DS, & McCabe CJ (2022). The partial derivative framework for substantive regression effects. Psychological Methods, 27(1), 121–141. 10.1037/met0000440 [DOI] [PubMed] [Google Scholar]

- Kim J, & Chatterjee S (2019). Student Loans, Health, and Life Satisfaction of US Households: Evidence from a Panel Study. Journal of Family and Economic Issues, 40(1), 36–50. 10.1007/s10834-018-9594-3 [DOI] [Google Scholar]

- Lindgren KP, Baldwin SA, Peterson KP, Ramirez JJ, Teachman BA, Kross E, Wiers RW, & Neighbors C (2022). Maturing Out: Between- and Within-Persons Changes in Social-Network Drinking, Drinking Identity, and Hazardous Drinking Following College Graduation. Clinical Psychological Science, 216770262210829. 10.1177/21677026221082957 [DOI] [PMC free article] [PubMed] [Google Scholar]

- Lovibond SH, & Lovibond PF (1996). Manual for the depression anxiety stress scales. Psychology Foundation of Australia. [Google Scholar]

- McCabe CJ, Halvorson MA, King KM, Cao X, & Kim DS (2021). Interpreting Interaction Effects in Generalized Linear Models of Nonlinear Probabilities and Counts. Multivariate Behavioral Research, 1–27. 10.1080/00273171.2020.1868966 [DOI] [PMC free article] [PubMed] [Google Scholar]

- Mossakowski KN (2008). Is the duration of poverty and unemployment a risk factor for heavy drinking? Social Science & Medicine, 67(6), 947–955. 10.1016/j.socscimed.2008.05.019 [DOI] [PubMed] [Google Scholar]

- Mulia N, Zemore SE, Murphy R, Liu H, & Catalano R (2014). Economic Loss and Alcohol Consumption and Problems During the 2008 to 2009 U.S. Recession. Alcoholism: Clinical and Experimental Research, 38(4), 1026–1034. 10.1111/acer.12301 [DOI] [PMC free article] [PubMed] [Google Scholar]

- Nolen-Hoeksema S (1991). Responses to depression and their effects on the duration of depressive episodes. Journal of Abnormal Psychology, 100(4), 569–582. 10.1037/0021-843X.100A569 [DOI] [PubMed] [Google Scholar]

- Richardson T, Elliott P, & Roberts R (2013). The relationship between personal unsecured debt and mental and physical health: A systematic review and meta-analysis. Clinical Psychology Review, 33(8), 1148–1162. 10.1016/j.cpr.2013.08.009 [DOI] [PubMed] [Google Scholar]

- Scott-Clayton J (2018). The looming student loan default crisis is worse than we thought. Evidence Speaks Reports, 2, 10. [Google Scholar]

- Sechopoulos S (2022, February 28). Most in the U.S. say young adults today face more challenges than their parents’ generation in some key areas. https://www.pewresearch.org/fact-tank/2022/02/28/most-in-the-u-s-say-young-adults-today-face-more-challenges-than-their-parents-generation-in-some-key-areas/

- Selenko E, & Batinic B (2011). Beyond debt. A moderator analysis of the relationship between perceived financial strain and mental health. Social Science & Medicine, 73(12), 1725–1732. 10.1016/j.socscimed.2011.09.022 [DOI] [PubMed] [Google Scholar]

- Singh-Manoux A, Marmot MG, & Adler NE (2005). Does Subjective Social Status Predict Health and Change in Health Status Better Than Objective Status?: Psychosomatic Medicine, 67(6), 855–861. 10.1097/01.psy.0000188434.52941.a0 [DOI] [PubMed] [Google Scholar]

- Tankersley J (2016, Debember). American Dream collapsing for young adults, study says, as odds plunge that children will earn more than their parents. Washington Post. https://www.washingtonpost.com/news/wonk/wp/2016/12/08/american-dream-collapsing-for-young-americans-study-says-finding-plunging-odds-that-children-earn-more-than-their-parents/ [Google Scholar]

- U.S. Bureau of Labor Statistics. (n.d.). National Longitudinal Survey of Youth 1997. Questionnaires (Rounds 1-19). Retrieved September 14, 2022, from https://www.nlsinfo.org/content/cohorts/nlsy97/other-documentation/questionnaires [Google Scholar]

- Wieczner J (2016, March 1). Millennial Workers: We’ll Be Worse Off Than Our Parents’ Generation | Fortune. Fortune. http://fortune.com/2016/03/01/millennials-worse-parents-retirement/