Summary

This study aims to comprehensively review a recently emerging multidisciplinary area related to the application of deep learning methods in cryptocurrency research. We first review popular deep learning models employed in multiple financial application scenarios, including convolutional neural networks, recurrent neural networks, deep belief networks, and deep reinforcement learning. We also give an overview of cryptocurrencies by outlining the cryptocurrency history and discussing primary representative currencies. Based on the reviewed deep learning methods and cryptocurrencies, we conduct a literature review on deep learning methods in cryptocurrency research across various modeling tasks, including price prediction, portfolio construction, bubble analysis, abnormal trading, trading regulations and initial coin offering in cryptocurrency. Moreover, we discuss and evaluate the reviewed studies from perspectives of modeling approaches, empirical data, experiment results and specific innovations. Finally, we conclude this literature review by informing future research directions and foci for deep learning in cryptocurrency.

Subject areas: Artificial intelligence, Machine learning, Social sciences, Economics

Graphical abstract

Artificial intelligence; Machine learning; Social sciences; Economics

Introduction

Deep learning is an algorithm model based on various deep neural networks. The ultimate goal of deep learning is to enable machines to analyze and learn like humans and recognize data such as text, images and sound. Deep learning is a complex machine learning algorithm that has achieved significant advancements in speech and image recognition. Compared with traditional machine learning algorithms, deep neural networks need data preprocessing and feature extraction before training. In addition, deep neural networks use the cascade of multi-layer nonlinear processing units for automatic feature extraction and transformation. This enhances the ability of neural networks to discover nonlinear relationships between data and improve the learning ability regarding the original data.1 In the past few years, based on the big data collected from information sets, parallel processing capabilities of graphics processing units (GPUs), and new families of convolutional neural networks, deep learning methods have achieved great success in many different applications, including image classification,2 object detection,3 time series prediction.4

Essential tools for deep learning have been evolving rapidly in the past few years. With ever-improving programming packages, it has become easier to implement and test new deep learning models. As an emerging field of machine learning, deep learning is currently applied in multiple scenarios, from autonomous vehicles to image recognition, hazard prediction, health informatics and bioinformatics.5,6,7 In addition, several comparative studies evaluated the performance of deep learning models versus standard machine learning models, for example, support vector machines (SVM),8 K-nearest Neighbors (KNN),9 and generalized regressive neural networks (GRNN)10 in economic research.

With a strong ability to process big data and learn nonlinear relationships between input features and predicted targets, deep learning models perform better in prediction tasks than linear and machine learning models in the financial field, especially in the cryptocurrency market. Cryptocurrencies are currencies generated by computer programs, distributed and circulated on the Internet based on cryptography and network P2P technology. In addition to studying the mechanism of digital currency from the perspective of computer science and cryptography, researchers have also started the economic analysis of cryptocurrency, such as the currency characteristics and asset attributes, as well as the innovation of introducing cryptocurrency to traditional monetary theory and payment methods.11,12,13 Some researchers also employ machine learning and deep learning models to model the cryptocurrency market. For example, Lahmiri & Bekiros10 compared the performance of long short term memory(LSTM) and generalized regression neural network(GRNN) in predicting cryptocurrency prices, which involves cryptocurrencies including Bitcoin, digital cash, and Ripple. They revealed that the LSTM model has better prediction performance than GRNN. Altan et al.14 claimed that by testing their proposed model using Bitcoin, Ripple, digital cash, and Litecoin time series data, the combination of LSTM and empirical wavelet transform (EWT) improved the performance of LSTM in predicting digital currency prices. Jiang & Liang15 developed a convolutional neural network(CNN) model to predict the price of Bitcoin, where historical data on financial asset prices is employed to train the proposed model and pooled portfolio weights are the model’s output.

There is considerable literature about cryptocurrency, and researchers have published several surveys reviewing and exploring the topic from different perspectives and application areas. Those include reviews on cryptocurrency trading systems,16 and mining systems,17,18 reviews on specific modeling tasks concerning cryptocurrency transactions such as knowledge discovery19 and cryptocurrency price prediction.20,21,22 A few of these studies review the cryptocurrency price prediction models from the perspective of modeling paradigms. For example, Sina et al.21 review the cryptocurrency price prediction models that use artificial neural networks (ANN)s. Similarly, Ahmed et al.20 focus on the traditional statistical and machine-learning techniques employed in cryptocurrency price prediction tasks. However, none of these studies review the deep learning methods involved in multiple modeling tasks in cryptocurrency, thus becoming a research gap to address in this study.

Therefore, this study comprehensively reviews the deep learning methods employed in cryptocurrency research across multiple modeling tasks, including price prediction, portfolio, bubble analysis, abnormal trading, trading regulations and initial coin offering in cryptocurrency. We first review popular deep learning models employed in multiple financial application scenarios, including CNNs, recurrent neural networks (RNNs), deep belief networks (DBNs), and deep reinforcement learning (DRL). We also give an overview of cryptocurrencies by outlining the cryptocurrency history and discussing primary representative currencies. Based on the reviewed deep learning methods and cryptocurrencies, we conduct a literature review on the new multidisciplinary area that employs deep learning models on cryptocurrency. We discuss applications of deep learning models in financial research from perspectives of modeling approaches, empirical data, experiment results and specific innovations. Finally, we point out the research challenges for future study.

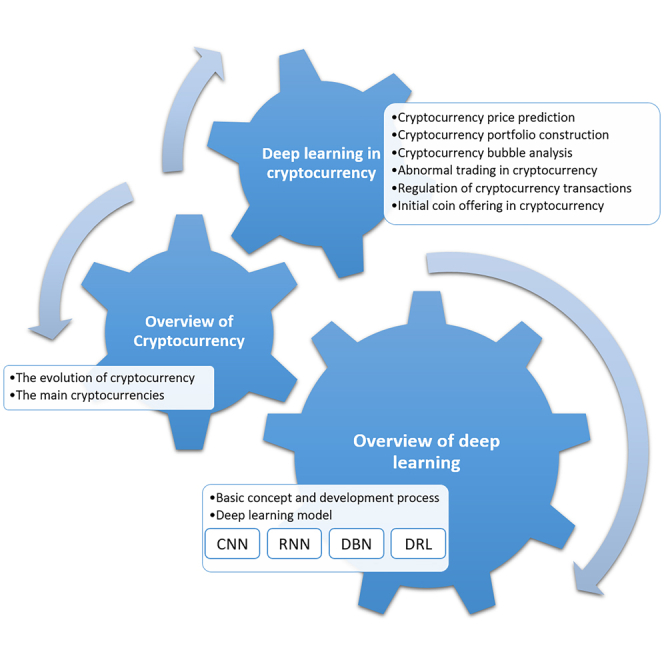

This study is organized as follows. Sections, Overview of deep learning and Overview of Cryptocurrency, respectively review the deep learning methods and development path of cryptocurrency. In the Deep learning in cryptocurrency Section, comprehensively review deep learning methods employed in multiple modeling tasks related to cryptocurrency. This is followed by the Challenges and Future Directions Section, where we identify the research challenges and directions. Finally, we conclude this literature review in the Conclusion.

Overview of deep learning

This section overviews the deep learning methods by introducing related concepts and development over the years and reviewing fundamental deep learning models. A group of deep learning models will be mentioned in this section.

Basic concept and development process

Deep learning is a new concept in artificial neural network research originally proposed by Geoffrey & Ruslan.33 It is a machine learning method that primarily simulates the human brain to evaluate and understand data and information. Through supervised and unsupervised learning, deep learning creates a new interpretation mechanism. Deep learning has significantly advanced artificial intelligence, which has made it possible for AI concepts and technology to be broadly accepted and used. Deep learning methods have enabled significant advancements in various fields, such as speech recognition,34 face recognition35 and image analysis.36 Therefore, it has quickly emerged as one of the most crucial ideas in artificial intelligence and computer technology and has profoundly and quickly impacted how people work, learn, and live. At the same time, the combination of deep learning and the financial sector has gained prominence as an emerging field of study in recent years, making advances in both theoretical and practical application.37,38

Deep learning methods can learn rules from vast amounts of data using neural network models, thus emerging as one of the most significant developments in artificial intelligence. It has consistently displayed high application vitality during the development process of more than ten years. To have an overview of the deep learning’s history, we discuss the crucial phases in the evolution of deep learning (See Figure 1).

Figure 1.

Development of artificial intelligence and deep learning

The idea of artificial intelligence was developed and established in the 1950s.39 Scientists including John McCarthy, Marvin Minsky, and Claude Shannon gathered in August 1956 at Hanover’s serene Dartmouth College to discuss the cutting edge of using machines to emulate human learning and other characteristics of intelligence. The Dartmouth Conference was a two-month gathering that marked the beginning of a new era in the development of artificial intelligence. Thus, 1956 also marked the birth of artificial intelligence.

Artificial intelligence has entered the “knowledge application period” since the middle of the 1970s.40 During this time, “expert systems”-based AI algorithms started to be used by businesses worldwide, and “knowledge processing” was the principal topic of mainstream AI research. Expert systems and knowledge engineering had extraordinary global growth throughout the 1980s, and both businesses and individual users have benefited financially from using them.

From the end of the 1980s to the beginning of this century, more and more algorithms were developed and applied, such as decision tree algorithm,41 boosting algorithm,42 support vector machine (SVM)43 and random forest.44

Hinton, a leading specialist in neural networks, created the neural network deep learning algorithm in 2006, considerably enhancing neural networks’ capabilities and ushering in a new era of deep learning in both academia and business.45 LeNets, a deep learning network developed by Hinton student Yann LeCun, is widely utilized in global banking and financial services as well as automated deposit and withdrawal equipment.46 As a result, 2006 might be considered to be the year when deep learning really got started and the year that it really started to catch on among academics.

At the beginning of 2010, the application in the military field is an essential process for the development of many cutting-edge technologies, and deep learning is certainly no exception: DARPA is the first deep learning project funded by the US Department of Defense in 2010, which has promoted the application and popularization of deep learning in the military and defense industry to a large extent.47 In 2011, deep learning made a breakthrough in speech recognition,48 improving various real-world applications such as e-commerce49 and customer service.50

In 2012, deep learning was applied to drug activity prediction and achieved the best results in the world. Google Brain, a deep learning-based face recognition system, made a breakthrough in 2012 by comprehending and recognizing cats’ faces from numerous photos.51 In 2017, these technologies were used in more real-world scenarios, making people’s daily lives convenient.

In 2014, the DeepFace system improved the accuracy of face recognition to 97.25%, which is close to the performance of normal humans.35 The promotion of application and the improvement of efficiency make face recognition technology reliable. At the same time, surpassing human capabilities means that deep learning is beginning to exert practical value.36,52

NVIDIA and Google developed particular processors for deep learning in 2015, motivating the development of deep learning technology from two aspects, hardware and software.53 Yann et al.1 proposed a new deep learning method, further revitalizing the research on neural networks. After that, deep learning continued to heat up.

In 2016, the computer program AlphaGo defeated Lee Sedol, one of the finest human Go players.54 The media enthusiastically hailed this victory as “truly conquering the most difficult and intelligent Go project.”55 In the game of Go, AlphaGo defeated Ke Jie, the current world No. 1 player, in 2017.56 This victory demonstrated that humans cannot defeat artificial intelligence using deep learning technology, making deep learning technology and artificial intelligence a hot topic of discussion worldwide.

Deep learning model

In this section, we respectively review four fundamental deep learning models, including (1) convolutional neural network, (2) deep belief network and (3) deep reinforcement learning.

Convolutional neural network

Convolutional neural network (CNN) is an outstanding feedforward neural network (FFNN) recognition technique.57 Its artificial neurons can respond promptly to surrounding units in a defined area, with an outstanding performance in large image processing and object detection.1,58 Therefore, in recent years, the emerging CNN plays a prominent role in image recognition and analysis, which also makes people pay more attention to its research and development.59,60,61,62,63

As shown in Figure 2, CNN takes FFNN as the technical core and collects, analyses and integrates image information through the “layer by layer” neuron response recognition mode to improve the efficiency of recognition and reliable quality. In Figure 2, CNN consists of input, convolutional, pooling, and fully connected layers. The input image first reaches the convolutional layer and gets processed by the pooling layer. It then goes through the convolutional and pooling layers again and finally enters the fully connected layer. We can see that the value of the fully connected layer is from 1024 to 512, and the final display is 10, which shows the great advantage of CNN in image processing. When the input propagates to further layers, the CNN model can use this structure to decrease the amount of input parameters and obtain abstract features.64

Figure 2.

Convolutional Neural Network

Notes: In Figure 2, CNN consists of input, convolutional, pooling, and fully connected layers. We can see that the value of the fully connected layer is from 1024 to 512, and the final display is 10, which shows the great advantage of CNN in image processing.

CNN has been employed in various application scenarios. The proposal and development of CNN technology enable the artificial neuron response method of FFNN to process large images while also having better performance in speech recognition.65 Moreover, Li66 studied the critical value of CNN application in computer vision, which involves three representative research topics, including object recognition,67 image annotation68 and image recognition.69 In addition, Zhou70 has proved the universality of CNN and the probability of using it to approximate any continuous function.

Considerable studies apply CNN to corporate financing decisions and financial forecasts. Ding27 combined neural tensor network and deep CNN to process the text information and predict stock price. The model in this study is composed of two parts, including (i) a neural tensor network that conducts event embedding training on the events extracted from the news text and (ii) a deep CNN that captures the impact of the events. Compared with the standard FFNN, the prediction accuracy of the established CNN-based model for the S&P 500 index and related individual stocks is improved by nearly 6%. Chen26 proposed a CNN-based financial time series analysis method. Vargas et al.25 proposed a new deep learning model, RCNN model, using 106,494 financial news from Reuters and compared its stock prediction performance with the traditional CNN and neural network (NN) models. Korczak & Hemes24 proposed a financial time series prediction method based on CNN and accordingly developed a multi-agent stock trading system. The experiment on S&P 500 index, FTSE 100 index, oil index and gold index proved that the proposed CNN-based method significantly improves the prediction accuracy. Sohangir et al.23 analyzed StockTwits investment sentiment data (from January 1, 2015 to June 30, 2015) to determine whether using deep learning models could improve StockTwits’ sentiment analysis performance. The results show that deep learning models can effectively assist financial sentiment analysis, and CNN is the best model to predict the sentiment of StockTwits authors. Based on empirical mode decomposition (EMD) and fully integrated empirical mode decomposition (CEEMD) algorithm, Rezaei et al.28 proposed CEEMD-CNN-LSTM and EMD-CNN-LSTM hybrid algorithms for the prediction of stock indexes. Jing et al.29 used CNN model to classify the hidden emotional factors extracted from stock forums, which improved the accuracy of stock prediction. Pol et al.30 used the CNN model to predict the financial data of more than 1761 Indian companies in the IT sector from 2015 to 2020 and rank the credit of each company. Ortu et al.31 focused on the two largest cryptocurrencies by market capitalization, Ethereum and Bitcoin, during the 2017–2020 period to predict and classify the trend of price movements with CNN and other deep learning models.

In addition, the application of CNN plays an important role in quantitative trading. Quantitative trading systems can be generally divided into three parts: trading signal (pattern recognition), position control and asset management. The application of CNN in signal recognition, information collection, image analysis and other activities within these three parts is of great help to the final trading decision. For example, Brim & Flann32 used CNN to obtain market returns that outperform the S&P 500 index and analyzed how the system trades. In order to facilitate relevant researchers to understand the research status in recent years, we create a table for comparative analysis of research from perspectives of model, data, results and innovations (See Table 1). By enumerating these studies, we find that CNN models perform well in the prediction tasks involved in various financial markets. Moreover, it can be incorporated into other models to increase their interpretability.

Table 1.

CNN applications in financial research

| Models | Targets | Markets | Data | Results | Innovation | References |

|---|---|---|---|---|---|---|

| CNN LSTM (RNN) |

Investment sentiment prediction |

Stock | StockTwits Investment Sentiment Data (January 1, 2015 June 30, 2015) | It is proved that CNN can overcome the problems of data mining methods in stock sentiment analysis | CNN is the best model to predict investor sentiment | Sohangir et al.23 |

| CNN | Financial time series method |

Stock, gold and petroleum |

S&P 500 index, FTSE 100 index, petroleum and gold index (hour, daily, weekly, monthly data) | The prediction error rate of CNN is significantly reduced | Proposed new A-Trader system’s investing strategy and a financial time series forecasting method. | Korczak and Hemes24 |

| CNN, RNN, RCNN |

Stock index forecast | Stock | 106,494 Reuters Financial News (20 October 2006-21 November 2013) | While RNN has more advantages in capturing contextual data and complex time features, CNN is better at capturing text semantics. | A new model called the RCNN model is developed. | Vargas et al.25 |

| CNN | Financial time series method |

Futures | Taiwan Index Futures One-minute Trading Data (January 2, 2001 April 24, 2015) | The CNN model can collect certain features and classify them for the futures market. | This paper proposes a deep learning-based financial time series analysis method | Chen et al.26 |

| CNN, novel neural tensor network |

Stock price prediction | Stock | Reuters, Bloomberg Financial News headlines (October 2006 November 2013) | The prediction accuracy is improved by about 6% | Deep learning models were first applied to event-driven stock market forecasting | Ding et al.27 |

| CNN, LSTM |

Stock price prediction | Stock | daily time series from January 2010 to September 2019, include the closing prices of the S&P 500, Dow Jones, DAX, and Nikkei 225 | It demonstrates how CNN maybe combined with LSTM, CEEMD, or EMD to increase prediction accuracy and exceed the competition. | The use of CEEMD-CNN-LSTM and EMD-CNN-LSTM hybrid algorithms. | Rezaei et al.28 |

| CNN, LSTM |

Time series analysis and financial market forecast- ing under investor sentiment |

Stock | Between January 1, 2017, and July 31, 2019, six industries having a market value of up to 1.008 billion yuan and five stocks were randomly chosen from each industry. | Future stock price predictions are more accurate when investor sentiment and technical indicators based on LSTM neural networks are combined. | Combining the LSTM neural network method for price prediction with the CNN model for sentiment analysis | Jing et al.29 |

| MLP, CNN, LSTM |

Company financial credit ranking |

Corporate Finance |

Financial data of over 1761 Indian companies with IT sector from 2015 to 2020 | MLP is the most efficient predictor of a company’s financial situation. | Combine several deep learning models to estimate each company’s credit rating from high to poor. | Pol et al.30 |

| MLP, LSTM, MALSTMFCN, CNN |

Financial time series method |

Crypto-currency | Bitcoin and Ethereum price time series from January 1, 2017 to January 1, 2021 | The CNN model performs the best among the constrained models. The LSTM neural network’s average accuracy in unrestricted is 83% and 84%, respectively. | Using unrestricted models of technical, trading, and social media variables to increase prediction accuracy. | Ortu et al.31 |

| CNN, DDQN |

Stock index forecast | Stock | Training dataset generated by 30 stocks in the S&P 500 index from January 2, 2013 to December 31, 2019, testing dataset from January 1, 2020 to June 30, 2020 | The feature map visualization in stock market prediction is realized. | Using CNN in DDQN to outperform S&P 500 index returns and analyze how does the system trade. | Brim and Flann32 |

Recurrent neural network

Recurrent neural network (RNN) is a general term for two kinds of artificial neural networks: temporal RNN and structural RNN. Specifically, the connections between neurons of temporal RNN constitute directed graphs, while structural recurrent neural networks use similar neural network structures to build more complex deep networks recursively. These two neutral networks’ training methods have slight differences even though they belong to the same algorithmic framework. Regarding operation mechanism, RNN is a kind of network constructed by the method of structural recursion.71

RNN models are generally used to describe sequences of dynamic behaviors that circulate states in the basic network framework and can accept a wider range of time series structure inputs. Current representative RNN include traditional RNN, LSTM neural network and gated recurrent unit (GRU) models. Unlike feedforward deep neural network (FDNN), RNN pays more attention to the feedback effect of the network. RNN has a specific memory function due to the connection between the current and previous states. In this model, the information flow is governed by three gates, including the input gate, the forget gate and the output gate. The input gate decides the information to store in the current state. The forget gate determines the removal of information. The output is related to the output information in the current state. The structure of RNN is shown in Figure 3.

Figure 3.

Recurrent Neural Network

Notes: In this model, the information flow is governed by three gates, including the input gate, the forget gate and the output gate. The input gate decides the information to store in the current state. The forget gate determines the removal of information. The output is related to the output information in current state.

Regarding specific applications of RNN, Graves et al.34 found that RNN could essentially guide and expand the application scope in speech recognition. This neural network model promotes greater technical innovation in speech recognition when it is applied to the combination of natural language sequences or voice analysis and interpretation.

In the financial field, RNN models are widely employed in financial market prediction research involving the stock market, futures market and crude oil market. Yoshihara et al.72 first proposed a deep learning model that combines RNN and restricted Boltzmann machine to process the text information of news events (834,882 financial news items of Keizai Shimbun from 1999 to 2008) and predict stock price movements. Xiong et al.73 used the LSTM neural network to model the S&P 500 volatility and studied the factors affecting the S&P 500 volatility, including the macroeconomic factors and the public sentiment factor represented by Google domestic trends data (from October 19, 2004 to July 24, 2015). Heaton et al.74 analyzed the stock prices of the S&P 500 index and 20 included companies, and proposed a hierarchical decision model for financial forecasting and classification problems, which, based on RNN models, can improve the forecasting performance of traditional financial applications. Singh et al.75 demonstrated that deep learning with the method 2-Directional 2-Dimensional Principal Component Analysis ((2D)2 PCA) can improve inventory multimedia (graph) prediction accuracy, compared with the traditional neutral network method. As the study showed that correlation coefficient between actual income and predicted income of (2D)2 PCA + DNN is 17.1% higher than (2D)2 PCA + RBFNN and 43.4% better than RNN in the aspect of stock prediction. Deng et al.76 used RNN to process the characteristics of real-time financial signals and tried to build quantitative trading strategies based on structure to beat experienced financial asset traders. This study uses deep learning technology to learn and extract relevant features from dynamic market conditions automatically and, afterward, uses reinforcement learning technology to make trading decisions in unknown environments. This model can reflect both the deep structure and the circular structure, and the experiment results show that the model performance is robust in both the stock market and the commodity futures market. Moreover, some researchers find that the combination of principal component analysis (PCA) and recurrent neural network (RNN) enables the consideration of both fundamental and price information of stocks and balances the trade-off between the performance and diversity of the selected stock, thus making the prediction of the future trend of the stock market more robust.77,78

Recent studies have extended and applied RNN models to improve different financial market forecasting methods. Karaoglu et al.79 improved RNN to detect excessive movement in noisy time series data streams. Berat Sezer et al.80 proposed a stock price prediction and trading system based on neural network technical analysis indicators. Bao et al.81 employ six market indexes, including the A-share CSI 300 index in mainland China, the Nifty 50 index representing the Indian stock market, the Hang Seng Index in Hong Kong stock market, the Nikkei 225 index in Tokyo, the S&P 500 index and the DJIA index in New York Stock Exchange, as examples. This study presents a novel deep learning framework where wavelet transforms (WT), stacked autoencoders (SAEs) and LSTM are combined to predict stock price and is proved to outperform other similar models in accuracy and profitability. Yan et al.82 employed LSTM to predict the daily closing price of Shanghai Composite Index from January 4, 2012 to June 31, 2017, which presents better prediction accuracy for both static and trend prediction of financial time series. This experiment illustrates the applicability and effectiveness of LSTM in financial time series forecasting. Meanwhile, researchers find that the wavelet decomposition and reconstruction of financial time series can improve the generalization ability of LSTM forecasting model and the prediction accuracy of long-term dynamic trend. For example, Fischer et al.83 applied LSTM networks to S&P 500 index time series forecasting (December 1989 to September 2015) and found that they performed better than non-categorical memory methods such as Random Forest (RF), deep neural networks (DNN), and logistic regression classifiers (LOG). Chen et al.84 proposed a new hybrid crude oil price prediction model based on Deep Belief Network (DBN) and LSTM model and used the model to analyze and simulate the crude oil price trend. Ji et al.85 used traditional stock financial index variables and social media text features as the input of the prediction model based on LSTM. Prachyachuwong & Vateekul86 adopted a bidirectional encoder model composed of LSTM and Bidirectional Encoder Representation from Transformers (BERT) architecture to predict the daily activity of the Thailand stock market. Adisa et al.87 improved LSTM model for financial prediction and found that the improved model was superior to the single classifier and ensemble classifier models.

Regarding portfolio allocation strategies, Xie et al.88 designed a two-stage system, namely LSTMcon, which consists of an asset price prediction model and a decision strategy based on set rules. Yue et al.89 proposed a deep reinforcement learning model based on the Markov decision process model in the context of COVID-19, including the stacked sparse denoising autoencoder (SSDAE) model and the long–short-term-memory-based autoencoder(LSTM-AE) model. Overall, the decision-making of the portfolio management process is improved from two perspectives: time series analysis and information extraction based on market observations. In order to facilitate relevant researchers to understand the research status in recent years, this section lists two tables for comparative analysis of model, data, experiment results and innovations, as shown in Tables 2 and 3. The RNN model is more widely employed in stock price prediction tasks, and multiple studies have validated the impact of different RNN model algorithms on prediction performances.

Table 2.

RNN applications in financial research (1)

| Models | Targets | Markets | Data | Results | Innovation | References |

|---|---|---|---|---|---|---|

| RNN, DBN |

Stock price trend prediction | Stock | 834,882 Nikkei Financial News (1999–2008) | The proposed DBN combination has the lowest error rate. | RNN is combined with restricted Boltzmann machine to predict the stock market trend. | Yoshihara et al.72 |

| LSTM (RNN) |

Stock index forecast | Stock | Google Domestic Trends Data (October 19, 2004 July 24, 2015) | The MAPE was 24.2%. | The impact of public sentiment and macroeconomic factors on the volatility of the S&P 500 index. | Xiong et al.73 |

| RNN | Stock price trend and stock index forecast | Stock | The S&P 500 index and the stock prices of 20 companies are included. | It improves the predictability of traditional financial applications. | A hierarchical decision model for the classification of financial forecasts is proposed. | Heaton et al.74 |

| RNN, DNN |

Stock price prediction | Stock | Multimedia data of Google’s stock price in the NASDAQ | The correlation coefficient between actual and predicted income for DNN is 17.1% higher than for RBFNN and 43.4% higher than for RNN. | Compared with traditional neural networks, (2D) ZPCA + has improved accuracy on Google datasets | Singh and Srivastava75 |

| RNN | Establish a real-time financial trading system based on deep learning |

Stock and futures | The first index-based IF stock futures contract in China and the first silver (AG) and sugar (SU) futures contract in the commodity market (2014.1–2015.9) | The model has good application effect and robustness in both stock market and commodity futures market | A model consisting of deep learning and reinforcement learning is proposed | Deng et al.76 |

| RNN | The performance of the model is examined in interperiod time series data | Stock | Istanbul Stock Exchange fixed time interval data | The model has good performance and has been successful in data trading. | RNN is improved to make it more suitable for time series data and detect excessive movement in noisy time series data streams | Karaoglu et al.79 |

| RNN | Stock price prediction | Stock | Daily stock prices for all Do230 stocks between 1997 and 2007 | In most cases, the results of the correct buy-and-hold strategy are achievable. | A stock price prediction and trading system based on neural network technical analysis index is proposed. | Sezer et a l.80 |

| LSTM (RNN), WT, SAEs |

Forecasts of stock prices and stock indices | Stock | CSI 300 index, NIFTY 50 Index, Hang Seng Index, Nikkei 225 index, S&P 500 index and Dow Jones Index | This model outperforms other similar models in terms of forecasting accuracy and profitability. | A deep learning framework combining wavelet transform, stacked autoencoder and LSTM is proposed to predict stock prices | Bao et al.81 |

Table 3.

RNN applications in financial research (2)

| Models | Targets | Markets | Data | Results | Innovation | References |

|---|---|---|---|---|---|---|

| LSTM (RNN) |

Forecast the daily closing price of the Shanghai Stock Exchange Composite Index |

Stock | Daily Closing Price of Shanghai Composite Index (January 4, 2012 June 31, 2017) | LSTM performs well for both static and dynamic trend prediction of financial time series. | According to the complex characteristics of financial time series, a new time series forecasting model is proposed. | Yan and Ouyang82 |

| LSTM (RNN), DNN |

Forecast stock price volatility |

Stock | S&P 500 Index (December 1989 to September 2015) | The LSTM network performs better than RAF, DNN, and LOG | The LSTM network is applied to financial time series forecasting, and portfolio strategy. | Fischer and Krauss83 |

| LSTM (RNN), DBN |

Forecasting Crude oil prices | Crude Oil | 2409 WTI Crude Oil Market Price Data (July 23, 2007 February 24, 2017) | The model improves the prediction accuracy | This paper proposes a novel hybrid crude oil price prediction model based on deep learning. | Chen et al.84 |

| Doc2Vec, SAE- LSTM, wavelet transform |

Stock price volatility forecast |

Stock | From January 2010 to November 2019, investors’ comments and company news on the top 15 pharmaceutical listed companies. | It eliminates the interference of random noise brought by stock market volatility to stock prediction. | Fusion of traditional financial features and social media text features derived from social media | Ji et al.85 |

| BERT, LSTM |

Stock and futures price volatility prediction |

Stock and futures markets | Economic topics in Thai news headlines from 2014 to 2020, and Thai stock market data | Simultaneously improving numerical and textual information enhances predicting performance and exceeds all baselines. | A deep learning model consisting of LSTM and from Transformer (BERT) is proposed. | Prachyachuwong and Vateekul86 |

| LSTM | Company financial credit score prediction |

Corporate Finance |

Credit score dataset provided by credit reporting agencies | The optimized LSTM model outperforms the single classifier model and the classifier model. | A method for optimizing deep learning algorithm parameters is given to close the gap left by LSTM prediction. | Adisa et al.87 |

| LSTM | Price prediction | Gold and Bitcoin | The prices of gold and bitcoin over a five-year trading period from September 11, 2016 to September 10, 2021 | The accuracy rate in the gold and bitcoin markets reached 98.5% and 98.8% respectively | Designs a two-stage system LSTMcon, which consists of an asset price forecasting model based on an ensemble rule | Xie et al.88 |

| MDP, SSDAE, LSTM-AE |

Quantitative portfolio management |

Stock | OHCLV data from January 1, 2007 to January 1, 2018 | In terms of Sharpe and Sortino ratios, the suggested portfolio management approach beats other models. | A deep reinforcement learning model for COVID-19 quantitative portfolio management is built using a Markov decision process model. | Yue et al.89 |

Deep belief network

Geoffrey Hinton proposed the DBN generative model in 2006.90 It is a generative model, which can generate training data with the entire neural network according to the maximum probability by training weight among neurons. DBN can be used to create data and categorize and define the properties of data. Many researchers analyze financial data using the DBN model to assist decision-making in financial transactions and investments.

In essence, the DBN model is an efficient machine learning algorithm that enables rapid data processing and integration by using a generative model. The integration of these two functionalities has a significant breakthrough point. As a result, DBN can better illustrate the transmission mode and data characteristics of information in financial applications.

As shown in Figure 4, DBN is derived from the restricted Boltzmann machine system (RBM). Stacked with the neuronal structure of RBM, the propagation of DBN is well-ordered. Meanwhile, the deep structure of DBN corresponds naturally to the deep learning architecture, reflecting the advantages of DBN regarding technological innovation.91

Figure 4.

Deep Belief Network

Notes: As shown in Figure 4, DBN is derived from the Restricted Boltzmann Machine system (RBM). Stacked with the neuronal structure of RBM, the propagation of DBN is well-ordered. Meanwhile, the deep structure of DBN corresponds naturally to the deep learning architecture, reflecting the advantages of DBN regarding technological innovation 91.

Hinton & Salakhutdinov33 first proposed the concept of a simple belief network and gave a prototype model. Their study proved that DBN-based neuron weight training can generate data with maximum probability, which meets the needs of computation and practical applications. Regarding financial applications, considerable studies use DBN on stock price forecasts. For example, Kuremoto et al.92 proposed a new neural network model for time series prediction with higher accuracy. Zhu et al.93 established an automatic stock decision support system by combining DBN with the oscillation box theory. The results show that systematic market-based trading with extreme learning machine algorithm outperforms the basic buy-and-hold strategy. Batres-Estrada94 applies new deep learning algorithms to predict financial stock data using the S&P 500 index (January 1, 1985 to December 31, 2006). Lanbouri95 used the financial data of 966 companies in France to combine deep learning and support vector machine (SVM) to build a financial distress prediction (FDP) model. Shen et al.96 to extend the application of DBN models to continuous data by introducing the constant restricted Boltzmann mechanism and use the proposed model to predict the weekly exchange rates of GBP/USD, INR/USD and BRL/USD. Sharang & Rao97 designed an intermediate frequency trading method based on the daily and biweekly average prices of US treasury futures over a five-year and ten-year term. They employed DBN model, which is composed of stacked restricted Boltzmann machines, to predict the weekly trend in the price of an asset portfolio. In addition, they devised trading strategies respectively based on the constructed prediction model and the random classifier model. To better understand the researches over the years, we create a table to summarize the model, data, results and innovations in DBN in Table 4. The DBN model has been used in the multifaceted subject of finance, particularly in forecasting company financial problems.

Table 4.

DBN applications in financial research

| Models | Targets | Markets | Data | Results | Innovation | References |

|---|---|---|---|---|---|---|

| DBN | Stock price trend prediction | Stock | The data are smoothed. | The new DBN combination proposed in this chapter has the lowest error rate. | A new neural network model for time series forecasting with high accuracy is proposed. | Kuremoto et al.92 |

| DBN | Stock price prediction | Stock | Historical trading data for the 400 stocks in the S&P 500 index | The model constructs systematic trading that outperforms the basic buy-and-hold strategy. | An automatic stock decision support system is established by using DBN and oscillatory box theory. | Zhu et al93 |

| DBN | Stock price prediction | Stock | S&P 500 Index (January 1, 1985 to December 31, 2006) | The results obtained by deep neural networks are better and more stable than the basic results. | New deep learning algorithms are used to predict financial stock data | Batres-Estrada98 |

| DBN | Forecast of financial distress of the company |

Corporate Finance |

Financial data for 966 French firms | The classification accuracy of the model is 76.8% | Deep learning and support vector machine are combined. | Lanbouri and Achchab95 |

| DBN | Exchange rate price forecast |

Foreign exchange | Weekly data for the three exchange rates GBP/USD, Indian Rupee/USD, and Brazilian real/USD | Compared with traditional methods, FFNN is more suitable for forecasting exchange rates and their effects. | An improved DBN algorithm (FFNN) is proposed to forecast the exchange rate | Shen et al.96 |

| DBN | Forecast of the weekly movement direction of the Treasury portfolio |

Treasury bond futures |

Daily and two-week average price data for 5 and 10-year Treasury futures. | The portfolio has a trade size of 10 units and a profit of 10 units, which is about 90,000 dollars. | Using the DBN of stack-constrained Boltzmann mechanism, an intermediate frequency trading strategy is designed |

Sharang and Rao97 |

| DBN | Financial time series methods |

Stock | Sample of financial series data of closing prices of all stocks in Shanghai and Shenzhen stock markets during the 100 working days prior to October 20, 2012 |

The accuracy of financial data samples selected by DBN model in quantitative decision analysis of financial time series data can reach 90.54% | Presents an improved modeling based on DBN and decision algorithm | Zeng et al.99 |

Deep reinforcement learning

Deep reinforcement learning (DRL) combines reinforcement learning (RL) and deep learning. The reinforcement learning algorithm sets the goals for DRL, while the deep learning algorithm provides the learning mechanism. DRL entails agents that observe states and take actions to gather long-term rewards. It also uses approximations or strategies to solve RL problems when the state space is too large or the action space is continuous. DRL has the powerful representation ability of neural networks to deal with high-dimensional inputs.66

Deep learning enables RL to be extended to previously intractable decision problems, namely environments with high-dimensional states and action spaces. There are two outstanding works in the DRL field. First the DRL development started by developing an algorithm that could learn directly from image pixels to play a series of video games on the Atari 2600 platform beyond learning ability of the human average.100 This study provides a solution to the instability of function approximation techniques in RL. It also demonstrates that RL agents can be trained on raw high-dimensional observations based only on reward signals. The second outstanding achievement is the development of the hybrid DRL system AlphaGo, which defeated the human world champion in Go101 after IBM’s Watson DeepQA system defeated the best human chess player 20 years ago.102 Unlike the DeepQA system’s manual rules, AlphaGo consists of neural networks trained using supervised and reinforcement learning and traditional heuristic search algorithms.

DRL is an end-to-end perception and control system from the standpoint of system structure, and its learning process can be summarized as follows: (1) The agent interacts with the environment every moment to obtain a high-dimensional observation. The agent then uses deep learning to interpret the observation to derive a representation of a particular state feature. (2) The agent then evaluates the value function of each action based on the expected return and maps the current state to the corresponding action using a specific strategy. (3) The environment responds to this action and receives the subsequent observation. The best method for achieving the objective can finally be found by repeating the abovementioned procedure.103

Currently, DRL algorithms have been applied to a wide range of problems, such as robotics, where the control strategy of the robot can now be learned directly from camera inputs in the real world,104 subsequent controllers are either manually designed or learned from low-dimensional features of the robot state. In a step toward more powerful agents, DRL has been used to create agents that can meta-learn,105 enabling them to adapt to complex visual environments that have not been seen before.106

DRL algorithms based on model-free approaches can generally be categorized as value-based and policy-based RL. Deep Q-network (DQN) is a common value-based RL method that solves the confused representation of high-dimensional state inputs by employing the maximum Q value as the low-dimensional action outputs.107 In contrast, policy-based RL is easier to implement in the continuous action space problem than value-based RL. This algorithm also prevents the policy deterioration due to value function mistake.108 Model-based RL, as opposed to model-free RL, requires less ongoing contact with the environment and learns a value function or policy in a data-efficient manner. Consequently, they can be applied to different scenarios.109

Using some algorithms that allow agents to learn how to create profits in any market sector, DRL is utilized in finance to boost earnings in financial markets. The main task of DRL is to collect data to design models with low latency and low cost training in financial markets. Using deep reinforcement learning enables the agent (the algorithm) to learn how to make profitable transactions, which also enables the methodology changes and the unique representation of the financial Markov decision process (FMDP).110 Liu et al.111 used the deep deterministic policy gradient (DDPG) algorithm as an alternative to exploring the optimal policy in the dynamic stock market. The algorithmic component of DDPG handles large action state spaces, pays attention to stability, eliminates sample correlation, and improves data utilization. The results show that the proposed model is robust in balancing risks and performs better than the Dow Jines Industrial Average and min-variance portfolio allocation method. Li et al.112 designed a new adaptive deep deterministic reinforcement learning framework (Adaptive DDPG) for optimal trading strategies in stock markets. The model combines optimistic and pessimistic deep RL, which relies on negative and positive forecast errors. The model can obtain better portfolio profits based on Dow Jones stocks in complex market situations. Li et al.113 studies DRL methods and their applications in stock decision-making mechanisms. The experiments with three classical DRL models (Deep Q-Network, Double DQN and Dueling DQN) show that the DQN model enables us to obtain better investment strategies to optimize stock trading returns. Raj Azhikodan et al.114 focused on the DRL automatic monitoring oscillation of securities trading, and they used a recursive convolutional neural network (RCNN) method to predict stock values from economic news. The primary focus of the DRL model’s application is stock market prediction, and more research is necessary to fully understand its use (See Table 5).

Table 5.

DRL applications in financial research

| Models | Targets | Markets | Data | Results | Innovation | References |

|---|---|---|---|---|---|---|

| DDPG | Investment portfolio allocation |

Stock | Daily data of Dow 30 stocks | The adaptive DDPG outperforms the baseline in terms of return on investment and Sharpe ratio. | The adaptive DDPG is compared with the traditional portfolio allocation strategy | Li et al.112 |

| DQN, DRL |

Stock market trading strategy | Stock | Daily data for 10 stocks from 2000 to 2018 | The DQN model works best in stock market investment decisions. | The feasibility of DRL in the field of financial strategy is demonstrated and three classical DRN models are compared. | Li et al.115 |

| RCNN, DRL |

The realization of automatic trading mechanism | Stock | 95,947 news headlines for 3,300 companies | It proves that deep reinforcement learning can learn the skills of stock trading. | Neutral network models based on deep deterministic policy gradients are trained to choose the action of selling, buying, or holding a stock | Azhikodan et al114 |

| DRL | Stock market trading strategy | Stock | Historical daily prices of the Dow 30 stocks from January 1, 2009 to September 30, 2018 | The proposed deep reinforcement learning method outperforms both baselines in terms of Sharpe ratio and cumulative return | A deep reinforcement learning agent model is trained and an adaptive trading strategy is obtained | Liu et al.116 |

Overview of cryptocurrency

To have an overview of cryptocurrency, we review the development path of cryptocurrency and introduce the main cryptocurrencies.

The evolution of cryptocurrency

The traditional monetary system is the collection of laws, regulations, legal structures, and organizations that the government uses to issue currency for use in economic activity. The major participants in this system are the central bank, the Treasury, the Mint and commercial banks. And three main different trading instruments are the legal tender, commodities and the asset backed by commodities from a historical perspective. Traditional monetary systems may be significantly vulnerable to bandwagon effects, where prices fluctuate under the impact of consumer behaviors. In addition, central banks may cause inflation by printing and devaluing money. As a result, traditional monetary systems are not convenient for purchase and cannot always satisfy the assumptions like infinite subdivision and relative stability of value.

The concept of exchanging money in digital form has become popular due to the drawbacks of conventional monetary exchange systems. The digital currency systems aim to improve the stability of the financial market and assist consumers by addressing problems like inflation and low yields. This concept can dramatically bring about economic benefits by enhancing operation efficiency, enabling convenience access and saving the cost of carry. The implementation of digital currency systems is also confronted with the question of whether the system should be based on the central bank or decentralized by replacing the central bank with a new monetary system.

David Chaum created the e-cash cryptosystem back in 1983.117 Twelve years later, he created DigiCash, another encryption system, to conceal financial transactions.118 Wei Dai employed the cryptosystem to create a new payment mechanism with a primary decentralization characteristic in 1998, the same year the word “cryptocurrency” first surfaced.119

The first and most prominent cryptocurrency is Bitcoin, launched by.120 Satoshi Nakamoto invented Bitcoin and made the source code available to the world. Bitcoin, altcoins, and tokens are the top three cryptocurrencies that are actively active on the market. Cryptocurrency technology is taking financial markets one step closer to the future by decentralizing money and releasing it from hierarchical power structures. With cryptocurrency technology, consumers and businesses execute transactions digitally through a peer-to-peer network.

In the short time since its birth, the cryptocurrency market has experienced exponential growth and widespread popularity (Figure 5). In recent years, cryptocurrencies have grown in popularity and received global media attention, attracting investors, academics, governments, regulators, and speculators. The future of Bitcoin, or any cryptocurrency, is not confined to any particular discipline; Instead, it transcends each domain.121

Figure 5.

Number of cryptocurrencies from 2013 to 2021 (https://www.statista.com/statistics/863917/number-crypto-coins-tokens/)

Litecoin was Launched in October of 2011. WordPress was the first retailer to accept Bitcoin payments in 2012.122 Many businesses now accept these digital currencies as payment for their goods and services. Moreover, some of them have developed their own digital currencies. El Salvador became the first nation to accept Bitcoin as legal money in June 2021. Following Resolution 215 in August 2021, Cuba recognized Bitcoin as a legal tender.123 By November 2021, there are 8,532 cryptocurrencies, up from 66 in November 2013.

Cryptocurrency investment has become more dependable due to the advancement of cryptocurrency research. However, considering the cryptocurrency market’s high risk and high volatility, the cryptocurrency market’s security and regulation are still vital. To stop crypto hijacking, there are considerable studies on the security of cryptocurrencies. Conrad et al.124 investigated the cryptocurrency security structure and discovered that security architecture is a complicated idea that incorporates security components of software, hardware, and operating systems in addition to procedures. McLean et al.125 sought to create security models that "describe any formal statement of a system’s confidentiality, availability, or integrity requirements.". Many researchers focus on the effectiveness of cryptocurrency mining by lowering the cost of mining. For example, Gundaboina et al.126 conducted statistical data analysis in a Dogecoin mining benchmark and found that the hashing algorithm determines mining cost. Mining companies are trying to use renewable energy to replace traditional energy and reduce the carbon footprint. Figure 6 summarizes the security and regulations that affected the cryptocurrency market in 2022, and the government regulatory policies for cryptocurrency risk events in 2023.

Figure 6.

Security and regulation events in the cryptocurrency market in 2022 and 2023

On February 3, the Wormhole system, which links Ethereum and Solana, was breached by hackers, who took 120,000 ETH with a market value of more than 320 million dollars. On March 29, the NFT game Axie Infinity revealed that its side chain Ronin Network had been compromised, causing losses of up to 620 million in the form of 173,600 ETH and 25.5 million USDC. An algorithmic stable-coin project called Beanstalk Farms was targeted on April 17, and the attack-related losses totaled 182 million USD dollars (https://www.bruegel.org/policy-brief/decentralised-finance-good-technology-bad-finance). On August 1, a compromise of the Nomad Bridge cross-chain technology resulted in the theft of more than 190 million USD dollars in cryptocurrency.127 On August 3, a large-scale theft occurred in the Solana system, causing a loss of much to 8 million in tokens from the wallets of several users. Due to the iBTC/aUSD pool, hackers also attacked the Polkadot ecological project Acala on August 14. As a result, more than 1.2 billion ecological stable-coins (AUSD) were created, which severely unanchored AUSD and caused a 70% price decline. Crypto market manufacturer Wintermute was attacked on September 21 and suffered a loss of roughly 162.5 million USD dollars (https://www.cshub.com/attacks/news/wintermute-loses-160-million-in-hack). On October 7, market manipulation by attackers resulted in a 100 million loss for the BNB Chain cross-chain bridge BSC Token Hub.128 A hack on October 12th cost Mango Markets, a DeFi platform with headquarters in Solana, more than 100 million USD dollars.129 Since the beginning of 2023, governments and regulators have begun to strengthen risk control in the cryptocurrency market. On January 3, the Federal Reserve, the Federal Deposit Insurance Corporation (FDIC) and the Office of the Comptroller of the Currency (OCC) issued a joint statement emphasizing that risks related to crypto assets cannot be transferred to the banking system. The Financial Accounting Standards Board (FASB) proposed an exposure draft on crypto assets in March 2023, which stipulates that entities must measure certain crypto assets at fair market value and recognize changes in fair value net income during each reporting period. The Financial Innovation and Technology for the 21st Century Act (FIT21) was proposed on July 20, 2023 to establish a regulatory framework for digital asset markets in the United States that provides clear rules for market participants and protects investors and consumers.

Traders in the cryptocurrency industry panicked and feared the onset of a “Lehman moment” in November 2022 after FTX, one of the biggest cryptocurrency exchanges in the world, collapsed. The timing of the incident, which had a significant impact on the cryptocurrency market, is reviewed in this survey.

As shown in Figure 7, between May 7 and May 13, 2022, numerous bitcoin decoupling incidents caused the cryptocurrency algorithm to ultimately enter a death spiral and progressively approach the brink of collapse.130 Following this event, crypto lending company Celsius ultimately suspended withdrawals on June 13 due to its usage of on-chain leverage and the derivative stETH. A few days later, Celsius applied for bankruptcy protection. Due to its significant holdings in GBTC and stETH, Three Arrows Capital also requested federal bankruptcy protection on July 2, using the Luna incident as the catalyst. In addition, the incident prompted Three Arrows’ creditor, Voyager Digital, to declare bankruptcy after suffering significant losses due to Three Arrows’ failure on a 670 million debt.131 According to Hodlnaut’s financial report as of August 8, the company had a funding gap of around 193 million. Its outstanding debt was 391 million Singapore dollars when its assets were valued as 122 million, or about 281 million Singapore dollars when its assets were valued as 88 million (https://finance.yahoo.com/news/hodlnaut-owes-us-200-mln-070407468.html). The massive funding shortfall forced the platform to suspend trading.

Figure 7.

FTX failure and related events (all taking place in 2022)

At the beginning of November, the disclosure of a massive hole in the financial sheet of cryptocurrency market maker Alameda intensified the panics in the cryptocurrency market. The bitcoin exchange FTX experienced a liquidity issue—large withdrawals due to social panic increase as the panic grew. When Coin An, the company that was going to purchase FTX, stated that it was pulling out of the agreement on November 9, FTX went into a complete meltdown. FTX declared bankruptcy on November 11.132 The demise of FTX also influenced the cryptocurrency market. Due to the issue at creditor FTX, BlockFi did not choose to exit, but unfortunately, on November 28, sought bankruptcy protection. Due to the demise of FTX and cash flow issues, cryptocurrency brokerage Genesis asked for a 1 billion emergency loan on April 14 and ceased accepting withdrawals on April 16. Genesis on November 21 claimed "no immediate plans to file for bankruptcy" and that as of December 8, it was still in the recovering period.133

The main cryptocurrencies

Cryptocurrency is a digital currency created based on a specific encryption algorithm. It is an open-source blockchain technology architecture, which enables to generate, manage, exchange, circulate and even destroy divisible digital units according to a certain logic according to complete user management.134 Such digital units are also generally called points, tokens, coins, tokens, or cryptocurrencies.

In 2009, when Bitcoin first became available, it had virtually no rivals. However, by 2011, new varieties of cryptocurrencies had begun to appear. There are currently tens of thousands of distinct cryptocurrency varieties. The top 10 cryptocurrencies (See Table 6 134) by market capitalization by March 3, 2023, are shown below (https://www.investing.com/crypto/currencies):

-

•

Bitcoin (BTC): The first cryptocurrency developed in 2009 is called Bitcoin. It utilizes blockchain technology and is decentralized and independent of all governments and central banks. More than 18.8 million Bitcoin tokens were in use as of September 2021, with a limit of 21 million.

-

•

Ethereum (ETH): Ethereum is also a blockchain network, much like Bitcoin. ETH is created with a proof-of-work algorithm as well. However, unlike Bitcoin, there is no upper limit for the creation of ETH.

-

•

Tether Coin (USDT): The USDT is the cryptocurrency pegged to the USD dollar, which also invests in the blue. Users can use SWIFT to transfer money to Tether provided bank accounts or the Bitfinex exchange to convert their money to USDT.

-

•

Binance Coin (BNB): The total amount issued is still 200 million. BNB is an Ethereum-based decentralized blockchain digital asset created by Ethereum.

-

•

USD Coin (USDC): USD coin (USDC) is a stablecoin that runs on the Ethereum blockchain and other blockchains. Its 1:1 parity with the dollar makes USDC a reliable medium of trade. The purpose of stablecoins like USDC is to facilitate quicker and less expensive transactions.

-

•

XRP: Ripple LABS is the company behind XRP. XRP cannot be mined, unlike Bitcoin and many other cryptocurrencies. Instead, there is a limited supply of it. XRP transactions are cheaper and faster than Bitcoin transactions due to the Ripple network’s transaction verification method.

-

•

ADA: The blockchain platform used by ADA, called Cardano, is a member of the third generation of blockchain platforms. Due to its reliance on reliable evidence (PoS), Cardano’s network may be more effective and durable because it does not require the intricate PoW computations and substantial power consumption necessary to mine coins like Bitcoin.

-

•

Polygon (MATIC): MATIC is an Indian blockchain scalability platform dubbed “Ethereum’s Internet of Blockchains” that aspires to build a multi-chain ecosystem of Ethereum-compatible blockchains.

-

•

Dogecoin: Dogecoin was introduced in 2013 and uses a PoW mechanism to operate on the blockchain network, much like Bitcoin and Ethereum. However, the total amount of coins that may be mined is limitless compared to Bitcoin’s 21 million coin restriction.

-

•

Binance USD (BUSD): A stable asset backed by USD that is listed and traded on Binance issued and managed by Paxos Trust Company, and subject to New York State Department of Financial Services regulation.

Table 6.

Information of major cryptocurrencies

| Names | Codes | Price (USD) | Value | Volume (24h) | Proposed time |

|---|---|---|---|---|---|

| Bitcoin | BTC | 22370.8 | 432.52B | 26.19B | 2009 |

| Ethereum | ETH | 1565.29 | 191.84B | 9.76B | 2013 |

| Tether coin | USDT | 1.0002 | 71.14B | 38.07B | 2014 |

| Binance coin | BNB | 290.51 | 45.99B | 466.23M | 2017 |

| USD Coin | USDC | 0.9996 | 43.17B | 4.33B | 2018 |

| XRP | XRP | 0.36601 | 18.78B | 1.06B | 2013 |

| Ada coin | ADA | 0.3367 | 11.67B | 388.80M | 2015 |

| Polygon | MATIC | 1.166 | 10.19B | 544.08M | 2017 |

| Dogecoin | DOGE | 0.075592 | 10.03B | 531.91M | 2013 |

| Binance USD | BUSD | 0.9997 | 9.68B | 7.85B | 2019 |

Deep learning in cryptocurrency

In this section, we comprehensively review the application of deep learning methods in cryptocurrency research across multiple modeling tasks, including price prediction, portfolio construction, bubble analysis, abnormal trading and initial coin offering.

Cryptocurrency price prediction

A variety of deep learning algorithms have been applied in the prediction of cryptocurrency prices. Ryotaro et al.8 used many machine learning algorithms ANN, SVM, LSTM, Ridge Regression, Heterogeneous Autoregressive model Realized Volatility (HARRV) and other models for comparative analysis. Among them, the prediction model based on LSTM has received a lot of attention and extension. Abdullah Ammer & Aldhyani137 found that LSTM has an accurate and good effect on the prediction of cryptocurrency after empirical studies in different periods; Fang et al.142 used LSTM model to present the characteristics of real-time tick data in cryptocurrency trading system and analyzed the trade-off between model accuracy and training frequency.

Hybrid models based on LSTM have gradually developed. First, D’Amato et al.138 combined RNN-Jordan neural network and LSTM to predict cryptocurrency price volatility, which verified that the model can provide more vital prediction ability; Based on the hybrid prediction model of RNN and LSTM, Kumari Priya et al.139 focused on analyzing how LSTM network upgraded traditional algorithms in the field of price prediction. Tanwar et al.141 considered the interdependence between parent currencies and adopted the hybrid model of GRU and LSTM to better predict the price of litecoin. Parekh et al.143 proposed a hybrid and robust model DL-Gues considering the interdependence between cryptocurrencies and market sentiment; Hansun et al.140 compared three commonly used deep network structures, namely LSTM, BiLSTM and GRU, using multiple prediction model methods, and found that the latter two could provide similar robust and accurate predictions.

In addition, considering the practical problems related to investment, Kim et al.144 proposed to construct a SAM (Segment Anything Model)-LSTM model based on an attention mechanism to predict the price trend of bitcoin, which is composed of several LSTM modules for on-chain variable groups and the attention mechanism. Park & Seo145 proposed an LSTM model and input features, including sellProfit (the profit that can be obtained when selling a specific amount of cryptocurrency), buyProfit (the profit that can be obtained when buying a specific amount of cryptocurrency) and maxProfit (the maximum profit that can be obtained between sellProfit and buyProfit) to help investors make investment decisions. In the first stage, the LSTM network is used to extract structured information from financial news, and in the second stage, a machine learning model with structured financial news input is employed to predict bitcoin prices. Luo et al.,146 considering the multi-scale properties of cryptocurrency prices, matched different machine learning algorithms like LSTM and Extreme Learning Machines (ELM). with the corresponding multi-scale components and built an integrated prediction model based on machine learning and multi-scale analysis.

Regarding other deep learning methods, Schnaubelt148 applied deep reinforcement learning to optimize limit order configuration on cryptocurrency exchanges. Lahmiri & Bekiros 10 applied deep feedforward neural network (DFFNN) to analyze and forecast high-frequency price data of bitcoin. Akyildirim et al.150 used ANN, SVM, Random Forest and Logistic Regression to analyze the predictability of the 12 most liquid cryptocurrencies. Jana et al.151 proposed a regression framework based on differential evolution to predict the one-day price of bitcoin based on the fusion of MLP, Random Forest, Support vector regression(SVR) and other algorithms. In particular, considering the epidemic’s impact, Ftiti et al.152 developed the HAR model to measure price volatility based on various deep learning algorithms. Oyedele et al.149 used relevant performance indicators to evaluate and benchmark the performance of CNN, DFFNN and gated recurrent unit (GRU) models based on Boosted Tree. From the studies mentioned above, we can conclude that the price prediction for various cryptocurrencies has been conducted using a wide range of deep learning algorithms. The most recent research has improved the prediction accuracy and efficiency by combining various algorithmic techniques (See Tables 7 and 8).

Table 7.

Research on cryptocurrency price prediction literature (1)

| Models | Data | Results | Innovation | References |

|---|---|---|---|---|

| ANN, LSTM, SVM, HARRV, Ridge regression |

Minute sampling of bitcoin returns over 3-h intervals | The ridge regression model performs best, supporting the assumption of autoregressive dynamics of the HARRV model. | A variety of deep learning algorithms are applied, and the prediction findings are used for dynamic risk hedging | Miura et al.8 |

| LSTM | It contains data from 2013 to 2018 for five cryptocurrencies including bitcoin. | The root-mean-square error of the model prediction results is small, and good accuracy is achieved | The LSTM is trained to learn and forecast the highest price for a future time using the highest price of Bitcoin on past dates. | Mittal and Bhatia135 |

| LSTM | From 7 December 2020 to 26 September 2021 USDP,BTG, OKB, TEL, AUDIO | Both LSTM and a single network integration based on LSTM can provide relatively accurate prediction of cryptocurrency. | Using LSTM and a single network ensemble based on LSTM to compare the returns on investment of these cryptocurrencies | Buyrukoğlu136 |

| LSTM | AMP, Ethereum, EOS, and XRP from May 2015 to April 2022 | LSTM has the most superior performance. | The implementation of a novel deep learning technique based on LSTM yields | Ammer and Aldhyani137 |

| RNN—Jordan, SETAR | Bitcoin, Ripple, and Ethereum | RNN-Jordan method better reflects the high volatility of cryptocurrencies. | By capturing complicated data interactions, it outperforms conventional methods in terms of accuracy. | D’Amato et al.138 |

| RNN, LSTM | Bitcoin | The model takes into account crucial information from the past, and the suggested model performs better and is more effective. | The price of any cryptocurrency is predicted in this research using a hybrid RNN and LSTM prediction model. | Priya et al.139 |

| RNN, LSTM | Bitcoin, Ethereum, Cardano, T-Ether, and Binance | BiLSTM and GRU have similar performance results in terms of accuracy | Multivariate forecasting models were used, while the process robustness was assessed through different RNN models | Hansun et al.140 |

| GRU, LSTM | Litecoin and Zcash | Hybrid models based on GRU and LSTM can be used in real-time scenarios and are well trained and evaluated using standard datasets. | The suggested model incorporates emotional aspects and takes into account how parent currencies are interdependent. | Tanwar et al.141 |

| RMSprop, LSTM |

Real-time tick data in cryptocurrency trading systems | Models that are more effective than those of individual assets due to the generic properties of cryptocurrencies also find a trade-off between model accuracy and training frequency. | The characteristics of the cryptocurrency market in a high-frequency environment are analyzed and presented | Fang et al.142 |

| DL-GuesS, GRU, LSTM, VADER |

Historical prices of Dash, Litecoin, and Bitcoin | The proposed DL-GuesS outperforms traditional systems in predicting cryptocurrency prices. | Proposed DL-GuesS model considering price history and recent Twitter sentiment. | Parekh et al.143 |

Table 8.

Research on cryptocurrency price prediction literature (2)

| Models | Data | Results | Innovation | References |

|---|---|---|---|---|

| CPD-Attention mechanism, SAM-LSTM |

BTC prices from March 27, 2018 to November 16, 2021 | The model enables price prediction models to predict unseen price ranges. | A SAM-LSTM-based prediction model is proposed | Kim et al.144 |

| LSTM | BTC, ETH, ADA, DASH, LTC, and XMR | The proposed model’s accurate response percentage has increased by roughly 13%–21%, according to experimental findings, which has significantly enhanced performance. | A deep learning model containing sellProfit, buyProfit, and maxProfit input features is presented with a criterion for which action is most beneficial at any given time. | Park and Seo145 |

| LSTM, Extreme learning machine |

The bitcoin price series from 2017/11/24 to 2020/4/21 and 2020/4/22 to 2020/11/27 are used as training and prediction datasets. | The prediction accuracy of the integrated model can reach 95.12%. | Multi-scale components to create an integrated prediction model based on machine learning and multi-scale analysis, taking into account the multi-scale features of bitcoin values. | Luo et al.146 |

| LSTM, CNN, Random forest | 980 news articles containing bitcoin between June 6, 2011 and May 13, 2019 | The proposed forecasting system produces a substantially greater time-out rate of return than the buy-and-hold approach. | By applying the LSTM network to sentiment analysis | Jakubik et al.147 |

| DRL | Currency pairs BTC/USD, ETH/USD, ETH/BTC from January 1, 2018 to June 30, 2019 | When compared to the execution of a single market order, the model produces a better order placement strategy that lowers the average total under execution by 37.71% | apply deep reinforcement learning to the optimal limit order placement problem | Schnaubelt148 |

| DFFNN | High frequency dataset of Bitcoin intraday price data from January 1, 2016 to March 16, 2018 | The proposed algorithm has advantages in terms of prediction accuracy. | Three distinct training strategies for deep feedforward neural networks are evaluated | Lahmiri et al.10 |

| CNN, Boosted trees, DFFNN, GRU |

BTC, ETH,BNB, LTC, XLM, and DOGE data from January 1, 2018 to December 31, 2021 | The CNN model gave a consistent and high explained variance score (on average) of 0.97 and had the minimum mean percentage error (0.06). |

Study performance evaluation using improved tree-based methods and DL genetic algorithms to forecast closing prices of various cryptocurrencies. | Oyedele et al.149 |

| ANN, SVM, Random forest, logistics regression | From April 1, 2013 to June 23, 2018, BCH, BTC,DSH, EOS, ETC, ETH, IOT, LTC, OMG, XMR, XRP and ZEC | There is some predictability of price trends in the cryptocurrency market, as evidenced by the average categorization accuracy of the algorithms being regularly over the 50% cutoff. | using ANN, SVM, RL, and logistic regression techniques, with past price data and technical indications serving as model features. | Akyildirim et al.150 |

| MLP, SVR, Random forest |

Bitcoin data from January 10, 2013 to February 23, 2019 | In both static and dynamic forecasting instances, the suggested method statistically outperforms all other competing models. | A regression framework based on differential evolution is proposed to predict the day-ahead price of bitcoin | Jana et al.151 |

| HAR model | Bitcoin, Ethereum, ETC, and XRP data from April 2018 to June 2020 | Times of crisis, especially the coronavirus disease pandemic, increase the volatility of cryptocurrency volatility. | Use high-frequency data and the HAR model to validate investors’ sensitivity to unfavorable news in chaotic periods. | Ftiti et al.152 |

Cryptocurrency portfolio construction

Deep learning methods have also been widely employed in cryptocurrency portfolio construction, especially portfolio management based on the DRL model.15,154,153 For example, Estalayo et al.155 allocated cryptocurrency portfolios around a combination of deep learning (DL) models and multi-objective evolutionary algorithms (MOEA) and, using its predictive ability, made accurate ex ante estimates of portfolio returns and risks. Sockin & Xiong215 facilitated decentralized bilateral trading of certain goods or services between cryptocurrency users across asset allocations using blockchain technology.

LSTM models have also been widely employed in cryptocurrency portfolio research. Osifo & Bhattacharyya156 compared the LSTM, autoregressive integrated moving average(ARIMA), moving average(MA), cumulative moving average (CMA), artificial neural networks (ANN) models in the risk control of pair trading in the cryptocurrency space. Gu et al.157 used LSTM to learn the temporal information of historical transactions and make price predictions. Aguayo Moreno & Garcia Medina158 constructed LSTM and GARCH hybrid models and found that deep learning models, including LSTM and MLP algorithms, and their different variables could better reduce the value at risk and enhance capital allocation for the uniform portfolio. Hashemkhani Zolfani et al.161 used return forecasts obtained in autoregressive integrated moving average (ARIMA), long short-term memory (LSTM) and random forest regression (RFR) models as return-related criteria, based on PROMETHEE II,A cryptocurrency portfolio allocation model is proposed. Current literature generally uses the DRL model to construct portfolios in the cryptocurrency market with an optimized investment performance. In addition, the involved studies focus on the diversification of portfolio risks (See Tables 9 and 10).

Table 9.

Research on cryptocurrency portfolio construction (1)

| Models | Data | Results | Innovation | References |

|---|---|---|---|---|

| CNN, DRL | 12 most traded cryptocurrency assets | The performance of the model strategy is compared to three benchmarks and three other portfolio management algorithms with positive results. | In this paper, we propose a model-free convolutional neural network that takes the historical prices of a group of financial assets as input and outputs the weights of this portfolio. | Jiang and Liang15 |