Abstract

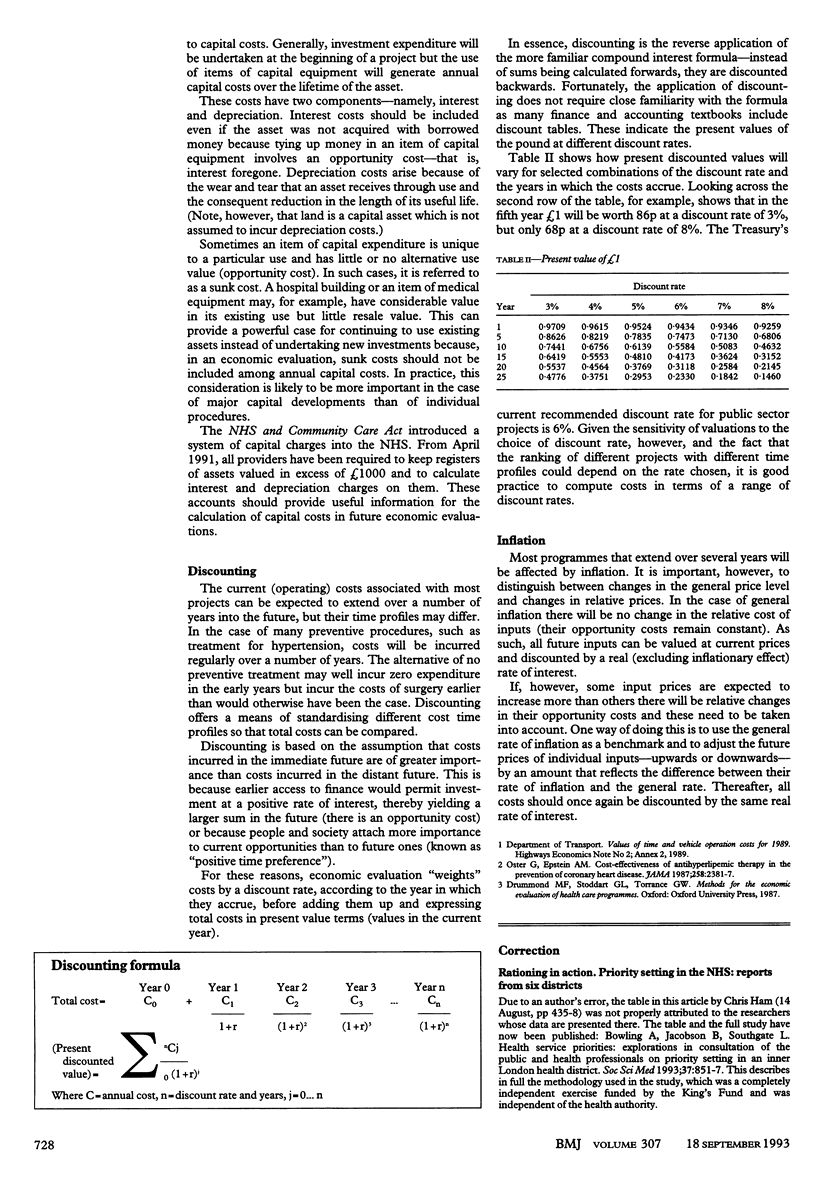

Whatever kind of economic evaluation you plan to undertake, the costs must be assessed. In health care these are first of all divided into costs borne by the NHS (like drugs), by patients and their families (like travel), and by the rest of society (like health education). Next the costs have to be valued in monetary terms; direct costs, like wages, pose little problem, but indirect costs (like time spent in hospital) have to have values imputed to them. And that is not all: costs must be further subdivided into average, marginal, and joint costs, which help decisions on how much of a service should be provided. Capital costs (investments in plant, buildings, and machinery) are also important, as are discounting and inflation. In this second article in the series Ray Robinson defines the types of costs, their measurement, and how they should be valued in monetary terms.

Full text

PDF

Images in this article

Selected References

These references are in PubMed. This may not be the complete list of references from this article.

- Oster G., Epstein A. M. Cost-effectiveness of antihyperlipemic therapy in the prevention of coronary heart disease. The case of cholestyramine. JAMA. 1987 Nov 6;258(17):2381–2387. [PubMed] [Google Scholar]