Abstract

Over the past decade, rising youth use of e-cigarettes and other electronic nicotine delivery systems (ENDS) has contributed to aggressive regulation by state and local governments. Between 2010 and mid-2019, ten states and two large counties adopted ENDS taxes. We use two large national surveys (Monitoring the Future and the Youth Risk Behavior Surveillance System) to estimate the impact of ENDS taxes on youth tobacco use. We find that ENDS taxes reduce youth ENDS consumption, with estimated ENDS tax elasticities of −0.06 to −0.21. However, we estimate sizable positive cigarette cross-tax effects, suggesting economic substitution between cigarettes and ENDS for youth. These substitution effects are particularly large for frequent cigarette smoking. We conclude that the unintended effects of ENDS taxation may considerably undercut or even outweigh any public health gains.

Keywords: Electronic nicotine delivery systems (ENDS), e-cigarettes, vaping, cigarettes, smoking, taxes, youth

JEL codes: H2, I1, I18

1. Introduction

In 2009, public health officials in the United States established Healthy People 2020 goals, one of which was to reduce the youth smoking rate from 19.5% to 16.0% by 2019 (HealthyPeople.gov 2020). In the introduction to a 2012 Surgeon General report on smoking, Department of Health and Human Services Secretary Kathleen Sebelius warned that “…youth and adult smoking rates that had been dropping for many years have stalled” (US Department of Health Human Services 2012). This situation quickly changed, however, as youth smoking rates fell to 6.0% by 2019, thus surpassing the Healthy People 2020 objective by 386%. What caused such an unanticipated decline in youth cigarette smoking?1 One candidate is the introduction of electronic cigarettes and other electronic nicotine delivery systems (“ENDS”). ENDS were first imported into the US in August 2006 (CASAA 2020) and overtook cigarettes as the most commonly used tobacco product among youth in 2014 (Pesko and Warman 2021). In 2019, 32.9% of youth used an ENDS over the past 30 days, while 10.7% used ENDS frequently; that is, on 20 or more of the past 30 days (Centers for Disease Control and Prevention 2020).

On the whole, the current scientific consensus is that ENDS are likely substantially less dangerous than combustible tobacco products (e.g., cigarettes), which are estimated to kill 480,000 Americans annually (US Surgeon General 2014). However, the exact relative risks remain uncertain. Based on data from an August 2020 survey of 137 tobacco scholars, the mean (median) tobacco expert believed that the effect of vaping ENDS on quality-adjusted life expectancy was 37% (25%) as large as the effect of smoking (Allcott and Rafkin 2021). Accounting for harms to others as well as the user, a 2013 expert panel concluded that ENDS were unlikely to exceed 5% of the harm of cigarettes (Nutt et al. 2014), a statistic cited in subsequent reviews of evidence on ENDS’ effects sponsored by Public Health England (McNeill et al. 2018). While the US debate does not use a specific estimate for these products’ relative risks, the National Academies of Sciences, Engineering, and Medicine’s 2018 report concluded that “…e-cigarettes appear to pose less risk to an individual than combustible tobacco cigarettes” and “…e-cigarette aerosol contains fewer numbers and lower levels of toxicants than smoke from combustible tobacco cigarettes.” Health costs may be higher, however, for informally sourced ENDS products than mainstream commercial ENDS because of unknown additives.

ENDS may affect youth health differently than adult health. One commonly cited reason is the potential deleterious effects of nicotine on youth brain development. However, as this evidence is based mostly on studies of rodents (US Surgeon General 2016), the relationship’s generalizability to humans is unclear (Balfour et al. 2021). Similarly, the magnitude of the danger posed by nicotine compared to other substances like alcohol, tetrahydrocannabinol (THC), caffeine, and sugar on adolescent brain development is also unclear.

Another commonly-voiced concern is the 2016 Surgeon General report’s conclusion that “…e-cigarette use is strongly associated with combustible tobacco product use” (US Surgeon General 2016). However, the idea that this association reflects a causal effect of ENDS use on subsequent smoking is inconsistent with the typical directionality of uptake over time—daily smoking is more common among young adults who tried cigarettes before ENDS (Friedman, Buckell, and Sindelar 2019; Etter 2018). This stated association also fails to accurately forecast rapidly declining youth cigarette use. Despite causal evidence that reducing ENDS access increases youth smoking (Pesko 2022b), the Surgeon General has declared high rates of youth ENDS use to be an epidemic (US Surgeon General 2018).

Policies designed to reduce access to ENDS therefore appear to prioritize the goal of reducing nicotine use—nicotine which has limited adverse effects on health outside of causing addiction—over the goal of harm reduction, which recognizes substitution from higher to lower-risk nicotine products by people who would not otherwise be able to quit as a benefit for public health. Such regulations have been increasing over time, beginning with ENDS minimum legal sales ages of 18 or higher implemented in all states between 2010 and 2016. As of March 2022, 30 states had adopted ENDS taxes (Public Health Law Center 2022) while 23 had added ENDS to their existing indoor smoking laws (American Non-Smokers Rights Foundation 2021).

Despite significant interest in the effect of regulation on youth ENDS use, studies have not yet estimated the effect of ENDS taxes on youth ENDS and combustible tobacco product use. We explore this question using two nationally representative datasets: Monitoring the Future (MTF) and the Youth Risk Behavior Surveillance System (YRBSS). Specifically, we use a continuous treatment difference-in-differences research design to estimate the relationship between ENDS taxes and a variety of outcomes, including ENDS use, combustible tobacco product use, sources of ENDS products (e.g., online purchasing, brick-and-mortar retailers, social sources), and perceived risk of ENDS use. In both MTF and YRBSS, we find that ENDS taxes reduce youth ENDS use and raise youth cigarette use, with evidence of particularly large effects on using these products regularly. We also find evidence that ENDS taxes raise perceptions of ENDS risk and shift the manner that youth obtain ENDS from retail sources to social sources.

By documenting both intended and unintended effects of ENDS taxation on youths, this study’s findings contribute to determining optimal ENDS tax policy. In particular, our results speak directly to the question of whether ENDS accessibility reduces youth combustible tobacco use. If this indirect effect on youth tobacco use is positive and large, and the direct harms of ENDS use are small, then imposing large taxes on ENDS products could conceivably worsen public health on net.

2. Background and related literature

2.1. ENDS taxation literature

There is a nascent but growing economic literature studying the effect of ENDS taxes on vaping and smoking outcomes. Broadly, the available literature suggests that ENDS and cigarettes are economic substitutes,2 although the magnitude of this relationship may vary across populations. This finding of substitution is consistent with literature finding minimum legal sales ages for ENDS reduce youth ENDS use (Nguyen 2020; Dave, Feng, and Pesko 2019; Abouk and Adams 2017; Pesko 2022a) and increase youth smoking (Friedman 2015; Pesko et al. 2016; Pesko and Currie 2019; Dave, Feng, and Pesko 2019; Pesko 2022a). A substitution relationship between cigarettes and ENDS is concerning for policymakers as, if true, restricting access to one good may increase demand for the other. Below, we review existing studies on ENDS taxes and tobacco use, and highlight our contributions to this literature. This section also provides evidence that ENDS accessibility, proxied by the price of the product, has a public health benefit in reducing combustible tobacco use.

Overall population:

Using Nielsen Retail Scanner Data (NRSD) from 2011 to 2019, Cotti et al. (2022) show that a $1.00 increase in the ENDS tax reduces ENDS sales by 52% and increases cigarette sales by 10%, which translates to an ENDS own-tax elasticity of −0.63 and cross-tax elasticity of 0.12. Cigarette taxes meanwhile have an own- [cross-] tax elasticity of −0.24 [0.83]. Allcott and Rafkin (2021) also use Nielsen data within the context of a broader shift-share paper, finding some evidence of substitution depending on whether area-specific time trends are included in the regression model or not.

Adults:

Pesko, Courtemanche, and Maclean (2020) use 2011–2018 data from the Behavioral Risk Factor Surveillance Survey and the National Health Interview Survey to study the effects of ENDS and cigarette taxes on adult vaping and smoking. The authors find that a $1.00 increase in the ENDS tax rate increases adult daily smoking propensity by 5.3% and the probability of “dual use” (i.e., consuming both ENDS and cigarettes) by 24.4%. These findings suggest a daily ENDS own-tax elasticity of −0.109 and cross-tax elasticity of 0.041. Further, cigarette taxes have an own- [cross-] tax elasticity on daily use of −0.085 [0.218] (Pesko, Courtemanche, and Maclean 2020).

Considering the experience of Minnesota, which adopted the first in the nation ENDS tax in August 2010, Saffer et al. (2020) test the effect of ENDS taxation on adult smoking. Using synthetic control methods, the authors find that adult smoking increases following an ENDS tax hike. The results imply a cross-elasticity of current smoking participation with respect to ENDS taxes of 0.13.

Friedman and Pesko (2022) study the effect of ENDS taxes on young adults ages 18–25 using data from the Current Population Survey’s Tobacco Use Supplement. They find that young adults use ENDS and cigarettes nearly interchangeably, with an ENDS own- [cross-] current (past 30-day) use tax elasticity of −0.539 [0.229] and a cigarette own- [cross-] current use tax elasticity of −0.429 [1.205].3

Pregnant women:

Abouk et al. (2022) study the effects of state and local ENDS taxes on pregnant women’s smoking behaviors. The authors use national birth record data of mother’s conceiving between 2013 to 2019 and investigate the effect of ENDS taxes on pre-pregnancy smoking and prenatal smoking. They find that raising ENDS taxes by $1.00 increases pre-pregnancy smoking by 0.5 and prenatal smoking by 0.4 percentage points (pp), which translates to a cross-tax elasticity of approximately 0.06. Using data from the Pregnancy Risk Assessment Monitoring System, the authors also find that ENDS taxes reduce pre-pregnancy ENDS use by 1.8 pp (elasticity = −0.28). The authors also find evidence that ENDS taxes increase news coverage of ENDS and raise perceptions of risk of ENDS.

Youth:

Pesko and Warman (2021) examine the effect of Minnesota’s 2013 ENDS tax increase—that is, above the tax level when first adopted in 2010—on youth smoking. The authors find that a 100% ad valorem tax increases cigarettes smoked among youth (unconditional on smoking status) by five additional cigarettes per month, or a little over three packs monthly for smokers using the mean youth smoking rate of 7.9%. Anderson, Matsuzawa, and Sabia (2020) primarily study the effect of cigarette taxes on youth marijuana use, but include an extension to the main analysis estimating the effect of ENDS tax adoption in three states (California, Pennsylvania, and West Virginia) using two waves of YRBSS data (2015 and 2017), one of the datasets we employ. Their empirical models include an indicator variable for ENDS taxes, implicitly treating all taxes equivalently regardless of their size and ignoring later changes in state ENDS tax rates. They find that ENDS tax adoption reduces current ENDS use by 3.4 pp and daily ENDS use by 0.8 pp, with imprecisely estimated effects on cigarette use.

To further our understanding of how ENDS taxes impact youth vaping and smoking, we build on these two studies in several ways. First, we leverage variation in ENDS taxes generated by ten states and two counties rather than a single state (Pesko and Warman 2021) or three states (Anderson, Matsuzawa, and Sabia 2020). Second, we quantify and exploit heterogeneity in ENDS tax magnitudes. These tax sizes vary substantially, from $0.05 per fluid milliliter (ml) in Delaware, Kansas, Louisiana, and North Carolina to over a $1.00 per fluid ml in California, Cook County Illinois, Minnesota, Pennsylvania, and Washington DC. Considering these differences allows us to report our findings in standard tax-elasticity terms and informs policy discussions by quantifying effects on youth tobacco product use for a specific tax policy. Third, we explore ENDS tax effects on how youth obtain ENDS. Given evidence that the 2019 outbreak of vaping-associated lung injuries was driven by additives in informally-sourced vaping products, shifts in youth product sourcing—e.g., from licensed retailers to informal contacts who may mix their own vaping concentrates outside of a retail setting like a vape shop—could have substantive health implications. Fourth, we consider a range of tobacco products that are common among youth but are taxed less aggressively (e.g., cigars), allowing us to characterize multiple margins along which youth may respond to ENDS taxes.

3. Data and methods

3.1. Data

Our analyses match policy data to two survey datasets, each of which has complementary strengths: the annual MTF dataset and the biennial YRBSS. Restricted-use, annual MTF data cover a nationally representative sample of 8th-, 10th-, and 12th-grade students in middle and high schools in the contiguous US, interviewing about 45,000 youth from nearly 400 public and private schools in the spring of each year. Our main analytic sample is comprised of MTF data for 2014—the first wave to include questions about ENDS use—through 2019, to avoid disruption from the COVID-19 outbreak starting in 2020. For cigarette use outcomes, sensitivity analyses extend the sample back to 2011. Restricted-use MTF data allow us to identify the county where each respondent’s school is located, in order to match respondents to their tobacco policy exposure at the county level.

The MTF survey includes several questions about cigarette and ENDS use and perceived risk of regular ENDS use. We use different questions to create the following variables, as described in detail in the Online Data Appendix: current ENDS use,4 frequent ENDS use (20 or more days over the past 30 days), ENDS initiation during the school year, ever ENDS use, current cigarette use, current cigarette or cigar use, current half pack daily cigarette use, and perceived likelihood of regular ENDS use being highly risky. In general, MTF information is collected across six different surveys (forms) each year, with ENDS questions included on a subset of these forms. Consequently, ENDS sample sizes are somewhat smaller than cigarette sample sizes. Ever ENDS use and ENDS initiation in particular were not collected in 2014 and only on select forms thereafter. For some years, some small states do not have any schools participating in the MTF survey. We restrict our main MTF analyses to a sample of states surveyed in each year to reduce sampling variability, which causes six small states to fall out of regression analysis, including two with ENDS taxes.5 Reassuringly, we show in a sensitivity analysis that our results also hold when inconsistently collected states are retained.

The National and State YRBSS survey high school students in public and private schools across the US about their health behaviors biennially. The Centers for Disease Control and Prevention (CDC) administer the National YRBSS, while State YRBSS data are collected by state education and health departments under CDC supervision, using a similar survey instrument. As YRBSS first asked about ENDS use in 2015, our analytic sample is limited to 2015–2019. Pooling the National and State datasets provides greater statistical power due to an increased sample size (N>580,000), and ensures that all states that adopted an ENDS tax by the end of June 2019 are represented.

YRBSS asks about ever use and frequency of past 30-day use for cigarettes, “electronic vapor product[s]” followed by example brand names marketed as nicotine ENDS (e.g., JUUL, Vuse, blu),6 and “cigars, cigarillos, or little cigars,” as well as how respondents usually obtain ENDS products. Additionally, the final two surveys also collected information on source of ENDS (i.e., retail, internet, social, other). While National and State YRBSS identify the state where a respondents’ school is located, they do not provide county or other substate identifiers.7

We weight both the MTF and the state and national YRBSS to return nationally representative results. To construct weights, we use the National Cancer Institute’s Surveillance, Epidemiology and End Results Program (SEER) data to calculate the state-by-year share of the youth population that falls in each age-by-gender-by-race/ethnicity bin i, sist (age 14, age 15, age 16, age 17, age 18, male, female, non-Hispanic White, non-Hispanic Black, Hispanic, and other race/ethnicity). We then calculate each respondent’s sample weight as [sist/nist]*StatePop14_18st, where nist is the number of YRBSS sampled individuals in age-by-gender-by-race-ethnicity bin i in state s at year t and StatePop14_18st is the SEER estimated population of 14-to-18-year-olds in state s at year t. In this construction, we are following the recent literature that applies similar SEER-constructed weights in analyses of the combined YRBSS data (Rees, Sabia, and Kumpas (2020); Bryan et al. (2020); and Sabia and Anderson (2016)). We use the SEER-constructed weights to accommodate the multi-year and multi-grade MTF analysis, and to maintain consistency with the YRBSS analysis. Sensitivity analyses show that our results are similar when using unweighted data.

We match tobacco control and other related policy data from public and proprietary sources to respondents by county for MTF and by state for YRBSS, since the latter lacks sub-state identifiers. We match these policy data by quarter for MTF and by year for YRBSS, since YRBSS does not include month or quarter of interview information. In particular, we average values across the 1st and 2nd quarters of each YRBSS survey year to match when the survey is typically fielded. Policy variables include cigarette excise taxes (the summation of federal, state, and local), percent population covered by indoor smoking restrictions and indoor vaping restrictions (two separate variables) in bars, restaurants, and private workplaces (each venue weighted equally), state laws establishing minimum legal sale ages for ENDS (0/1), percent population covered by Tobacco 21, laws prohibiting smoking and vaping in K-12 public schools (two separate variables, 0/1), ENDS product packaging laws (0/1), ENDS retail licensure requirements (0/1), beer taxes, vertical ID laws (0/1), medical marijuana legalization (0/1), recreational marijuana legalization (0/1), unemployment rates, and poverty rates. See the Online Data Appendix for further information and sources. All local laws are population-weighted to the county level for MTF and to the state level for YRBSS. All monetary variables are adjusted to 2019 dollars using the Bureau of Labor Statistics’ Consumer Price Index.

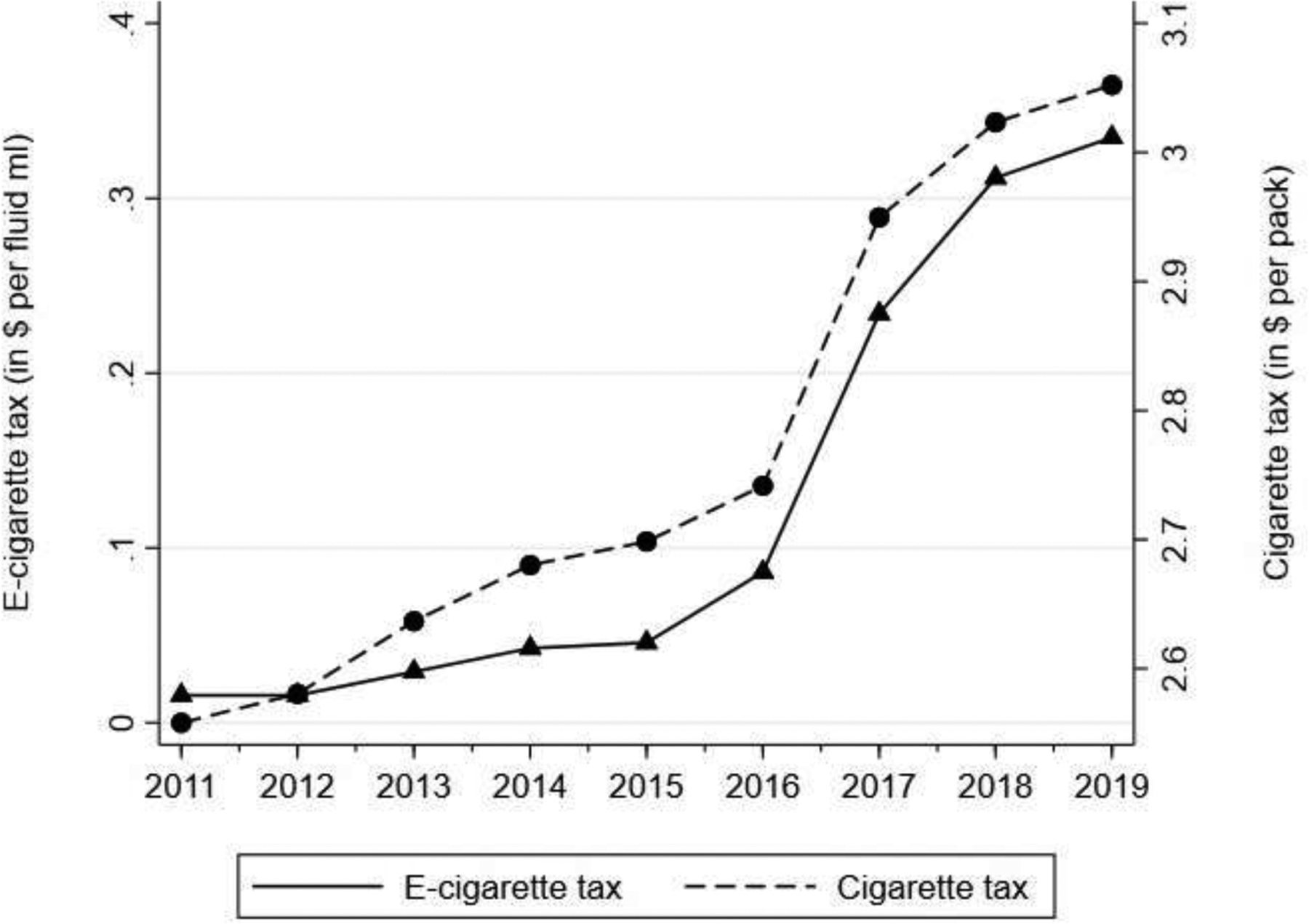

Our main policy variable of interest is the state or local ENDS tax rate. ENDS taxes are levied in different ways, including as an excise tax per unit or fluid ml of liquid, or as an ad valorem tax on wholesale prices. Cotti et al. 2021 developed a method to standardize these taxes into a single ENDS tax per fluid ml measure as shown in Table 1. In brief, the authors used 2013 to identify an average national8 wholesale price of $2.63 per fluid ml and 1.02 containers per fluid ml, and then multiplied future tax changes by these base values to generate taxes standardized per fluid ml. One benefit of this measure is that only legislated tax changes affect standardized tax values, thus avoiding endogeneity of prices and related issues (Gruber and Köszegi 2001). For reference, one JUUL pod has 0.7 fluid ml, equivalent to approximately one pack of cigarettes (Truth Initiative 2019).9

Table 1.

ENDS Tax Changes Through 2nd Quarter of 2019

| Locality | Effective Date | Unit Taxed | Tax Amount | Tax per ml, Q1-2 2015 ($) | Tax per ml, Q1-2 2017 ($) | Tax per ml, Q1-2 2019 ($) |

|---|---|---|---|---|---|---|

| District/State | ||||||

| California | 4/2017, 7/2017, 7/2018 | Wholesale price | 27.3%, 65.1%, 62.8% | $0 | $0.72 | $1.65 |

| Delaware | 1/2018 | Per fluid milliliter | $0.05 | $0 | $0 | $0.05 |

| Kansas | 1/2017, 7/2017 | Per fluid milliliter | $0.20, $0.05 | $0 | $0.20 | $0.05 |

| Louisiana | 7/2015 | Per fluid milliliter | $0.05 | $0 | $0.05 | $0.05 |

| Minnesota | 8/2010, 7/2013 | Wholesale price | 35.0%, 95.0% | $2.49 | $2.49 | $2.49 |

| North Carolina | 6/2015 | Per fluid milliliter | $0.05 | $0.02 | $0.05 | $0.05 |

| New Jersey | 10/2018 | Per fluid milliliter | $0.10 | $0 | $0 | $0.10 |

| Pennsylvania | 7/2016 | Wholesale price | 40.0% | $0 | $1.05 | $1.05 |

| Washington, DC | 10/2015, 10/2016, 10/2017, 10/2018 | Wholesale price | 67.0%, 65.0%, 60%, 96% | $0 | $1.70 | $2.52 |

| West Virginia | 7/2016 | Per fluid milliliter | $0.08 | $0 | $0.08 | $0.08 |

| County/City | ||||||

| Chicago, Illinois | 1/2016, 1/2019 | Per container / per fluid milliliter1 | $0.80 / $0.55, $1.50 / $1.20 | |||

| Cook County, IL | 5/2016 | Per fluid milliliter | $0.20 | $0 | $0.94 | $1.50 |

| Montgomery County, MD | 8/2015 | Wholesale price | 30.00% | $0 | $0.79 | $0.79 |

Notes: Please see the online data appendix for further details.

The Chicago tax is added to the Cook County tax based on the share of the population residing in Chicago.

Table 2 reports MTF and YRBSS descriptive statistics with weights for the variables discussed above, separately for the overall sample and two sub-samples: areas that implemented ENDS taxes by the end of 2019 and areas that did not. Current ENDS use rates are 15.2% in MTF and 21.1% in YRBSS, with mean rates approximately 1.5 pp higher in non-treated than treated states. Current cigarette use rates are approximately 6.6% in the MTF and 8.1% in the YRBSS, and are also moderately higher in non-treated states. YRBSS results may report higher ENDS use in part because YRBSS only includes high school students, whereas MTF also includes 8th graders, who are less likely to use these products.

Table 2:

Descriptive Statistics, 2014–2019 (MTF); 2015–2019 (YRBSS)

| Overall |

MTF Treated |

Non-Treated | Overall |

YRBSS Treated |

Non-Treated | |

|---|---|---|---|---|---|---|

| Outcomes | ||||||

| Current ENDS Use | 0.152 | 0.142 | 0.156 | 0.211 | 0.198 | 0.215 |

| [N=126,306] | [N=40,298] | [N=86,008] | [N=538,992] | [N=126,637] | [N=412,355] | |

| Frequent ENDS Use | 0.038 | 0.035 | 0.039 | 0.047 | 0.049 | 0.047 |

| [N=126,306] | [N=40,298] | [N=86,008] | [N=538,992] | [N=126,637] | [N=412,355] | |

| Current Cigarette Smoker | 0.066 | 0.060 | 0.069 | 0.081 | 0.073 | 0.084 |

| [N=244,360] | [N=78,538] | [N=165,822] | [N=580,788] | [N=135,993] | [N=444,795] | |

| Current Cigarette or Cigar Smoker | 0.080 | 0.073 | 0.083 | 0.113 | 0.093 | 0.117 |

| [N=246,192] | [N=79,112] | [N=167,080] | [N=580,788] | [N=135,993] | [N=444,795] | |

| ENDS Perceived Risk “Greatly Risky” | 0.192 | 0.199 | 0.189 | - | - | - |

| [N=86,486] | [N=27,804] | [N=58,682] | - | - | - | |

| Current Cigarette Smoker (smoked at least 1/2 pack a day in the past month) | 0.012 | 0.010 | 0.012 | - | - | - |

| [N=244,360] | [N=78,538] | [N=165,822] | ||||

| Current Cigarette Smoker (smoked at least a full pack a day in the past month) | 0.006 | 0.005 | 0.006 | - | - | - |

| [N=244,360] | [N=78,538] | [N=165,822] | ||||

| Frequent Cigarette Smoker | - | - | - | 0.022 | 0.015 | 0.023 |

| - | - | - | [N=580,788] | [N=135,993] | [N=444,795] | |

| ENDS Sources * | ||||||

| Retail Source | - | - | - | 0.212 | 0.185 | 0.227 |

| - | - | - | [N=55,902] | [N=22,260] | [N=33,642] | |

| Internet | - | - | - | 0.038 | 0.042 | 0.035 |

| - | - | - | [N=55,902] | [N=22,260] | [N=33,642] | |

| Social Source | - | - | - | 0.617 | 0.628 | 0.611 |

| - | - | - | [N=55,902] | [N=22,260] | [N=33,642] | |

| Other Source | - | - | - | 0.133 | 0.145 | 0.126 |

| - | - | - | [N=55,902] | [N=22,260] | [N=33,642] | |

| Individual Characteristics | ||||||

| Female | 0.516 | 0.514 | 0.517 | 0.489 | 0.489 | 0.490 |

| Age | 16.005 | 15.997 | 16.009 | 16.003 | 16.014 | 16.000 |

| (1.985) | (1.994) | (1.981) | (1.426) | (1.424) | (1.426) | |

| White, non-Hispanic | 0.550 | 0.472 | 0.585 | 0.543 | 0.487 | 0.560 |

| Black/African American, non-Hispanic | 0.148 | 0.129 | 0.156 | 0.148 | 0.146 | 0.149 |

| Hispanic/Latino | 0.237 | 0.307 | 0.206 | 0.240 | 0.281 | 0.228 |

| Other Races, non-Hispanic | 0.066 | 0.092 | 0.054 | 0.068 | 0.085 | 0.063 |

| Grade | 10.050 | 10.083 | 10.035 | 10.445 | 10.481 | 10.434 |

| (1.665) | (1.647) | (1.673) | (1.190) | (1.195) | (1.188) | |

| Policy and Economic Covariates | ||||||

| ENDS Tax Rate per ml (2019 $) | 0.174 | 0.562 | - | 0.166 | 0.703 | - |

| (0.516) | (0.801) | - | (0.456) | (0.709) | - | |

| Cigarette Tax Rate per Pack (2019 $) | 2.967 | 3.137 | 2.890 | 2.954 | 3.260 | 2.859 |

| (1.379) | (1.421) | (1.353) | (1.285) | (0.972) | (1.353) | |

| Beer Tax Rate (2019 $) | 0.302 | 0.241 | 0.330 | 0.314 | 0.255 | 0.332 |

| (0.277) | (0.161) | (0.312) | (0.286) | (0.175) | (0.310) | |

| Tobacco 21 Percent Population Coverage | 0.146 | 0.300 | 0.077 | 0.174 | 0.462 | 0.085 |

| ENDS Minimum Legal Sale Age (0/1) | 0.873 | 0.936 | 0.844 | 0.924 | 1.000 | 0.900 |

| Indoor Smoking Restrictions Percent Population Coverage | 0.802 | 0.896 | 0.760 | 0.792 | 0.928 | 0.750 |

| Indoor ENDS Restrictions Percent Population Coverage | 0.229 | 0.425 | 0.141 | 0.264 | 0.532 | 0.181 |

| Recreational Marijuana Laws (0/1) | 0.128 | 0.218 | 0.087 | 0.163 | 0.378 | 0.096 |

| Medical Marijuana Laws (0/1) | 0.526 | 0.761 | 0.420 | 0.579 | 0.807 | 0.508 |

| Vertical License Law (0/1) | 0.968 | 0.963 | 0.970 | 0.975 | 0.959 | 0.980 |

| Unemployment Rate | 4.862 | 5.195 | 4.713 | 4.544 | 4.480 | 4.563 |

| (1.576) | (1.732) | (1.476) | (0.880) | (0.499) | (0.967) | |

| Poverty Rates | 14.200 | 14.076 | 14.256 | 12.697 | 12.015 | 12.908 |

| (5.219) | (4.764) | (5.411) | (2.513) | (2.693) | (2.416) | |

| N | 254,516 | 81,823 | 172,693 | 600,877 | 139,509 | 461,368 |

Notes: Means and standard deviations (in parenthesis) are reported. Since state/county-level information is available in the MTF data, policy/economic controls are at the county level except for beer taxes, marijuana laws, and vertical ID laws in which we only have state-level data. Since county information is not available in the national / state YRBSS, available county-level information is population-weighted to the state level.

ENDS sources are only for the years 2017–2019 and are conditional on an individual being a current ENDS user.

Non-adopting states appear to have higher shares of White, non-Hispanic youth, and less restrictive tobacco control regulation generally, though higher beer taxes and less marijuana access. Unweighted descriptive results are provided in Appendix Table 1.

3.2. Methods

To investigate the effect of ENDS taxes on youth vaping and smoking outcomes, we estimate the following regression for county-level MTF data:

| (1) |

The parameter β1 is the coefficient of interest, which captures the effect of ENDS taxes on our outcomes. Xit is a covariate matrix comprised of individual-level sociodemographic variables (gender, age, grade, and race/ethnicity [White, Black, Hispanic, and other], along with missing-value indicators for each sociodemographic variable). Zct adjusts for the policies described above.

Distinct analyses will consider each of the following outcomes as Yilt: any ENDS use in the past 30 days, frequent ENDS use (20 or more days over the past 30 days), initiating ENDS use during the current school year, current cigarette use, various measures of heavy cigarette use, current cigarette or cigar use, perceived likelihood of regular ENDS use being highly risky, and source of ENDS (i.e., retail, internet, social, other).

The above specification is based on a continuous treatment difference-in-differences research design, capitalizing on the variation in treatment intensity generated from jurisdictions newly adopting ENDS taxes of varying amounts as well as subsequent changes to their tax rates. The specification includes “two-way fixed effects” (TWFE) to account for spatial and temporal heterogeneity. Fixed-effects for year-quarter of interview (δt) adjust for national time trends, while area (or jurisdiction) fixed-effects (γl) adjust for time-invariant differences in the outcome variable by tax jurisdiction l, defined here as states with two exceptions: Cook County, Illinois and Montgomery County, Maryland, both of which are separated from their respective states due to local ENDS taxes, as in other work (Cotti et al. 2022; Allcott and Rafkin 2021).

As YRBSS data lack interview quarter and county identifiers, those analyses utilize state and year rather than tax jurisdiction and quarter. Otherwise, the MTF and YRBSS specifications are identical. Standard errors are clustered by state for both data sources.

Our treatment variable follows a staggered adoption, that is jurisdictions adopt ENDS taxes at different points in time. Recent econometric literature shows that this treatment regime can lead to bias in regression coefficients in TWFE estimators when treatment effects are heterogenous across treated units or time (Goodman-Bacon 2021). The most concerning source of this bias is “forbidden comparisons” attributable to dynamic treatment effects (Borusyak, Jaravel, and Spiess 2022). In the binary treatment variable case, TWFE coefficient estimates can be decomposed to all possible two*two difference-in-differences comparisons. Some of these comparisons will be “reasonable” in that newly treated units are compared to untreated units. However, some comparisons will be “forbidden:” those that compare newly treated units to previously treated units. If treatment effect dynamics are present (e.g., treatment effects grow over time after the tax is adopted), then the latter type of comparison can lead to negative weighting and possibly sign-reversals. Another limitation of using TWFE regressions to estimate causal effects with a staggered treatment regime is the estimator’s weights. TWFE regression models place the most weight on observations for which treatment “turns on” in the middle of the panel. This is an artifact of the OLS minimization procedure which upweights observations with the most variance in the treatment variable. If there is heterogeneity across units in treatment effects, weighting in this manner can lead to a regression coefficient that departs from the average treatment effect on the treated which is a common parameter of interest in applied microeconomics.

The recent economic literature has developed both tools to diagnose these issues (Goodman-Bacon 2021) and methods that are robust to bias attributable to heterogeneity and dynamics in treatment effects (de Chaisemartin and D’Haultfoeuille 2022; Callaway and Sant’Anna 2021; Borusyak, Jaravel, and Spiess 2022).10 A common theme of recent estimators developed to address bias from dynamics in treatment effects is selecting “clean” comparison groups. That is, only untreated units are included in the comparison group, thereby circumventing issues related to “forbidden” comparisons. To address the issue related to weighting, estimators in this new literature allow the researcher to select their own weights (Callaway and Sant’Anna, 2020).

However, our treatment variable is continuous which adds complexity; thus, one could view our estimator as a generalized difference-in-differences estimator. At the time of writing, the econometric literature is only beginning to offer tools to address this setting (Callaway, Goodman-Bacon, and Sant’Anna 2021). With a continuous (or multi-valued) treatment variable, there are more objects of potential interest to the researcher. As noted by Callaway, Goodman-Bacon, and Sant’Anna (2021), there are at least four parameters salient to applied microeconomics questions: 1) average treatment effect on the treated (ATT), 2) average treatment effect (ATE), 3) average causal response on the treated (ACRT), and 4) average causal response (ACR).11 Callaway, Goodman-Bacon, and Sant’Anna (2021) introduce the concept of “dose” in estimation of continuous treatment variable effects, the dose of the treatment is simply the intensity of treatment, in our context is the size (in dollars) of the ENDS tax. The ATT and ATE are “level” effects in that they provide an estimate of the effect of a specific dose level (e.g., $1.00) relative to zero dose ($0.00). These target parameters are reasonable in the binary treatment setting as there is just one treatment dose: treated vs. untreated. On the other hand, ACRT and ACR are “slope” effects in that they reveal the effect of an incremental change in treatment dose on the outcome (e.g., $1.00 increase in the ENDS tax from $0.50 to $1.50).12 Our parameter of interest in our study is the ACRT.

Recovery of a causal estimate of the ACRT requires the researcher to make certain assumptions which we now list and then discuss in our context; see Callaway, Goodman-Bacon, and Sant’Anna (2021) for a full discussion of these assumptions. The first is random sampling. We expect that our data satisfy this assumption given that we rely on two nationally representative surveys. The second is support, meaning there must be jurisdictions at the actual dosage levels we are examining. Practically, this assumption implies that we are estimating across particular discrete ATT points; that is, the points that correspond to tax values that are levied in jurisdictions in our sample and not other values. Third, there are no anticipation effects, meaning treatment (i.e., ENDS tax adoption) cannot have effects prior to adoption (i.e., the tax being levied).13 Thus, we assume that youth in our sample do not change their tobacco product purchasing and associated behaviors prior to the tax change. If youth are myopic and/or do not pay attention to government tax policy discussions in their locality (versus adopted taxes), then this assumption seems reasonable. The fourth assumption is parallel trends. However, we must assume a different version of parallel trends than is required with a binary treatment variable. Callaway, Goodman-Bacon, and Sant’Anna (2021) refer to this assumption as “strong parallel trends:” all groups that receive treatment at the same time (regardless of dose) would have followed the same path of potential outcomes at every possible dose level. Thus, strong parallel trends place restrictions on treated potential outcomes, not just untreated potential outcomes as in case of a binary treatment regime.14

With these four assumptions, we are able to recover an estimate of the ACR, but not the ACRT; instead, we recover an estimate of the ACRT plus a selection bias term, where the selection relates to jurisdictions (or rather decision makers in jurisdictions) selecting their level or dose of the treatment (ENDS taxation level in our context).15 To recover a causal estimate of the ACRT, we assume that selection bias is zero. This assumption is potentially reasonable if individual youth tobacco product consumption decisions (our outcomes) are not the driving factors that drives policy makers to adopt specific values of ENDS taxes. We attempt to provide suggestive evidence on the extent to which this assumption is reasonable. To this end, we extend the concept of “balance testing.” Using the Monitoring the Future data (MTF), one of two data sets we use in our main analyses, we divide the sample into groups of ENDS tax jurisdictions that had taxes as of the 2nd quarter of 2019 (when our study ends) of $0.00, $0.01 to $1.00, $1.01 to $2.00, and $2.00 to $2.52 (the highest tax in place) and compare tobacco product use and demographics of youth at baseline (year 2014). While current ENDS use rates are quite stable across groups, we see evidence that higher ENDS tax adopting locations have higher Hispanic share. If Hispanic share is related to selection into treatment dose, then our results may be interpreted most conservatively as an estimate of the ACR parameter. However, if other factors (for example, youth use of tobacco products) are more salient for selection into dose (that is, the factors that policymakers consider when establishing ENDS tax rates), then we may be less concerned about selection into dose in our setting and thus our findings may be interpreted as an estimate of the ACRT parameter.

In our manuscript, we rely upon TWFE regression to estimate the ACRT. Thus, we impose the admittedly strong assumptions noted above.16

4. Results

4.1. Effects of ENDS taxes on ENDS outcomes

Table 3 panel A presents estimates of the standardized ENDS tax rate’s effects on youth ENDS use. The first four columns’ specifications leverage the MTF’s ENDS data availability to estimate responses along various consumption margins. Coefficient estimates generally suggest that higher ENDS taxes are effective in reducing use among youth, with marginally statistically significant reductions (10% level) in current and regular ENDS use, and a statistically significant decline in ever-use. Specifically, a $1.00 increase in the standardized tax, which represents about twice the observed standard deviation in the tax, reduces the likelihood of currently using ENDS by 1.9 pp (model 1). The estimated ENDS participation tax elasticity is −0.08, which translates into an ENDS participation price elasticity of −0.43 for the youth population.17,18

Table 3:

Main Results

| Panel A: Effects of ENDS Tax on ENDS Use | |||||

|---|---|---|---|---|---|

| Outcome | Current ENDS User | Regular ENDS User | ENDS Initiation | Ever Use ENDS | Current ENDS User |

| ENDS Tax Rate per ml (2019 $) | −0.019+ | −0.013+ | −0.008 | −0.052*** | −0.071** |

| (0.010) | (0.007) | (0.014) | (0.010) | (0.025) | |

| [−0.040,0.002] | [−0.028,0.001] | [−0.036,0.021] | [−0.072,−0.031] | [−0.120, −0.022] | |

| <0.071> | <0.073> | <0.581> | <0.000> | <0.006> | |

| Cigarette Tax Rate per Pack (2019 $) | −0.005 | 0.009+ | −0.003 | 0.012 | 0.041 |

| (0.008) | (0.005) | (0.013) | (0.008) | (0.026) | |

| [−0.021,0.012] | [−0.001,0.019] | [−0.029,0.022] | [−0.004,0.028] | [−0.012, 0.094] | |

| <0.552> | <0.065> | <0.789> | <0.135> | <0.129> | |

| Data | MTF | MTF | MTF | MTF | YRBSS |

| Years | 2014–2019 | 2014–2019 | 2015–2019 | 2015–2019 | 2015–2019 |

| N | 126,306 | 126,306 | 66,124 | 85,541 | 538,992 |

| Dependent Variable Mean | 0.152 | 0.038 | 0.104 | 0.287 | 0.213 |

| ENDS Elasticity | −0.075 | −0.212 | −0.059 | −0.146 | −0.164 |

| Cigarette Elasticity | −0.095 | 0.712 | −0.097 | 0.127 | 0.568 |

| Panel B: Effects of ENDS Tax on ENDS Perceived Risk and Sources | |||||

| Outcome | ENDS Perceived Risk | Retail Source | Social Source | Internet Source | Other Source |

| ENDS Tax Rate per ml (2019 $) | 0.029* | −0.076* | 0.101* | 0.019 | −0.044* |

| (0.014) | (0.034) | (0.046) | (0.015) | (0.021) | |

| [0.001,0.057] | [−0.143, −0.008] | [0.008, 0.194] | [−0.012, 0.049] | [−0.086, −0.002] | |

| <0.041> | <0.029> | <0.034> | <0.220> | <0.040> | |

| Cigarette Tax Rate per Pack (2019 $) | −0.003 | 0.086** | −0.105* | 0.006 | 0.014 |

| (0.007) | (0.031) | (0.049) | (0.019) | (0.021) | |

| [−0.017,0.011] | [0.023, 0.148] | [−0.204, −0.006] | [−0.032, 0.044] | [−0.029, 0.056] | |

| <0.671> | <0.009> | <0.038> | <0.747> | <0.522> | |

| Data | MTF | YRBSS | YRBSS | YRBSS | YRBSS |

| Years | 2014–2018 | 2017–2019 | 2017–2019 | 2017–2019 | 2017–2019 |

| N | 86,486 | 55,902 | 55,902 | 55,902 | 55,902 |

| Dependent Variable Mean | 0.192 | 0.185 | 0.627 | 0.042 | 0.145 |

| Panel C: Effects of ENDS Tax on Combustible Tobacco Product Use | |||||||

|---|---|---|---|---|---|---|---|

| Outcome | Current Cigarette Use | Current Cigarette Use (half pack a day) | Current Cigarette or Cigar Use | Current Cigarette Use | Regular Cigarette Use | Daily Cigarette Use | Current Cigarette or Cigar Use |

| ENDS Tax Rate per ml (2019 $) | 0.013* | 0.006** | 0.012+ | 0.008 | 0.016 | 0.014 | 0.007 |

| (0.006) | (0.002) | (0.006) | (0.013) | (0.014) | (0.012) | (0.016) | |

| [0.001,0.026] | [0.002,0.010] | [−0.001,0.024] | [−0.019, 0.035] | [−0.011, 0.043] | [−0.011, 0.039] | [−0.024, 0.038] | |

| <0.041> | <0.008> | <0.069> | <0.544> | <0 244> | <0.257> | <0.658> | |

| Cigarette Tax Rate per Pack (2019 $) | −0.001 | −0.002 | −0.002 | −0.010 | −0.012 | −0.008 | −0.011 |

| (0.005) | (0.002) | (0.007) | (0.013) | (0.014) | (0.012) | (0.017) | |

| [−0.011,0.010] | [−0.005,0.001] | [−0.015,0.012] | [−0.035, 0.016] | [−0.039, 0.016] | [−0.033, 0.016] | [−0.045, 0.023] | |

| <0.892> | <0.227> | <0.819> | <0.544> | <0.398> | <0.491> | <0.502> | |

| Data | MTF | MTF | MTF | YRBSS | YRBSS | YRBSS | YRBSS |

| Years | 2014–2019 | 2014–2019 | 2014–2019 | 2015–2019 | 2015–2019 | 2015–2019 | 2015–2019 |

| N | 244,360 | 244,360 | 246,192 | 580,788 | 580,788 | 580,788 | 504,639 |

| Dependent Variable Mean | 0.066 | 0.012 | 0.080 | 0.080 | 0.019 | 0.014 | 0.107 |

| ENDS Elasticity | 0.123 | 0.341 | 0.089 | 0.041 | 0.336 | 0.412 | 0.031 |

| Cigarette Elasticity | −0.032 | −0.530 | −0.056 | −0.355 | −1.792 | −1.784 | −0.321 |

p<0.10,

p<0.05,

p<0.01,

p<0.001

Notes: All MTF models include tax jurisdiction fixed-effects, year-by-quarter fixed-effects, and each of the individual controls and policy/economic covariates listed in Table 2. All YRBSS models include state fixed-effects, year fixed-effects, and each of the individual controls and policy/economic covariates listed in Table 2. Regressions are weighted, standard errors are corrected for clustering at the state level, 95% confidence intervals are shown in [ ] and p-values are shown in < >.

The ENDS participation margin here combines regular users and occasional users. About three quarters of adolescents who report currently using ENDS do so occasionally and are not regular users (see Table 2). When we expressly consider whether higher ENDS taxes impact those who use ENDS more frequently, we continue to find a marginally significant negative effect. Comparing the coefficient estimates between current use and regular use indicates that about two-thirds of the reduction in current use associated with higher ENDS taxes is driven by a reduction in regular use (1.3/1.9 pp), suggesting that this latter, more intense, margin of use is especially elastic. This pattern is borne out by the estimated tax elasticity of regular use, which is more than double the participation elasticity (−0.21 vs. −0.08).

Among adolescents in particular, current ENDS use includes established users, new initiates, and experimenters. Column (3)’s results suggest that higher ENDS taxes may deter initiation, with the tax elasticity (−0.06) similar to that for ENDS participation (−0.08), though imprecisely estimated. As our initiation measure is noisy, potentially explaining this imprecision, we turn to ever-use of ENDS – which is directly reported in the data – as a proxy for initiation and experimentation (Dave et al. 2019). By definition, year-to-year changes in ever-use — the variation leveraged in fixed-effects models — capture the prevalence of new initiates and experimenters. Thus, taxes’ effects on ever-use should reflect their impacts on new initiation and experimentation. We find a significant and relatively large effect of ENDS taxes on ever-use of ENDS, with a $1.00 increase in the standardized tax resulting in a 5.2 pp decrease in ever ENDS use.

Reassuringly, the last column in Table 3 Panel A confirms that higher taxes significantly and effectively reduce current ENDS use in a different adolescent sample (YRBSS). That coefficient estimate is larger than the MTF estimate, perhaps due in part to higher mean ENDS use in the YRBSS, which started collecting ENDS data one year later than MTF and considered older respondents (high school students only).

Estimates of the cross-effects of cigarette taxes on ENDS use are generally insignificant, in line with recent evidence that cigarette taxes may have lost their bite in terms of affecting youth (Hansen et al. 2017). Only for regular ENDS use is there a marginally significant effect of cigarette taxes, suggesting that higher cigarette taxes may drive some adolescents to substitute towards frequent ENDS use, consistent with the products being economic substitutes for youth.

Table 3 panel B reports estimates for other outcomes related to ENDS use, including perceived risk (from the MTF) and source of ENDS purchases (from the YRBSS). Column (1) suggests that higher ENDS taxes significantly increase the perceived risk of using that product among youth, which is similar to previously reported findings for reproductive age women (Abouk et al. 2022). While stricter tax policy might lead adolescents to adjust their risk beliefs directly, perhaps by reducing the general availability of ENDS and drying up the social market, an alternative explanation is that risk beliefs are concurrent to (or bundled with) individuals’ consumption decisions. For instance, Viscusi (2016) finds that cigarette users expect ENDS to be less risky than non-users. In this context, the reduction in ENDS use and initiation (Table 3 panel A) and the upward adjustment of the perceived risk of ENDS use would go hand-in-hand.

Given that retailers are restricted from selling ENDS to youth (by federal law since August 2016 and in most states even earlier than that), the finding that youth are responding to the monetary cost of a product that they are legally restricted from purchasing may appear counterintuitive.19 However, as shown in Table 2, a sizeable fraction (25%) of adolescents who use ENDS report purchasing the product themselves either through retail or internet sources. These individuals would be directly affected by any increase in the monetary cost. Others who obtain ENDS through social sources or third-party purchases may also be affected (e.g., if price increases are passed on via the third party or affect peers’ willingness to share).20

As expected, retail purchases by youth are the most responsive to higher ENDS taxes (see Table 3 Panel B). A $1.00 increase in ENDS taxes reduces the likelihood that youth obtain their ENDS through retail sources by about 7.6 pp (41.1% relative to the sample mean). Moreover, we also find a significant reduction in “other sources” (e.g., stealing from a store). These findings are consistent with Table 3‘s coefficient estimates, corroborating the hypothesis that higher taxes decrease youth ENDS consumption primarily through retail purchases. Moreover, the indication that higher taxes may shift how teens acquire ENDS is notable. Specifically, among those who continue to use ENDS, there is evidence of substitution away from retail and other sources into social sources (10.1 pp or 16.1% increase), a shift which may have direct adverse health effects if socially-sourced ENDS products are more likely to be contaminated with unknown additives. Critically, higher cigarette taxes, which lower the relative cost of ENDS, appear to have inverse effects, encouraging significant substitution towards retail ENDS purchases and away from the social market.

4.2. Effects of ENDS taxes on cigarettes and other tobacco product use

While higher ENDS taxes appear to significantly deter youth from using ENDS, the public health implications of this impact depend on potential substitution towards other higher-risk tobacco products. We assess this possibility with the results reported in Table 3 panel C, considering reported use of combustible tobacco products (cigarettes and cigars) from MTF (columns 1–3) and YRBSS (columns 4–7). Coefficient estimates based on the MTF sample suggest that higher ENDS taxes significantly increase cigarette use, on both the extensive and intensive margins. Consumption of at least a half pack per day is particularly responsive to shifts in ENDS tax policy, with a $1.00 increase in the standardized ENDS tax increasing it by 1.3 pp. YRBSS sample estimates suggest a similar pattern of substitution into cigarette use from higher ENDS taxes, with coefficient estimates largely similar to the MTF estimates though imprecise due to inflated standard errors. Across outcomes, own-effects of cigarette taxes are negative but not statistically distinguishable from zero.21

If ENDS taxes impact the demand for other tobacco products only through their direct effects on the demand for ENDS, the own-tax effects on ENDS use in Table 3 can be construed as a “first-stage” effect, bounding the size of the impacted adolescent population that may substitute towards other tobacco products. Specifically, MTF estimates suggest that a $1.00 increase in the ENDS tax reduces ENDS participation by about 2.0 pp. We would therefore not expect the spillover effects of ENDS taxes on cigarettes to be larger than this magnitude. About 2% of adolescents (based on the MTF) are changing their ENDS use behaviors due to higher ENDS taxation, and a subset of these (1.3 pp or about 68% of the impacted population) are switching to cigarettes. This “treatment-on-the-treated” effect is smaller if we use the YRBSS estimates, which suggest that 23% of teens who respond to higher ENDS taxes with reduced ENDS use are substituting towards regular cigarette use. Such scaled estimates should be interpreted with caution, and are meant to be suggestive, since they can vary dramatically with small changes in the underlying parameters. Nevertheless, they provide a means to gauge the credibility of estimated ENDS tax effect-sizes, and broadly suggest that a non-negligible fraction of teens reducing their use of ENDS because of a tax could be substituting into combustible tobacco use instead.

4.3. Effects of ENDS taxes on dual-use and any use outcomes

Across our sample period, approximately 30% of current (past-month) ENDS users also currently use cigarettes. From a health perspective, “dual-use” could represent a good or bad outcome. Dual-use of ENDS and a combustible tobacco product could be health-improving if it represents attempts to quit and/or reduce cigarette smoking, or health-deteriorating if it facilitates continued smoking among individuals who would otherwise quit (e.g., if they could not continue using nicotine in smoke-free locations). In Table 4, we do not find statistically significant evidence that ENDS taxes affect youth dual-use or for that matter, an indicator for any use (i.e., of ENDS or combustible tobacco).

Table 4:

Effects of ENDS Tax on Dual and Any Use

| Outcome | Current Dual Use | Current Any Use | Current Dual Use | Current Any Use |

|---|---|---|---|---|

| ENDS Tax Rate per ml (2019 $) | 0.004 | −0.01 | 0.005 | −0.046 |

| (0.004) | (0.013) | (0.012) | (0.034) | |

| [−0.004,0.012] | [−0.036,0.017] | [−0.020, 0.030] | [−0.115, 0.034] | |

| <0.371> | <0.462> | <0.701> | <0.187> | |

| Cigarette Tax Rate per Pack (2019 $) | 0.002 | −0.004 | −0.004 | 0.035 |

| (0.004) | (0.010) | (0.012) | (0.028) | |

| [−0.006,0.009] | [−0.024,0.016] | [−0.028, 0.021] | [−0.021, 0.091] | |

| <0.691> | <0.682> | <0.775> | <0.216> | |

| Data | MTF | MTF | YRBSS | YRBSS |

| Years | 2014–2019 | 2014–2019 | 2015–2019 | 2015–2019 |

| N | 123,631 | 123,631 | 524,842 | 474,336 |

| Dependent Variable Mean | 0.041 | 0.178 | 0.059 | 0.231 |

| ENDS Elasticity | 0.053 | −0.033 | 0.032 | −0.093 |

| Cigarette Elasticity | 0.112 | −0.068 | −0.177 | 0.455 |

p<0.10,

p<0.05,

p<0.01,

p<0.001

Notes: All MTF models include tax jurisdiction fixed-effects, year-by-quarter fixed-effects, and each of the individual controls and policy/economic covariates listed in Table 2. All YRBSS models include state fixed-effects, year fixed-effects, and each of the individual controls and policy/economic covariates listed in Table 2. Regressions are weighted, standard errors are corrected for clustering at the state level, 95% confidence intervals are shown in [ ] and p-values are shown in < >.

4.4. Heterogeneous effects of ENDS taxes

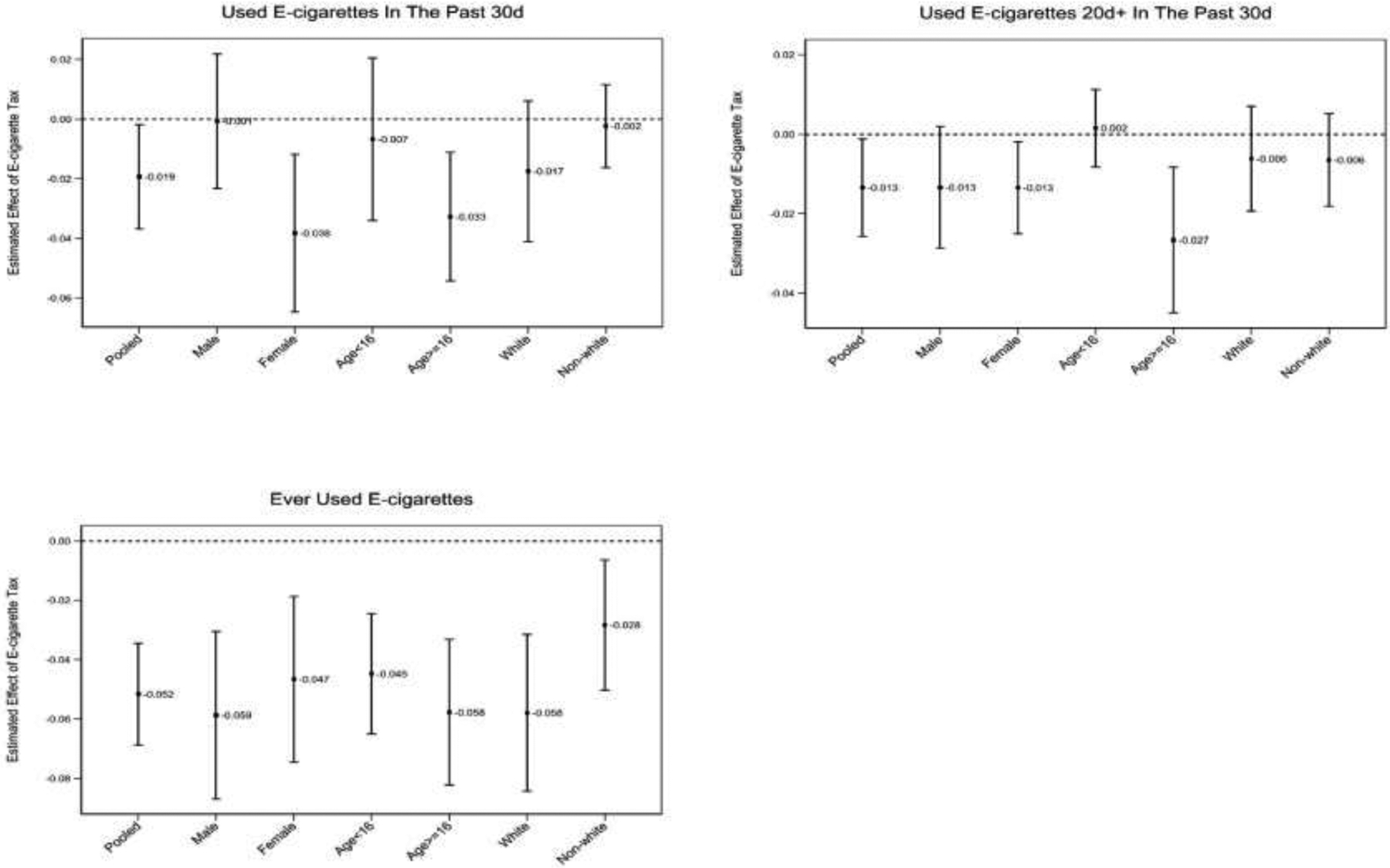

In Figures 2–5, we assess whether vaping- and smoking-responses to ENDS taxes differ across gender, age, and race for Table 3 outcomes that were statistically significant (p<0.10). These figures summarize estimates from stratified samples, parallel to the pooled-sample coefficient estimates presented in Tables 3. In our discussion of these results, we draw on the weight of the evidence across broad patterns that emerge from these coefficient estimates.

Figures 2 and 3 respectively present heterogeneous responses in ENDS use across sub-populations from the MTF and the YRBSS. The effect of higher ENDS taxes on ENDS use is largely negative for all groups, though some interesting differentials emerge. While ENDS taxes affect male and female ever-use similarly, only females show statistically significant current- and regular-use responses in MTF. The tax effect is also generally larger for older adolescents (ages 16+) than younger adolescents (ages < 16) in both data sources, consistent with more ENDS use among older teens. This pattern may also reflect greater reliance on retail sources among older teens, as retail purchases are expected to be more elastic to cost.22

Figure 2:

Heterogeneity Check, Box-Whisker Graphs for Standardized ENDS Tax Rate (MTF)

Notes: Estimated treatment effects are shown along with vertical bars depicting their 90% confidence intervals.

Figure 3:

Heterogeneity Check, Box-Whisker Graphs for Standardized ENDS Tax Rate (YRBSS)

Notes: Estimated treatment effects are shown along with vertical bars depicting their 90% confidence intervals.

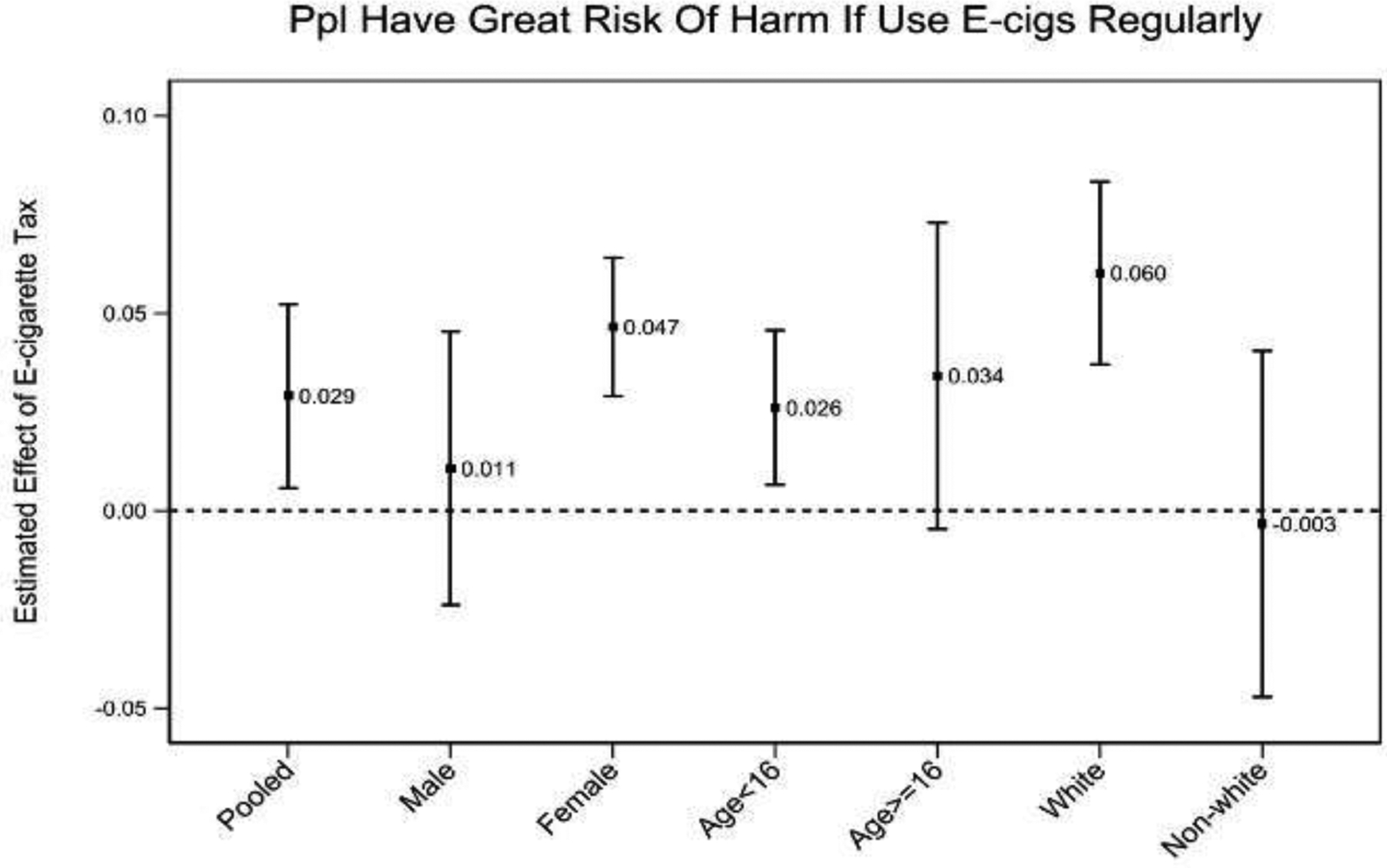

When it comes to risk perceptions regarding ENDS, there is some indication that female teens’ risk beliefs are more elastic with respect to taxes than males (Figure 4). Differences are even more evident by race: White teens exhibit a much stronger and significant upward revision of their perceived risk of ENDS in response to ENDS taxes, while effects for non-White teens are close to zero and insignificant.

Figure 4:

Heterogeneity Check, Box-Whisker Graphs for Standardized ENDS Tax Rate (MTF)

Notes: Estimated treatment effects are shown along with vertical bars depicting their 90% confidence intervals.

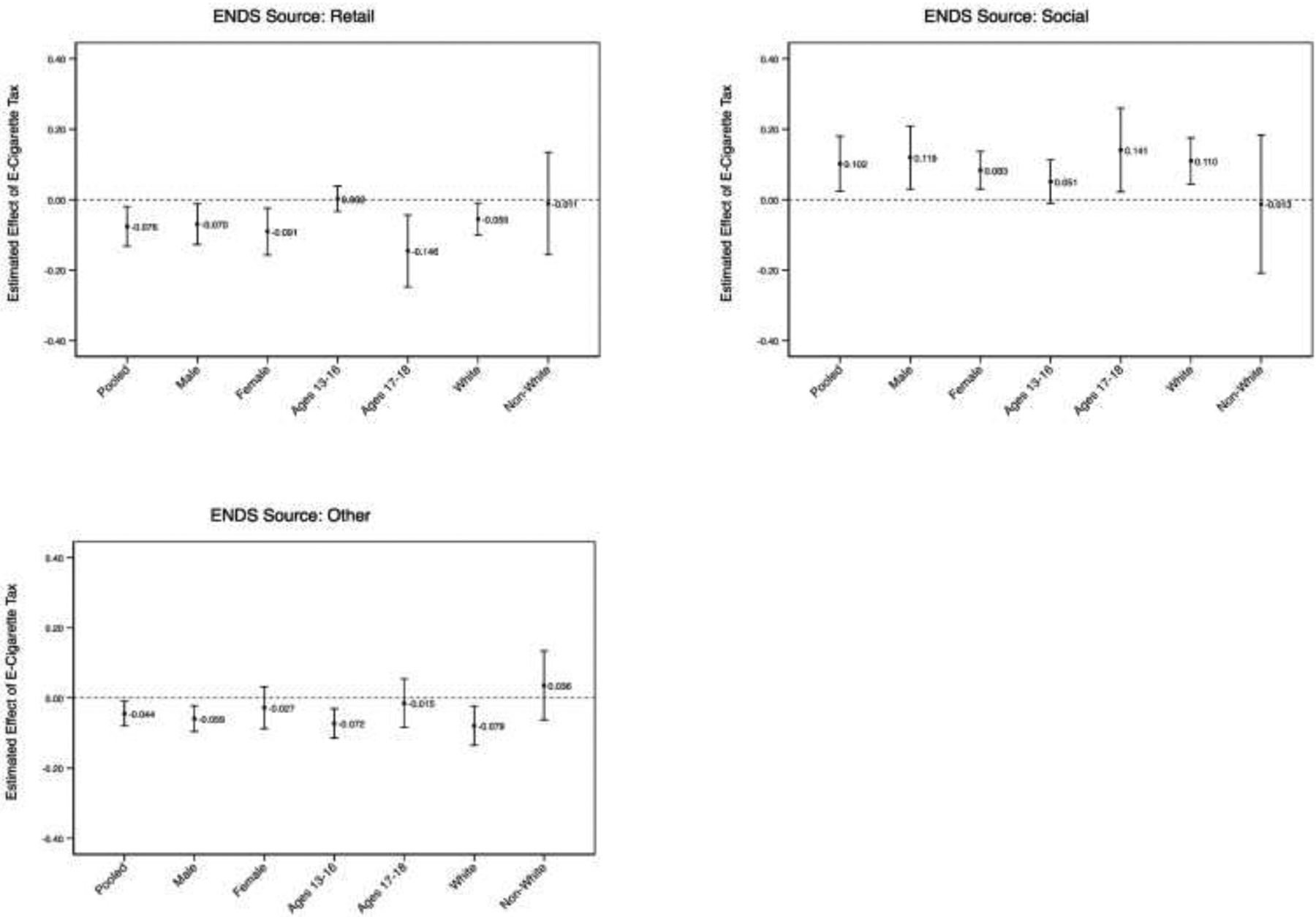

Figure 5 presents differential effects across sources of ENDS acquisition based on the YRBSS. Mirroring the heterogeneity in consumption and use by age, we find that retail purchases (a much more important source of ENDS for older teens and teens that regularly use ENDS) are significantly responsive to taxes for older but not younger adolescents. Similarly, higher ENDS taxes appear to significantly limit younger teens’ reliance on the social market, a source which tends to be relatively more important for that age-group.23 This relationship may operate as a chain reaction, since many younger teens obtain ENDS by borrowing them from friends or older peers. Specifically, if ENDS taxes constrain older peers’ ability to purchase ENDS from retail sources, downstream effects may limit younger teens’ ENDS access through social sources. Older teens may respond to ENDS taxes by substituting towards social sources and constraining their own retail purchases, though the substitution here is less than one-to-one. This behavior might be explained if, ex ante, older teens are more likely to pay for their ENDS, while younger teens rely more on “bumming” a vape. In this case, ENDS taxes would have more impact for older teens, and thus larger effects on their current and frequent ENDS use, in line with Figures 2 and 3. Those who substantially reduce their ENDS use in response to taxes may fall back on bumming ENDS from social sources—a habit that might be less socially acceptable or viewed as freeloading for regular or heavy users—instead of purchasing ENDS themselves.24

Figure 5:

Heterogeneity Check, Box-Whisker Graphs for Standardized ENDS Tax Rate (YRBSS)

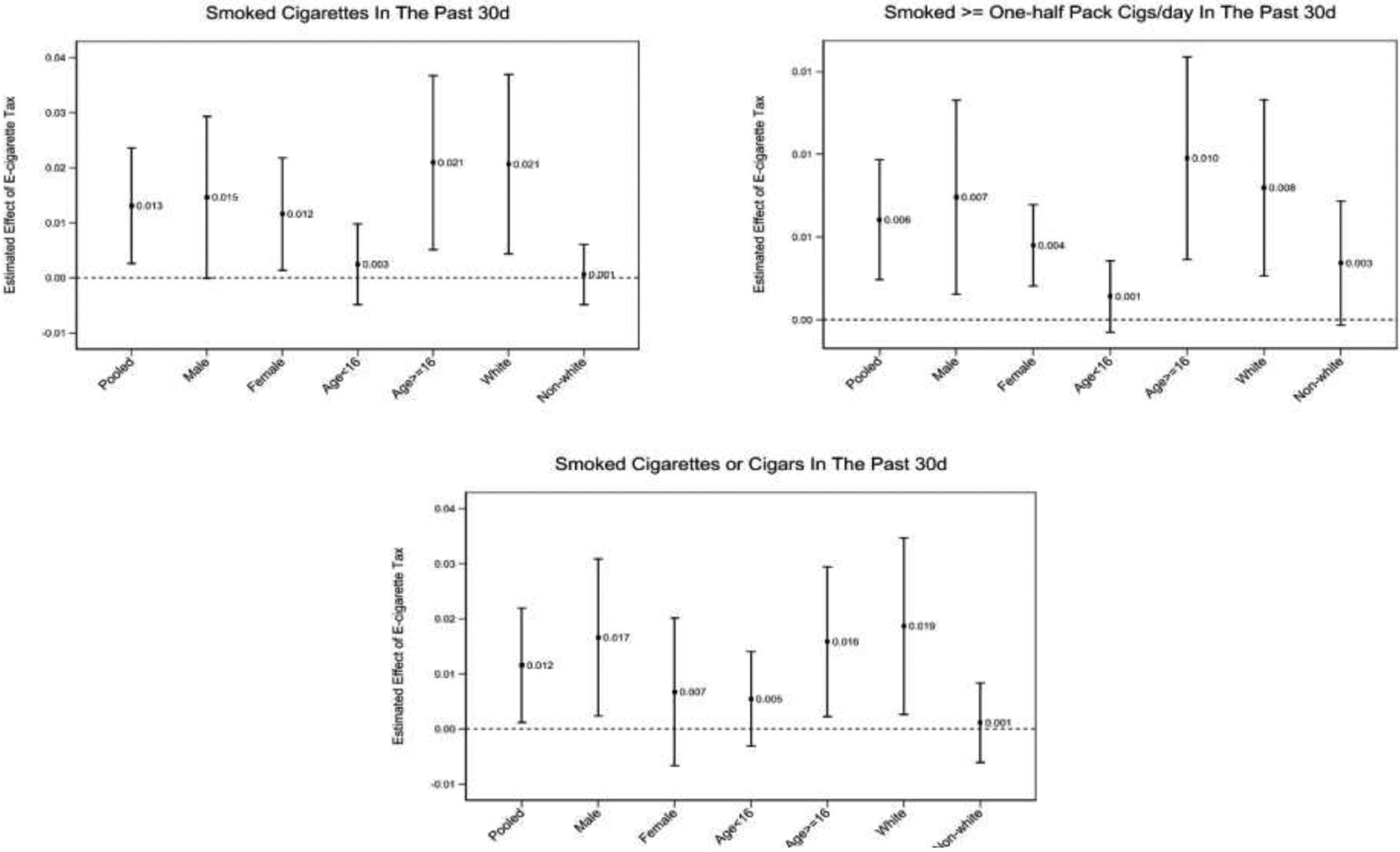

Finally in Figure 6, we assess heterogeneity in the cross-tax effects on combustible cigarette use for statistically-significant outcomes at baseline. Spillover effects mainly line up with the first-order effects on ENDS use. In particular, older and White teens tend to display a stronger substitution response towards cigarettes than younger and non-White teens.

Figure 6:

Heterogeneity Check, Box-Whisker Graphs for Standardized ENDS Tax Rate (MTF)

Notes: Estimated treatment effects are shown along with vertical bars depicting their 90% confidence intervals.

5. Checks of validity and robustness

Table 5, Table 6, and online appendix tables provide additional checks to assess the identifying assumptions’ validity and explore our main results’ sensitivity to alternate specifications, measurement error in the ENDS tax rate, added observable confounders, and sampling and other estimation issues.

Table 5:

Sensitivity Analysis, Adding One Period Lead

| Panel A: Effects of ENDS Tax on ENDS Use and ENDS Perceived Risk | ||||||

|---|---|---|---|---|---|---|

| Outcome | Current ENDS User | Regular ENDS User | ENDS Initiation | Ever Use ENDS | Current ENDS User | ENDS Perceived Risk |

| ENDS Tax Lead (0, 1) | −0.001 | 0.005 | 0.008 | 0.003 | 0.017 | 0.002 |

| (0.013) | (0.006) | (0.011) | (0.014) | (0.021) | (0.009) | |

| [−0.027,0.025] | [−0.006,0.016] | [−0.014,0.030] | [−0.026,0.031] | [−0.024, 0.059] | [−0.016,0.019] | |

| <0.952> | <0.364> | <0.476> | <0.856> | <0.406> | <0.849> | |

| ENDS Tax Rate per ml (2019 $) | −0.020+ | −0.012+ | −0.005 | −0.051*** | −0.061** | 0.029* |

| (0.010) | (0.007) | (0.013) | (0.012) | (0.021) | (0.014) | |

| [−0.041,0.001] | [−0.026,0.002] | [−0.031,0.021] | [−0.074,−0.027] | [−0.104, −0.018] | [0.001,0.058] | |

| <0.068> | <0.098> | <0.695> | <0.000> | <0.006> | <0.043> | |

| Cigarette Tax Rate per Pack (2019 $) | −0.005 | 0.010+ | −0.002 | 0.012 | 0.036 | −0.003 |

| (0.008) | (0.005) | (0.013) | (0.008) | (0.024) | (0.007) | |

| [−0.021,0.011] | [−0.000,0.020] | [−0.029,0.024] | [−0.004,0.029] | [−0.012, 0.083] | [−0.017,0.012] | |

| <0.540> | <0.059> | <0.853> | <0.129> | <0.136> | <0.708> | |

| −0.001 | 0.005 | 0.008 | 0.003 | 0.017 | 0.002 | |

| Data | MTF | MTF | MTF | MTF | YRBSS | MTF |

| Years | 2014–2019 | 2014–2019 | 2015–2019 | 2015–2019 | 2015–2019 | 2014–2018 |

| N | 126,306 | 126,306 | 66,124 | 85,541 | 538,992 | 86,486 |

| Dependent Variable Mean | 0.152 | 0.038 | 0.104 | 0.287 | 0.213 | 0.192 |

| Panel B: Effects of ENDS Tax on Combustible Tobacco Product Use | |||||||

|---|---|---|---|---|---|---|---|

| Outcome | Current Cigarette Use | Current Cigarette Use (half pack a day) | Current Cigarette or Cigar Use | Current Cigarette Use | Regular Cigarette Use | Daily Cigarette Use | Current Cigarette or Cigar Use |

| ENDS Tax Lead (0, 1) | −0.003 | −0.002 | −0.003 | 0.004 | 0.002 | 0.0005 | 0.0005 |

| (0.006) | (0.002) | (0.007) | (0.008) | (0.006) | (0.006) | (0.010) | |

| [−0.015,0.009] | [−0.006,0.002] | [−0.016,0.010] | [−0.012, 0.021] | [−0.011, 0.014] | [−0.012, 0.013] | [−0.019, 0.020] | |

| <0.646> | <0.358> | <0.643> | <0.607> | <0.794> | <0.942> | <0.960> | |

| ENDS Tax Rate (2019 $) | 0.012* | 0.006* | 0.011+ | 0.011 | 0.017 | 0.015 | 0.007 |

| (0.005) | (0.002) | (0.006) | (0.010) | (0.011) | (0.010) | (0.014) | |

| [0.001,0.023] | [0.001,0.010] | [−0.001,0.022] | [−0.009, 0.031] | [−0.006, 0.040] | [−0.006, 0.035] | [−0.021, 0.036] | |

| <0.029> | <0.012> | <0.066> | <0.291> | <0.145> | <0.166> | <0.612> | |

| Cigarette Tax Rate (2019 $) | −0.001 | −0.002 | −0.002 | −0.010 | −0.012 | −0.009 | −0.012 |

| (0.006) | (0.002) | (0.007) | (0.012) | (0.013) | (0.012) | (0.017) | |

| [−0.012,0.010] | [−0.006,0.001] | [−0.016,0.012] | [−0.034, 0.013] | [−0.038, 0.015] | [−0.032, 0.015] | [−0.045, 0.022] | |

| <0.855> | <0.187> | <0.787> | <0.378> | <0.372> | <0.471> | <0.492> | |

| Data | MTF | MTF | MTF | YRBSS | YRBSS | YRBSS | YRBSS |

| Years | 2014–2019 | 2014–2019 | 2014–2019 | 2015–2019 | 2015–2019 | 2015–2019 | 2015–2019 |

| N | 244,360 | 244,360 | 246,192 | 580,788 | 580,788 | 580,788 | 504,639 |

| Dependent Variable Mean | 0.066 | 0.012 | 0.080 | 0.080 | 0.019 | 0.014 | 0.107 |

p<0.10,

p<0.05,

p<0.01,

p<0.001

Notes: All MTF models include tax jurisdiction fixed-effects, year-by-quarter fixed-effects, and each of the individual controls and policy/economic covariates listed in Table 2. All YRBSS models include state fixed-effects, year fixed-effects, and each of the individual controls and policy/economic covariates listed in Table 2. Regressions are weighted, standard errors are corrected for clustering at the state level, 95% confidence intervals are shown in [ ] and p-values are shown in < >.

Table 6:

Sensitivity Analysis, Alternative Estimation Methods

| Outcome | Current ENDS User | Regular ENDS User | Ever Use ENDS | ENDS Perceived Risks | Current Cigarette Use | Current Cigarette Use (half pack a day) | Current Cigarette or Cigar Use |

|---|---|---|---|---|---|---|---|

| Baseline (Table 3) | −0.019+ | −0.013+ | −0.052*** | 0.029* | 0.013* | 0.006** | 0.012+ |

| (0.010) | (0.007) | (0.010) | (0.014) | (0.006) | (0.002) | (0.006) | |

| [126,306] | [126,306] | [85,541] | [86,486] | [244,360] | [244,360] | [246,192] | |

| Stacked DID | −0.018+ | −0.011 | −0.039*** | 0.022+ | 0.008 | 0.004* | 0.008 |

| (0.010) | (0.007) | (0.008) | (0.011) | (0.005) | (0.002) | (0.006) | |

| [649,259] | [649,259] | [420,214] | 515,496 | [1,313,040] | [1,313,040] | [1,323,656] | |

| de Chaisemartin & D’Haultfreuille (2022) | −0.081 | −0.029 | −0.153+ | 0.108 | 0.049 | 0.021 | 0.034 |

| (0.080) | (0.034) | (0.092) | 0.135 | (0.046) | (0.017) | (0.049) | |

| [726] | [726] | [726] | [504] | [726] | [726] | [726] | |

| Data | MTF | MTF | MTF | MTF | MTF | MTF | MTF |

| Years | 2014–2019 | 2014–2019 | 2015–2019 | 2014–2018 | 2014–2019 | 2014–2019 | 2014–2019 |

p<0.10,

p<0.05,

p<0.01,

p<0.001

Notes: Estimated coefficients for ENDS tax rate per ml (2019 $) reported. All MTF models include tax jurisdiction fixed-effects, year-by-quarter fixed-effects, and each of the individual controls and policy/economic covariates listed in Table 2. We estimate these alternative estimation methods using only MTF because YRBSS is otherwise limited by having only three waves of data for e-cigarette use outcomes and by a lack of substate information used in the stacked difference-in-differences model. Regressions are weighted (or in application of de Chaisemartin & D’Haultfoeuille [2022] the regression is estimated using aggregate data in which weights were applied at the time of collapsing), standard errors are corrected for clustering at the state level, estimate sample sizes are shown in [ ].

The tax-response parameters are identified off within-jurisdiction changes over the sample period in the two-way fixed effects regressions, drawing on the assumption of strict exogeneity (Wooldridge 2010). This implicitly presumes that jurisdictions that have not adopted any ENDS taxes or changed their ENDS tax rates are valid counterfactuals for the “treated” jurisdictions. More specifically, a consistent estimate of the tax-response parameter (β1 in equation 1) requires that the tax rate in a given jurisdiction and period t be orthogonal to that locality’s error term in all periods. Violations of this assumption are usually driven by either time-varying jurisdiction -specific unobservables correlated with the ENDS tax, or policy endogeneity, wherein the jurisdiction’s past experiences with youth ENDS use may influence its enactment and level of ENDS taxation.

The recency of most jurisdiction’ ENDS tax adoption and youth surveys’ addition of ENDS use questions prevents estimation of flexible event-study models for ENDS use outcomes.25 We therefore check for potential policy endogeneity and assess the broader identifying assumption by re-estimating models with the inclusion of a one-period lead on ENDS tax adoption (Table 5).26 These models underscore two points which instill some degree of confidence in the credibility of the research design. First, coefficient estimates on the lead for ENDS adoption are statistically insignificant, invariably smaller than the main effect, and largely close to zero in all models. This finding suggests that trends in ENDS use outcomes prior to the adoption of the tax do not materially differ between treated and control jurisdictions. Second, our main ENDS tax effects on ENDS and cigarette use are not materially altered by controlling for the lead on policy adoption.

In Table 6, we show results using alternative estimation strategies.27 Emerging literature has identified important issues that arise in TWFE analyses with staggered adoption of the treatment, as in our case with multiple jurisdictions shifting their ENDS tax policy at different times. In the presence of dynamic treatment effects, the treatment effect recovered by the TWFE model may be biased and may capture the true treatment effect plus additional terms that reflect deviations from parallel trends and bias due to treatment effect dynamics and heterogeneity (Goodman-Bacon 2021). The latter bias is often largely due to using earlier-treated units as a counterfactual for later-treated units.

This issue of such bias may be less problematic here than in other contexts given that only nine states plus Washington DC and two large counties imposed taxes on ENDS by mid-2019, when our sample ends. Consequently, we have a large untreated comparison group and, as ENDS taxes are relatively recent phenomena within US markets, few instances of earlier-treated units serving as a counterfactual for later-treated units, minimizing such concerns. This hypothesis is confirmed by a decomposition (Goodman-Bacon 2021) of the comparisons driving the estimated treatment effects in our MTF analyses (dichotomizing our tax variable). This decomposition indicates that between 91.6% and 94.4% of the weight of our estimator (depending on the time horizon available for each outcome) can be attributed to the comparison of treated states (states that have imposed an ENDS tax) versus never adopters, and between 1.9% to 3.0% can be attributed to the comparisons of earlier-adopting versus later-adopting states. The potentially problematic comparison—using earlier-treated or already-treated states as a counterfactual for later-treated states—drives only about 3.7% to 5.4% of the average treatment effect in our estimation.

To excise potential impacts from dynamic treatment effects, our first approach is a “stacked difference-in-differences estimator” (Cengiz et al. 2019). For this, we first define a common “event window” around the adoption of an ENDS tax: two years prior to the tax, the year of the tax, and one-year post-tax.28 We then define a “cohort” as a collection of treatment tax jurisdictions that experience an “event” at the same time (i.e., jurisdictions that adopt an ENDS tax at the same time). We allow for separate cohorts for tax jurisdictions that adopt the tax in the same period, but have a different “dose” of the event (i.e., ENDS tax level), which allows different doses of the event to have differential impacts. Second, for each cohort, we select tax jurisdictions that have never implemented an ENDS tax by the end of our study period (“never treated”) and those tax jurisdictions that have not yet adopted an ENDS tax during the event window (“not yet treated”) to serve as the comparison group.29 By selecting treatment and comparison tax jurisdictions in this manner, we are able to account for two sources of bias in TWFE with a staggered treatment regime: 1) comparing later treated units to earlier treated units which can lead to bias and (potentially) negative weighting if there are dynamic treatment effects across tax jurisdictions (i.e., “forbidden comparisons” (Borusyak, Jaravel, and Spiess 2022)), and 2) variance weighting which places the most weight on observations whose treatment “turns on” in the middle of the panel (these observations have the greatest variance in treatment status and thus OLS, in minimizing the sum of squared errors, upweights these observations) and may therefore lead to poor estimates of the average treatment on the treated (ATT) effect if there is heterogeneity in the ATT. Finally, we stack each cohort (i.e., collections of treatment tax jurisdictions and each group’s comparison tax jurisdictions) and estimate an equation similar to that outlined in Equation (1), but we include cohort-specific tax jurisdiction fixed effects and cohort-specific time fixed effects. We continue to cluster standard errors at the tax jurisdiction-level. For tax jurisdictions that have multiple tax changes, we do not consider later tax changes that occurred outside the event window since these tax jurisdictions are already treated and the effects of later tax changes may be conflated with potential dynamic effects of the earlier tax changes. We also exclude Minnesota as this state was treated throughout our study period.

The middle panel of Table 6 presents estimates of the tax response from this stacked difference-in-differences model. Reassuringly, our previous findings stand: we find consistent and robust evidence that higher ENDS taxes significantly reduce adolescent ENDS use along multiple margins. The stacked difference-in-differences estimates further suggest, as before, that higher ENDS taxes are associated with a greater perceived risk of ENDS and substitution into cigarettes. Coefficient magnitudes of the substitution effects are attenuated by roughly one-third compared to those from the baseline model, and as a result only one of three smoking outcomes remains precisely estimated.

Finally, the bottom panel of Table 6 presents results from a recently proposed estimator by de Chaisemartin and d’Haultfoeuille (2022): the multiperiod difference-in-differences (MDID).30 Similar to the stacked difference-in-differences estimator outlined above, the MDID estimator produces parameter estimates that are robust to bias from heterogeneous and dynamic treatment effects. MDID is able to accommodate both reversible and multi-valued treatments, which is valuable in our setting. We collapse the data to the tax jurisdiction-year-quarter level using population weights. While MDID can accommodate multi-valued treatments, the estimator cannot accommodate fully continuous treatments such as our ENDS tax variable. Therefore, we re-categorize the continuous ENDS tax into the following bins to create a multi-valued treatment variable: no tax, $0.01 to $1.00 tax, $1.01 to $2.00 tax, and $2.01 to $2.52 (the highest tax amount we observe through mid-2019). We account for within-tax jurisdiction correlations in calculating standard errors. The coefficient estimates show the average effect over the post period for a one unit change in treatment intensity, relative to the period before the ENDS tax comes into place. Coefficient estimates are all in the same direction as our baseline results and sizably larger, though also imprecise. The reduction in precision may be attributable to the MDID estimator being less efficient than OLS, the loss of power from aggregating from the microdata to the tax jurisdiction-quarter-year level, conversion from the continuous measure to a multi-valued variable, and/or better representation ofuncertainty in the effect of e-cigarette taxes on youth tobacco use.

We show that our coefficients are broadly similar to baseline results when modeling the dichotomous outcomes via probit regression (marginal effects are presented in Online Appendix Table 2).31 Since source outcomes are mutually exclusive, we also model this using a multinomial logit model in Online Appendix Table 3. We include in this model a category for not using ENDS so as to not condition the sample on only users. Here we find that a $1.00 increase in ENDS taxes increases the probability of not using ENDS by 3.1 pp, reduces the probability of purchasing from retail sources by 1.6 pp, and reduces the probability of obtaining ENDS from other sources by 1.0 pp. There are no statistically significant reductions in obtaining ENDS from social and internet sources, which is consistent with baseline results that are conditional on remaining an ENDS user.

Next, in Online Appendix Tables 4, we show the effect of controlling for alternative sets of variables.32 We show our baseline results (from Table 3) in the first row. In the second row, we add other state-level tobacco control policies of ENDS licensure laws, ENDS product packaging laws, and K-12 public school campus bans for smoking and vaping products.33 The coefficient estimate on ENDS taxes is similar to baseline results when adding the extra controls. In the third and fourth rows, we add little and large cigar tax variables. Each category of cigar has ad valorem and excise taxes depending on the state, and states use different thresholds for determining what constitutes a little cigar; therefore, this lack of standardization makes it difficult to control for these taxes. While results vary somewhat depending on which set of cigar tax variables we control for, across both specifications we collectively find evidence supporting the robustness of all previously reported relationships. Finally, in the last row we control for unique variables available in the MTF: parental education and a respondent’s county’s urban/rural status.34 These controls have no noticeable impact on previously reported relationships.

Next, in Online Appendix Table 5 we show robustness of our results to using alternative samples. In particular, we drop two states that adopted ENDS MLSA and licensure laws at the same time that ENDS taxes came into place,35 we retain irregularly surveyed states in the MTF that we otherwise dropped from our main analysis, and we use a longer time horizon (through 2011) for cigarette outcomes.

In Online Appendix Table 6, we show results using alternative estimation strategies. First, we show instrumental variables (IV) estimates from models where the standardized tax rate is instrumented with the separate tax components (i.e., ad valorem tax rate, liquid excise tax rate, container excise tax rate). This strategy may reduce any bias due to measurement error in the standardized tax construction. The F-statistic exceeds 10,000, and the IV results are virtually identical to baseline results.

Finally, we show that our results are consistent when using a broader “any vaping” variable (including of THC) that became available in 2017 (Appendix Table 7) and when not utilizing population weights (Appendix Table 8). In Online Appendix Table 9 we show little in the way of changes in statistical inference when accounting for the small number of treated units through wild cluster bootstrapping, or when accounting for multiple comparisons using Holm-Bonferroni adjustment36 or a sharpened two-stage adjustment (Benjamini, Krieger, and Yekutieli 2006; Anderson 2008).

6. Discussion

Our study contributes to the literature by 1) using multiple large-scale youth survey datasets to provide some of the first national evidence of ENDS taxes’ effects on youth, and 2) studying the effect of ENDS taxes on youth using four types of outcomes: ENDS use, cigarette use, perceptions of the risk of ENDS, and source of ENDS. By estimating ENDS taxes’ effects on youth use of both ENDS and cigarettes, as well as intensity of use, ENDS sources, and ENDS risk perceptions, this research provides the most comprehensive picture to date of ENDS taxes’ effects on youth, whom legislators often claim they are protecting when taxing ENDS. While our baseline results yield ENDS tax elasticities ranging from −0.06 to −0.21 depending on the measure of ENDS use, and indicate that ENDS taxes increase perceptions of ENDS risks, other findings suggest concurrent costs: cross-tax elasticities are positive and particularly large for frequent cigarette use outcomes, and sourcing results suggest that ENDS taxes shift youth towards social ENDS sources. The latter change may have implications for short- and long-run health outcomes, as observed during the 2019 outbreak of vaping-associated lung injuries, when use of informally sourced cannabis vaping products containing vitamin E acetate led to a rash of illnesses and deaths.

As of March 2022, 30 US states had adopted an ENDS tax (Public Health Law Center 2022). However, if reducing ENDS accessibility increases combustible tobacco use, as suggested by this study and prior work (Pesko, Courtemanche, and Maclean 2020; Saffer et al. 2020; Pesko and Warman 2021; Abouk et al. 2022; Cotti et al. 2022; Friedman 2015; Dave, Feng, and Pesko 2019; Pesko, Hughes, and Faisal 2016; Pesko and Currie 2019; Friedman and Pesko 2022; Pesko 2022a), these taxes could potentially prove harmful to public health. That is, given current evidence suggesting smoking is substantially more dangerous than using ENDS, the health costs from greater youth smoking as a result of ENDS taxes may considerably undercut or even outweigh benefits from reduced youth ENDS use, though an exact calculation is beyond the scope of this research.