Abstract

Background

Little is known about hospital pricing for coronary artery bypass grafting (CABG). Using new price transparency data, we assessed variation in CABG prices across US hospitals and the association between higher prices and hospital characteristics, including quality of care.

Methods and Results

Prices for diagnosis related group code 236 were obtained from the Turquoise database and linked by Medicare Facility ID to publicly available hospital characteristics. Univariate and multivariable analyses were performed to assess factors predictive of higher prices. Across 544 hospitals, median commercial and self‐pay rates were 2.01 and 2.64 times the Medicare rate ($57 240 and $75 047, respectively, versus $28 398). Within hospitals, the 90th percentile insurer‐negotiated price was 1.83 times the 10th percentile price. Across hospitals, the 90th percentile commercial rate was 2.91 times the 10th percentile hospital rate. Regional median hospital prices ranged from $35 624 in the East South Central to $84 080 in the Pacific. In univariate analysis, higher inpatient revenue, greater annual discharges, and major teaching status were significantly associated with higher prices. In multivariable analysis, major teaching and investor‐owned status were associated with significantly higher prices (+$8653 and +$12 200, respectively). CABG prices were not related to death, readmissions, patient ratings, or overall Centers for Medicare and Medicaid Services hospital rating.

Conclusions

There is significant variation in CABG pricing, with certain characteristics associated with higher rates, including major teaching status and investor ownership. Notably, higher CABG prices were not associated with better‐quality care, suggesting a need for further investigation into drivers of pricing variation and the implications for health care spending and access.

Keywords: coronary artery bypass surgery, coronary artery disease, health care spending, price transparency, price variation

Subject Categories: Health Services, Quality and Outcomes, Disparities, Cost-Effectiveness, Chronic Ischemic Heart Disease

Nonstandard Abbreviations and Acronyms

- CMS

Centers for Medicare and Medicaid Services

Research Perspective.

What Is New?

Leveraging recent legislation mandating the release of hospital‐reported commercial prices, we demonstrate a nearly 2‐fold pricing variation within hospitals and a 3‐fold variation between hospitals for coronary artery bypass grafting hospitalizations.

Prices varied significantly by geography, teaching status, and investor ownership, among other hospital characteristics, but were not associated with either coronary artery bypass grafting–specific or hospital‐wide outcomes, including 30‐day mortality and readmission rates.

What Question Should Be Addressed Next?

Given that higher coronary artery bypass grafting prices were not associated with higher quality of care, subsequent research should seek to further elucidate hospital‐ and insurer‐level factors predictive of prices and identify opportunities for policy to reduce pricing variation not tied to outcomes.

Payment for hospital services in the United States remains poorly characterized. While Medicare has a national episode‐based payment system, with published prices, the prices paid by commercial health insurance payers have been considered confidential. In 2021, the Centers for Medicare and Medicaid Services (CMS) issued new price transparency guidelines requiring hospitals to provide detailed pricing information for the first time. 1 Here, price is the amount negotiated by the insurance company, which includes the payment from the insurance company to the hospital and any coinsurance payments for patients. The regulation aimed to provide greater transparency into health care prices for patients, payers, and regulators.

Since the enactment of the new price transparency legislation, multiple studies have documented substantial variation in payer‐negotiated prices across a broad spectrum of medical services, including diagnostics, procedures, and prescription drugs. 2 , 3 , 4 , 5 , 6 However, little has been published in the cardiovascular field, despite its contribution to overall US health care spending. Oseran et al surveyed a limited selection of 20 top‐ranked US hospitals and found large price differences across routine outpatient cardiovascular tests such as echocardiography and angiography. 7 Wei et al expanded the scope of the analysis to include all reporting hospitals nationwide for echocardiography and additionally assessed hospital factors influencing price variation. 8 However, insurer‐negotiated prices for inpatient cardiovascular care remains understudied. Furthermore, important questions remain unanswered about the association between price and quality of care. The association between cardiovascular quality of care measures with the price of care is a critical question.

Coronary artery bypass grafting (CABG) is a cornerstone in the management of coronary artery disease. In 2019, there were 160 000 isolated CABG surgeries, with 60 000 paid for by Medicare (amounting to >$12 billion) and ≈100 000 reimbursed by commercial insurance plans. 9 , 10 Because CABG is a common and high‐cost procedure, it is important to understand how the price for CABG varies across hospitals and how this variation relates to quality of care.

Using a database of listed hospital prices, we evaluated the variation in CABG prices within and across hospitals. We further compared commercial and self‐pay prices relative to Medicare payments. Finally, we evaluated the association of CABG pricing with hospital characteristics and quality‐of‐care metrics.

Methods

Data

The 2021 Hospital Price Transparency Rule required all US hospitals to release a publicly available, machine‐readable file containing prices for medical services, including chargemaster, self‐pay, and commercial rates. We extracted hospital price data from the Turquoise Health database, a commercial data source containing aggregated pricing information from 6378 hospitals. 11 This study was deemed exempt by the Stanford Institutional Review Board as it involved analysis of publicly available, deidentified data. The data that support the findings of this study are available from the corresponding author upon reasonable request.

CABG Price and Hospital Characteristics

We used prices for diagnosis related group code 236 (CABG without percutaneous transluminal coronary angioplasty without major cardiac complications) given that this is the most frequent CABG diagnosis related group across Medicare (33% of discharges attributable to diagnosis related groups 231–236). 9 The data were queried on January 5, 2023, and reflect cross‐sectional pricing data compiled from 2021 to 2022. Hospitals with the following identifiers were excluded: psychiatric, children's, imaging center, rehabilitation, Department of Defense, and Veterans Affairs. We also excluded hospitals with <2000 overall discharges annually.

Compliant hospitals were those with price data available in the database in an analyzable format, and noncompliant hospitals were those that did not have formatted price data in the database.

We enriched the pricing data from Turquoise Health with hospital and geographic characteristics as previously described (see Table S1 for details). 8 , 12 , 13 , 14 , 15 , 16 , 17 , 18 , 19 , 20 , 21 , 22 In brief, categorical hospital characteristics included major teaching status (defined as membership in the Council of Teaching Hospitals and Health Systems), US census‐based division, major investor ownership, hospital type, rurality, and disproportionate share hospital status. Continuous chararacteristics included inpatient total revenue, annual inpatient discharges, total hospital beds, total system beds, and hospital referral region beds per 1000 people. Data on health care prices, spending, usage, and socioeconomic vulnerability across US government‐designated Core‐Based Statistical Areas was sourced from the Health Care Cost Institute Healthy Marketplace Index. 22 Data on market concentration as measured by the Herfindahl–Hirschman Index were also sourced from the Health Care Cost Institute.

Quality metrics were extracted from the CMS Hospital Compare database. This included the CMS hospital overall rating score, the Hospital Consumer Assessment of Healthcare Providers and Systems patient hospital rating score, post‐CABG risk‐adjusted 30‐day mortality and readmission rates, and hospital‐wide postdischarge risk‐adjusted 30‐day mortality and readmission rates. Readmission and mortality rates were standardized and were analyzed as categorical variables on the basis of their official statistical comparison to the national average (better, no different, or worse than the national average). 23

Statistical Analysis

Descriptive statistics were used to characterize the hospitals, while comparison of characteristics between compliant and noncompliant hospitals was performed using the chi‐square test (Table S2). Variation in median commercial price within hospitals was assessed by calculating the ratio between the 90th and 10th percentile payer‐negotiated rate (within‐hospital ratio). 8 Variation across hospitals was calculated by dividing the national 90th percentile hospital rate by the 10th percentile hospital rate (between‐hospital ratio). 24 To minimize the impact of outliers, prices were Winsorized below the first percentile and above the 99th percentile.

Association between median commerical price per hospital and hospital factors was assessed via the Kruskal–Wallis test for categorical variables. To evaluate the association between continuous variables and CABG prices, we evaluated the Spearman rank correlation and used linear regression to estimate the association between a 1 SD change in the standardized continuous variable and CABG price. The hospital was the unit of analysis for both the categorical and continuous tests of association.

A multivariable linear regression model was generated on the basis of hospital characteristics meeting a P value threshold of <0.1 on univariate analysis and preselected variables of interest. To minimize collinearity, factors found to be associated with each other (P<0.05 on Fisher's exact test for categorical covariates and r>0.5 for continuous covariates) were filtered to include only the one most correlated with the outcome variable. The final variable list included major teaching status, investor ownership, disproportionate share hospital status, annual inpatient admissions, total system beds, hospital referral region hospital beds per 1000 people, Herfindahl–Hirschman Index, and socioeconomic vulnerability index.

To assess the impact of quality of care on the aforementioned characteristics, a second multivariable model was generated including CABG‐specific and hospital‐wide outcome measures, which were treated as predictors: 30‐day CABG readmission rate, 30‐day CABG mortality rate, 30‐day hospital wide readmission rate, 30‐day hospital‐wide mortality rate, Hospital Consumer Assessment of Healthcare Providers and Systems patient hospital rating, and CMS hospital rating. For a detailed breakdown of the covariates tested in the univariate and multivariable analysis, see Table S1.

Statistical analyses were performed using R Version 4.1.1 (R Foundation for Statistical Computing, Vienna, Austria) and Prism Version 9.4.0 (GraphPad Software, San Diego, CA). A P value of <0.05 was considered statistically significant for 2‐sided comparisons. A standardized mean difference of >0.10 was considered meaningful. 25

Results

Reporting Hospital Characteristics

Among 6378 hospitals in the Turquoise database, 1038 offered CABG and 544 were compliant with price transparency requirements (52.4%) (see Figure S1 for cohort creation process). Reporting hospitals differed from nonreporting hospitals across multiple characteristics (Table S2). Nonteaching hospitals, smaller hospitals, and hospitals earning less revenue were more likely to be noncompliant, while hospitals that were for‐profit, investor owned, rural, and higher revenue were more likely to be compliant.

CABG Price Variation

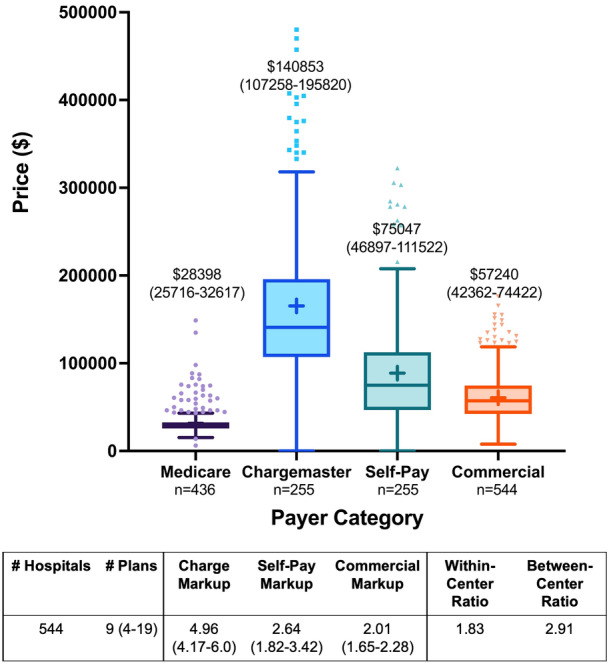

There was significant variation in price across payer categories, with chargemaster, self‐pay, and commercial rates being 4.96, 2.64, and 2.01 times the Medicare rate, respectively (Figure). The median within‐hospital ratio of the 90th and 10th percentile payers in CABG commercial price was 1.83 (interquartile range, 1.33–2.60). The ratio of prices between the 90th and 10th percentile hospital nationally was 2.91. Prices varied substantially across census regions, with the lowest and highest median prices corresponding to the East South Central and Pacific regions, respectively ($35 624 versus $84 080).

Figure 1. Comparison and variation of CABG prices across payers.

CABG indicates coronary artery bypass grafting.

Association Between Hospital and Regional Characteristics and CABG Price

Factors significantly associated with higher commercial CABG rates included higher total inpatient revenue ($285 per $100 million; P<0.01), more annual inpatient discharges ($231 per 1000 discharges; P<0.01), and major teaching status (+$4431; P=0.01) (Table 1). Investor‐owned hospitals had higher prices, but this result did not achieve statistical significance (+$7096; P=0.06). For‐profit status (P=0.65), urban locality (P=0.55), number of hospital beds (P=0.06), and number of health system beds (P=0.33) were not significantly associated with price. Among regional factors, health care spending and health care pricing were significantly associated with higher CABG prices, whereas higher regional health care usage was associated with lower prices. Higher numbers of hospital beds per 1000 people within a hospital referral region was associated with lower prices (−$8060 per 1000 people; P<0.01). There was no association between CABG price and regional socioeconomic vulnerability or market concentration as measured by Herfindahl–Hirschman Index.

Table 1.

Univariate Analysis of Factors Associated With CABG Commercial Price

| Hospital categorical factors | No. of hospitals | Median price | IQR | P value |

|---|---|---|---|---|

| Teaching status | ||||

| Major teaching | 114 | 60 809 | 46 546–79 183 | 0.01 |

| Not major teaching | 430 | 56 378 | 41 197–71 313 | |

| Region | ||||

| New England | 16 | 57 386 | 40 557–70 139 | <0.01 |

| Middle Atlantic | 70 | 52 773 | 43 082–72 398 | |

| South Atlantic | 100 | 64 287 | 54 103–80 299 | |

| East North Central | 123 | 61 695 | 45 138–75 183 | |

| East South Central | 26 | 35 624 | 30 463–52 551 | |

| West North Central | 49 | 49 876 | 39 563–59 977 | |

| West South Central | 125 | 46 139 | 39 283–63 020 | |

| Mountain | 15 | 75 747 | 73 085–85 014 | |

| Pacific | 19 | 84 080 | 63 763–95 672 | |

| Major investor owned | ||||

| Major investor owned | 95 | 63 020 | 43 175–78 252 | 0.06 |

| Not major investor owned | 449 | 55 924 | 41 699–72 128 | |

| Hospital type | ||||

| For‐profit | 104 | 62 618 | 41 650–77 296 | 0.65 |

| Not‐for‐profit | 385 | 55 969 | 41 621–72 128 | |

| Government | 49 | 59 611 | 45 938–75 203 | |

| Urban/rural | ||||

| Urban | 524 | 56 970 | 42 373–73 671 | 0.55 |

| Rural | 19 | 62 219 | 41 265–85 420 | |

| DSH | ||||

| DSH | 476 | 58 237 | 42 732–75 364 | 0.12 |

| Not DSH | 68 | 49 696 | 41 311–68 583 | |

| Hospital continuous factors | No. of hospitals | Regression coefficient±SE | Spearman P value | Correlation coefficient (r) |

|---|---|---|---|---|

| Inpatient total revenue (per $100 million) | 536 | 285±67 | <0.01 | 0.22 |

| Annual inpatient discharges (per 1000) | 536 | 231±81 | <0.01 | 0.13 |

| Total hospital beds (per 100) | 544 | 884±368 | 0.06 | 0.08 |

| Total system beds (per 1000) | 532 | 416±108 | 0.33 | −0.04 |

| HRR hospital beds per 1000 | 544 | −8060±2365 | <0.01 | −0.20 |

| CBSA health care price index | 434 | 50 349±8482 | <0.01 | 0.30 |

| CBSA health care spending index | 434 | 46 941±9877 | <0.01 | 0.26 |

| CBSA health care usage index | 434 | −18 685±8583 | 0.03 | −0.10 |

| CBSA socioeconomic vulnerability index | 434 | 86±6690 | 0.67 | 0.02 |

| HHI market concentration (per 1000) | 434 | −556±982 | 0.17 | −0.07 |

| Hospital‐wide outcomes | No. of hospitals | Median price | IQR | P value |

|---|---|---|---|---|

| CMS hospital‐wide mortality rate | ||||

| Better than national average | 132 | 55 495 | 43 224–75 310 | 0.19 |

| Same as national average | 287 | 55 924 | 41 585–71 260 | |

| Below national average | 107 | 61 525 | 43 192–80 283 | |

| CMS hospital‐wide readmission | ||||

| Better than national average | 239 | 59 246 | 43 017–75 174 | 0.26 |

| Same as national average | 46 | 51 384 | 44 108–65 095 | |

| Below national average | 241 | 56 387 | 41 140–75 362 | |

| HCAHPS patient hospital rating | ||||

| 1 | 13 | 60 900 | 35 690–77 741 | 0.30 |

| 2 | 113 | 55 174 | 39 609–73 353 | |

| 3 | 295 | 57 042 | 42 744–75 291 | |

| 4 | 111 | 58 413 | 44 661–73 370 | |

| 5 | 2 | 36 631 | 36 469–36 793 | |

| CMS overall hospital rating | ||||

| 1 | 28 | 62 163 | 53 563–82 491 | 0.02 |

| 2 | 105 | 54 933 | 39 612–75 203 | |

| 3 | 159 | 53 154 | 39 697–67 913 | |

| 4 | 167 | 59 350 | 43 726–78 306 | |

| 5 | 79 | 58 062 | 44 035–76 833 | |

| CABG outcomes | No. of hospitals | Regression coefficient±SE | Spearman P‐value | Correlation coefficient (r) |

|---|---|---|---|---|

| CMS CABG 30‐d mortality rate | 463 | −1293±1231 | 0.15 | −0.07 |

| CMS CABG 30‐d readmission rate | 461 | 616±1220 | 0.92 | <0.01 |

CABG indicates coronary artery bypass grafting; CBSA, core‐based statistical area; CMS, Centers for Medicare and Medicaid Services; DSH, disproportionate share hospital; HCAHPS, Hospital Consumer Assessment of Healthcare Providers and Systems; HHI, Herfindahl–Hirschman Index; HRR, hospital referral region; and IQR, interquartile range.

In the multivariable analysis, investor ownership was associated with higher CABG price: +$16 490 (P<0.01) and +$8872 (P=0.05) with and without adjustment for hospital quality‐of‐care measures, respectively (Tables 2 and 3). Major teaching hospitals also had significantly higher CABG prices: +$8961 (P=0.01) and +$9531 (P<0.01) with and without adjustment for other hospital characteristics and quality measure performance. Each additional 1000 annual inpatient discharges was associated with a $263 increase in CABG price (P=0.03) after all adjustments.

Table 2.

Multivariable Associations Between Hospital and Regional Characteristics and CABG Price

| Hospital/health system factors (n=544) | Estimate±SE* | 95% CI | P value |

|---|---|---|---|

| Region | |||

| New England | Reference | ||

| Middle Atlantic | 14 410±8151 | −5972 to 30 433 | 0.08 |

| South Atlantic | 20 670±8288 | −1614 to 36 967 | 0.01 |

| East North Central | 19 870±8065 | 4380 to 35 724 | 0.01 |

| East South Central | −1640±9924 | 4012 to 17 869 | 0.87 |

| West North Central | 10 420±8693 | −21 149 to 27 510 | 0.23 |

| West South Central | 6203±8887 | −6669 to 23 675 | 0.49 |

| Mountain | 29 460±11 680 | −11 269 to 52 427 | 0.01 |

| Pacific | 34 010±10 710 | 6495 to 55 073 | <0.01 |

| Major teaching (Reference: not major teaching) | 9531±3373 | 2900 to 16 163 | <0.01 |

| Major investor owned (Reference: not investor owned) | 8872±4512 | 1 to 17 742 | 0.05 |

|

DSH Abbreviations: (Reference: Not DSH) |

1239±3668 | −5972 to 8450 | 0.74 |

| Annual inpatient discharges (per 1000) | 274±109 | 59 to 489 | 0.01 |

| Total system beds (per 1000) | 58±156 | −249 to 364 | 0.71 |

| HRR hospital beds per 1000 (per 1 bed) | −2306±3646 | −9115 to 4503 | 0.51 |

| Herfindahl–Hirschman Index | 5250±10 310 | −1501 to 2552 | 0.61 |

| Socioeconomic vulnerability index | 8717±8945 | −8868 to 26 302 | 0.33 |

Regression coefficient±standard error.

DSH indicates disproportionate share hospital; and HRR, hospital referral region.

Table 3.

Multivariable Associations Between Hospital and Regional Characteristics and CABG Price Including Hospital‐Wide and CABG‐Specific Outcomes

| Outcomes (n=544) | Estimate±SE* | 95% CI | P value |

|---|---|---|---|

| Hospital 30‐day mortality rate | |||

| Better than national average | Reference | ||

| Same as national average | 3813±4651 | −5338 to 12 964 | 0.41 |

| Below national average | 3804±3387 | −2859 to 10 467 | 0.26 |

| Hospital 30‐day readmission | |||

| Better than national average | Reference | ||

| Same as national average | −2872±3158 | −9085 to 3342 | 0.36 |

| Below national average | −4121±4996 | −13 949 to 5707 | 0.41 |

| CABG 30‐d mortality rate | −583±1416 | −3368 to 2203 | 0.68 |

| CABG 30‐d readmission rate | 1155±1382 | −1564 to 3874 | 0.40 |

| CMS overall hospital rating | |||

| 1 | Reference | ||

| 2 | −6242±6183 | −18 406 to 5921 | 0.31 |

| 3 | −10 390±6296 | −22 776 to 1997 | 0.10 |

| 4 | 125±6844 | −13 340 to 13 589 | 0.99 |

| 5 | −11 950±8028 | −27 743 to 3844 | 0.14 |

| HCAHPS patient hospital rating | |||

| 1 | Reference | ||

| 2 | 7819±9440 | −10 752 to 26 390 | 0.41 |

| 3 | 12 320±9446 | −6267 to 30 901 | 0.19 |

| 4 | 16 120±9703 | −2964 to 35 213 | 0.10 |

| 5 | 22 020±13 540 | −4616 to 48 655 | 0.10 |

| Region | |||

| New England | Reference | ||

| Middle Atlantic | 13 200±8714 | −3945 to 30 341 | 0.13 |

| South Atlantic | 17 860±8980 | 193 to 35 526 | 0.05 |

| East North Central | 20 090±8613 | 3144 to 37 031 | 0.02 |

| East South Central | −2874±10 760 | −24 034 to 18 286 | 0.79 |

| West North Central | 7536±9508 | −11 169 to 26 242 | 0.43 |

| West South Central | −512±9774 | −19 740 to 18 716 | 0.96 |

| Mountain | 25 350±12 760 | 253 to 50 452 | 0.05 |

| Pacific | 34 890±11 450 | 12 363 to 57 422 | <0.01 |

| Major teaching (reference: not major teaching) | 8961±3654 | 1773 to 16 148 | 0.01 |

| Major investor owned (reference: not investor owned) | 16 490±5482 | 5705 to 27 275 | <0.01 |

| DSH (reference: not DSH) | −2432±4403 | −11 094 to 6229 | 0.58 |

| Annual inpatient discharges (per 1000) | 263±121 | 25 to 502 | 0.03 |

| Total system beds (per 1000) | −8±18 | −362 to 345 | 0.96 |

| HRR hospital beds per 1000 (per 1 bed) | −742±3900 | −8414 to 6930 | 0.85 |

| Herfindahl–Hirschman Index | 6048±11 640 | −16 858 to 28 954 | 0.60 |

| Socioeconomic vulnerability index | 16 840±9992 | −2817 to 36 496 | 0.09 |

CABG indicates coronary artery bypass grafting; CMS, Centers for Medicare and Medicaid Services; DSH, disproportionate share hospital; HCAHPS, Hospital Consumer Assessment of Healthcare Providers and Systems; and HRR, hospital referral region.

Regression coefficient±standard error.

After accounting for hospital characteristics and quality performance, hospitals in the East North Central and Pacific regions charged significantly higher prices than New England, which was the reference region (+$20 090 and +$34 890, respectively; P=0.02 and P<0.01).

Association Between Mortality Rate and CABG Prices

There was no statistically significant association between mortality rate and CABG price. There was a weak correlation for the CABG‐specific 30‐day mortality rate (r=−0.07) and a weak association for hospital‐wide mortality rate (P=0.19). There was not a significant association between CABG‐specific 30‐day mortality rate and CABG price (−$1293 per 1 SD increase in mortality rate [95% CI, −$3712 to $1126]). After adjusting for hospital and regional characteristics (Table 3), the CABG mortality rate was not associated with price (P=0.68). The results were similar for the hospital‐wide mortality rate (Table 3).

Association Between Readmissions and CABG Prices

There was similarly no statistically significant association between readmissions and CABG price. CABG‐specific 30‐day readmissions showed a weak correlation with CABG price (r<0.01). There was no significant association between hospital‐wide readmissions and price (P=0.26), nor was there an association with CABG readmissions (+$616 per 1 SD increase in readmission rate [95% CI, −$1781 to $3014]). After adjusting for selected hospital characteristics and quality metrics, CABG‐specific readmissions were still not associated with price (P=0.40; Table 3). This was true for hospital‐wide readmissions as well (Table 3).

Association Between Hospital Ratings and CABG Prices

Patient ratings were not associated with price (P=0.30). Higher CMS hospital rating were associated with higher price in univariate analysis (P=0.02). After adjusting for hospital characteristics and quality performance, the association between CMS hospital rating was no longer significant. Hospitals with higher patient Hospital Consumer Assessment of Healthcare Providers and Systems scores had higher CABG prices, with a 5‐star hospital having a $22 020 (95% CI, −$4616 to $48655) higher price than a hospital with a 1‐star rating, although this did not achieve statistical significance (P=0.10).

Discussion

The 2021 Federal Hospital Price Transparency Rule was enacted to promote price transparency across medical services, with the goal of reducing pricing variability and financial inequity. For CABG surgery, we found that median commercial payments were more than 2 times higher than Medicare payments. We also observed substantial variation in prices at the hospital level and within hospitals.

Economists often relate price and quality, with consumers seeing price as a proxy for quality. In this study, we found that the commercial health plan price for CABG was not significantly associated with the quality of care across several important metrics of hospital quality. Rather, price was associated with hospital characteristics including major teaching status, investor ownership, and hospital‐wide volume. While a strict comparison with prior literature is not possible given the lack of commercial price data availability before 2021, previous studies using statewide and nationwide claims data have not found an association between prices and clinical outcomes. 26 , 27 , 28 , 29 , 30 Another study examining out‐of‐pocket prices for CABG also found no association between quoted prices and CABG‐specific quality metrics. 31

There are significant questions about the overall structure of the US health care market, the impact of hospital consolidation on hospital market power in payer price negotiations, and the value associated with a market that requires individual negotiaiton of hospital–payer contracts. The policy community has been keen to examine the data provided by the Hospital Price Transparency Rule to gain greater insight into the functioning of this market. These results seem to raise more questions than answers to these larger policy questions. While documenting substantial regional pricing variation and substantial differences between commercial prices and Medicare payments, the intrahospital price variation is much greater than has been previously known. This variation could be related to underlying negotiation relationships between health plans and hospitals or could represent a significant inefficiency on the part of health plan negotiations. The source of this variation requires further study.

To our knowledge, this study is the first to assess commercial price variation and predictors of prices for CABG. While lower than the variation in price for other services, including percutaneous coronary intervention (3.6 times) and oncologic surgery (≈5–20 times), the within‐ and between‐hospital variation in CABG prices is substantial, considering that the median commercial price is $57 240. 5 , 7 With commercial payers responsible for 62.5% of CABG operations in the United States, the markup between commercial and Medicare prices could account for up to $3 billion in added health care expenditures annually. 9 , 32

Previous reports of CABG prices have relied on cost‐to‐charge ratios, with estimates that vary from $36 400 to $52 434. 26 , 33 , 34 These estimates are prone to inaccuracies because cost‐to‐charge ratios do not account for differences across service lines. 35 Furthermore, charges are determined at the discretion of individual hospitals, and their methodology is often opaque. Finally, the rates arrived at using cost‐to‐charge ratios are indexed to Medicare allowable rates and do not reflect the actual prices that insurers pay. The present study adds valuable real‐world data, demonstrating higher commercial CABG payment rates than previous estimates determined from cost‐to‐charge ratios. We also found more variation in commercial rates than estimated in prior studies. 26 , 34

In addition to substantial heterogeneity in commercial rates across hospitals, we also observed significant variation in self‐pay rates for CABG. The interquartile range for self‐pay rates was $64 626, ranging from $46 897 to $111 523. It is unclear what these amounts represent—they could be the basis for negotiating with patients for discounted care or an amount used by the hospital in the calculation of their community benefit. 36 What is clear is that these prices are higher than the Medicare payment rate in 87% of reporting hospitals and higher than the median commercial payment in 59% of hospitals.

Two years after the price transparency rule was enacted, compliance remains poor (52.3% in this study, which is similar to other recent estimates ranging from 48% to 59%). 37 , 38 Reasons for the persistently low adherence rate are multifactorial but likely include low penalties and inconsistent enforcement. 39 Additional enforcement efforts may be needed to ensure broader reporting.

This study has several limitations. The data analyzed were cross‐sectional and do not reflect trends in price over time. Pricing data were not available from noncompliant hospitals, which may have differences in pricing structure compared with compliant hospitals. There were also some differences in the characteristics of compliant versus noncompliant hospitals, which may be a source of potential bias. Some hospitals also had missing characteristics, which may influence the associations identified here, but this constituted a small minority of the total cohort. The outcome metrics studied here were limited to Medicare patients, not patients with private health insurance. However, Medicare patients constitute a large proportion of CABG surgeries. Finally, this study did not capture costs after the index hospitalization, which would be valuable in comparing payment variation across an entire episode of care.

Overall, private health plan payments for CABG were significantly greater than Medicare prices. There is significant inter‐ and intrahospital variation in negotiated prices for CABG. Variations in CABG prices were associated with hospital characteristics but not with hospital quality. These data raise important questions about the efficiency of administration in the US health care market.

Sources of Funding

This work was funded by a grant from the National Heart, Lung, and Blood Institute (1K23HL151672–03).

Disclosures

None.

Supporting information

Data S1.

Acknowledgments

Author Contributions: Drs Wei, Milligan, and Sandhu conceived and designed the study. Drs Wei, Milligan, and Paranjpe and P. Sharma collected patient data. Drs Wei, Milligan, and Paranjpe and P. Sharma analyzed the data. Drs Wei, Milligan, Paranjpe, Lam, Heidenreich, Kalwani, Schulman, and Sandhu and P. Sharma contributed to design the study and provided critical input on the manuscript. Dr Wei wrote the manuscript with input from all authors.

This manuscript was sent to Tazeen H. Jafar, MD, MPH, Associate Editor, for review by expert referees, editorial decision, and final disposition.

Supplemental Material is available at https://www.ahajournals.org/doi/suppl/10.1161/JAHA.123.031982

For Sources of Funding and Disclosures, see page 9.

References

- 1. Hospitals | CMS. Accessed July 19, 2022. https://www‐cms‐gov.laneproxy.stanford.edu/hospital‐price‐transparency/hospitals#key‐provisions.

- 2. Jiang J (Xuefeng), Forman HP, Gupta S, Bai G. Price variability for common radiology services within U.S. hospitals. Radiology. 2023;306:221815. doi: 10.1148/radiol.221815 [DOI] [PubMed] [Google Scholar]

- 3. Jiang J (Xuefeng), Makary MA, Bai G. Commercial negotiated prices for CMS‐specified shoppable surgery services in U.S. hospitals. Int J Surg 2021;95:106107. doi: 10.1016/j.ijsu.2021.106107 [DOI] [PubMed] [Google Scholar]

- 4. Xiao R, Ross JS, Gross CP, Dusetzina SB, McWilliams JM, Sethi RKV, Rathi VK. Hospital‐administered cancer therapy prices for patients with private health insurance. JAMA Intern Med. 2022;182:603–611. doi: 10.1001/jamainternmed.2022.1022 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 5. Xiao R, Miller LE, Workman AD, Bartholomew RA, Xu LJ, Rathi VK. Analysis of price transparency for oncologic surgery among National Cancer Institute‐designated cancer centers in 2020. JAMA Surg. 2021;156:582–585. doi: 10.1001/jamasurg.2021.0590 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 6. Feldman WB, Rome BN, Brown BL, Kesselheim AS. Payer‐specific negotiated prices for prescription drugs at top‐performing US hospitals. JAMA Intern Med. 2022;182:83–86. doi: 10.1001/jamainternmed.2021.6445 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 7. Oseran AS, Ati S, Feldman WB, Gondi S, Yeh RW, Wadhera RK. Assessment of prices for cardiovascular tests and procedures at top‐ranked US hospitals. JAMA Intern Med. 2022;182:996–999. doi: 10.1001/jamainternmed.2022.2602 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 8. Wei C, Milligan M, Lam M, Heidenreich PA, Sandhu A. Variation in cost of echocardiography within and across US hospitals. J Am Soc Echocardiogr. 2023;36:569–577. doi: 10.1016/j.echo.2023.01.002 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 9. Medicare Inpatient Hospitals – by Geography and Service . Centers for Medicare & Medicaid Services Data. Accessed January 3, 2023. https://data.cms.gov/jsonapi/taxonomy_term/dataset.

- 10. Bowdish ME, D'Agostino RS, Thourani VH, Schwann TA, Krohn C, Desai N, Shahian DM, Fernandez FG, Badhwar V. STS adult cardiac surgery database: 2021 update on outcomes, quality, and research. Ann Thorac Surg. 2021;111:1770–1780. doi: 10.1016/j.athoracsur.2021.03.043 [DOI] [PubMed] [Google Scholar]

- 11. Turquoise Health. Accessed July 19, 2022. https://turquoise.health/.

- 12. Provider of Services Current Files | CMS. Accessed July 19, 2022. https://www.cms.gov/Research‐Statistics‐Data‐and‐Systems/Downloadable‐Public‐Use‐Files/Provider‐of‐Services.

- 13. HCAHPS: Patients' Perspectives of Care Survey | CMS. Accessed July 19, 2022. https://www.cms.gov/Medicare/Quality‐Initiatives‐Patient‐Assessment‐Instruments/HospitalQualityInits/HospitalHCAHPS.

- 14. AHA Annual Survey. Accessed July 19, 2022. https://www.ahasurvey.org/taker/asindex.do.

- 15. Disproportionate Share Hospital (DSH) | CMS. Accessed August 4, 2022. https://www.cms.gov/Medicare/Medicare‐Fee‐for‐Service‐Payment/AcuteInpatientPPS/dsh.

- 16. Documentation and Files | CMS. Accessed July 19, 2022. https://www.cms.gov/medicare/physician‐fee‐schedule/search/documentation.

- 17. Compendium of U.S. Health Systems. Accessed July 19, 2022. https://www.ahrq.gov/chsp/data‐resources/compendium.html.

- 18. FAQ . Dartmouth atlas of health care. Accessed July 19, 2022. https://www.dartmouthatlas.org/faq/.

- 19. Hospital General Information | Provider Data Catalog. Accessed May 2, 2023. https://data.cms.gov/provider‐data/dataset/xubh‐q36u.

- 20. Complications and Deaths – Hospital | Provider Data Catalog. Accessed May 2, 2023. https://data.cms.gov/provider‐data/dataset/ynj2‐r877.

- 21. Unplanned Hospital Visits – Hospital | Provider Data Catalog. Accessed May 2, 2023. https://data.cms.gov/provider‐data/dataset/632h‐zaca.

- 22. User S. HMI. HCCI. Accessed February 7, 2023. https://healthcostinstitute.org/hcci‐originals/healthy‐marketplace‐index/hmi.

- 23. HOSPITAL_Data_Dictionary.pdf. Accessed May 24, 2023. https://data.cms.gov/provider‐data/sites/default/files/data_dictionaries/hospital/HOSPITAL_Data_Dictionary.pdf.

- 24. Xiao R, Rathi VK, Gross CP, Ross JS, Sethi RKV. Payer‐negotiated prices in the diagnosis and management of thyroid cancer in 2021. JAMA. 2021;326:184–185. doi: 10.1001/jama.2021.8535 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 25. Sandhu AT, Heidenreich PA, Bhattacharya J, Bundorf MK. Cardiovascular testing and clinical outcomes in emergency department patients with chest pain. JAMA Intern Med. 2017;177:1175–1182. doi: 10.1001/jamainternmed.2017.2432 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 26. Kilic A, Shah AS, Conte JV, Mandal K, Baumgartner WA, Cameron DE, Whitman GJR. Understanding variability in hospital‐specific costs of coronary artery bypass grafting represents an opportunity for standardizing care and improving resource use. J Thorac Cardiovasc Surg. 2014;147:109–115. doi: 10.1016/j.jtcvs.2013.08.024 [DOI] [PubMed] [Google Scholar]

- 27. Cowper PA, DeLong ER, Peterson ED, Hannan EL, Ray KT, Racz M, Mark DB. Variability in cost of coronary bypass surgery in New York state: potential for cost savings. Am Heart J. 2002;143:130–139. doi: 10.1067/mhj.2002.119617 [DOI] [PubMed] [Google Scholar]

- 28. Ghali WA, Hall RE, Ash AS, Moskowitz MA. Identifying pre‐ and postoperative predictors of cost and length of stay for coronary artery bypass surgery. Am J Med Qual. 1999;14:248–254. doi: 10.1177/106286069901400604 [DOI] [PubMed] [Google Scholar]

- 29. Saleh SS, Racz M, Hannan E. The effect of preoperative and hospital characteristics on costs for coronary artery bypass graft. Ann Surg. 2009;249:335–341. doi: 10.1097/SLA.0b013e318195e475 [DOI] [PubMed] [Google Scholar]

- 30. Guduguntla V, Syrjamaki JD, Ellimoottil C, Miller DC, Prager RL, Norton EC, Theurer P, Likosky DS, Dupree JM. Drivers of payment variation in 90‐day coronary artery bypass grafting episodes. JAMA Surg. 2018;153:14–19. doi: 10.1001/jamasurg.2017.2881 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 31. Giacomino BD, Cram P, Vaughan‐Sarrazin M, Zhou Y, Girotra S. Association of hospital prices for coronary artery bypass grafting with hospital quality and reimbursement. Am J Cardiol. 2016;117:1101–1106. doi: 10.1016/j.amjcard.2016.01.004 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 32. Alexander JH, Smith PK. Coronary‐artery bypass grafting. N Engl J Med. 2016;374:1954–1964. doi: 10.1056/NEJMra1406944 [DOI] [PubMed] [Google Scholar]

- 33. Dani SS, Minhas AMK, Arshad A, Krupica T, Goel SS, Virani SS, Sharma G, Blankstein R, Blaha MJ, Al‐Kindi SJ, et al. Trends in characteristics and outcomes of hospitalized young patients undergoing coronary artery bypass grafting in the United States, 2004 to 2018. J Am Heart Assoc. 2021;10:e021361. doi: 10.1161/JAHA.121.021361 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 34. Hadaya J, Sanaiha Y, Tran Z, Shemin RJ, Benharash P. Defining value in cardiac surgery: a contemporary analysis of cost variation across the United States. JTCVS Open. 2022;10:266–281. doi: 10.1016/j.xjon.2022.03.009 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 35. Bai G, Anderson GF. Extreme markup: the fifty US hospitals with the highest charge‐to‐cost ratios. Health Aff (Millwood). 2015;34:922–928. doi: 10.1377/hlthaff.2014.1414 [DOI] [PubMed] [Google Scholar]

- 36. Zare H, Eisenberg M, Anderson G. Charity care and community benefit in non‐profit hospitals: definition and requirements. Inquiry. 2021;58:00469580211028180. doi: 10.1177/00469580211028180 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 37. Milligan MG, Orav EJ, Lam MB. Determinants of commercial prices for common radiation therapy procedures. Int J Radiat Oncol Biol Phys. 2023;115:23–33. doi: 10.1016/j.ijrobp.2022.04.053 [DOI] [PubMed] [Google Scholar]

- 38. Haque W, Ahmadzada M, Janumpally S, Haque E, Allahrakha H, Desai S, Hsiehchen D. Adherence to a federal hospital price transparency rule and associated financial and marketplace factors. JAMA. 2022;327:2143–2145. doi: 10.1001/jama.2022.5363 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 39. Muoio D. CMS issued over 300 warnings, but no fines, to hospitals falling short on price transparency last year. Fierce Healthcare Published January. 2022;7. Accessed July 20, 2022. https://www.fiercehealthcare.com/hospitals/cms‐has‐issued‐over‐300‐warnings‐but‐no‐fines‐to‐hospitals‐falling‐short‐price [Google Scholar]

Associated Data

This section collects any data citations, data availability statements, or supplementary materials included in this article.

Supplementary Materials

Data S1.