Purpose of review

This review describes how plasma is sourced for fractionation into plasma-derived medicinal products (PDMPs), such as immunoglobulin (Ig) together with differences between plasma from whole blood (recovered plasma) and from plasmapheresis (source plasma) in terms of global plasma supply. Specific areas of growth in immunoglobulin use are identified alongside novel therapies, which may reduce demand for some immunoglobulin indications.

Recent findings

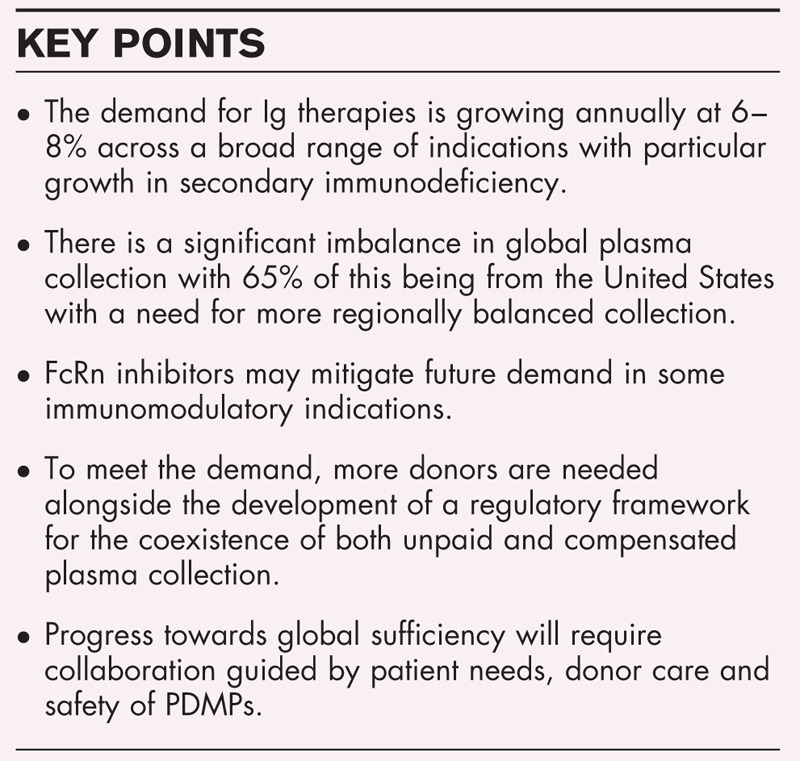

There has been a 6--8% annual growth in immunoglobulin use. Secondary immunodeficiency alongside improved recognition and diagnosis primary immunodeficiency disorders are drivers whereas the novel neonatal Fc receptor inhibitors (FcRni) may reduce demand for some immunomodulatory indications.

Summary

There is a significant geographical imbalance in global supply of plasma with 65% collected in the United States. This results in a dependency of other countries on United States supply and argues for both more plasma supply and greater regionally balanced plasma collection. In addition, progress towards a transparent, regulated and well tolerated framework for the coexistence of unpaid and compensated plasma donations is needed as unpaid donation will not be sufficient. These discussions should be informed by the needs of patients for this life-saving therapy, the care of donors and the safety of plasma and PDMPs.

Keywords: convalescent plasma, fractionation, immunoglobulin, plasma, plasmapheresis

INTRODUCTION

Immunoglobulins, polyclonal/polyvalent (IgG) and hyperimmune (H-IgG) are plasma derived medicinal products (PDMPs) produced by fractionation. Immunoglobulin replacement therapy (IgRT) began in 1952 [1] with subsequent developments in intramuscular immunoglobulin (IMIg), intravenous immunoglobulin (IVIg), subcutaneous immunoglobulin (SCIg) and most recently, facilitated SCIg (fSCIg) routes [2].

Today Ig therapies are used in a wide range of indications with increasing demand and availability directly linked to supply of the raw material, human plasma. This article reviews plasma sourcing and manufacture alongside a global perspective to challenges in supply and new therapies, which may impact on some of the current indications for immunoglobulin therapy.

Box 1.

no caption available

PLASMA COLLECTION AND IMMUNOGLOBULIN MANUFACTURE

Ig therapies are manufactured from plasma collected from a large number of donors to ensure diverse specificities of antibodies against a broad spectrum of pathogens [3,4]. Manufacture is a complex, strictly regulated process to ensure safety, quality, purity and potency of therapies [3–12].

Plasma is obtained either from whole blood donation by separating from cells (recovered plasma) or by direct plasma donation through plasmapheresis (source plasma) or co-collected during platelet apheresis. Plasmapheresis separates plasma by centrifugation while returning blood cells to the donor. Donor care is key both for the well being of the donor and quality of the plasma.

A unit of recovered plasma ranges from 100 to 260 ml (WHO) [13] and can be used as fresh frozen plasma (FFP), convalescent plasma therapy (CPT) as for COVID-19, or to manufacture PDMPs. Whole blood donors are usually only permitted to donate every 3 months to avoid anaemia.

Plasmapheresis (source plasma) yields more plasma (450–880 ml) (WHO) [13] depending on regulations in the country of collection [14▪▪,15,16]. In the United States donation frequency is twice weekly with 2 days between and maximally 104 donations annually [9] but only 0.3% donate more than 100 times, 14% more than 50 times, whereas 49% donated 10 times or fewer annually [17]. In Europe, maximum annual donations range from 24 to 60. The European Directorate for the Quality of Medicines (EDQM) nonbinding recommendations advise a maximum of 33 plasma donations per year with at least 96 h between the donations [18]. Compared with recovered plasma, plasmapheresis allows collection of much larger annual plasma volumes available for fractionation due a combination of higher donation frequency and a larger volumes per donation.

Manufacture by fractionation of Ig from up to tens of thousands of units of pooled plasma takes from 7 to 12 months and is based on cold ethanol precipitation of proteins developed by Cohn et al. in the 1940s [19–21] with additional dedicated steps to increase purity, yield, improve quality and enhance safety margins to prevent potential transmission of pathogens. These steps vary between brands and include plasma protein separation by precipitation and/or chromatography, protein purification using ion exchange or affinity chromatography, and steps (one or more) for the inactivation or removal of potential infectious agents, such as blood-borne viruses and prions [22–27].

INDICATIONS AND USES OF IMMUNOGLOBULIN THERAPIES

Ig therapies for primary immunodeficiency (PID) and Kawasaki diseases are on the WHO List of Essential Medicines [28,29] and are unique biological products with no single product or method of administration suitable for all patients [30]. It is well established that the differences in manufacturing processes can affect individual tolerability, risk of adverse events, infusion rate and potentially efficacy [31] making access to a range of different Ig therapies vital.

Indications for Ig therapy vary depending on the region/country (Table 1) as does use in a wide range of other off-license indications [32–35].

Table 1.

Approved indications for immunoglobulin Europe and United States

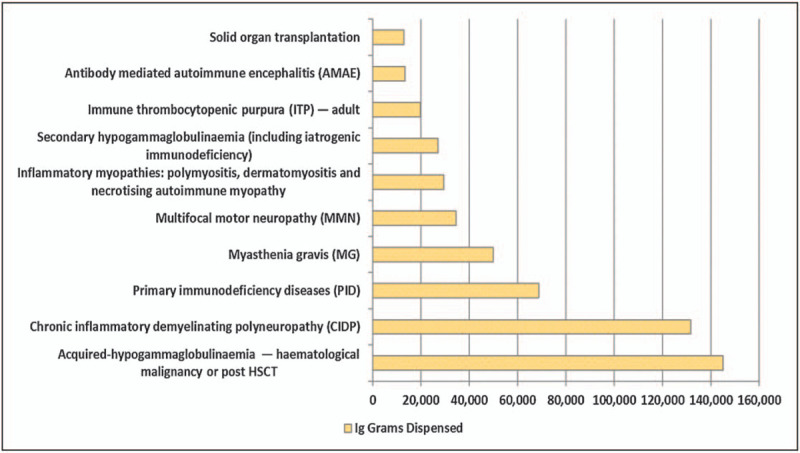

Currently PID and secondary inmmunodeficiency (SID) are the major indications as exemplified from Australian National Blood Authority data [36] (Fig. 1) and the UK Database [37] with PID (1 514 760 g), CIDP (1 239 547 g) and SID (991 511 g). In the United States, PID represents roughly 30% (including some SID), CIDP 20%, myasthenia gravis 10%, ITP 9%, others 31%, (M. Hotchko, MRB Personal communication, 1 July 2020).

FIGURE 1.

Data from the Australian National Blood Authority showing the amount of immunoglobulin dispensed by medical condition with the highest amount being for secondary antibody deficiency because of hematological malignancy or haematopoietic stem cell transplantation (HSCT) and this being more than twice that for primary immunodeficiency (PID). On the basis of data https://www.blood.gov.au/ig-usage-data-and-statistics.

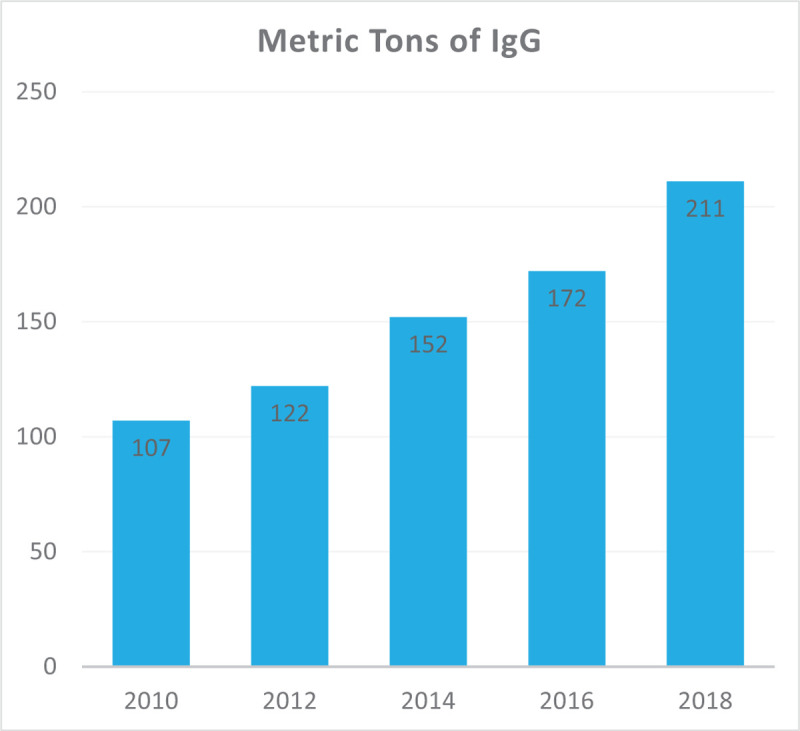

Overall global Ig demand has increased annually by 6–8% (Fig. 2), with a higher rate in emerging markets because of lower starting consumption levels [38].

FIGURE 2.

The annual growth rate in global immunoglobulin use (based on data from the Marketing Research Bureau) showing the year on year rise in immunoglobulin use between 2010 and 2018 at an average of around 12% per year.

Factors influencing annual growth in consumption are complex and not only include increasing use in SID and neurological conditions but also improved diagnosis for PID particularly in developed countries linked to increasing use of newborn and calculated globulin screening [39–41,42▪▪]. However, the reality of massive worldwide underdiagnosis for around 70–90% of PID patients persists [43]. Encouragingly, disease-specific diagnostic tests for PIDs are now on the WHO List of Essential In-Vitro Diagnostics Tests [44] with 430 different PIDs identified in the latest IUIS classification [45].

Supply dynamics of PDMPs have historically been characterized by intermittent shortages with Ig therapies recently ranked third most frequent medicinal product facing shortages in the EU pharmacists report of medicinal products [46].

NEW THERAPIES WHICH MAY REDUCE IMMUNOGLOBULIN USE

Set against this growth are some potential areas of reduction for immunomodulatory indications because of new therapies.

Three evolving therapeutic approaches overlap with immunomodulatory mechanisms of action of Ig including – blockade of the neonatal Fc receptor (FcRn) and other Fc receptors (FcR), reducing autoantibody production, and complement inhibition [32,47–50,51▪▪,52▪▪].

The FcRn functions as a recycling mechanism to prevent degradation and extend the half-life of IgG and albumin in the circulation. Maintenance of serum IgG levels is proportionally more dependent on recycling than production [49,50]. One mechanism by which hdIVIg reduces pathogenic autoantibodies is by saturation of FcRn receptors [53].

Several FcRn inhibitors (FcRni) rozanolixizumab, efgartigimod, orilanolimab, and nipocalimab selectively targeting IgG recycling are in clinical trials for CIDP, MG and ITP. These can reduce serum IgG by 45–80% [54–57], levels returning to baseline after 28 and 57 days depending on the FcRni [54–58]. FcRni have potential for future use in a much wider variety of antibody-mediated autoimmune diseases, which may reduce pressure for Ig on repertoire-dependent indications such as PID and SID.

Further strategies targeting FcR in autoimmune disease are multimerization of recombinant Fc portion of antibodies and modification of Fc by hyper-sialylation [59▪▪] (M254). Recombinant fragment crystallizable (rFc) multimers primarily target Fcγ receptors (FcγRs) but may also affect the complement system [60,61▪].

Significant advances have also been made in terms of targeting B cells predominantly for hematological malignancies, such as CD19 (Ineblizumab), CD22 (Epratuzumab), CD38 (Daratumumab, Isatuximab) as well as proteasome inhibitors. Future indications in autoimmune and inflammatory disease as with rituximab are likely, impacting indications for hdIVIg, such as neuromyelitis optica (NMO) [58].

There is also increasing interest in complement inhibition in autoimmune and inflammatory diseases with novel inhibitors (eclulizumab, tesidolumab and ravulizumab) targeting C5 and the C5a blocking antibody (IFX-1) noting that complement inhibition is another mechanism of action of hdIVIg [62].

ENSURING SUFFICIENT FUTURE GLOBAL SUPPLY

Ensuring sufficient global supply and stability requires both increased plasma supply and improved fractionation technology to optimize yield from each litre of plasma alongside a vibrant R&D platform for novel PDMPs.

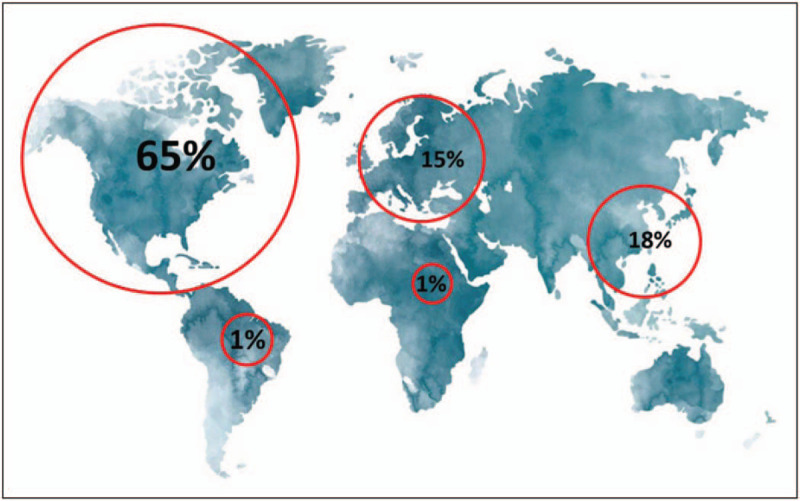

There are significant regional differences in collected volumes of recovered and source plasma. In 2017, the United States supplied 65% of world plasma for fractionation (Fig. 3), and 71% of all source plasma, whereas Europe was the largest supplier of recovered plasma with only 10% of source plasma [63]. Latin America and Africa currently account for a very small proportion of global plasma supply and have a rapidly growing demand. The United States has the highest global Ig sales at 46% (Fig. 4) but is in fact a net exporter with 65% of the world plasma collection.

FIGURE 3.

The global distribution of plasma (source and recovered) collection (based on data from the Marketing Research Bureau) showing the current world reliance on the United States-based plasma collection.

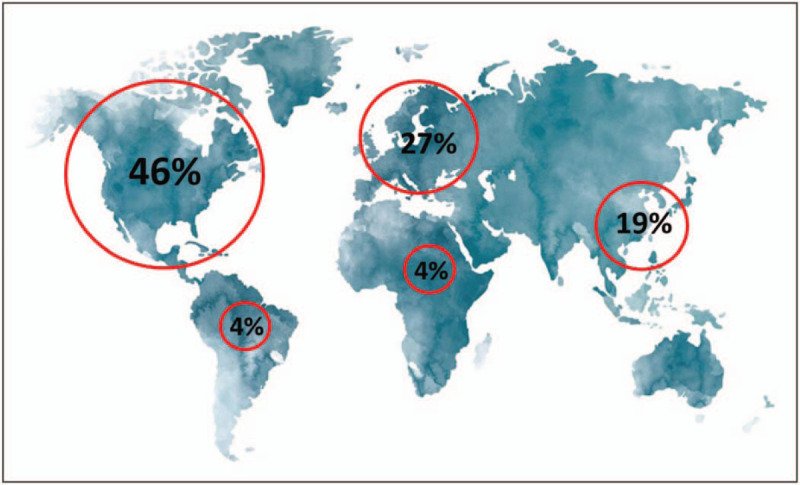

FIGURE 4.

Global immunoglobulin sales (based on data from the Marketing Research Bureau 2018) showing the currently low levels of sales per head and potential for growth in areas, such as Latin America and Africa alongside European sales dependent on the United States plasma collection.

Strategies to attract and retain more blood and plasma donors, especially source plasma donors given that in 2015, recovered plasma accounted for only 13% of fractionated plasma worldwide [64], are key alongside harmonization of best practice in donation frequency and volume limits to ensure the safety of donors and quality of final products.

In the United States and some EU countries, such as Germany, Austria, the Czech Republic and Hungary, source plasma donors are compensated for their donations. However, in most other EU countries, plasma donor compensation is currently not authorized with reliance on unpaid donations. Germany, Austria, the Czech Republic and Hungary collect proportionally a much higher plasma volume than any other European country (three times higher). In 2017, whilst the nonprofit public sector collected 55% of European plasma used for fractionation, the commercial sector collected 45% but from just four countries with a population of 112 million (European population 743 million) (M. Hotchko, MRB. Personal communication, 1 July 2020).

Could both compensated and unpaid co-exist and contribute together towards increased plasma collection? From a viral safety perspective, it is well established that PDMPs made from compensated plasma donations are just as well tolerated as those made from unpaid donations [65]. There is the need for a re-evaluation [66] of this growing disparity in collections across Europe to ensure future global supply based on more regionally balanced plasma collection.

Today's reality is that the United States contributes the large majority of the world's plasma supply (Fig. 3), making other regions, such as Europe highly dependent on American (largely compensated) plasma donors, creating an imbalance, which could jeopardize access to life-saving Ig therapies. The past has shown us that national sources of plasma can become unusable from 1 day to the next, such as with the variant Creutzfeldt--Jakob disease (vCJD) crisis in the UK in the 1990s. There has been significant inertia in evidence-based decisions concerning the ability to fractionate UK plasma again despite growing national and global need. The costs have been high in terms of opportunity, loss of sovereign fractionation capacity, supply shortages and the exposure to rising global price. Additionally, the COVID-19 pandemic is likely to lead to further strains on immunoglobulin supply as plasma donations have declined in 2020 (https://www.pptaglobal.org/media-and-information/ppta-statements/1081-ppta-repeats-appeals-for-plasma-donations). Stay-at-home and social distancing measures have led to reductions in regular attendances at donor centres whilst the urgent need for SARSCoV2 antibody-positive plasma for CPT and H-IgG has been an ongoing priority. This highlights the need for universal and international access to PDMPs (including CPT and H-IgG) and for collecting more plasma. In the UK and other countries, response times to the pandemic for CPT would have been markedly quicker had an existing national network for plasma donation at scale already been in place.

CONCLUSION

There has been significant and year on year growth of around 6–8% in the requirement for immunoglobulin for predominantly Immunology, Neurology and Hematology indications. Major drivers include increases in SID, better recognition and diagnosis of PID albeit on a background of massive underdiagnosis globally.

Novel therapies such as FcRn inhibitors may reduce demand in some of the current immunomodulatory indications for Ig. However, to meet demand there needs to be an increase in plasma collection with reduction in the current imbalance of 65% of plasma coming from the US towards a much more regionally balanced collection and with a view to attain global sufficiency in PDMPs. In addition, transparent and collaborative discussions concerning the regulatory framework to allow the coexistence of both unpaid and compensated plasma donation need to progress and should be patient-centred. The underpinning rationale should be the needs of patients for these life-saving therapies, the care of donors and the safety of plasma and PDMPs.

Acknowledgements

We would like to gratefully acknowledge the expertise and help of Larisa Cervenakova especially in relation to details of plasma collection and manufacture.

Financial support and sponsorship

None.

Conflicts of interest

S.J. declares Advisory Board, Speaker, Conference, Clinical Trial, DSMB, or Projects with CSL Behring, Shire, Takeda, Thermofisher, Swedish Orphan Biovitrum, Biotest, Binding Site, BPL, Octapharma, Sanofi, LFB, Pharming, Biocryst, Zarodex, Weatherden and UCB Pharma.

J.P. is the Executive Director of the International Patient Organisation for Primary Immunodeficiencies (IPOPI). IPOPI regularly receives support from a broad range of companies involved in the manufacture of immunoglobulin therapies and the field of primary immunodeficiencies. For an updated list please visit www.ipopi.org.

REFERENCES AND RECOMMENDED READING

Papers of particular interest, published within the annual period of review, have been highlighted as:

▪ of special interest

▪▪ of outstanding interest

REFERENCES

- 1.Bruton OC. Agammaglobulinemia. Pediatrics 1952; 9:722–728.14929630 [Google Scholar]

- 2.Jolles S. Hyaluronidase facilitated subcutaneous immunoglobulin in primary immunodeficiency. Immunotargets Ther 2013; 2:125–133. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 3.European Medicines Agency. Guideline on the clinical investigation of human normal immunoglobulin for intravenous administration (IVIg). EMA/CHMP/BPWP/94033/2007 rev. 3. Committee for Medicinal Products for Human Use (CHMP), 28 June 2018. Available at: https://www.ema.europa.eu/en/documents/scientific-guideline/guideline-clinical-investigation-human-normal-immunoglobulin-intravenous-administration-ivig-rev-3_en.pdf (Accessed 15 June 2019) [Google Scholar]

- 4.European Medicines Agency. Guideline on the clinical investigation of human normal immunoglobulin for subcutaneous and/or intramuscular administration (SCIg/IMIg). EMA/CHMP/BPWP/410415/2011 rev 1. 23 July, 2015. Available at: https://www.ema.europa.eu/en/documents/scientific-guideline/guideline-clinical-investigation-human-normal-immunoglobulin-subcutaneous/intramuscular-administration-scig/imig_en.pdf (Accessed 15 June 2020) [Google Scholar]

- 5.European Medicines Agency. Guideline on plasma-derived medicinal products. EMA/CHMP/BWP/706271/2010. London. 21 July, 2011. Available at: https://www.ema.europa.eu/en/documents/scientific-guideline/guideline-plasma-derived-medicinal-products_en.pdf (Accessed 29 April 2019) [Google Scholar]

- 6.European Medicines Agency. Guideline on core SmPC for human normal immunoglobulin for intravenous administration (IVIg). 28 June 2018. Available at: https://www.ema.europa.eu/en/documents/scientific-guideline/guideline-core-smpc-human- normal-immunoglobulin-intravenous-administration-ivig-rev-5_en.pdf (Accessed 29 April 2019) [Google Scholar]

- 7.European Medicines Agency. Guideline on core SmPC for human normal immunoglobulin for subcutaneous and intramuscular administration. 26 February 2015. Available at: https://www.ema.europa.eu/en/documents/scientific-guideline/guideline-core-smpc-human-normal-immunoglobulin-subcutaneous-intramuscular-administration_en.pdf (Accessed 15 June 2020). [Google Scholar]

- 8.U.S. Code of Federal Regulations (CFR). Title 21. Part 630. E-CFR data. 11 June 2020. Requirements for blood and blood components intended for transfusion or for further manufacturing use. Available at: https://www.ecfr.gov/cgi-bin/text-idx?SID=b9a1e78f3a48d2d51657842ddf61f0a4&mc=true&node=pt21.7.630&rgn=div5 (Accessed 15 June 2020). [Google Scholar]

- 9. [(Accessed 20 June 2020)]. U.S. Code of Federal Regulations (CFR) Title 21. Part 640. Additional standards for human blood and blood products. E-CFR data, June 11, 2020. Available at: https://www.ecfr.gov/cgi-bin/text-idx?SID=b9a1e78f3a48d2d51657842ddf61f0a4&mc=true&node=pt21.7.640&rgn=div5#se21.7.640_130. [Google Scholar]

- 10.U.S. Food and Drug Administration. Guidance for industry: For the submission of chemistry, manufacturing and controls and establishment description information for human blood and blood components intended for transfusion or for further manufacture and for the completion of the Form FDA 356 h ‘Application to market a new drug, biologic or an antibiotic drug for human use’. May, 1999. Available at: https://www.fda.gov/downloads/BiologicsBloodVaccines/GuidanceComplianceRegulatoryInformation/Guidances/Blood/ucm080803.pdf (Accessed 20 June 2020) [PubMed] [Google Scholar]

- 11.Plasma Protein Therapeutics Association (PPTA). International Quality Plasma Program (IQPP). Available at: https://www.pptaglobal.org/safety-quality/standards/iqpp (Accessed on 20 June 2019). [Google Scholar]

- 12.Plasma Protein Therapeutics Association (PPTA). Quality standards of excellence, assurance and leadership (QSEAL). Available at: https://www.pptaglobal.org/safety-quality/standards/qseal (Accessed 20 June 2019). [Google Scholar]

- 13.WHO Recommendations for the production, control and regulation of human plasma for fractionation. Annex 4. 2005. WHO Technical Report Series No 941, 2007 https://www.who.int/bloodproducts/publications/TRS941Annex4blood.pdf?ua=1 (Accessed 5 July 2020). [Google Scholar]

- 14▪▪.Burnouf T. An overview of plasma fractionation. Ann Blood 2018; 3:33. [Google Scholar]; Very helpful overview of plasma fractionation processes for anyone using immunoglobulin therapy.

- 15.An EU programme of COVID-19 convalescent plasma collection and transfusion. Guidance on collection, testing, processing, storage, distribution and monitored use. Version 2.0. 19 June, 2020. Available at: https://ec.europa.eu/health/sites/health/files/blood_tissues_organs/docs/guidance_plasma_covid19_en.pdf [Accessed 17 september 2020]. [Google Scholar]

- 16.Expanded access to convalescent plasma for the treatment of patients with COVID-19. Version 8.0. 16 June, 2020. National Clinical Trial (NCT) Protocol Identified Number 04338360. Available at: https://www.uscovidplasma.org/pdf/COVID-19%20Plasma%20EAP.pdf [Accessed 17 september 2020]. [Google Scholar]

- 17.Schreber GB, Kimber MC. [(Accessed 20 June 2020)]. Source Plasma Donors: A Snapshot. Transfusion. TRANSFUSION 2017 Vol. 57 Supplement S3 (Page 110A). Available at: https://www.pptaglobal.org/images/presentations/2017/Schreiber.AABBposterAbstract_Source_Plasma_Donors_A_Snapshot_2017_9.27.17.pdf. [Google Scholar]

- 18.20th Edition of the Guide to the preparation, use and quality assurance of blood components. European Committee (Partial Agreement) on Blood Transfusion (CD-P-TS). European Directorate for the Quality of Medicines (EDQM). Council of Europe. Recommendation No R (95) 15. Available at: https://www.edqm.eu/en/blood-guide [Accessed 17 september 2020]. [Google Scholar]

- 19.Cohn EJ, Oncley JL, Strong LE, et al. Chemical, clinical, and immunological studies on the products of human plasma fractionation. I. The characterization of the protein fractions of human plasma. J Clin Invest 1944; 23:417–432. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 20.Cohn E, Strong L, Hughes W, et al. Preparation and properties of serum and plasma proteins. IV. A system for the separation into fractions of the protein and lipoprotein components of biological tissues and fluids. J Am Chem Soc 1946; 68:459–475. [DOI] [PubMed] [Google Scholar]

- 21.Radosevich M, Burnouf T. Intravenous immunoglobulin G: trends in production methods, quality control and quality assurance. Vox Sang 2010; 98:12–28. [DOI] [PubMed] [Google Scholar]

- 22.Hooper JA. Intravenous immunoglobulins: evolution of commercial IVIG preparations. Immunol Allergy Clin North Am 2008; 28:765–778. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 23.Dichtelmüller HO, Biesert L, Fabbrizzi F, et al. Robustness of solvent/detergent treatment of plasma derivatives: a data collection from Plasma Protein Therapeutics Association member companies. Transfusion 2009; 49:1931–1943. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 24.Thyer J, Unal A, Thomas P, et al. Prion-removal capacity of chromatographic and ethanol precipitation steps used in the production of albumin and immunoglobulins. Vox Sang 2006; 91:292–300. [DOI] [PubMed] [Google Scholar]

- 25.Cai K, Gröner A, Dichtelmüller HO, et al. Prion removal capacity of plasma protein manufacturing processes: a data collection from PPTA member companies. Transfusion 2013; 53:1894–1905. [DOI] [PubMed] [Google Scholar]

- 26.Farrugia A, Quinti I. Manufacture of immunoglobulin products for patients with primary antibody deficiencies - the effect of processing conditions on product safety and efficacy. Front Immunol 2014; 5:665. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 27.Buchacher A, Iberer G. Purification of intravenous immunoglobulin G from human plasma – aspects of yield and virus safety. Biotechnol J 2006; 1:148–163. [DOI] [PubMed] [Google Scholar]

- 28.World Health Organization Model List of Essential Medicines, 21st List, 2019. 2019; Geneva: World Health Organization, Available online: https://apps.who.int/iris/bitstream/handle/10665/325771/WHO-MVP-EMP-IAU-2019.06-eng.pdf?ua=1 (Accessed 5 July 2020). [Google Scholar]

- 29.World Health Organization Model List of Essential Medicines for Children, 7th List, 2019. 2019; Geneva: World Health Organization, Available online: https://apps.who.int/iris/bitstream/handle/10665/325772/WHO-MVP-EMP-IAU-2019.07-eng.pdf?ua=1 (Accessed 5 July 2020). [Google Scholar]

- 30.Chapel H, Prevot J, Gaspar HB, et al. Editorial Board for Working Party on Principles of Care at IPOPI. Primary immune deficiencies – principles of care. Front Immunol 2014; 5:627. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 31.Kerr J, Quinti I, Eibl M, et al. Is dosing of therapeutic immunoglobulins optimal? A review of a three-decade long debate in Europe. Front Immunol 2014; 5:629. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 32.Perez EE, Orange JS, Bonilla F, et al. Update on the use of immunoglobulin in human disease: a review of evidence. J Allergy Clin Immunol 2017; 139 (3S):S1–S46. [DOI] [PubMed] [Google Scholar]

- 33.Jolles S, Sewell WAC, Misbah SA. Clinical use of intravenous immunoglobulin, 2005 British Society for Immunology. Clin Exp Immunol 2005; 142:1–11. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 34.Tonkovic B, Rutishauser LK. Descriptive review and analysis of immunoglobulin utilization management from 2,548 prior authorization requests. J Manag Care Spec Pharm 2014; 20:357–367. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 35. [(Accessed 15 June 2020)]. An EU-wide overview of the market of blood, blood components and plasma derivatives focusing on their availability for patients Creative Ceutical Report, revised by the Commission to include stakeholders’ comments. Available at: https://ec.europa.eu/health/sites/health/files/blood_tissues_organs/docs/20150408_cc_report_en.pdf. [Google Scholar]

- 36. [(Accessed15 June 2020)]. https://www.blood.gov.au/ig-usage-data-and-statistics. [Google Scholar]

- 37. [(Accessed 15 June 2020)]. http://igd.mdsas.com/wp-content/uploads/ImmunoglobulinDatabaseAnnualReport201819.pdf. [Google Scholar]

- 38.Marketing Research Bureau. Available online: https://marketingresearchbureau.com/list-of-reports/worldwide-immunoglobulin-igg-forecast-2023/ (Accessed 19 June 2020). [Google Scholar]

- 39.Holding S, Khan S, Sewell WA, et al. Using calculated globulin fraction to reduce diagnostic delay in primary and secondary hypogammaglobulinaemias: results of a demonstration project. Ann Clin Biochem 2014; 52 (Pt 3):319–326. [DOI] [PubMed] [Google Scholar]

- 40.Jolles S, Borrell R, Zouwail S, et al. Calculated globulin (CG) as a screening test for antibody deficiency. Clin Exp Immunol 2014; 177:671–678. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 41.Holding S, Jolles S. Current screening approaches for antibody deficiency. Curr Opin Allergy Clin Immunol 2015; 15:547–555. [DOI] [PubMed] [Google Scholar]

- 42▪▪.Pecoraro A, Jolles S, Crescenzi L, et al. Validation of calculated globulin (CG) as a screening test for antibody deficiency in an Italian University Hospital. Curr Pharm Biotechnol 2018; 19:728–733. [DOI] [PubMed] [Google Scholar]; Validation of a cost-effective screening approach for antibody deficiency in a large Italian Teaching Hospital.

- 43. [[Accessed 17 september 2020]]. Primary Immunodeficiencies (PID) – Driving Diagnosis for Optimal Care in Europe, European Reference Paper. Available at: http://worldpiweek.org/sites/default/files/basic_page_documents/PI_European_Reference_Paper.pdf [Ref list] [Google Scholar]

- 44.World Health Organization. Second WHO Model List of Essential In Vitro Diagnostics (EDL). WHO/MVP/EMP/2019.05. Available at: https://www.who.int/docs/default-source/nutritionlibrary/complementary-feeding/second-who-model-list-v8-2019.pdf?sfvrsn=6fe86adf_1] [Accessed 20 June 2020]. [Google Scholar]

- 45.Tangye SG, Al-Herz W, Bousfiha A, et al. Human inborn errors of immunity: 2019 update on the classification from the international union of immunological societies expert committee. J Clin Immunol 2020; 40:24–64. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 46. [[Accessed 15 June 2020]]. EAHP Medicines Shortages Survey 2018. Available at: https://www.eahp.eu/sites/default/files/report_medicines_shortages2018.pdf. [Google Scholar]

- 47.Nagelkerke SQ, Kuijpers TW. Immunomodulation by IVIg and the role of Fc-Gamma receptors: classic mechanisms of action after all? Front Immunol 2014; 5:674. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 48.Li N, Zhao M, Hilario-Vargas J, et al. Complete FcRn dependence for intravenous Ig therapy in autoimmune skin blistering diseases. J Clin Invest 2005; 115:3440–3450. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 49.Kim J, Hayton WL, Robinson JM, Anderson CL. Kinetics of FcRn-mediated recycling of IgG and albumin in human: pathophysiology and therapeutic implications using a simplified mechanism-based model. Clin Immunol 2007; 122:146–155. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 50.Roopenian DC, Akilesh S. FcRn: the neonatal Fc receptor comes of age. Nat Rev Immunol 2007; 7:715–725. [DOI] [PubMed] [Google Scholar]

- 51▪▪.Peter H-H, Ochs HD, Cunningham-Rundles C, et al. Targeting FcRn for immunomodulation: benefits, risks, and practical considerations. J Allergy Clin Immunol 2020; 146:479.e5–491.e5. [DOI] [PMC free article] [PubMed] [Google Scholar]; Review of the practical clinical considerations of FcRn inhibition drawing on the available trial data as well as primary immunodeficiencies with impact on recycling of IgG.

- 52▪▪.Patel DD, Bussel JB. Neonatal Fc receptor in human immunity: function and role in therapeutic intervention. J Allergy Clin Immunol 2020; 146:467–478. [DOI] [PubMed] [Google Scholar]; Excellent review of targeted therapeutic interventions for FcRn.

- 53.Hansen RJ, Balthasar JP. Intravenous immunoglobulin mediates an increase in antiplatelet antibody clearance via the FcRn receptor. Thromb Haemost 2002; 88:898–899. [PubMed] [Google Scholar]

- 54.Blumberg LJ, Humphries JE, Jones SD, et al. Blocking FcRn in humans reduces circulating IgG levels and inhibits IgG immune complex-mediated immune responses. Sci Adv 2019; 5:eaax9586. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 55.Kiessling P, Lledo-Garcia R, Watanabe S, et al. The FcRn inhibitor rozanolixizumab reduces human serum IgG concentration: a randomized phase 1 study. Sci Transl Med 2017; 9:eaan1208. [DOI] [PubMed] [Google Scholar]

- 56.Ling LE, Hillson JL, Tiessen RG, et al. M281, an anti-FcRn antibody: pharmacodynamics, pharmacokinetics, and safety across the full range of IgG reduction in a first-in-human study. Clin Pharmacol Ther 2019; 105:1031–1039. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 57.Ulrichts P, Guglietta A, Dreier T, et al. Neonatal Fc receptor antagonist efgartigimod safely and sustainably reduces IgGs in humans. J Clin Invest 2018; 128:4372–4386. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 58.Kleiter I, Ralf Gold R. Present and future therapies in neuromyelitis optica spectrum disorders. Neurotherapeutics 2016; 13:70–83. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 59▪▪.Shock A, Humphreys D, Nimmerjahn F. Dissecting the mechanism of action of intravenous immunoglobulin in human autoimmune disease: lessons from therapeutic modalities targeting Fcγ receptors. J Allergy Clin Immunol 2020; 146:492–500. [DOI] [PubMed] [Google Scholar]; Excellent review of the FcR therapy area.

- 60.Spirig R, Campbell IK, Koernig S, et al. rIgG1 Fc hexamer inhibits antibody-mediated autoimmune disease via effects on complement and FcgammaRs. J Immunol 2018; 200:2542–2553. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 61▪.Zuercher AW, Spirig R, Baz Morelli A, et al. Next-generation Fc receptor-targeting biologics for autoimmune diseases. Autoimmun Rev 2019; 18:102366. [DOI] [PubMed] [Google Scholar]; Description of current Fc receptor targeting therapies including Fc multimers, FcRni and anti Fc monoclonal antibodies.

- 62.Spycher M, Matozan K, Minnig K, et al. In vitro comparison of the complement-scavenging capacity of different intravenous immunoglobulin preparations. Vox Sang 2009; 97:348–354. [DOI] [PubMed] [Google Scholar]

- 63.Robert P. An analysis of the impact of international transfers of plasma on the availability of immunoglobulin therapies. The Source Fall 2019; 10–14. Available at: https://vault.netvoyage.com/neWeb2/delView.aspx?env=%2FQ14%2Ft%2F3%2Fl%2Fq%2F∼190925112919679.nev&dn=1&v=2&dl=1&p=0&e=&t=dfcqsfLXNzVH6qRtkbOpMfsiOHo%3D&cg=NG-N9RHSZR6&hd=1&nf=N&s=VAULT-PVPGFHJ2 [Accessed 17 September 2020]. [Google Scholar]

- 64.Weinstein M. Regulation of plasma for fractionation in the United States. Ann Blood 2018; 3:3.http://aob.amegroups.com/article/view/4255/4985http://aob.amegroups.com/article/view/4255/4985. [Accessed 19 June 2020]. [Google Scholar]

- 65.EMA CPMP Position Statement ‘Non-Remunerated and Remunerated Donors: Safety and Supply of Plasma Derived Medicinal Products’, EMEA/CPMP/BWP/1818/02/Final, 30 May 2002. [Google Scholar]

- 66.Jaworski P M, Bloody Well Pay Them: The case for Voluntary Remunerated Plasma Collections, © Adam Smith Research Trust 2020. Available at: https://static1.squarespace.com/static/56eddde762cd9413e151ac92/t/5ee267f9ce32482076be1a98/1591896062393/Bloody+Well+Pay+Them+-+Peter+Jaworski.pdf [Accessed 17 September 2020]. [Google Scholar]