Abstract

Based on data on school visits from Safegraph and on school closures from Burbio, we document that during the Covid-19 crisis secondary schools were closed for in-person learning for longer periods than elementary schools, private schools experienced shorter closures than public schools, and schools in poorer US counties experienced shorter school closures. To quantify the long-run consequences of these school closures, we extend the structural life cycle model of private and public schooling investments by Fuchs-Schündeln et al. (Econ J 132:1647–1683, 2022) to include private school choice and feed into the model the school closure measures from our empirical analysis. Future earnings and welfare losses are largest for children that started public secondary schools at the onset of the Covid-19 crisis. Comparing children from the top to children from the bottom quartile of the income distribution, welfare losses are 0.5 percentage points larger for the poorer children if school closures were unrelated to income. Accounting for the longer school closures in richer counties reduces this gap by about 1/4. A policy intervention that extends schools by 6 weeks generates significant welfare gains for children and raises future tax revenues sufficient to pay for the cost of this schooling expansion.

Keywords: Covid-19, School closures, Inequality, Intergenerational persistence

Introduction

Governments around the world responded to the Covid-19 health crisis by shutting down economic and social activity, resulting in severe recessions and closed schools for much of 2020. The economic consequences of these lockdown measures triggered a large scientific and popular literature. As many countries are on the path of economic recovery from this crisis, focus is shifting from the short- to the long-run consequences of the crisis. One such concern is the long-run impact of the significant loss of instructional time in schools during 2020–21 on children’s education, earnings potential and future welfare.

In this paper, we use a structural life-cycle model and school visit measures from anonymized cell phone data combined with learning mode data to quantify the heterogeneous impact of school closures during the Covid-19 crisis on children affected at different ages and coming from households with different socio-economic parental characteristics. Our data suggests that secondary schools were closed for in-person learning for longer periods than elementary schools, implying that younger children experienced shorter school closures than older children, and that private schools1 experienced shorter closures than public schools, and schools in poorer US counties experienced shorter school closures. We use these empirical facts as inputs for a positive and normative analysis of the long-run consequences of the observed Covid-19-induced school closures on the affected children. To do so, we extend the structural life cycle model of schooling investments studied in Fuchs-Schündeln et al. (2022) to include the choice of parents to send their children to private schools, empirically discipline it with data on parental investments from the PSID, and then feed into the model the school closures measures from our empirical analysis to quantify the aggregate and distributional consequences of the Covid-19 school closures.

We highlight two main findings. First, the aggregate losses of human capital, college attainment, the present discounted value of earnings and welfare are large: the present discounted value (PDV) of future gross earnings (after the current school children enter the labor market) falls by 1.27% and the welfare losses amount to 0.71% of permanent consumption. These results materialize despite the fact that parents optimally adjust their private time- and resource investment into their children, as well as inter-vivos transfers of wealth to their offspring.

Second, if all children had their schools closed for the same amount of time, then younger children, and those from disadvantaged backgrounds would suffer larger welfare losses, as our previous work suggested.2 However, due to the significant empirically documented differences in the extent of the school closures, these conclusions are partially overturned, and partially accentuated. The fact that, on average, secondary schools were closed much longer than primary schools leads to the finding that it is children just starting secondary school that endure the largest losses in their earnings capacity (a reduction of the PDV of earnings of approximately 1.5%) and welfare (a decline of 0.83%).

Turning to socio-economic characteristics, we make two empirical observations. First, private schools were closed on average for fewer days than public schools, and private schools are dis-proportionally frequented by children from parents with higher socio-economic characteristics (in the model, associated with higher education, higher wealth and being married). However, focusing on only public schools, these were closed for longer in counties with higher average income.

The quantitative model maps these empirical findings into expected differential welfare consequences. Children attending private schools on average lose points less welfare (measured in terms of permanent consumption), than children attending public schools, accentuating the larger welfare losses poorer children have in the absence of differential school closures. Within public schools, however the income gradient of welfare losses goes in the opposite direction since poorer areas in the USA, especially in the South but also the Midwest, saw shorter school closures on average than the more affluent regions on both coasts. Of course, children from poorer households are still worse off and might have been affected more severely from the Covid-19 crisis along many other dimensions, but the fact that, again on average, their schools were locked for shorter periods of time than the schools in richer counties implies that the losses in human capital, lifetime earnings, and ultimately, welfare, are more benign than those children from richer families (or more precisely, residing in richer counties).

Finally, and motivated by the significant and heterogeneous human capital and welfare losses we consider potential policy interventions designed to mitigate the instructional losses from the Covid-19 crisis. One such proposal is to keep schools open for parts of future summer periods to make up the lost time. In the model, since we have a well-defined cost of schooling and model-predicted consequences of additional schooling on future human capital, earnings and taxes, we can ask whether such a measure is a positive net present discounted value proposition for households. Furthermore, since a policy intervention that keeps all schools open might not be feasible due to scarcity in the availability of teachers or physical infrastructure, we also investigate for which group of students such a policy intervention is especially promising, both in terms of the budgetary consequences for the government and in terms of welfare for the individual students. We find that for the average child the welfare gains from expanded schooling are significant (0.22% in terms of consumption equivalent variation), and induce an increase in future revenues from labor income and consumption taxes approximately sufficient to pay for the entire cost of the reform; that is, the reform is essentially budget-neutral. Finally, the welfare gains from the expansion are highest for children from income-poor households, whereas the fiscal consequences for the government look most favorable if the intervention is targeted to children from the most affluent households.

In the next section, we briefly relate our model to the existing literature. Section 3 describes the data we use to construct measures of school closures and the empirical measures of school closures we will employ in the structural model. That model is spelled out in Sect. 4 and calibrated in Sect. 5. We present the results on the differential welfare consequences of the school closures in Sect. 6, and Sects. 7 and 8 contain the counterfactual policy analysis and robustness analysis, respectively. Section 9 concludes. Details about the construction of the data as well as the dynamic programs in the model can be found in Appendix.

Related Literature

Our paper is part of the massive literature on the consequences of the Covid-19 epidemic on the economy. The early literature focused on short-run predictions of the evolution of the health crisis and the economic recession, triggered by a fall in the healthy work force and its desire to work in risky sectors, the demand for goods and services induced by falling household incomes as well as massive government-mandated economic lockdowns. Representative contributions include Atkeson (2020), Fernandez-Villaverde et al. (2020), Greenstone et al. (2020) and Alemán et al. (2021) on the health side and Eichenbaum et al. (2020) as well as Krueger et al. (2020), Moll et al. (2020) on the economic side. A subset of this literature (see, e.g., Argente et al. (2020), Acemoglu et al. (2020), Glover et al. (2020), Brotherhood et al. (2020)) has considered optimal lockdown policies, where the main benefit of shutting down part of the economy is a slower transmission of the virus, and the main cost is modeled as the reduction of economic activity and thus incomes of individuals of current working age. The paper by Ma et al. (2022) makes the important point that the impact of the economic contraction on child mortality, especially in developing economies, can be so severe to render lockdown measures counterproductive for protecting the lives of children. The potential impact of closing schools as part of the lockdown is not considered in this literature.

Complementary to this work, our paper takes a longer-run perspective and analyzes the consequences of one specific aspect of the crisis, school closures, that initially did not receive much attention, likely due to the fact that the main costs associated with this non-pharmacological intervention accrue mostly in the medium to long-run when the cohort of school children affected by school closures enter the higher education- or labor market. In our previous work (Fuchs-Schündeln et al. 2022) we used a structural life cycle model to quantify the impact of a hypothetical school closure for 12 months on average human capital accumulation, lifetime earnings and welfare. In the current paper we build on this framework, but turn to school visits data from Safegraph and information on school learning modes from Burbio to measure the actual length of school closures. Crucially, we argue that there is significant heterogeneity across school types (public versus private), grade level (elementary versus secondary), and parental backgrounds in the extent to which schools were closed. This analysis is motivated by an emerging body of evidence that learning achievement during the pandemic was substantially lower than in prior years, suggesting that the virtual instruction brought about by school closures was much less effective than traditional in-person instruction.3

Therefore, the main contribution of the current paper is to develop a new measure of effective school closures using Safegraph school visits data and employ it in a structural life cycle model with human capital accumulation to quantify the long-run earnings and welfare consequences of the affected children. On the empirical side, the Safegraph visits data has been used by other studies to measure social distancing behavior, the impact of the pandemic on in-person services, and industry affiliation of particular businesses (e.g., Allcott et al. (2020), Goolsbee and Syverson (2021), or Kurmann et al. (2021) among many others). The papers closest to ours are Chernozhukov et al. (2021) and Bravata et al. (2021) who estimate the association between changes in Safegraph visits to schools and the spread of Covid-19 at the county level, as well as Parolin and Lee (2021) who use the Safegraph data to construct a school closure index and, like us, match the Safegraph data with information from NCES and other sources to relate their school closure index to grade level (elementary versus secondary) and a variety of socioeconomic indicators.4 Different from these papers, we build on the approach by Kurmann and Lalé (2021) and combine the Safegraph visits data with data on learning modes by Burbio to estimate a mapping of changes in school visits to in-person schooling time. This allows us to construct a measure of effective schooling time by school type (public versus private school), grade level, and parental background, which in turn constitutes a crucial input for our model simulations.5

On the modeling side, we take a structural approach to answer our applied policy question, building on the literature modeling human capital accumulation in children of school age and public education, see, e.g., Cunha et al. (2006), Cunha and Heckman (2007), Cunha et al. (2010), Caucutt and Lochner (2020), Kotera and Seshadri (2017), Lee and Seshadri (2019), Yum (2020), Caucutt et al. (2020), Daruich (2022), Morchio (2022), Jang et al. (2021) and especially Agostinelli et al. (2020). A complementary, more empirically oriented literature, assesses the importance of instruction time or schooling inputs for student outcomes, see, e.g., Lavy (2015), Carlsson et al. (2015), Rivkin and Schimann (2015), Fitzpatrick et al. (2011), Pischke (2007),Jaume and Willén (2019), Werner and Woessmann (2021) and Maldonado et al. (2021).6

Data

In this section, we describe the data and procedures to measure effective schooling time during the pandemic. We start with the Safegraph data, how we measure changes in visits to schools, and how we match the schools with records from the National Center for Education Statistics (NCES) to obtain information on different school characteristics. Then, we show how we use Burbio data on school learning modes to map changes in school visits to total in-person learning and effective schooling time. Finally, we present the empirical results that serve as input for the structural model simulations.

Measuring In-person Learning

Safegraph School Visit Data

The first source of information for measuring in-person learning comes from Safegraph, which provides data for over 6 million Places of Interest (POIs) for the USA using cell phone pings.7 From this large set of POIs we extract establishments with North American Industry Classification System (NAICS) code 611110 (“Elementary and Secondary Schools”) that are present in Safegraph’s Weekly Patterns, which provides data on weekly visits by POI. We then match Safegraph’s POIs with NAICS code 611110 by school name and address to public and private schools from the Department of Education’s National Center for Education Statistics (NCES), resulting in about 102,500 high-quality matches of schools with Safegraph data on weekly visits. Appendix B provides details of the matching procedure and results. Relative to the universe of schools in the NCES, we lose about 22,000 schools, but the matched school sample remains highly representative of the overall population of schools in terms of socioeconomic and geographic makeup.

Measuring Changes in School Visits

The Safegraph data provide weekly visit counts for each school by dwell times. There are dwell time intervals (less than 5, 5 to 10, 11 to 20, 21 to 60, 61 to 120, 121 to 240, more than 240 minutes), Denoting weekly visits counts as for , the total visits count for school j in week t is

As Fig. 4 in Appendix shows, prior to the pandemic, both aggregate total visit counts and aggregate visits longer than 240 minutes per day decline markedly during the weeks of Thanksgiving, Christmas, and Summer break. In addition and in line with the public health emergency declared on March 13, 2020, both visits series drop precipitously during the week of March 15 to March 21, 2020, and remain substantially lower thereafter.

Fig. 4.

Aggregate time series of visits (week 1 = 1st week of 2020)

We construct changes in school visits as the dwell-time weighted growth rate in visits relative to average visits prior to the pandemic. This measure, which is different from Chernozhukov et al. (2021), Bravata et al. (2021), and Parolin and Lee (2021) who instead consider year-over-year changes in visits, has the advantage that it is not affected by holidays and other variations in visits that fall on different weeks across years, thereby reducing measurement error. Furthermore, we normalize weekly visits for each school by the county-level count of cell phone devices in the Safegraph data so as to control for spurious variations in school visits due to changes in sample coverage.8 The construction of our measure of school visit changes involves three steps:

- For each school j, we define weights as:

where denotes the base period (November 2019 through the end of February 2020, excluding the weeks of Thanksgiving, Christmas and New Year); and measures the contribution of a dwell time d to school j’s raw visits counts during the base period. - Using the weights, we measure weighted weekly visits at school j in week t as

where denotes the normalization by SG devices during week t in county in which the school j is located. - Given weighted and normalized school visits, we measure the change in school visits as

where is the mean value of during the base period.

In order to further reduce measurement error, we top-code at 100%. In addition, if in any week t outside of the base period while and , we replace by the average of and . This adjustment implements the assumption that during the school year 2020–21, schools did not reopen for only one week at a time. Finally, we drop about 30,000 schools with sparse or very noisy visit data, and apply weights to ensure that the remaining sample of roughly 70,000 schools remains representative of the full sample of schools in the USA. See Appendix B.1 for details on the sample selection criteria and weighting procedure.

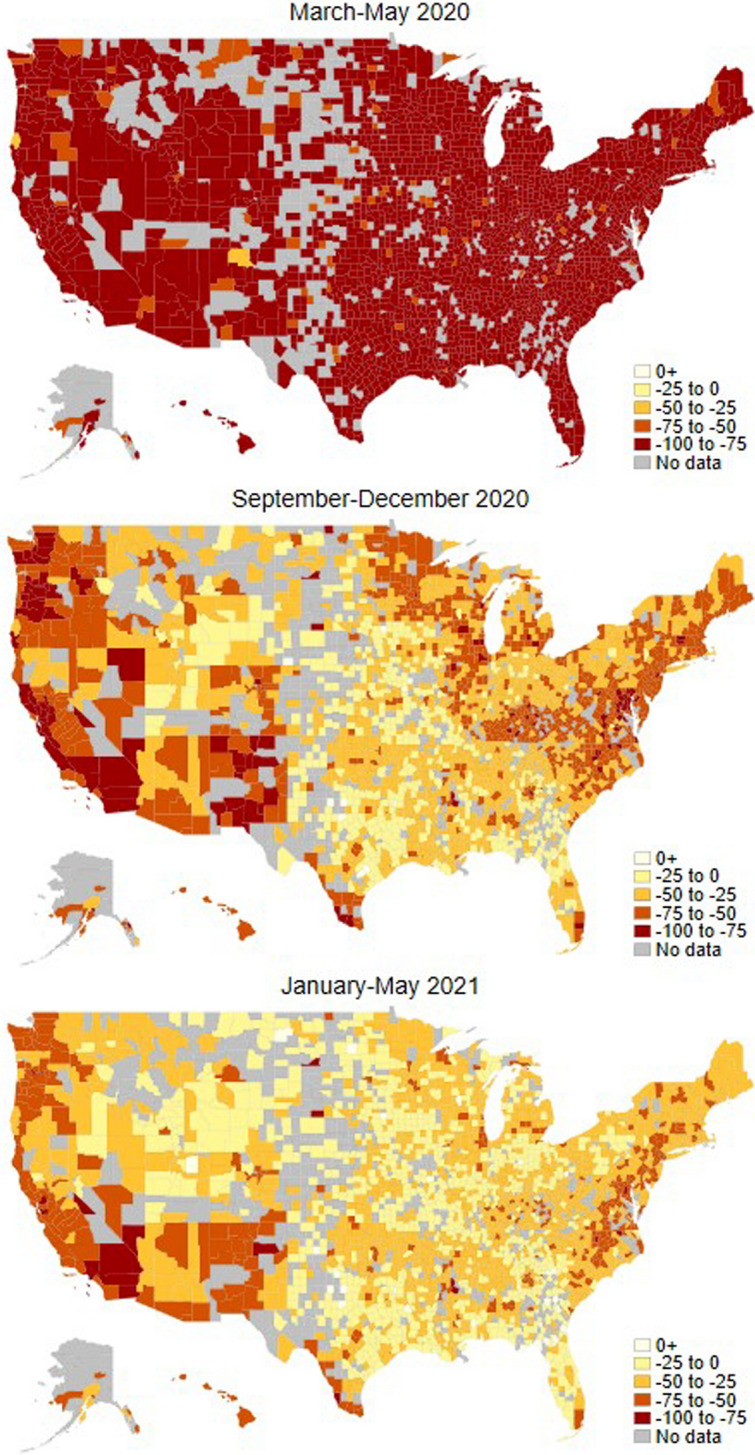

Figure 1 presents histograms of the distribution of changes in school visits during three subperiods (averaged over the weeks within a subperiod). The figure shows that relative to the pre-pandemic period, school visits declined massively during March–May 2020, and were still significantly lower during September–December 2020 and (less so) during January–May 2021.

Fig. 1.

Distribution of changes in school visits for selected subperiods

Figure 2 shows the geographical variation in county average school visit changes for the three subperiods. During March–May 2020, school visits were 75 to 100 percent below pre-pandemic levels, without much regional variation. During September–December 2020, in contrast, we observe substantial variation in school visits across different regions, as many schools in the Southern, Midwestern, and Central Northern parts of the USA reopened while schools in the Western and Eastern parts remained largely closed. During January–May 2021, the situation becomes again more even, with school visits returning toward pre-pandemic levels in most counties except on the West Coast, parts of the East Coast, and a few other counties across the USA.

Fig. 2.

Average Change in School Visits by County: March–May 2020

From Changes in School Visits to In-person Learning

While the Safegraph data provide us with a high-frequency measure of changes in school visits for a large, representative sample of public and private schools, it is not clear what a given decline in school visits represents in terms of lost in-person learning. To map changes in school visits into a measure of in-person learning, we relate our school visit data to estimates of school learning mode from Burbio. Burbio is a private company that collects data for 1200 public school districts representing 47 percent of USA. K-12 student enrollment in over 35,000 schools in all 50 states. The data is aggregated to the county level and primarily used for commercial purposes, but the company generously shared the data with us and other researchers. The information on learning mode consists of weekly indicators between mid-August 2020 and mid-June 2021 that for each county provide the percent of public school students engaged in a traditional, a hybrid, or a virtual learning mode. Traditional means that students attend in-person school every day of the week; hybrid means that students attend 2–3 days per week in-person; virtual means that students do not attend school in person. Appendix B.2 contains details about the Burbio data.

To construct the mapping, we start by computing county-level averages of the fractions that public school students spent in learning mode between week and week from the Burbio data, i.e.,

| 1 |

where denotes the percent of students in county c who spent week t in learning mode L; and is the number of weeks considered. For instance, for computed from September 2020 to June 2021 means that public school students in county c spent one third of the school year 2020–2021 in traditional learning mode.

Next, we define the fraction of the school year that students in county c effectively spent in in-person learning mode as and the fraction effectively spent in virtual learning mode as , where measures the fraction of total student-days that are spent in person when the learning mode is hybrid. We then relate these measures to the change in Safegraph school visits with the following linear regression

or equivalently,

| 2 |

where is the student-weighted average of changes in school visits across schools in county c. The regression tells us not only how a given change in school visits maps into total in-person learning relative to its pre-pandemic level, , but also the average proportion of in-person learning when students are in hybrid mode. Since , the regression also tells us how a given change in school visits maps into total virtual learning .

We estimate (2) using Burbio and Safegraph data for Fall 2020 only. The reason we do not use data for Winter and Spring 2021 is that during this period, school districts increasingly moved away from virtual learning. As a result, changes in traditional learning are close to linear with hybrid learning . In a regression, this implies and since is subject to idiosyncratic noise. During Fall 2020, in contrast, there are changes across all three learning modes, which enables us to identify the mapping between and , controlling for .

Table 1 reports the results of the estimation. In column (1), we consider all counties for which we have data on both Burbio learning modes and Safegraph school visits (3049 out of 3124 available counties in Burbio). The sample represents almost 95 percent of all public-school students in the USA. The mapping between the different variables is tightly estimated, with a of over 0.5 and highly significant coefficients. A 1 percentage point decline in school visits reduces the average fraction of weeks spent in traditional learning mode by 1.14 percentage points, and the estimated average fraction of hybrid learning mode spent in in-person learning mode is 0.5 or 2.5 days out of a 5 day school week. Furthermore, we verify using a nonparametric binned scatter plot that over the range of school visit changes observed, the resulting relationship between total in-person learning and the change in school visits is indeed well represented by a linear function. Finally, the estimated intercept is 101.67, close to the predicted value of 100 when school is fully in-person (i.e., and ).

Table 1.

Regression of traditional learning against changes in school visits

| Dependent variable: Traditional (in-person) learning mode | ||||

|---|---|---|---|---|

| (1) | (2) | (3) | (4) | |

| Change in school visits | 1.14*** | 1.12*** | 1.13*** | 1.15*** |

| (0.04) | (0.04) | (0.04) | (0.05) | |

| Hybrid learning mode | − 0.50*** | − 0.49*** | − 0.48*** | − 0.43*** |

| (0.02) | (0.03) | (0.03) | (0.03) | |

| Intercept | 101.67*** | |||

| (2.51) | ||||

| Adjusted | 0.513 | 0.513 | 0.522 | 0.589 |

| N of counties | 3049 | 3049 | 2438 | 794 |

| N of students (in thousands) | 48,013 | 48,013 | 47,250 | 40,485 |

| % of all public-school students | 94.5 | 94.5 | 92.9 | 79.6 |

Safegraph and Burbio data are averaged at the county level for Fall 2020 (weeks of September 27–October 3 to December 13–December 19, excluding the week of Thanksgiving). All regressions are weighted by county-level student enrollment and standard errors (in parenthesis) are clustered at the state level. In columns (2)–(4) the intercept is constrained to 100

As robustness checks, in column (2) we restrict the intercept to 100 and rerun the regression, while in columns (3) and (4), we reduce the sample to the counties with at least 5 schools for which we have data, respectively, to the counties in the top-25 percent of the population distribution. The results are strikingly robust across the different specifications: a 1 percentage point decline in school visits reduces the fraction of weeks spent in effective in-person learning by 1.14 percentage points, and hybrid learning mode is estimated to correspond to a fraction of 0.43 to 0.49 of in-person learning mode.

In sum, the regressions confirm that there is a tight linear relationship between change in school visits and effective in-person learning. We therefore feel confident to use this mapping to infer effective schooling time at the individual school level.

Effective Schooling Time by School Characteristic

In the model simulations below, effective schooling time over the two-year period between Summer 2019 and Summer 2021 will be an important input to quantify the consequences of learning loss during the pandemic. We proceed as follows to infer this value from our estimates of in-person learning. According to the NCES table of “Number of instructional days and hours in the school year” (https://nces.ed.gov/programs/statereform/tab5_14.asp), there are 180 instructional days per year in almost every state. Dividing this number by 5 (since weekends are excluded from the counts), we obtain 36 weeks of potential schooling per year.9 Equivalently, we have 72 weeks of potential schooling for the two-year period between Summer 2019 and Summer 2021. For the 25 weeks between September 2019 and mid-March 2020 that precede the pandemic, we set effective school time to 100 percent. For the remaining 11 weeks of the 2019–2020 school year (week of Mar 15–Mar 21 through the week of May 24–May 30) and the 36 weeks of the 2020–2021 school year, hence for weeks, we calculate effective schooling time using the estimates in Table 1 as follows. For a set of schools with a certain characteristic s (e.g., public vs private schools), we take the average student-weighted change in school visits and calculate effective schooling time as , where , , and denotes the effectiveness of virtual learning. Thus, our estimate of effective schooling time – what we will call schooling input in the model-based analysis – during the two-year period from 2019 to 2021, as a percent of what schooling time would have been without the pandemic, is

| 3 |

The equation makes clear that schooling input depends importantly on the effectiveness of virtual schooling . While empirical evidence is accumulating that virtual instruction was a highly imperfect substitute for in-person instruction, pinning down how much less effective exactly virtual instruction was for the average student is a non-trivial task.

The most direct way to determine , and the one we follow for our benchmark result, is to use empirical studies that directly measure the loss in schooling inputs from test score declines. Dorn et al. (2021) find, based on data from Curriculum Associates, a standardized test provider, that by the end of the 2020–21 school year, public school students in grades 1–6 were on average 5 months behind in mathematics relative to their pre-pandemic peers. Under the assumption that lost effective schooling time translates one-to-one into learning loss, then based on (3), this implies a value for the effectiveness of virtual learning of , the benchmark value we use.

On the one hand, this value of may overstate the effectiveness of virtual learning both because of selection due to higher rates of absenteeism and declines in enrollment of lower-achieving students, and because many parents compensated for the loss of in-person schooling by taking over some of the instructional duties of teachers or paid tutors to do so (as they will in our model). On the other hand, students may also have been negatively affected by pandemic disruptions not directly related to schooling (e.g., health issues, job loss in the family), which would imply learning losses even if virtual schooling was highly effective.

Anticipating model simulation results below, we find that with a value of , we obtain an average learning loss of about 8.5% over the 2-year Covid period, while with a value of , we obtain a learning loss of about 12%. Both of these values are considerably smaller than the estimated average learning losses by Dorn et al. (2021), suggesting that disruptions not directly related to schools (and not taken into account by our model) indeed exerted a non-negligible negative impact. To make further progress, we contrast our simulation results with empirical studies such as Goldhaber et al. (2022) that seek to estimate pandemic learning loss directly as a function of instructional mode while controlling for regional differences in pandemic health and economic outcomes as well demographic and socio-economic characteristics of students. Their results imply that relative to students who attended school mostly in-person, learning loss was about twice as large for students who were primarily in virtual mode than for students who were primarily in hybrid mode.10 This suggests that the effectiveness of virtual learning was indeed low for the average student. We therefore consider a conservative assumption, and appears as a plausible alternative whose consequences we explore in Sect. 8.1.

Table 2 shows lost effective schooling time by school characteristics under the two different assumptions about the effectiveness of virtual learning. Across all schools in the sample, school visits declined by a student-weighted average of over the period from mid-March 2020 through the end of the 2020–21 school year. Using the average of the coefficient estimates in columns (2) and (4) of Table 1, this implies total in-person learning of about during that period and total virtual learning of about .

Table 2.

Estimates of effective schooling time over the 2019–2021 period

| All | Elementary | Secondary | |

|---|---|---|---|

| With virtual learning at 25% effectiveness | |||

| All | 69.4 | 71.7 | 64.2 |

| [68.7, 70.1] | [71.0, 72.3] | [63.4, 65.0] | |

| Private schools | 74.4 | 74.7 | 71.6 |

| [73.9, 75.0] | [74.1, 75.2] | [70.9, 72.2] | |

| Public schools, all | 68.9 | 71.5 | 63.8 |

| [68.2, 69.6] | [70.8, 72.1] | [63.0, 64.6] | |

| Public schools, top-25% income | 65.9 | 68.5 | 60.1 |

| [65.1, 66.6] | [67.8, 69.2] | [59.2, 61.0] | |

| Public schools, bottom-25% income | 72.9 | 74.9 | 68.6 |

| [72.3, 73.5] | [74.4, 75.5] | [67.9, 69.3] | |

| With virtual learning at 0% effectiveness | |||

| All | 59.2 | 62.2 | 52.3 |

| [58.3, 60.1] | [61.4, 63.1] | [51.2, 53.3] | |

| Private schools | 65.9 | 66.2 | 62.1 |

| [65.2, 66.7] | [65.5, 67.0] | [61.2, 62.9] | |

| Public schools, all | 58.5 | 62.0 | 51.7 |

| [57.6, 59.5] | [61.1, 62.8] | [50.6, 52.8] | |

| Public schools, top-25% income | 54.5 | 58.0 | 46.8 |

| [53.5, 55.5] | [57.1, 58.9] | [45.6, 48.0] | |

| Public schools, bottom-25% income | 63.9 | 66.6 | 58.2 |

| [63.1, 64.7] | [65.9, 67.3] | [57.2, 59.1] | |

The upper panel reports the share of effective schooling time for the 2019–2021 period as a percent of what schooling time would have been without the pandemic under the assumption that virtual learning was 25% as effective as in-person learning. The lower panel reports the share of effective schooling time under the assumption that virtual learning was not effective (i.e., the figures correspond to the share of potential schooling time over the 2019–2021 period that was effectively spent in the classroom). In each cell, the bracketed numbers correspond to lower and upper bounds based on the Burbio estimates reported in Table 1, and the point estimate is computed as the mid-point of the interval

For the baseline case of effectiveness of virtual learning, effective schooling time over the two-year period over the 2019–20 and 2020–21 school years therefore equals about

relative to a situation with full in-person learning. This value is shown in the top-left corner of the first panel of Table 2. If instead, virtual learning had effectiveness, the implied effective schooling time equals , as shown in the top-left corner of the second panel of Table 2.

The remainder of the table reports results of the same calculations separately for private versus public schools and for elementary versus secondary schools. Private schools experienced on average smaller declines in school visits during the pandemic than public schools. Similarly, elementary schools experienced smaller declines in school visits than secondary schools (either private or public, although for public schools the difference between elementary and secondary schools is larger). As a result, effective schooling time during the pandemic is estimated to have been highest for private elementary schools and lowest for secondary public schools.

The last two rows of each panel dig deeper into differences across public schools by looking separately at schools located either in a county ranked in the top or the bottom quartile of the national household income distribution. Perhaps surprisingly, public schools in affluent counties experienced on average a larger decline in school visits and therefore lower effective schooling time during the pandemic than public schools in less affluent counties. As shown in separate work by Kurmann and Lalé (2021), this difference is primarily due to the fact that the affluent counties are disproportionally located in states where schools did not return to full in-person instruction for a large part of the 2020–21 school year. Within quartiles of average household income, the difference in effective schooling time between elementary and secondary schools remains similar as reported in Table 2.

To sum up, the results in this section reveal large differences in total in-person schooling across different types of schools. Under what we argue are reasonable assumptions about the effectiveness of virtual schooling, this implies substantial variations in effective schooling time, i.e., schooling input. In the model simulations that follow, we will exploit these variations in schooling input to analyze the extent to which they result in heterogeneous earnings- and welfare losses for children in different school types, grades, and with different household income.

A Quantitative Life Cycle Model with Education Choices

We now describe the structural life cycle model that we will employ to measure the heterogeneous consequences for lifetime earnings, welfare, and taxes paid of the school closures we measured empirically in the previous section. We first describe the demographics, timing, stochastic structure, endowments, preferences and government policy and then formulate the individual decision problems recursively, since this is the representation we will compute. Since this model shares many features with the one used in Fuchs-Schündeln et al. (2022) we will focus on the novel features relative to their model when presenting the recursive representation of the model, relegating a complete account of all other dynamic programming problems of the model to Appendix A.

Individual State Variables, Risk, and Economic Decisions

We model individuals living in discrete time and denote the current period by t. Ours is a partial equilibrium model where individuals of two generations, a parent generation and a children generation, live through a full life cycle. When children live in the parental household, the key education investment decisions (whether to send the child to private or public school, and how much time and resources to invest into the child during her schooling years) are being taken by parents. The child generation makes one key decision upon becoming an independent household: equipped with inter-vivos transfers of the parent it decides what tertiary education, if any, to attain. After this decision this generation lives through a standard consumption-saving life cycle model; the same is true for the parental generation after the children have left the household. The timing and events in the model are summarized in Fig. 3. We now turn to a detailed description of the underlying heterogeneity of individuals and of each phase of the life cycle they undergo.

Fig. 3.

Life-cycle of child and parental households

Individuals are part of either the child or parental generation, . They differ in their marital status for single and married, their age , where a model period and age j spans two years in real time, their asset position a, their current human capital h, their education level for no higher education (no high school completion), high school attendance and completion, college attendance and completion, and idiosyncratic productivity risk modeled as a two state Markov process with state vector , where is low and is high labor productivity, and transition matrix and initial distribution as well as a transitory shock drawn from distribution . Parents decide in each period to send their children either to public or private school, . All individual state variables and the range of values they can take are summarized in Table 3.

Table 3.

State variables

| State Var. | Values | Interpretation |

|---|---|---|

| k | Generation | |

| m | Marital status | |

| j | Model age | |

| a | Assets | |

| s | School type | |

| h | Human capital | |

| e | Education | |

| Persistent productivity shock | ||

| Transitory productivity shock |

This table lists the state variables of the quantitative model

Demographics

Parents give birth to children when they are of age . The number of children a parental household has differs by marital status m and educational attainment of the parents e. There is no survival risk and all households live until age J. Therefore the cohort size within each generation remains constant over time. We now describe in detail how life unfolds first for parents and then for children, as summarized in Fig. 3.

Life of the Parental Generation

In the model, parental households start their economic life at age just before their children are born. Their initial characteristics include their exogenous marital status m, education level e, initial idiosyncratic productivity states and and initial assets a. These initial states are exogenously given to the household, and drawn from the population distribution which are derived directly from the data, as described in the calibration section.

Parents observe the innate ability (initial human capital) of their children at child model age (real biological age 4), which depends on parental education e and marital status m. Children live with their parents until child age (parental age ), at which point they leave the household to form their own independent household. During these years (parental ages ), parents invest resources and time into their children. For all ages of the child ( is real biological age 6), parents further decide in each period whether to send their children to a public or a private school, , trading off the cost of private school tuition with higher productivity in the human capital production function and thus higher human capital (and associated higher chance of attending college) as well as ultimately, higher expected earnings of their children. If parents opt for private school, then they pay private school tuition , which depends on a child’s age j because we distinguish between tuition for primary and secondary education.11 Attendance in public schools is free, . Kindergarten at child age and school type determines the schooling investment which together with the resource and time investments determines the evolution of a child’s human capital. As a result of these choices, the human capital of a child during school ages evolves according to

| 4 |

where g is a function of the child’s age j (to reflect age differences in the relative importance of education inputs) as well as a function of the school type s (to reflect potential productivity differences across the two school types), and depends positively on the three inputs (parental resources , parental time and schooling input ). To give the human capital accumulation technology a clearer interpretation, from the perspective of the model, h will be useful because it decreases the utility cost of succeeding in high school and college and it increases earnings conditional on a given tertiary education level. Thus, our notion of human capital should be interpreted as broad, including all cognitive and non-cognitive skills that contribute to tertiary schooling success and is rewarded through higher earnings in the labor market.

When children leave the household at parental age , their parents may give them inter-vivos transfers . This is the final interaction between parents and children, after which the two households separate. Parents also make the private school choice on behalf of their children with which the latter start their independent life. Thus, parental transfers to children for whom the parents choose private school have to be at least as high as the school fees, thus .

The remainder of parental life then unfolds as a standard life cycle model. Throughout their working ages, parental households spend an exogenous amount of time on market work which differs by marital status. Labor productivity and thus individual wages are determined by an exogenous productivity profile that depends on household age j, education e, marital status m, and is impacted by the persistent shock and the transitory shock . Labor income of parents of age j, education e and marital status m and hit by shocks is then given by

| 5 |

In addition to making human capital investment decisions for their children when these are present in the household, parents in each period make a standard consumption-saving choice, subject to a potentially binding borrowing constraint , which will be parameterized such that the model replicates well household debt at the age at which households have children . The borrowing limits decline linearly to zero over the life cycle toward the last period of work. Parents work until retirement at age , at which point they start to receive per-period retirement benefits until the end of life at age J. Table 4 summarizes the choices of parents described thus far, and those of children, to which we turn next.

Table 4.

Per period decision variables

| Dec. Var. | Values | Decision period | Interpretation |

|---|---|---|---|

| c | Consumption | ||

| Asset accumulation | |||

| s | School Type | ||

| Time investments | |||

| Monetary investments | |||

| b | Monetary inter-vivos transfer | ||

| e | (Higher) education |

This table lists the decision variables of the economic model

Life of the Children Generation

Children born at age are economically inactive for the first periods of their life. A child’s human capital during ages evolves as the outcome of parental investment decisions described above and schooling input . At the beginning of age and based on both the level of human capital as well as the financial transfer b from their parents (which determines their initial wealth a), children make a discrete higher education decision , where stands in for the choice not to complete high school, hs for high school completion, and co for college completion, respectively. For simplicity, children are stand-in bachelor households through their entire life-cycle.

Acquiring a high school or college degree comes at a utility cost (psychological cost) , which is decreasing in the child’s acquired human capital h and also depends on parental education as well as on whether the student attended private or public school, . In addition, college education requires a monetary cost . Children may finance some of their college expenses by borrowing, subject to a credit limit given by , which is zero for i.e.. for individuals not going to college. As was the case for parents, this limit decreases linearly with age and converges to zero at the age of retirement requiring the children generation to pay off their student loans prior to their retirement.

Youngsters who decide not to complete high school, , enter the labor market immediately at age . Those who decide to complete high school, but not to attend college, do so at age . While at high school, , they work part-time at wages of education group , and those children attending a private high-school also have to pay the school tuition . Those youngsters who decide to attend college enter the labor market at age and also work part-time at wages of education group during their high-school and college years

When the children generation enters the labor market (either without a high-school diploma, with a high-school degree or with a college degree), the acquired human capital during the school years is mapped into an idiosyncratic permanent labor productivity state , which is increasing in acquired human capital h and also positively depends on education e to reflect differential complementarities between education and human capital in generating earnings. When starting to work, children also draw the persistent productivity shock , which follows the same first-order Markov chain as for the parental generation, and stochastic transitory productivity . Labor income of children during the working period is then given by

We restrict attention to the two generations directly impacted by the Covid-19 school crisis, and thus assume that the child generation does not have offspring of their own. As a consequence the remaining decision problem of the child generation, after labor market entry, constitutes a completely standard life-cycle consumption-saving problem.

Recursive Formulation of the Decision Problems

Our model is a partial equilibrium model where the only interaction of the decision problems comes in the period in which the children generation leaves the household. Furthermore, children do not make economic decisions prior to that period. We can therefore solve the entire model backward, starting from the retirement phase of the children generation. The details of those recursive problems not spelled out explicitly in the main text are contained in Appendix A.

Children

The children generation undergoes three distinct phases, first making the education decision, and then living through a working phase and a retirement phase with which we begin.

The Retirement Phase During the retirement phase, at ages , the children generation solves a standard consumption-saving maximization problem, facing a typical budget constraint of the form:

where is pension income, whose dependence on (the persistent income state in the period prior to retirement), education e and human capital h captures the progressive nature of the social security system in past earnings, which are in turn determined by . The function represents a progressive labor income tax code, and capital and consumption are taxed at proportional rates . The associated value function at the time of retirement is given by with .

Working Life Let denote the value function of a children household (assumed to be single) aged j that has entered the labor market with education level e, human capital h and has received stochastic income shocks . This value function is the result of a standard consumption-saving maximization problem, as for retired households, but with budget constraint now given by

Here is taxable labor income, with being the social security payroll tax. The argument of the tax function T encodes that employer contributions to social security are not taxable income. In addition to the budget constraint, the household faces an age-, education, and generation-specific borrowing limit .

The Higher Education Choice The key choice of the children generation impacted by the Covid-19 crisis and associated loss in schooling is the higher education decision this generation will make in the model right after the establishment of an independent household, and after having received inter-vivos transfers from their parents. 16-year-olds have three discrete choices : they can either decide to drop out of high school and enter the labor market directly at age 16, or complete high school prior to labor market entry at age 18, or third, go to and complete college at age 22 prior to labor market entry. To spell out this higher education decision problem, we first have to specify the values from each of these three discrete options.

Dropping Out of High School Members of the children generation that made the decision to drop out of high school at model age (real age 16), i.e., chose , directly enter the labor market with permanent deterministic productivity , then draw the persistent income shock (which then evolves according to the Markov transition matrix ) and the transitory income shock . The expected value of entering the labor market as a high-school drop-out is then given by12

where is the lifetime utility of a worker of age j with assets and human capital (a, h) that has drawn productivity shocks , as defined in the previous paragraph.

Completing High School Youngsters that at age decide to complete high school but not attend college (i.e., choose ) work part-time during high school at a deterministic wage and then enter the labor market two years later at , when they draw stochastic labor productivity , . In contrast to the group, for children choosing their school type s is a relevant state variable because children in private high school have to pay the private school tuition . Parental education is a state variable since the utility cost of completing high school depends on the education of their parents. This dependence captures heterogeneity in peer groups and social networks across socio-economic groups that affect the difficulty of completing high school.

Expected lifetime utility from high school completion is then given by

| 6 |

subject to

| 7a |

| 7b |

| 7c |

That is, high-school students work for high-school drop-out wages for a fraction of their time and obtain period utility from consumption u(c) and disutility from (exogenous) labor supply . The utility cost associated with attending high school is decreasing in the human capital h previously acquired by the student. Children form expectations over their stochastic labor market productivity when they enter the labor market upon graduating at age . Their remaining life (labor market and retirement) then unfold as described above.

Obtaining a College Degree Children who decide, at age to attend, and by assumption, to complete, college (i.e., choose ), during high school age solve the same problem as those who chose a high school education (), with the difference that the continuation value differs at age (the youngster goes to college rather than entering the labor market). Thus the value of choosing, at age , the college option, is given by

| 8 |

where is expected lifetime utility at age (age 18 in real time) from entering college. The budget set is identical to that in Eq. (7). Note that this value function still depends on parental education because the utility cost from attending college will be, but no longer on high school type s.

Finally, during the two college periods students pay college tuition and work part-time at high-school wages. Furthermore, they can borrow up to a limit to pay for tuition. Thus, their budget set is described by

| 9a |

| 9b |

| 9c |

The Bellman equation differs between age and since at the first age students have two years (one model period) left in college, whereas at age their continuation value is determined by labor market entry as college graduate. The corresponding Bellman equations are

and

which are both maximized subject to Eq. (9). Here, as before, is expected utility lifetime from entering the labor market as a college graduate at age (age 22 in real time) with (human) capital and having drawn initial shocks .

The Education Decision Having spelled out above the values for the three education choices , the choice is simply to choose the alternative that gives the highest expected lifetime utility, and the pre-education decision value function of children aged (which will enter parental lifetime utility through one-sided altruism) is given by:

| 10 |

In the computational implementation, we additionally apply Extreme Value Type I (Gumbel) distributed taste shocks to smooth this discrete decision problem.13 Accordingly, youngsters choose the three education alternatives with state -specific probabilities , for .

Parents

Given the focus of the paper, we model parental households as becoming economically active at the beginning of age when they give birth to children. Since human capital formation of parents is completed at this stage, we normalize parental human capital to and let it be constant over the remainder of parental life. Children live with adult households until they form their own households and make decisions as described above. Household separation occurs at parental age , after which the parental generation lives through a standard life cycle model whose recursive formulation is described in Appendix A.2. Let denote the expected lifetime utility from this life cycle of a parent household at the beginning of age with education and marital status (e, m), stochastic productivity shocks and assets . Working backward in age, we now discuss the inter-vivos transfer decision when children leave the household and the child human capital investment decisions. It is convenient14 to express the recursive problems in those stages conditional on the private/public school choice and we formally describe this choice at the end of this section.

Inter-vivos Transfers At parental age children leave the household, and at this age parents can make inter-vivos transfers b. These transfers immediately (that is, within the period) become assets of their children. The dynamic program of parents at this age conditional on then is

| 11 |

subject to

Here is the pre-education decision value function of their children defined in Eq. (10), and the parameter measures the intensity of altruism of parents toward their children.1516 Note that private school fees are not present in the parental budget constraint because these fees are paid by the children if they decide to continue with high school. However, since parents make the private/public school choice for the current period on behalf of their children, transfers b have to exceed the respective fees. Since also for children whom their parents send to a public school transfers have to be (weakly) positive, we condense the constraints on transfers as , for .17

Investment Decision The value function of children in the previous dynamic program that parents solve at age includes their human capital h since it determines both the higher education decision as well as future earnings of this generation directly. We now turn to the accumulation of this human capital when the children are of school age and reside with their parents (at parental ages ). During these ages parents invest resources and time investments into each of their children and pay private, child-age dependent per-child school tuition in case they decide to send their children to a private school. Parents derive utility from per capita consumption of its household members and suffer disutility from hours worked in the market and at home taking care of their children (rather than enjoying leisure). The dynamic program during this stage of the parental life cycle conditional on can then be written as

subject to

The parameter is a weight on time spent with children, and reflects the possibility that reading to children carries a different disutility (or even positive utility) of time than work. Note that the sum of hours worked and time investment in children in the function is divided by the number of working household members.

Private Schooling Decision At each age 18 parents decide on whether to send their children to a public or a private school. The optimal choice of parents is given by19

| 12 |

Government

The government runs a pension system with a balanced budget. It also finances exogenous government spending, expressed as a share of aggregate output G/Y, and aggregate education spending on public schools (for pre-tertiary and tertiary education) through consumption taxes, capital income taxes and the progressive labor income tax system T(y). In the initial pre-Covid-19 scenario, the government budget clears by adjustment of the average labor income tax rate encoded in T(.). In the thought experiment with school closures we hold fiscal policy constant, therefore implicitly assuming that the budget deficits or surpluses generated by a change in private behavior are absorbed by government debt which is serviced or repaid by future generations not explicitly modeled.

The Covid-19 Thought Experiment

We compute an initial stationary partial equilibrium with exogenous wages and returns prior to model period . In period , the COVID-19 shock unexpectedly hits, and from that point on unfolds deterministically. That is, factor prices and fiscal policies are fixed by our partial equilibrium assumption, and households, after the initial surprise, have perfect foresight with respect to aggregate economic conditions. The COVID-19 crisis impacts the economy through an education crisis: the government temporarily closes schools, represented in the model by a temporary reduction in school investment into child human capital production. The reduction of differs by type of school s and age of the child j. Regarding the private/public school choice in the period of the shock we assume the following timing protocol. In the beginning of the period, parents observe their own current period state variables as well as the human capital of their children h. They then decide on whether to send their children to a private or public school, . Next, the corona shock hits and only after the realization of the shock, parents decide on their consumption and savings and the monetary and time investments into their children . That way, the private/public schooling decision in the period of the corona shock does not change when the corona shock hits. We then trace out the impact of these temporary shocks on parental human capital inputs (both time and money) and intergenerational transfer decisions, as well as on the education choices, future earnings in the labor market, and ultimately, the distribution of welfare of the children generation, focusing specifically on the impact of the heterogeneity in the length of school closures by school type and the age of children. Since children in the model differ by age and the type of school they attend at the time of the shock (as well as in terms of parental characteristics), so will the long-run impact on educational attainment, future wages, and welfare.

Calibration

A subset of parameters is calibrated exogenously not using the model. These first-stage parameters are summarized in Table 18. The second-stage parameters are those that are calibrated endogenously by matching moments in the data and are summarized in Appendix C, Table 19. We next describe our choice and sources of first-stage parameters and the moments we match to calibrate the second-stage parameters. We focus the description on elements relevant to the characteristics of parents, human capital accumulation and the school closures experiment and relegate other aspects of the calibration, including a description of the data sets we use, to Appendix C.

Table 18.

First-stage calibration parameters

| Parameter | Interpretation | Value | Source (data/lit) |

|---|---|---|---|

| Population | |||

| Age at economic birth (age 4) | 0 | ||

| Age at beginning of econ life (age 16) | 6 | ||

| Age at finishing HS (age 18) | 7 | ||

| Age at finishing CL (age 22) | 9 | ||

| Fertility Age (age 32) | 14 | ||

| Retirement Age (age 66) | 31 | ||

| J | Max. Lifetime (age 80) | 38 | |

| Fertility rates | See main text | PSID 2011–2017 | |

| Distribution of parents by martial status and education, age | See main text | PSID 2011–2017 | |

| Preferences | |||

| Relative risk aversion parameter | 1 | ||

| Curvature of labor disutility | 0.5 | ||

| Labor Productivity | |||

| Age Profile | See main text | PSID 1968–2012 | |

| Realizations of Transitory Shock | [0.881, 1.119] | PSID 1968–2012 | |

| States of Markov process | [0.8226, 1.1774] | PSID 1968–2012 | |

| Transition probability of Markov process | 0.0431 | PSID 1968–2012 | |

| Hours worked for students, as a fraction of full time (HS and CL) | See main text | ||

| Ability gradient of earnings | See main text | NLSY79 | |

| Endowments | |||

| r | (Annual) interest rate | 4.0% | Siegel (2002) |

| l(m) | Average hours worked by marital status (annual) | PSID 2011–2017 | |

| Asset distr-n of parents by martial status and education, age | See main text | PSID 2011–2017 | |

| Borrowing limit for parents at age | See main text | PSID 2011–2017 | |

| Education-specific repayment amount for parents: singles | See Sect. 5.2.4 | ||

| Education-specific repayment amount for parents: couples | See Sect. 5.2.4 | ||

| Ability/Human Capital and Education | |||

| Private school tuition (primary) | $3294 | PSID CDS I-III | |

| Private school tuition (secondary) | $6588 | PSID CDS I-III | |

| College tuition costs (annual, net of grants and subsidies) | $14756 | Krueger and Ludwig (2016) | |

| College borrowing limit | $45000 | Krueger and Ludwig (2016) | |

| rp(ch) | Repayment amount for children who choose college | 0.049 | see section 5.5 |

| Elast of subst b/w human capital and CES inv. aggr. | 1 | Cunha et al. (2010) | |

| Elast of subst b/w public inv. and CES aggr. of private inv. | 2.43 | Kotera and Seshadri (2017) | |

| Elast of subst b/w monetary and time inv. | 1 | Lee and Seshadri (2019) | |

| CES share parameter of monetary and time inv. (age bin 6–8) | 0.5 | Normalization | |

| Share of government input for ages 6 and older | 0.676 | Kotera and Seshadri (2017) | |

| Innate ability dist-n of children by parental char-s | See main text | PSID CDS I | |

| Normalization parameter of initial dist-n of initial ability | 0.1248 | PSID CDS I-III | |

| Government policy | |||

| Public pre-college education spending by age | UNESCO (1999–2005) | ||

| Consumption Tax Rate | 5.0% | Legislation | |

| Capital Income Tax Rate | 20% | Legislation | |

| Soc Sec Payroll Tax | 12.4% | Legislation | |

| G/Y | Government consumption to GDP | 13.8% | Current value |

First-stage parameters calibrated exogenously by reference to other studies and data

Table 19.

Second-stage calibration parameters

| Parameter | Interpretation | Value |

|---|---|---|

| Preferences | ||

| Time discount rate (target: asset to income ratio, age 25–60) | 0.9773 | |

| Altruism parameter (target: average IVT transfer per child) | 0.7755 | |

| Labor Productivity | ||

| Normalization parameter (target: ) | ||

| Human Capital and Education | ||

| Utility weight on time inv. (target: average time inv.) | 1.1024 | |

| Slope parameter of (target: average monetary inv.) | ||

| Age-dependency of (target: slope of time inv.) | ||

| Age-dependency of (target: slope of money inv.) | 0.1493 | |

| Share of government input for age bin 4-6 (target: average time inv. age bin 4-6) | 0.5554 | |

| Productivity parameter for (target: fraction of group ) | 1.8103 | |

| Investment scale parameter (target: average HK at age ) | 1.1894 | |

| Investment scale parameter for (target: average HK at age ) | 1.0657 | |

| utility costs (target: fraction of group ) | − 2.2373 | |

| utility costs (target: fraction of group ) | − 0.9882 | |

| utility costs (target: conditional fraction of group ) | − 1.0493 | |

| Government policy | ||

| Level parameter of HSV tax function (balance gvt budget) | 0.8877 | |

| Pension replacement rate (balance socsec budget) | 0.1893 | |

Second-stage parameters calibrated endogenously by targeting selected data moments

Preferences

The per period sub-utility function u(x) is of the standard iso-elastic power form

We set (logarithmic utility), and consequently child and adult equivalence scale parameters are irrelevant for the problem. In the parental household’s problem, the per period sub-utility function v(x) is

so that if , parameter can be interpreted as a Frisch elasticity of labor supply. In our model of exogenous labor supply this interpretation of course seizes to be relevant, but it provides us with a direct way of calibrating the power term of the utility function. We set based on standard estimates of the Frisch elasticity.20

When children live in the parental household, we have . are hours worked by marital status, which we calculate from the data, giving annual hours of and . The time cost parameter is calibrated to match average time investments by parents into the education of children, giving (with further details described below as part of the calibration of the human capital technology).

When children attend high school or college, they experience utility costs for according to the cost function

Utility costs of obtaining a high-school degree are equal to and are thus monotonically decreasing and convex in the acquired human capital h. Utility costs for obtaining a college degree depend on parental education and are equal to, .

The parameters of the cost function are calibrated to match education shares in the data for the three groups . We measure these shares for adults older than age 22 – which is the labor market entry age of all education groups in the model – and younger than age 38 based on the PSID waves 2011, 2013, 2015 and 2017.21 Parameter is calibrated to match the fraction of children without a high school degree of 12.16%, giving . With regard to the additional utility costs during the college period we restrict and calibrate it to match the fraction of children with a college degree of 33.21% giving . The parameter is calibrated to match the fraction of children in college conditional on parents having a college degree of 63.3% as in Krueger and Ludwig (2016), giving .

Households discount utility at rate . We follow Busch et al. (2020) and calibrate it to match the assets to income ratio in the PSID for ages 25 to 60 giving an annual discount factor of . Utility of future generations is additionally discounted at rate . Parameter is chosen so that average per child inter-vivos transfer is ca. 61,200$, as implied by the Rosters and Transfers supplement to the PSID (based on monetary transfers from parents to children until age 26, see Daruich (2022)). This gives .

Initial Distribution of Parents

For the initial distributions of parents at the fertility age, we restrict the sample to parents aged 25–35, leaving us with 3024 observations.22

Marital Status

Marital status is measured by the legal status of parents. This gives a share of singles of and a share of married households of .

Education Categories

We group the data by years of education of household heads older than age 22. Less than high school, , is for less than 12 years of formal education. High school completion (but no college) is for more than 12 but less than 16 years of education. College is at least 16 years of education. The population shares of parents in the three education categories by their marital status are summarized in the top panel of Table 5.23

Table 5.

Fraction of households, number of children and lower asset limits by education and marital status

| Education e | Marital status m | si | ma |

|---|---|---|

| Fraction of households | ||

| no | 0.2194 | 0.1621 |

| hs | 0.6064 | 0.5577 |

| co | 0.1742 | 0.2802 |

| Number of children | ||

| no | 2.36 | 2.33 |

| hs | 1.86 | 2.15 |

| co | 1.77 | 1.96 |

| Lower asset limit | ||

| no | − 2380 | − 18,931 |

| hs | − 33,065 | − 51,332 |

| co | − 60,037 | − 43,629 |

Top panel: Fraction with education by marital status. Middle panel: Number of children by marital status and education. Bottom panel: lower asset limit for parents at model age , expressed in 2010 dollars by marital status and education

Number of Children

The number of children by marital status and education of parents is computed as the average number of children living in households with household heads aged 25-35. It is summarized in the middle panel of Table 5.

Assets

Conditional on the initial distribution of parents by marital status and education, we measure the distribution of assets according to asset quintiles, which gives the initial distribution . We set the borrowing constraint of parents as follows. First, we calculate average assets (debt) of the lowest asset quintile at age from the data and set it equal to the initial debt of parents in the lowest asset quintile in the model. The result is summarized in the bottom panel of Table 5.

For all ages we then compute the borrowing limit recursively as:

| 13 |

where rp(e, m, pa) is chosen such that the terminal condition is met.

Income

We draw initial income shocks assuming independence of the asset position according to the stationary invariant distribution of the 2-state Markov process, thus .

Productivity

We use PSID data to regress by education of the household head log wages measured at the household level on a cubic in age of the household head, time dummies, family size, a dummy for marital status, and person fixed effects. Predicting the age polynomial (and shifting it by marital status) gives our estimates of . We next compute log residuals and estimate moments of the earnings process by GMM and pool those across education categories and marital status.24 We assume a standard process of the log residuals according to a permanent and transitory shock specification, i.e., we decompose log residual wages as

where , for density functions , and estimate this process pooled across education and marital status. To approximate the persistent component in our model, we translate it into a 2-state Markov process targeting the conditional variance of , conditional on , (accounting for the two year frequency of the model). The transitory component is in turn approximated in the model by two realizations with equal probability with the spread chosen to match the respective variance . The estimates and the moments of the approximation are reported in Table 6.

Table 6.

Stochastic wage process

| Parameter | Estimates | Markov Chain | Transitory Shock | |||

|---|---|---|---|---|---|---|

| Estimate | 0.9559 | 0.0168 | 0.0566 | 0.9569 | [0.8226, 1.1774] | [0.881, 1.119] |

This table contains the estimated parameters of the residual log wage process

We set the fraction of time working during high school to , which can be interpreted as a maximum time of work of one day of a regular work week. In college, students may work for longer hours and we accordingly set .

The mapping of acquired human capital into earnings according to is based on Abbott et al. (2019). We use their data – the NLSY79, which includes both wages and test scores z of the Armed Forces Qualification Test (AFQT) – to measure residual wages of education group e (after controlling for an education specific age polynomial) and run the regression

where is an education group specific error term and are average test scores. We denote the education group specific coefficient estimate by , see Table 7. The estimated ability gradient is increasing in education reflecting complementarity between ability and education. In the model, we correspondingly let

where is average acquired human capital at (biological age 16) and is an education group e specific normalization parameter, chosen such that for all e. The normalization—which gives , for , respectively—implies that the average education premia are all reflected in , which in turn are directly estimated on PSID data.

Table 7.

Ability gradient by education level

| Education level | Ability gradient |

|---|---|

| HS − | 0.351 (0.0407) |

| (HS & CL −) | 0.564 (0.0233) |

| (CL & CL +) | 0.793 (0.0731) |

This table contains the estimated ability gradient , using NLSY79 as provided in replication files for Abbott et al. (2019). Standard errors are in parentheses

Human Capital Production Function

At birth at age , the innate ability (initial human capital) of children is determined, conditional on the distribution of parents by parental characteristics , by the function . We calibrate the distribution from the Letter Word test score distribution in the PSID Child Development Supplement (CDS) surveys I–III, and match it to parental characteristics by merging the survey waves with the PSID. Table 8 reports the joint distribution of average test scores of the children by parental education and marital status. We use this test score distribution as a proxy for the initial human capital distribution of children conditional on parental education and marital status.25 We base the calibration of the initial ability distribution of children on this data by drawing six different types of children depending on the combination of marital status (2) and parental education (3). Children’s initial human capital is normalized as the test score of that -group relative to the average test score. We further scale the resulting number by the calibration parameter and, thus, initial human capital of the children is a multiple of . Parameter is calibrated exogenously to match the ratio of mean test scores at ages 3–5 to mean test scores at ages 16–17, which gives . Initial abilities relative to average abilities and the corresponding multiples of for the six types are contained in Table 8.

Table 8.

Initial ability by parental education

| Marital status and educ of HH head | Avg. Score | Fraction of |

|---|---|---|

| Single low | 35 | 0.843 |

| Single medium | 38 | 0.906 |

| Single high | 46 | 1.107 |

| Married low | 39 | 0.945 |

| Married medium | 41 | 0.984 |

| Married high | 45 | 1.085 |

This table contains the estimated initial ability of children as measured by the letter word test in the Child Development Supplement Surveys 1–3 (years 1997, 2002, 2007) of the PSID

At ages children receive parents’ education investments through money and time and school input . Education investments of the respective education institution are certain, known by parents, and equal across children. In the baseline pre-Covid-19 scenario we normalize the education input in both institutions to 1 unit of time, thus for both s and all j. In private school one unit of time leads to a higher productivity than in public schools which is reflected in a productivity parameter . Specifically, we normalize , for and calibrate , for endogenously to match the average fraction of parents with children in private schools of observed in the data. This gives for . Given these inputs, human capital is acquired in a multi-layer human capital production function

| 14a |

| 14b |

| 14c |

which partially features age dependent parameters for calibration purposes. We divide the endogenous age dependent per child monetary and time investments by the parents , as well as the CES aggregate of these (normalized) investments, , by their respective unconditional means through which we achieve unit independence.

The outermost nest (first nest) augments human capital and total investments according to a CES aggregate with age-specific parameter and age-independent substitution elasticity . We set ,26 and calibrate to match (per child) time investments by age of the child. We model age dependency as

| 15 |

and determine by an indirect inference approach such that the age pattern of log per child time investments in the data equals the pattern in the model for biological ages 6 to 14 of the child. Recall that we in turn match the average level of time investments at biological ages 6 to 14 by calibrating the utility cost parameter . Time investments at biological age 4 are matched differently, with details described below. The intercept term is calibrated to match average monetary investments. Consistent with Cunha et al. (2010), we find that the weight on acquired human capital at age j is increasing in j, so that investments become less important in the course of the life-cycle. While our model is not directly comparable to their empirical analysis,27 also the magnitude of is similar.

In the second nest, we restrict for and calibrate it exogenously according to the estimates for the US by Kotera and Seshadri (2017) – who estimate the parameters of a CES nesting of private and public education investments similar to ours – giving .

At biological age 4 of the child, children are still in kindergarten. To take into account this structural break in the process of education according to the institutional setting, we separately calibrate to match the average time investments by parents into their children at biological age 4 of the child. This gives .