Abstract

Commercial health plans pay higher prices than public payers for hospital care, which accounts for more than 5 percent of US gross domestic product. Crafting effective policy responses requires monitoring trends and identifying sources of variation. Relying on data from the Healthcare Provider Cost Reporting Information System, we describe how commercial hospital payment rates changed relative to Medicare rates during 2012–19 and how trends differed by hospital referral region (HRR). We found that average commercial-to-Medicare price ratios were relatively stable, but trends varied substantially across HRRs. Among HRRs with high price ratios in 2012, ratios increased by 38 percentage points in regions in the top quartile of growth and decreased by 38 percentage points in regions in the bottom quartile. Our findings suggest that restraining the growth rate of HRR commercial hospital price ratios to the national average during our sample period would have reduced aggregate spending by $39 billion in 2019.

In 2019 US spending on hospital care totaled $1.2 trillion, accounting for 32 percent of all health care expenditures and more than 5 percent of gross domestic product.1 One factor underlying the high cost of hospital care is the prices paid by commercial health plans, which have increased substantially over time and are now much higher than the prices paid by public payers.2–13 Policy makers seeking to increase the affordability of health care have considered options to reduce commercial hospital prices, such as by regulating prices directly or increasing the competitiveness of hospital markets.14 To craft effective policies and to understand their distributional consequences, policy makers will need to closely monitor trends and identify sources of variation in hospital prices.

In this study we evaluated the extent to which trends in commercial hospital prices have differed across the United States, building on previous studies that have documented substantial regional variation in commercial plans’ hospital prices in a given year.6–9

Study Data And Methods

DATA

We obtained estimates of commercial-to-Medicare payment rate ratios for 2012–19 using RAND Hospital Data, which is a cleaned and processed version of annual cost report data submitted by hospitals to the Healthcare Cost Report Information System (HCRIS). Every Medicare-certified hospital must submit a cost report, meaning that these data encompass all US hospitals except federal hospitals and some children’s hospitals.15 HCRIS data are useful for evaluating trends in commercial hospital prices because they include most US hospitals, capture all commercial payers at those hospitals, are timely, and are available for multiple years.

We applied a handful of data cleaning steps and sample restrictions to the data. First, we dropped the top and bottom 0.5 percent of hospital-year observations—that is, hospitals with commercial-to-Medicare price ratios below 28 percent and above 448 percent—to exclude a small number of unreasonably small and large values. Second, we interpolated missing data between years. Third, we dropped hospitals that were still missing one or more years of data after interpolation. Fourth, we dropped hospitals that had low levels of either commercial or Medicare volume—that is, fewer than 100 discharge equivalents in any year. Discharge equivalents are a measure of total inpatient and outpatient volume and are calculated by multiplying the number of inpatient discharges by the ratio of total inpatient and outpatient revenues to inpatient revenues. Fifth, we retained short-term general hospitals. Finally, we excluded a small number of hospitals that could not be matched to an HRR (for example, hospitals in the US territories). Our final sample contained 3,612 hospitals and 306 HRRs from the period 2012–19.

Estimates of commercial-to-Medicare price ratios are based on hospital revenue and charge data. In particular, the managers of the RAND Hospital Data file generate estimates of commercial-to-Medicare price ratios in three steps.16 First, they estimate commercial charges and revenues by subtracting Medicare, Medicaid, Children’s Health Insurance Program, state and local indigent care, charity care, and government grant amounts from total charges and revenues. These estimates therefore exclude Medicare Advantage and Medicaid managed care plans. Second, they calculate revenue-to-charge ratios for commercial payers and Medicare. Finally, they divide the former by the latter to estimate commercial-to-Medicare price ratios. This approach is similar to the methodology used in a study published in Health Affairs by Ge Bai and Gerard Anderson, which relied on financial data from hospitals in Florida to estimate price ratios based on revenue-to-charge ratios.11 Another prior Health Affairs article, by Thomas Selden and colleagues, provided suggestive evidence that hospital cost-to-charge ratios are similar for commercial and Medicare patients.2 If that is the case, then the RAND Hospital Data estimates of commercial-to-Medicare price ratios are approximately equal to the ratio of revenue-to-cost ratios.

We obtained HRR- and national-level data for each year by taking the average of hospital-level price ratios weighted by the number of commercial discharge equivalents.

ANALYSIS

Our analyses examined trends in commercial-to-Medicare price ratios both overall and by HRR-level initial price ratio quartile and percentage-point-change quartile from 2012 to 2019 within a given initial price ratio quartile (that is, sixteen groups altogether). Our rationale for stratifying results based on initial price ratio quartiles was to determine whether or not any differences reflected regression to the mean. Quartiles were calculated after weighting price ratios by the number of 2012 commercial discharge equivalents. In supplementary analyses, we held hospital-level commercial discharge equivalents constant at 2012 levels and allowed price ratios to vary as observed—that is, ignoring changes in price ratios associated with shifts in where patients sought care—and vice versa before evaluating HRR- and national-level trends. The online appendix includes an analysis of hospital-level price ratio trends.17

LIMITATIONS

A limitation of our study is that although HCRIS data offer a timely and relatively comprehensive picture of price ratio trends, they provide less granular information than some of the other sources that have been used to estimate commercial prices and price ratios. For example, HCRIS data do not allow researchers to identify procedure-specific price ratios or price ratio differences across insurers. In addition, in contrast to analyses that rely on claims and survey data, we were unable to adjust for potential differences in service mix across commercial and Medicare populations that may affect price markups. HCRIS estimates of commercial-to-Medicare price ratios in a given year have a strong correlation with estimates of price ratios based on claims data from the RAND Hospital Price Transparency Project (see appendix exhibits 2 and 3, which graph the relationship between the two measures at both the hospital level and the HRR level).17 This does not rule out the possibility that our results may be biased—for example, to the extent that differences in service mix between commercial and Medicare populations changed over time within a given HRR, which could affect relative revenue-to-charge ratios.

Study Results

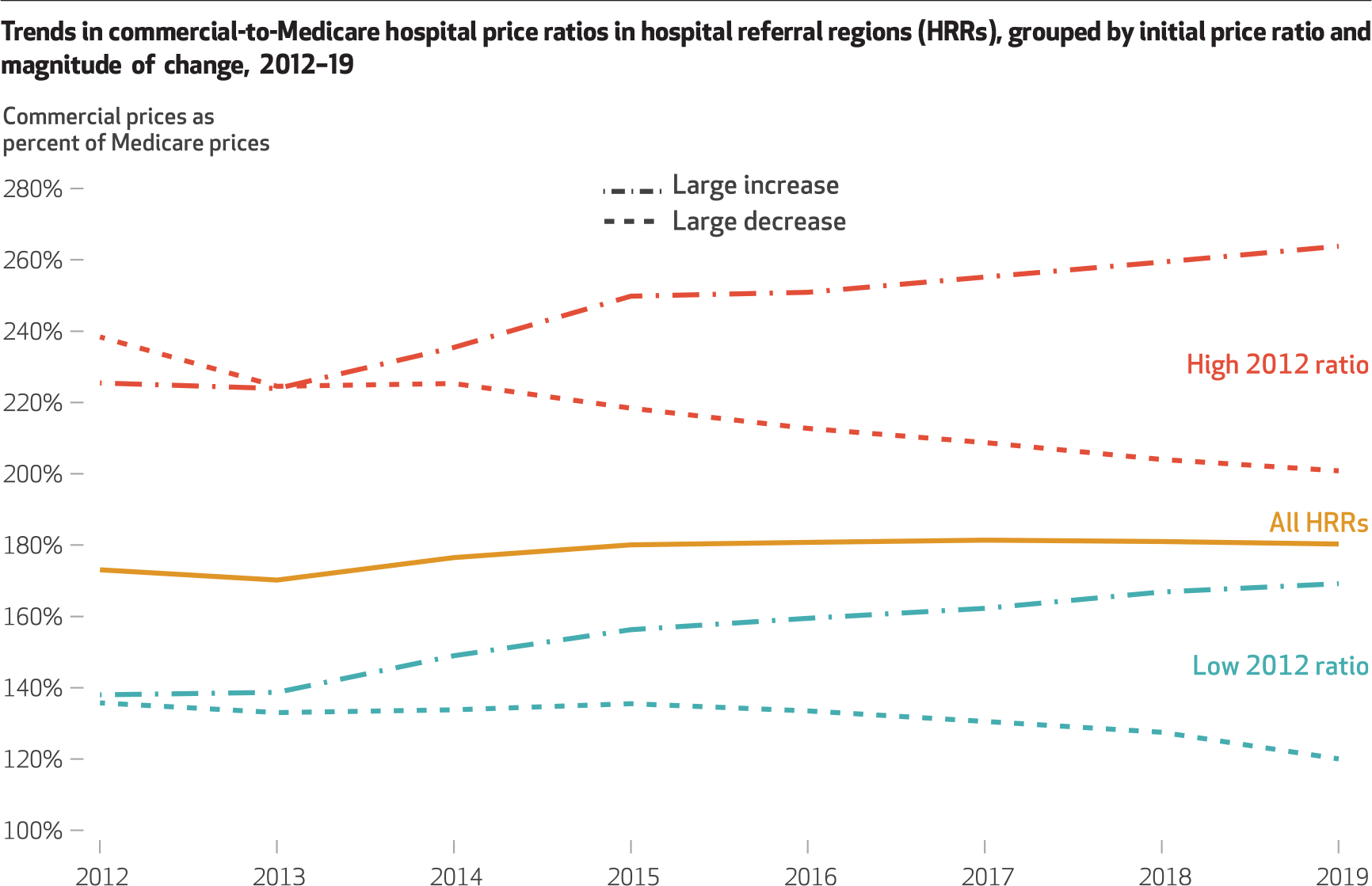

Between 2012 and 2019 average commercial-to-Medicare price ratios were relatively stable, but trends varied substantially across HRRs in high- and low-ratio regions alike (exhibit 1). On average, price ratios increased by 7 percentage points between 2012 and 2019. Among HRRs that had high price ratios in 2012 (the top quartile), there was a large divergence in growth over time: Commercial-to-Medicare price ratios increased by 38 percentage points, on average, in regions with large increases (the top quartile of change) while decreasing by 38 percentage points, on average, in regions with large decreases (the bottom quartile). There was also a large divergence in trends among HRRs that had low initial price ratios (the bottom quartile); the price ratio increased by 31 percentage points in regions with large increases while decreasing by 16 percentage points in regions with large decreases. Thus, many HRRs with either low or high commercial-to-Medicare price ratios in 2012 converged substantially to the national average, whereas many other HRRs drifted to further extremes. Although there was a large amount of variation in trends irrespective of initial price ratio levels, the greatest amount of variation occurred in regions with high initial price ratios (see appendix exhibit 4, which depicts the distribution of changes by initial price ratio quartile).17

Exhibit 1. Trends in commercial-to-Medicare hospital price ratios in hospital referral regions (HRRs), grouped by initial price ratio and magnitude of change, 2012–19.

SOURCE Authors’ analysis of 2012–19 Healthcare Cost Report Information System (HCRIS) data. NOTES Price ratio estimates reflect estimated commercial revenue-to-charge ratios divided by Medicare revenue-to-charge ratios. “High 2012 ratio” and “Low 2012 ratio” refer to HRRs with the highest 25 percent (top quartile) and lowest 25 percent (bottom quartile) of commercial-to-Medicare price ratios in the initial year of the study period. “Large increase” and “Large decrease” refer to HRRs that, within their initial price ratio group, are in the top and bottom quartiles of price ratio change, as measured during the 2012–19 study period. Price ratios are weighted by the number of commercial discharge equivalents.

We found that these trends in price ratios were driven primarily by hospitals changing their commercial prices relative to Medicare rates rather than by patients switching to facilities with higher or lower price ratios. Appendix exhibit 5 depicts price ratio trends after hospital volume is held constant at 2012 levels while price ratios are allowed to vary as observed; it yields results similar to those of our main analyses.17 In contrast, appendix exhibit 6 depicts trends after price ratios are held constant and hospital volume is allowed to vary; it yields muted results.17

Exhibits 2 and 3 list the HRRs that had large increases and decreases in price ratios, respectively, among regions with high ratios in 2012. Of the nineteen HRRs with large increases, eleven were in California, including eight in Northern California, and three were in Wisconsin. The nineteen HRRs with large decreases were more geographically diverse, although four were in Indiana.

EXHIBIT 2.

Trends in commercial-to-Medicare hospital price ratios among 19 hospital referral regions (HRRs) with high ratios in 2012 and large ratio increases in 2012–19

| HRR name | 2012 | 2019 | Changea |

|---|---|---|---|

| Tacoma, WA | 222% | 337% | 115 |

| Chico, CA | 237 | 338 | 101 |

| San Mateo County, CA | 246 | 329 | 83 |

| Santa Barbara, CA | 282 | 362 | 80 |

| Salinas, CA | 221 | 290 | 69 |

| Bend, OR | 222 | 288 | 66 |

| Napa, CA | 222 | 276 | 54 |

| Alameda County, CA | 251 | 294 | 43 |

| Sacramento, CA | 215 | 257 | 42 |

| San Francisco, CA | 209 | 248 | 39 |

| San Jose, CA | 227 | 264 | 38 |

| Green Bay, WI | 239 | 277 | 37 |

| Santa Rosa, CA | 224 | 260 | 36 |

| San Luis Obispo, CA | 200 | 234 | 34 |

| Greeley, CO | 266 | 294 | 28 |

| Billings, MT | 203 | 224 | 21 |

| Marshfield, WI | 215 | 236 | 21 |

| Roanoke, VA | 210 | 230 | 20 |

| Madison, WI | 211 | 230 | 19 |

SOURCE Authors’ analysis of 2012–19 Healthcare Cost Report Information System (HCRIS) data. NOTES Price ratio estimates reflect estimated commercial revenue-to-charge ratios divided by Medicare revenue-to-charge ratios. The commercial-to-Medicare hospital price ratios for these nineteen HRRs fall into the top quartile of ratios in 2012 and, among hospitals in the top quartile of ratios in 2012, the top quartile of ratio increases during the 2012–19 study period.

Percentage points.

EXHIBIT 3.

Trends in commercial-to-Medicare hospital price ratios among 19 hospital referral regions (HRRs) with high ratios in 2012 and large ratio decreases in 2012–19

| HRR name | 2012 | 2019 | Changea |

|---|---|---|---|

| Gulfport, MS | 267% | 158% | −109 |

| Lafayette, IN | 357 | 279 | −78 |

| Pueblo, CO | 275 | 197 | −78 |

| Lawton, OK | 220 | 167 | −54 |

| Casper, WY | 246 | 193 | −52 |

| Hickory, NC | 223 | 171 | −52 |

| St. Joseph, MI | 233 | 182 | −51 |

| Bloomington, IL | 254 | 207 | −47 |

| Cape Girardeau, MO | 255 | 209 | −46 |

| Albany, GA | 219 | 173 | −46 |

| South Bend, IN | 254 | 211 | −43 |

| Longview, TX | 264 | 224 | −40 |

| Contra Costa County, CA | 314 | 273 | −40 |

| Munster, IN | 215 | 185 | −30 |

| Reading, PA | 206 | 177 | −29 |

| Omaha, NE | 206 | 181 | −25 |

| Rapid City, SD | 203 | 178 | −25 |

| Gary, IN | 218 | 195 | −23 |

| Stockton, CA | 234 | 215 | −20 |

SOURCE Authors’ analysis of 2012–19 Healthcare Cost Report Information System data. NOTES Price ratio estimates reflect estimated commercial revenue-to-charge ratios divided by Medicare revenue-to-charge ratios. The commercial-to-Medicare hospital price ratios for these nineteen HRRs fall into the top quartile of ratios in 2012 and, among hospitals in the top quartile of ratios in 2012, the bottom quartile of ratio increases during the 2012–19 study period.

Percentage points.

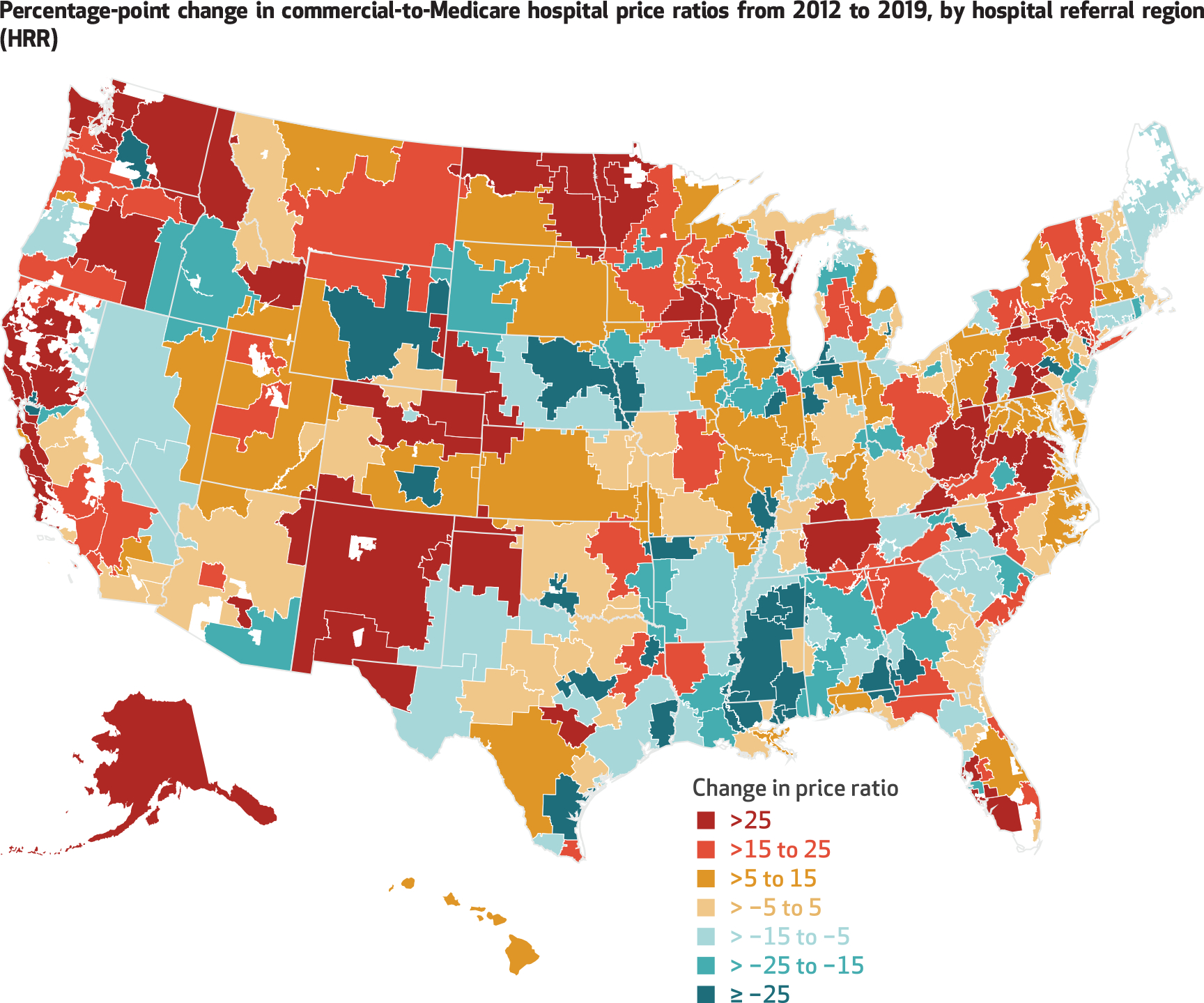

Exhibit 4 maps trend results in price ratios from the period 2012–19, illustrating how trends varied substantially across the country by HRR and within states. For example, in Colorado, commercial prices increased from 266 percent to 296 percent of Medicare rates in the Greeley HRR, whereas they decreased from 275 percent to 197 percent of Medicare rates in the Pueblo HRR. (Appendix exhibits 7 and 8 map price ratio levels in 2012 and 2019, respectively, for every HRR, and appendix exhibit 10 displays price ratios for each HRR by year.)17

Exhibit 4. Percentage-point change in commercial-to-Medicare hospital price ratios from 2012 to 2019, by hospital referral region (HRR).

SOURCE Authors’ analysis of 2012–19 Healthcare Cost Report Information System (HCRIS) data. NOTES Price ratio estimates reflect estimated commercial revenue-to-charge ratios divided by Medicare revenue-to-charge ratios. Areas with no color are not part of an HRR.

Discussion

We found that average commercial-to-Medicare price ratios were relatively stable during the period 2012–19. However, trends varied substantially by HRR, with large increases in some regions and reductions in others. Although prior work has documented substantial variation in commercial prices across the US in a given year,6–9 we found that there was a large amount of geographic variation in price growth as well. Researchers could easily update our analyses to help policy makers monitor hospital price trends in the future (see the appendix for details).17

It was beyond the scope of this study to identify why commercial-to-Medicare price ratios increased substantially in some regions while falling in others, although some of our results align with anecdotal changes in health care markets. For example, during our sample period the state attorney general, labor unions, and employers brought legal action related to anticompetitive behavior against the dominant hospital system in Northern California, Sutter Health, which resulted in a $575 million settlement.18 This aligns with our finding that many of the regions with both high initial price ratios and large increases were in Northern California. In addition, in 2012 Massachusetts established the Health Policy Commission to monitor and reduce health care spending, with the objective of limiting growth to the state gross domestic product.19 Massachusetts stands out as a state in which commercial-to-Medicare price ratios were low throughout the sample period, with only modest levels of growth.

The variation in price ratio trends across HRRs suggests that there may be opportunities to constrain growth. Had the HRR-level percentage-point increases in commercial-to-Medicare price ratios been capped at the increase observed at the national level (7 percentage points), then the average ratio would have been 164 percent in 2019—that is, 9 percent less than the level observed (180 percent). Multiplying this 9 percent decrease by private insurers’ expenditures on hospital care in 2019 ($438 billion) suggests savings of $39 billion in 2019.1 For purposes of comparison, related work relied on the same data as this study and estimated that capping commercial prices at 200 percent of Medicare rates would have reduced hospital spending by about $43 billion in 2018.14 Aggregate savings would be larger if growth constraints were also applied to hospital charges, which would benefit self-pay patients and other payers.

Researchers and analysts have proposed a variety of policy options to reduce hospital price levels and price growth. One approach would be to regulate prices directly. For example, in 2010 Rhode Island capped commercial price inflation based on the growth rate of Medicare rates plus 1 percent.20 A cap on price levels, as opposed to growth, would have a more immediate effect that would be concentrated among a smaller group of hospitals (that is, those with prices above the cap). Another approach to constraining commercial prices would be to increase the competitiveness of hospital markets, such as by strengthening antitrust regulation or improving price transparency. Previous research suggests that increasing hospital market competition may reduce costs without necessarily reducing the quality of care,21 although doing so would entail some unique practical challenges. For example, hospital markets are already highly concentrated in many parts of the country,22 and some regions might not have a sufficient patient base to support several competing hospitals.23

Our estimates of commercial-to-Medicare price ratio levels and trends at the national level are consistent with some, but not all, of the prior research on this topic. Estimates of commercial-to-Medicare price ratios from previous studies range from 141 percent to 247 percent;2–10,12,13 our estimate (180 percent in 2019) falls within this broad range. Two prior Health Affairs articles and an American Hospital Association (AHA) report (along with a subsequent data release) found that average commercial hospital prices increased dramatically relative to Medicare rates between 1996 and 2012 before tapering off in subsequent years.2–5 In contrast to the latter finding, we estimated that there was a modest increase in price ratios after 2012. Among other differences from our study, the previous Health Affairs articles2,3 included Medicare Advantage and Medicaid managed care plans in their estimates of commercial prices and relied on survey data, which allowed them to adjust for health conditions and other patient characteristics, although these results were subject to sampling error. The AHA study relied on hospital-reported data but did not explain its methodology.4,5 Estimates of price ratios may vary across studies based on a variety of factors, such as the data set, the sample of hospitals and commercial insurers, the services analyzed, the weighting approach, and the method for deriving ratios.

Conclusion

Average commercial-to-Medicare hospital price ratios were relatively stable between 2012 and 2019, but trends varied substantially across HRRs. Restraining the growth of commercial prices has the potential to achieve significant reductions in health care spending.

Supplementary Material

Acknowledgments

Funding was provided by Arnold Ventures. The funding source had no role in the design and conduct of the study; collection, management, analysis, and interpretation of the data; and preparation, review, or approval of the manuscript.

Contributor Information

Zachary Levinson, RAND Corporation, Arlington, Virginia..

Nabeel Qureshi, RAND Corporation, Santa Monica, California..

Jodi L. Liu, RAND Corporation, Santa Monica.

Christopher M. Whaley, RAND Corporation, Santa Monica.

NOTES

- 1.Centers for Medicare and Medicaid Services. National health expenditures data: historical [Internet]. Baltimore (MD): CMS; 2020. Dec 16 [cited 2021 Jul 6]. Available from: https://www.cms.gov/Research-Statistics-Data-and-Systems/Statistics-Trends-and-Reports/NationalHealthExpendData/NationalHealthAccountsHistorical [Google Scholar]

- 2.Selden TM, Karaca Z, Keenan P, White C, Kronick R. The growing difference between public and private payment rates for inpatient hospital care. Health Aff (Millwood). 2015;34(12):2147–50. [DOI] [PubMed] [Google Scholar]

- 3.Selden TM. Differences between public and private hospital payment rates narrowed, 2012–16. Health Aff (Millwood). 2020;39(1):94–9. [DOI] [PubMed] [Google Scholar]

- 4.American Hospital Association. Trendwatch chartbook 2018: trends affecting hospitals and health systems [Internet]. Washington (DC): AHA; 2018. [cited 2022 Jan 28]. Available from: https://www.aha.org/system/files/2018-07/2018-aha-chartbook.pdf [Google Scholar]

- 5.American Hospital Association. Trendwatch chartbook 2020: supplementary data tables, trends in overall health care market [Internet]. Washington (DC): AHA; 2020. [cited 2022 Jan 28]. Available from: https://www.aha.org/system/files/media/file/2020/10/TrendwatchChartbook-2020-Appendix.pdf [Google Scholar]

- 6.Cooper Z, Craig SV, Gaynor M, Van Reenen J. The price ain’t right? Hospital prices and health spending on the privately insured. Q J Econ. 2019;134(1):51–107. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 7.Whaley CM, Briscombe B, Kerber R, O’Neill B, Kofner A. Nationwide evaluation of health care prices paid by private health plans: findings from round 3 of an employer-led transparency initiative [Internet]. Santa Monica (CA): RAND Corporation; 2020. Sep 18 [cited 2022 Jan 28]. Available from: https://www.rand.org/pubs/research_reports/RR4394.html [Google Scholar]

- 8.Chernew ME, Hicks AL, Shah SA. Wide state-level variation in commercial health care prices suggests uneven impact of price regulation. Health Aff (Millwood). 2020;39(5):791–9. [DOI] [PubMed] [Google Scholar]

- 9.Baker LC, Bundorf MK, Devlin AM, Kessler DP. Medicare Advantage plans pay hospitals less than traditional Medicare pays. Health Aff (Millwood). 2016;35(8):1444–51. [DOI] [PubMed] [Google Scholar]

- 10.Maeda JL, Nelson L. An analysis of private-sector prices for hospital admissions [Internet]. Washington (DC): Congressional Budget Office; 2017. Apr 4 [cited 2022 Jan 28]. (Working Paper No. 2017–02). Available from: https://www.cbo.gov/publication/52567 [Google Scholar]

- 11.Bai G, Anderson GF. Market power: price variation among commercial insurers for hospital services. Health Aff (Millwood). 2018;37(10):1615–22. [DOI] [PubMed] [Google Scholar]

- 12.Wallace J, Song Z. Traditional Medicare versus private insurance: how spending, volume, and price change at age sixty-five. Health Aff (Millwood). 2016;35(5):864–72. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 13.Lopez E, Neuman T, Jacobson G, Levitt L. How much more than Medicare do private insurers pay? A review of the literature [Internet]. San Francisco (CA): Henry J. Kaiser Family Foundation; 2020. Apr 15 [cited 2022 Jan 28]. Available from: https://www.kff.org/medicare/issue-brief/how-much-more-than-medicare-do-private-insurers-pay-a-review-of-the-literature/ [Google Scholar]

- 14.Liu JL, Levinson ZM, Qureshi NS, Whaley CM. Impact of policy options for reducing hospital prices paid by private health plans [Internet]. Santa Monica (CA): RAND Corporation; 2021. Feb 18 [cited 2022 Jan 28]. Available from: https://www.rand.org/pubs/research_reports/RRA805-1.html [Google Scholar]

- 15.Asper F Introduction to Medicare cost reports [Internet]. Minneapolis (MN): Research Data Assistance Center; 2013. Aug 14 [cited 2022 Jan 28]. Available from: https://resdac.org/videos/introduction-medicare-cost-reports-0 [Google Scholar]

- 16.Corporation RAND. RAND Hospital Data: FAQs [Internet]. Santa Monica (CA): RAND Corporation; 2021. [cited 2022 Jan 28]. Available from: https://www.hospitaldatasets.org/faq [Google Scholar]

- 17.To access the appendix, click on the Details tab of the article online.

- 18.Thomas K Sutter Health to pay $575 million to settle antitrust lawsuit. New York Times [serial on the Interne; t]. 2019. Dec 21 [cited 2022 Jan 28]. Available from: https://www.nytimes.com/2019/12/20/health/sutter-health-settlement-california.html [Google Scholar]

- 19.Massachusetts Health Policy Commission. Health care cost growth benchmark [Internet]. Boston (MA): The Commission; 2021. [cited 2022 Jan 28]. Available from: https://www.mass.gov/info-details/health-care-cost-growth-benchmark [Google Scholar]

- 20.Baum A, Song Z, Landon BE, Phillips RS, Bitton A, Basu S. Health care spending slowed after Rhode Island applied affordability standards to commercial insurers. Health Aff (Millwood) 2019;38(2):237–45. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 21.Gaynor M What to do about healthcare markets? Policies to make health-care markets work [Internet]. Washington (DC): Brookings Institution; 2020. Mar 10 [cited 2022 Jan 28]. Available from: https://www.brookings.edu/research/what-to-do-about-health-care-markets-policies-to-make-health-care-markets-work/ [Google Scholar]

- 22.Fulton BD. Health care market concentration trends in the United States: evidence and policy responses. Health Aff (Millwood). 2017;36(9):1530–8. [DOI] [PubMed] [Google Scholar]

- 23.Glied SA, Altman SH. Beyond antitrust: health care and health insurance market trends and the future of competition. Health Aff (Millwood). 2017;36(9):1572–7. [DOI] [PubMed] [Google Scholar]

Associated Data

This section collects any data citations, data availability statements, or supplementary materials included in this article.