Abstract

Many low‐income countries are in the process of scaling up health insurance with the goal of achieving universal coverage. However, little is known about the usage and financial sustainability of mandatory health insurance. This study analyzes 26 million claims submitted to the Tanzanian National Health Insurance Fund (NHIF), which covers two million public servants for whom public insurance is mandatory, to understand insurance usage patterns, cost drivers, and financial sustainability. We find that in 2016, half of policyholders used a health service within a single year, with an average annual cost of 33 US$ per policyholder. About 10% of the population was responsible for 80% of the health costs, and women, middle‐age and middle‐income groups had the highest costs. Out of 7390 health centers, only five health centers are responsible for 30% of total costs. Estimating the expected health expenditures for the entire population based on the NHIF cost structure, we find that for a sustainable national scale‐up, policy makers will have to decide between reducing the health benefit package or increasing revenues. We also show that the cost structure of a mandatory insurance scheme in a low‐income country differs substantially from high‐income settings. Replication studies for other countries are warranted.

Keywords: claims data, health insurance, scale‐up, Tanzania, universal health coverage

1. INTRODUCTION

Universal health coverage has been high on the global health agenda for the last decade (Boerma et al., 2014; WHO, 2005). Universal health coverage means that all people obtain quality health services without suffering financially as a result of seeking health care (WHO, 2010). However, across low‐ and middle‐income countries (LMICs), high out‐of‐pocket (OOP) health spending still persists and impoverishes households (Wagstaff et al., 2020). Reducing OOP health service expenditure can be accomplished by expanding free health care services at point of use, scaling up health insurance coverage, or—most frequently—a mixture of both (WHO, 2020).

The number of countries in Africa with national health insurance is gradually increasing (WHO, 2019). However, the percentage of the population enrolled in health insurance remains low. Many African countries have enrollment rates below 10%, with the notable exceptions of Rwanda, which reached enrollment rates of about 90% in 2015 (Chemouni, 2018) and Ghana with an enrollment rate of 56% in 2014 (Amu et al., 2018). Ghana and Rwanda are also two of the very few countries in Africa where enrollment is mandatory for the entire population (McIntyre et al., 2018).

But several challenges exist for LMICs trying to scale up health insurance coverage. On the demand side, poor populations may be unable to pay insurance premiums (Msuya et al., 2007), do not trust the health system (Kamuzora & Gilson, 2007; Maluka & Bukagile, 2014), perceive the quality of care to be low (e.g., due to frequent drug stock‐outs) (Linje, 2015; Macha et al., 2014), struggle to understand the benefits of health insurance (Kapologwe et al., 2017; Obrist et al., 2007; Panda et al., 2015), have limited awareness of benefit packages (Kapologwe et al., 2017; Kumburu, 2015) or are discouraged by prolonged registration processes (Banerjee et al., 2021; Kumburu, 2015). From the insurers' perspective, large informal sectors make it difficult to enroll people through employers and to calculate affordable income‐based premiums (Borghi et al., 2013; Fenny et al., 2018). Moreover, since coverage rates are still very low and the voluntary enrollment in most countries leads to adverse selection of the population insured, it is hard to estimate which health services would be used most often in LMICs and the costs of covering the entire population.

Previous studies on health insurance in LMICs have mainly relied on household survey data. Various studies have examined factors associated with health insurance enrollment (Amu et al., 2018; Proaño Falconi & Bernabé, 2018; Salari et al., 2019). Other studies have shown that health insurance coverage in LMICs is correlated with decreased OOP expenditure (Aryeetey et al., 2016; Chua & Sommers, 2014; King et al., 2009; Thornton et al., 2010), decreased catastrophic health expenditure (Baicker et al., 2013; Barasa et al., 2017; Kusi et al., 2015) and increased health service usage (Blanchet et al., 2012; Chomi et al., 2014; Fiestas Navarrete et al., 2019; Ghislandi et al., 2015; Simon et al., 2017). There is mixed evidence of improved health outcomes (Abrokwah et al., 2014; Mensah et al., 2010; Robyn et al., 2012; Sommers et al., 2016, 2017; Wang et al., 2009).

For high‐income countries (HICs), insurance claims data are also frequently used to study service utilization (Cicero et al., 2009; Kotzan et al., 2001) and health care costs (Cai et al., 2014; Nasseh et al., 2016; Schwarzkopf et al., 2013). Claims data have several advantages compared to survey data, including lower costs for data collection, larger sample sizes, more frequent data points, greater detail and accuracy related to diseases and medicines prescribed. Moreover, such administrative data has lower susceptibility to survey biases linked to attrition, social desirability or recall (Finkelstein & Taubman, 2015). Disadvantages of using claims data include fewer variables than household surveys and that they only cover insured people.

To our knowledge, very few studies have analyzed health insurance claims data for African countries. Two studies in South Africa use only a small sub‐sample of claims to determine chronic disease risk factors (Kolbe‐Alexander et al., 2008) and to predict survival rates of HIV‐infected adults (Nachega et al., 2010). In Ghana, claims from the National Health Insurance Scheme have been analyzed to determine the most frequently used medicines (Ankrah et al., 2018).

In this study we use a rich administrative dataset from the Tanzanian National Health Insurance Fund (NHIF) to study which policyholders use which types of services, drugs, and health facilities, how often and the associated costs. We merge the NHIF policyholder data with the 2016 NHIF claims data and data on the geographic location of health facilities in Tanzania. This analysis is unique in that it is the first comprehensive analysis of a large‐scale mandatory health insurance database for any African country. Moreover, as the health insurance we analyze is mandatory for an entire population group in Tanzania, the results should also be less biased by adverse selection of high‐risk groups. Hence, this study should substantially advance our understanding about the opportunities and barriers to scaling up health insurance coverage in a low‐income setting. Although only data from 2016 is available, we assume that the general insights and implications are still relevant today: NHIF coverage rates have stayed almost the same over the last five years (7% in 2016 and 8% in 2021) and a Single National Health Insurance (SNHI) is under discussion. 1

2. STUDY SETTING AND CONTEXT

Tanzania has experienced relatively high economic growth per capita since the year 2000, averaging 4% per year (see Table 1). But in 2016, the Gross Domestic Product (GDP) per capita was still only 2926 US$ and the national poverty rate at 28% (World Bank, 2021). Indicators of health outcomes and health care access have also improved for Tanzania over the last decade (see Table 1). Between 2007 and 2016, life expectancy at birth increased from 56 to 64 years, the under‐five mortality rate decreased from 84 to 57 per 1000 live births and maternal mortality from 685 to 539 per 100,000 live births. Health access indicators are still lower than in neighboring Kenya and Rwanda, but higher than the average on the African continent (World Bank, 2021).

TABLE 1.

Country characteristics from Tanzania and neighboring countries for the year 2016

| Tanzania | Kenya | Rwanda | SSA | |

|---|---|---|---|---|

| Macroeconomic indicators | ||||

| GDP per capita, PPP (current international $) | 2926 | 3122 | 1978 | 3802 |

| GDP per capita growth (annual %) | 4 | 3 | 3 | −1 |

| Poverty headcount ratio at $1.90 a day (2011 PPP) (% of population) | 49 | 37 | 56 | 41 |

| Population growth (annual %) | 3 | 2 | 3 | 3 |

| Fertility rate, total (births per woman) | 5 | 4 | 4 | 5 |

| Health (access) indicators | ||||

| Life expectancy at birth, total (years) | 64 | 65 | 68 | 60 |

| <5 mortality rate (per 1000 live births) | 57 | 44 | 39 | 82 |

| Maternal mortality ratio (per 100,000 live births) | 539 | 346 | 260 | 545 |

| Births attended by skilled health staff (% of total) | 64 | 62 | 91 | 58 |

| Pregnant women receiving prenatal care (%) | 98 | 96 | 99 | 82 |

| Health finance indicators | ||||

| Government health expenditure per capita, PPP (current international $) | 45 | 52 | 44 | 69 |

| Current health expenditure per capita, PPP (current international $) | 112 | 144 | 130 | 198 |

| Current health expenditure (% of GDP) | 4 | 5 | 7 | 5 |

| Out‐of‐pocket expenditure per capita, PPP (current international $) | 25 | 40 | 8 | 73 |

| Out‐of‐pocket expenditure (% of current health expenditure) | 22 | 28 | 6 | 37 |

| Health insurance indicator | ||||

| Coverage of health insurance schemes (% population) | 32% | 20% | 87% | ‐‐ |

Note: Health insurance coverage consists in Tanzania of 7% National Health Insurance Fund and 25% Community Health Fund (2018); Kenya 19% National Health Fund and 1.3% Community‐based Health Insurance (2016); Rwanda 82% Community Based Health Insurance and 5% formal sector insurance (MMI, RAMA) (2016).

Abbreviations: GDP, Gross Domestic Product; MMI, Military Medical Insurance; PPP, Purchasing Power Parity; RAMA, Rwandaise d’Assurance Maladie; SSA, sub‐Saharan Africa.

Total annual health expenditure per capita for Tanzania is 112 US$, similar to other African countries, corresponding to around 4% of the GDP per capita (World Bank, 2021). Average per capita OOP expenditure in Tanzania (25 US$ per year) is lower than in other African countries (73 US$). However, neighboring Rwanda, with the highest insurance coverage in sub‐Saharan Africa (SSA), has significantly lower per capita OOP expenditure (8 US$ per year). Rwanda also shows that it is technically possible for a country to include the informal sector and rural workers into a mandatory health insurance scheme, with 80% of these sectors being enrolled, and 90% of the total population (Chemouni, 2018).

Tanzania's main voluntary insurance for informal rural sector workers, the Community Health Fund (CHF), 2 covers around 25% of the population (NHIF, 2018). In total, 32% of the Tanzanian population possesses health insurance. The health insurance structure in Tanzania is highly fragmented, however, with many small schemes targeting different population groups (Amu et al., 2018; Chomi et al., 2014; McIntyre et al., 2008). The government aims to unify existing schemes into one national health insurance fund and to extend health insurance coverage to the entire Tanzanian population (MoHCDGEC, 2019). In addition to reaching the entire population, a major question is how to set affordable premiums for various socioeconomic groups while keeping the national scheme financially solvent (Renggli et al., 2019; Lee et al., 2018a, 2018b).

In this study, we analyze claims data from the NHIF, a mandatory health insurance for all Tanzanian public sector employees covering 7% of the population. 3 Employees contribute 6% of their monthly salary as a premium (on average 669,109 Tanzanian shilling (TZS); around 288 US$ per year), 3% paid by them and 3% paid by their employer. Compared to the 15% on wages paid in Rwanda, this premium is low, especially for a scheme covering formal sector workers. 4 The premium covers public servants, but also the spouse, parents of both sides, and up to four children younger than 18 years within the household. The NHIF currently provides a wide range of benefits (see Appendix Table A1) and few health services require special approval from the NHIF. 5 These include cancer, dialysis, dental treatments, scan diagnostics and reading glasses. National Health Insurance Fund members are entitled to use care from the network of accredited health facilities, including both public and private facilities. According to official records, 79% (n = 7390) of all health facilities in Tanzania were accredited in 2019 (MoH, 2019). All covered services are provided free of charge to members of the NHIF in accredited health facilities. The health facility then submits a claim to NHIF for reimbursement of any costs incurred.

From a financial perspective, the NHIF is by far the largest insurance scheme in Tanzania, with over 480,000 million TZS (around 206 million US$) in annual revenue (NHIF, 2018). The scheme's annual surplus has, however, decreased every year since 2014/2015, from 148,000 million down to 32,000 million TZS in 2017/2018 (NHIF, 2018). Although this trend is not an immediate problem, it has already raised concerns related to long‐term financial sustainability, especially since there are discussions about whether to subsidize insurance premiums or services for informal and rural populations (Lee et al., 2018b). If NHIF barely generates annual surplus, the opportunity for cross‐subsidy will be lost and the ultimate aim to extend health insurance coverage to the entire Tanzanian population will become financially unfeasible. The key objective of this analysis is to better understand the financial sustainability of NHIF and to identify cost drivers for the insurance scheme.

3. DATA & ANALYTICAL STRATEGY

The analysis is based on three data sources: the NHIF policyholder database (2016 and 2017), the NHIF claims database (2016), and the Health Facility Registry database (for more details, see Table A2 in the Appendix). To receive the NHIF policyholder and the NHIF claims database, ethical clearance was obtained from the Ifakara Health Institute (IHI) Institutional Review Board (IHI/IRB/EXT/No:028–2016) and the Tanzanian National Institute for Medical Research (NIMR/HQ/R.8a/Vol.IX/2340). The Health Facility Registry database is publicly available on the Internet (MoH, 2019).

3.1. National Health Insurance Fund policyholder data

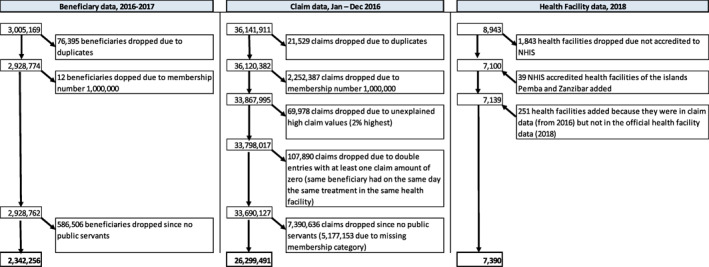

The NHIF policyholder dataset includes all persons registered in the NHIF in 2016 and 2017. The original sample is comprised of 3,005,169 insured (including both premium‐paying principals and their dependents). Although originally designed and implemented to provide compulsory health insurance for public servants, the NHIF started to expand its coverage in 2012 to other groups who can join on a voluntary basis, as part of a first effort to cover the entire population. For this study, only the mandatory membership group “public servants” (including police, councilors, members of parliament and public employees) and their dependents is used to keep adverse selection due to self‐selected, high‐risk individuals from biasing the results. 6 In fact, we observe adverse selection for the voluntarily insured, as the 586,506 individuals who are not public servants have significantly higher costs per person than the mandatory insured public servant group: 7160 TZS versus 4833 TZS. Moreover, 76,407 entries were duplicates (2.5%) and were excluded from the analysis.

This leaves a total of 2,342,256 policyholders, or 4.42% of the Tanzanian population. The database includes the following information: anonymized membership number, birth date, gender, whether the person is the premium‐paying principal or a dependent (spouse, child, parent, others), the insurance contribution per year (premium) and the principal's salary. A limitation of this dataset is that the region where the policyholder lives is not recorded. However, the location of the health facility is available for persons with a claim in 2016.

The sample of mandatory public servants and their dependents is different from the Tanzanian population as follows (see Table 2). First, it is older: whereas the age group 0–19 years old is underrepresented, the age groups 20–69 and especially 50–69 are overrepresented. One reason could be that public servants have fewer children, on average, than the general population (Mturi & Hinde, 1994; Vavrus & Larsen, 2003). No significant gender differences in the distribution can been detected. However, public servant employees receive, on average, a higher monthly salary of 500,001–900,000 TZS (around 215–386 US$, or 2580‐4632 US$ per year) compared to the average formal sector worker in Tanzania (300,000–500,000 TZS) (Tanzania National Bureau of Statistics, 2018a). The informal sector, which accounts for 76% of the non‐agricultural workforce in Tanzania, is very likely to have even lower incomes (Oxford Business Group, 2021).

TABLE 2.

Distribution of National Health Insurance Fund (NHIF) public servant policyholder by age, gender (2016/2017) compared to the total population

| Distribution NHIF policyholder 2016/17, % | NHIF policyholder 2016/17, % population | Distribution total population based on CENSUS 2012, % | |

|---|---|---|---|

| Age | |||

| <5 | 9.72 | 2.32 | 18.54 |

| 5–9 | 10.19 | 2.64 | 17.05 |

| 10–19 | 14.14 | 2.68 | 23.30 |

| 20–29 | 21.73 | 6.28 | 15.28 |

| 30–39 | 15.02 | 6.21 | 10.68 |

| 40–49 | 10.02 | 6.29 | 7.03 |

| 50–59 | 10.54 | 12.47 | 3.73 |

| 60–69 | 5.24 | 10.28 | 2.25 |

| 70–79 | 2.35 | 8.05 | 1.29 |

| 80–89 | 0.88 | 8.11 | 0.48 |

| 90+ | 0.17 | 1.99 | 0.38 |

| Total | 100.00 | 4.42 | 100.00 |

| Gender | |||

| Male | 48.45 | 4.43 | 48.28 |

| Female | 51.55 | 4.40 | 51.72 |

| Total | 100.00 | 4.42 | 100.00 |

Note: Unit is per person (NHIF policyholder n = 2,342,256). The NHIF policyholder 2016/17 and % population was calculated as: number of NHIF policyholder 2016/2017 in a certain age/gender group divided by number of total population based on CENSUS 2012 in a certain age/gender group. The Census data was retrieved from IPUMS (2020).

A comparison of the number of public servant employees enrolled (principal members) with data from the official public employee and earnings survey (EES) from 2016 (Tanzania National Bureau of Statistics, 2018a) suggests that although enrollment is mandatory for public servant employees, in practice 72% 7 of all public servants are enrolled under NHIF. However, the younger public servants (between 15 and 35 years old) show almost full coverage rates (94%), whereas older public servants (36+ years) have a lower enrollment rate. This implies that some public servants seem to be able to choose not to be insured (e.g., contract not yet renewed). Thus, unobserved adverse selection where low health risk individuals do not insure cannot be completely ruled out. However, it is substantially lower than in any voluntary insurance schemes, in particular given that we observe nearly full coverage among young public servants.

3.2. National Health Insurance Fund claims data

The NHIF claims database includes all NHIF claims for health services used by NHIF policyholders in the year 2016. The original number of claims is 36,141,911. 8 Since we only focus on the mandatory membership group of public servants for the final analysis, which represent 73% of the total claim data in 2016, the total sample size is 26,299,491 claims. The claims database includes the following information: anonymized membership number, birth date, gender, treatment date, claim value, facility registered name, facility type, facility ownership, region, district and claim details (treatment type, e.g., X‐Ray, Ibuprofen). 9 A limitation of the data is that the claim details only describe the treatment without reporting a diagnosis. Therefore, we can only make reasonable assumptions regarding the underlying disease for a selected number of claim types, for example, anti‐malaria drug to treat malaria or dialysis for kidney‐related diseases. In contrast, antibiotics could be used for all kinds of bacterial diseases.

3.3. Health Facility Registry

The Health Facility Registry, maintained by the Ministry of Health, Community Development, Gender, Elderly and Children (MoHCDGEC), provides information on the main characteristics of all health facilities in Tanzania in 2018 (MoH, 2019). This dataset lists a total of 8943 health facilities from mainland Tanzania, 10 of which 7100 (79.8%) are NHIF accredited, suggesting that the NHIF accreditation process is relatively easy. For each health facility, we have information on the facility ID, the registered name, the common name, the facility type (dispensary/pharmacy, health center, hospital, clinic, 11 health lab), ownership (public, private), and the geographical location (region, district, council, ward, village/street), including Global Positioning System coordinates. Information on 39 accredited health facilities for the islands Pemba and Zanzibar are also included. Moreover, 251 health facilities that are listed in the claims dataset from 2016 were included in our final dataset, although they are not listed in the Health Facility Registry of 2018. The final analysis thus covers 7390 NHIF accredited health facilities. Policyholders covered by the NHIF can only access health services through accredited health facilities in Tanzania.

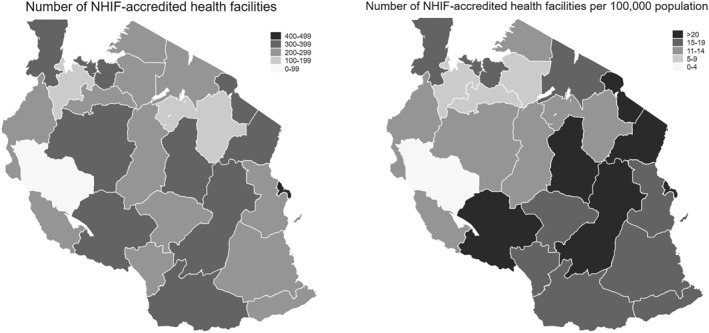

Around 75% of all NHIF‐accredited health facilities are public health facilities and the remainder are private. Primary health care, such as dispensaries and pharmacies (84.4%), account for the vast majority of NHIF‐accredited health facilities. NHIF‐accredited health facilities are scattered all over Tanzania, but are also concentrated in certain regions: the number of NHIF‐accredited health facilities is particularly high in the regions of Dar es Salaam (7% of all accredited facilities), Dodoma (5.3%), Tanga (5.2%) and Morogoro (5%), and low in Katavi (1.1%), Geita (2.2%) and the islands (below 1%). Accounting for population density, regions with a high number of health facilities per 100,000 inhabitants are Dodoma, Morogoro and Kilimanjaro (more than 23 health facilities per 100,000 inhabitants), whereas low rates can be found in Katavi, Geita, Simiyu and Shinyanga (less than 10 health facilities per 100,000 inhabitants) (see Figure A1 in the Appendix). Hospitals, clinics, and health labs are more frequent in Tanzania's largest city, Dar es Salaam.

3.4. Analytical strategy

In a first step, we merged the three databases. The NHIF policyholder and claims databases were merged using three uniquely identifying variables: anonymized membership number, birth date, and gender. Forty‐seven percent of policyholders were matched with at least one claim, meaning that 53% of people enrolled in the health insurance appeared not to have used any health services in 2016. However, 14% of all claims (corresponding to around 204,751 unique membership numbers) could not be matched to the policyholder database. These claims were excluded from the final analysis for the policyholders because no information about membership characteristics was available. The claims and health facility databases were merged using five uniquely identifying variables: facility name, region, district, facility type, and ownership. OpenRefine software was used in order to clean identifying variables, since different naming and misspelling made it impossible to merge all facilities directly.

In a second step, we analyzed the three datasets to answer the following four questions with the objective of better understanding the usage pattern, cost drivers, and financial sustainability of a mandatory insurance scheme in a low‐income setting:

Which policyholders have the greatest utilization and costs of health care services?

What is the financial sustainability for national scale‐up of a mandatory health insurance?

Which services are used the most and at what cost?

Which health facilities have the greatest utilization and at what cost?

The first research question, “Which policyholders have the greatest utilization and costs of health care services?”, contributes to existing studies showing that health insurance enrollment increases health care utilization among the insured compared to the uninsured (Chomi et al., 2014; Fiestas Navarrete et al., 2019; Ghislandi et al., 2015; Simon et al., 2017). To answer it, we first show the distribution of policyholders and their utilization in a concentration curve. Then, we estimate three regressions to explain which people with insurance take up at least one health care service per year, how many times health care services are used and, the total claim value per policyholder (in log scale, see Section 4.1). A logistic regression is used to analyze what type of policyholder is more likely to make a claim and a Tobit‐model 12 is used to assess the drivers of the number of claims per person.

The second research question, “What is the financial sustainability for national scale‐up of a mandatory health insurance?”, contributes to the discussion of scaling up health insurances in many LMICs (e.g., WHO, 2019). We estimate the expected total health expenditures as well as the required premiums if such insurance is made mandatory for the entire population (see Section 4.2). We apply a simple back‐of‐the‐envelope calculation using the coefficients (on age, gender, and income) from our results in Section 4.1 13 and the population shares from Table 2 and extrapolate it to Tanzania Census Data (IPUMS, 2020) from 2012, which provides information on population characteristics. We assume that disease burdens and behavior are the same for the entire population as they are for public servants—controlling for differences in age, gender, and income. Since we only include the mandatory membership group in our analysis, we avoid possible biases due to adverse selection in the form of self‐selected high‐risk individuals into the insurance (see Section 3.1) when predicting mandatory national health insurance costs.

The third research question, “Which services are used the most and at what cost?”, provides insights into the claim details to learn more about drug and health service utilization in low‐income settings that has so far been hampered by a lack of access to such databases (Ankrah et al., 2018). In two descriptive tables, we first analyze the cost structure of claims by service type and second, we analyze the most frequent service details (see Section 4.3).

Finally, the fourth research question, “Which health facilities have the greatest utilization and at what cost?”, contributes to the few studies about equity in access to health services examining the general utilization of health care facilities based on household surveys (Chomi et al., 2014; Fiestas Navarrete et al., 2019; Ghislandi et al., 2015; Simon et al., 2017) and health facility surveys (Baker et al., 2015; Do et al., 2016; Kanyangarara et al., 2018). We first provide descriptive insights about all health facilities in Tanzania by type and ownership status. Second, we show the distribution of health facilities and their costs in a concentration curve. Third, we analyze in three regressions which health facilities had at least one NHIF claim per year, how many times health care services are used, and the total claim value per health facility (in log scale, see Section 4.4). Similar to the method used to answer the first research question, a logistic regression is used to analyze what type of health facility is more likely to receive a claim and a Tobit‐model is used to assess the drivers of the number of claims per health facility.

Overall, the results of the four research questions will be put in context of the findings from other countries to better understand the magnitude of the results. Since access to such databases in LMICs is still lacking, we mostly compare our results with data from HICs that is publicly available (e.g., AOK, 2019; Dieleman et al., 2020; EDI, 2020; Vuffray, 2018; Wieser et al., 2014). These results will highlight whether we can rely on studies from HICs or if more studies from LMICs are warranted.

4. RESULTS

4.1. Usage and costs of the mandatory insurance by policyholders

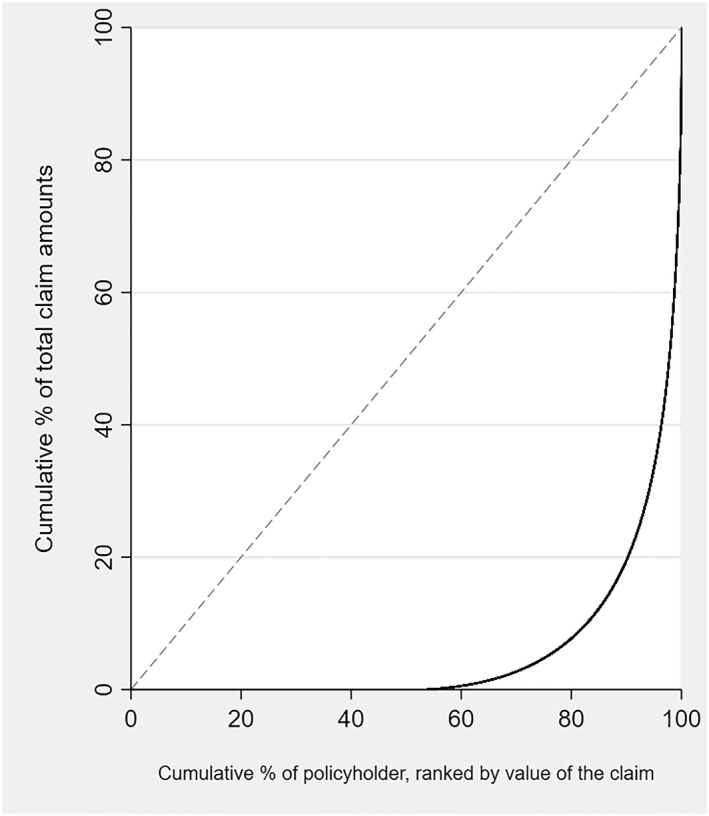

In 2016, out of the 2,342,256 public servants and their dependents enrolled in the mandatory NHIF, only 47% made at least one claim during the year. From these 1,100,860 beneficiaries, 26,299,491 claims were recorded in our database. To our knowledge, such information is not available for any other LMICs. Compared to HICs for which data is available for some selected countries, this is a rather low percentage of policyholders using any health services. In Switzerland, 14 for example, 84% of people enrolled in mandatory health insurance used at least one service in 2018 (EDI, 2020). Moreover, only a small percentage of policyholders (10%) in the NHIF account for most of the health care expenditure (80%) (see Figure 1). Expenditures appear to be somewhat less concentrated in mandatory health insurances in HICs. For example, claims data from the mandatory Swiss health insurance shows that 20% of the insured accounted for 80% of the costs (Vuffray, 2018).

FIGURE 1.

Concentration curves of total National Health Insurance Fund (NHIF) claim amounts by policyholder. The 45° line would indicate that each policyholder accounts for the same amount of costs.

On average, the total claim value of a policyholder (including those with zero claims) in a single year was 76,166 TZS (33 US$). This corresponds to about 1% of the average yearly income of a public servant and around 20% of the yearly insurance fee paid by employer and employee. However, only 26% of policyholders actually pay an insurance premium, whereas 74% are non‐paying “dependents” (including spouse, up to four children, and parents). Therefore, the average total claim value for each family (with 3.6 members, on average) consists of 3.6% of the average salary of the principal public servant and about 60% of the estimated yearly insurance fee. While, this rate is still low compared to some HICs, such as Switzerland, where total claim value per policyholder is on average 90% of the yearly mandatory insurance fee (AOK, 2019; Dieleman et al., 2020; EDI, 2020), it is important for NHIF to run a surplus with public servants in order to achieve universal health coverage, as insurance schemes for poor informal and rural populations need to be subsidized (Lee et al., 2018b).

Analyzing which policyholder characteristics are more likely to be associated with at least one claim within a year (Table 3, Column I), we show that women are 1.3 times more likely to have a claim than men, and people in the older working age population (30–59 years old) are around 1.2 times more likely than younger professionals (20–29 years old) and the oldest age groups to have a claim. Moreover, the lowest‐ and highest‐income groups have significant lower probability to take up at least one health care service than the reference middle‐income category. The results for women are in line with other countries, whereas the differences between age groups are surprising. In other countries, children under 5 years old and the elderly usually use more health services than working‐age adults (Dieleman et al., 2020; EDI, 2020). However, comparing the results to the nationally representative Demographic and Health Survey of 2015 in Tanzania, we find a similar pattern for the age groups (DHS, 2021). It is possible that lower recorded usage rates for children below five in Tanzania occur because some health services for children are provided for free. The result for income groups might be driven by the highest‐salary group having enough money to visit private non‐accredited health facilities and/or being in better health (Fichera & Savage, 2015). On the contrary, the lowest‐salary group might sometimes not even be able to afford to travel to a health provider and/or miss work and/or live in a rural area with worse health care access (see Figure A1 in Appendix and Salari et al., 2019). 15

TABLE 3.

Factors correlated with take‐up of services, number of claims and value of claim per policyholder

| (I) | (II) | (III) | |

|---|---|---|---|

| Policyholder had a claim | Number of claims per policyholder | Total value of claims (log) per policyholder | |

| Logit odds ratio | Tobit‐Coefficient | Tobit‐Coefficient | |

| Status (ref. Principal) | |||

| Dependent | 1.000 (0.997) | 0.412 (0.000) | 0.053 (0.003) |

| Gender (ref. Male) | |||

| Female | 1.337 (0.000) | 7.691 (0.000) | 1.724 (0.000) |

| Age (ref. 20–29 years) | |||

| <5 | 0.822 (0.000) | −1.564 (0.000) | −0.968 (0.000) |

| 5–9 | 1.140 (0.000) | 1.464 (0.000) | 0.538 (0.000) |

| 10–19 | 0.969 (0.000) | −3.501 (0.000) | −0.388 (0.000) |

| 20–29 ref. group | |||

| 30–39 | 1.256 (0.000) | 5.122 (0.000) | 1.318 (0.000) |

| 40–49 | 1.239 (0.000) | 6.230 (0.000) | 1.357 (0.000) |

| 50–59 | 1.107(0.000) | 6.386(0.000) | 0.854 (0.000) |

| 60–69 | 0.896 (0.000) | 4.618 (0.000) | −0.142 (0.000) |

| 70+ | 0.928 (0.000) | 7.119 (0.000) | 0.201 (0.000) |

| Monthly salary (ref. 500,001–900,000 TZS) | |||

| <150,000 | 0.570 (0.000) | −9.605 (0.000) | −2.999 (0.000) |

| 150,001–300,000 | 1.202 (0.000) | 4.078 (0.000) | 0.988 (0.000) |

| 300,001–500,000 | 0.893 (0.000) | −1.964 (0.000) | −0.579 (0.000) |

| 500,001–900,000 ref. group | |||

| 900,001–1,200,000 | 0.920 (0.000) | −1.127 (0.000) | −0.421 (0.000) |

| 1,200,001–1,500,000 | 0.903 (0.000) | −1.096(0.000) | −0.281 (0.000) |

| >1,500,000 | 0.247 (0.000) | −25.041 (0.000) | −7.965 (0.000) |

| Constant | 0.979 (0.000) | −6.747 (0.000) | 1.301 (0.000) |

| Observations | 2,342,255 | 2,342,255 | 2,342,255 |

| Pseudo R‐squared | 0.054 | 0.013 | 0.019 |

Note: Unit is per policyholder (n = 2,342,256). P‐values in parenthesis. Average age (20–29) and average salary (500,001–900,000 TZS) category were used as reference categories.

Abbreviation: TZS, Tanzanian shilling.

Each beneficiary who took up a health service had a median of 15 claims per year and an average of 24 claims. Since several claims can be recorded per visit, the results seem plausible. Overall, all policyholders (including those with zero claims) had an average of 11 claims. Each beneficiary who took up at least one health service (i.e., had a recorded claim) had a median of 3 visits per year (average is 4.5 visits). As a result of high take‐up rates and a high number of claims, again women, the middle‐income group and the population group aged 30–59 had the highest total costs (see Column (III) in Table 3). This result is particularly surprising for the age groups. For example, in Switzerland, costs increase with age and the elderly incur costs up to 15 times higher than young adults (EDI, 2020), while in the US, children below the age of one incur costs almost 10 times higher than children aged 5–9 years (Dieleman et al., 2020).

4.2. The costs of scaling up a health insurance

If covered health services would not change (see Section 4.1), total health claims for Tanzania would amount annually to 3300 billion TZS (1.4 billion US$) or 62,350 TZS (27 US$) per person. Revenues could rise to around 750 billion TZS (320 million US$) per year if all formal sector employees (5% of Tanzanians) would contribute similarly as currently public servants, that is, 6% of their average salary. 16 If formal sector employees would contribute 15% of their salaries (as in Rwanda, see Footnote 4), collected funds would increase to 1900 billion TZS (820 million US$). Hence, a mandatory scheme would require additional funding of between 1400 and 2500 billion TZS (0.6–1.0 million US$) per year. 17 This would correspond to about 25%–45% of current annual government health expenditures (Purchasing Power Parity, see Table 1) that would have to be financed out of taxes or international contributions to the Tanzanian health budget.

Another option would be to ask the remaining informal workforce (42% of the total Tanzanian population) to contribute with 65,000–116,000 TZS or 25–50 US$ per year to the insurance fund, which might be difficult, given that 26% of the population in Tanzania lives on less than 589,703 TZS (256 US$) a year (Tanzania National Bureau of Statistics, 2018b), that is, they would have to contribute 10%–20% of their annual income. In Rwanda, the country with by far the highest health insurance coverage rate on the African continent, premiums for the lowest‐income group in the informal sector are entirely paid by the government, the middle‐income group in the informal sector pays 3000 RwF per person per year (3 US$), and the highest‐income group in the informal sector pays 7000 RwF per person per year (7 US$). Moreover, the informal workforce has a more limited service package in Rwanda than the full paying formal employees (15% of gross salary), which raises equity concerns. Policy makers in Tanzania could decrease costs by redefining the essential service package (for the entire population) or health facilities to be covered (gatekeeping). 18 Sections 4.3 and 4.4 will provide some first insights for possible avenues to consider.

4.3. Cost drivers of the mandatory insurance by health services

Three‐fourths of all claims were made for medicines (e.g., paracetamol), consumables (e.g., dispensing bag), and diagnostic examinations (e.g., malaria blood smear test) (Table 4). The mean claim values for these three categories are, however, rather low, at around 5000–6000 TZS (2–3 US$) per claim. In contrast, inpatient and surgical charges, which account for fewer than 1% of total claims, are much more expensive per claim, and thus these claims together account for 14% of the total claim value. For example, the mean claim value for surgical charges (e.g., C‐sections) is 259,948 TZS (112 US$), over 50 times higher than the mean claim value for medicine. Since no similar data is currently available for other LMICs, we can again only compare to HICs. Total claim amounts for medicines and consumables are twice as high as a share of total costs in Tanzania (40%) compared to HICs, where they account for less than 20% of total costs (AOK, 2019; Dieleman et al., 2020; EDI, 2020). One reason for this difference could be that costs of inpatient services are higher in HICs; another reason is that they conduct more inpatient procedures. We do not expect that the observed difference is caused by higher prices for medicines or higher use of medicines in HICs (Ankrah et al., 2018; Horumpende et al., 2018; Klein et al., 2018).

TABLE 4.

National Health Insurance Fund (NHIF) claims by service types

| Number of claims | Claim amount (in TZS) | ||||||

|---|---|---|---|---|---|---|---|

| Frequency | Percent | Sum (million) | Percent | Mean | Median | Max (million) | |

| Consultation charges | 4,666,349 | 17.75 | 28,459 | 16.03 | 6099 | 2000 | 1.96 |

| Medicine & consumables | 14,225,609 | 54.12 | 74,328 | 41.86 | 5225 | 1500 | 23.69 |

| Diagnostic examination | 6,848,748 | 26.06 | 35,017 | 19.72 | 5113 | 2000 | 2.00 |

| Inpatient charges | 123,210 | 0.47 | 11,472 | 6.46 | 93,110 | 32,500 | 32.50 |

| Surgical charges | 53,662 | 0.20 | 13,949 | 7.86 | 259,948 | 130,000 | 6.00 |

| Procedural charges | 243,254 | 0.93 | 12,121 | 6.83 | 49,827 | 10,000 | 15.45 |

| Other charges | 124,642 | 0.47 | 2206 | 1.24 | 17,697 | 15,000 | 8.00 |

| Total | 26,285,474 | 100.00 | 177,531 | 100.00 | 6754 | 2000 | 32.50 |

Note: Unit is per claim (n = 26,299,491). 14,017 claims have missing values for service type.

Abbreviation: TZS, Tanzanian shilling.

We are further able to investigate the frequency and costs of specific health treatments. Table 5 shows the 10 most frequently used health services, the 10 most expensive health services, and the 10 health services that account for the highest total costs. 19 The most often used medicines are pain killers (e.g., Ibuprofen + Paracetamol, 7.1%), antibiotics (e.g., Amoxycillin, 2.4%), anti‐malaria drugs (e.g., Artemether + Lumefantrine, 1.5%) and treatments for eye infections (e.g., Ciprofloxacin, 1.3%). These findings are consistent with an analysis of the National Health Insurance Scheme in Ghana, which showed that painkillers, anti‐malaria drugs, anti‐infectives and antihypertensives are the most prescribed drugs (Ankrah et al., 2018). In addition, diagnostics for a broad variety of disease detection such as urine (5.7%), malaria blood smear (5.1%), and stool analysis (2.3%) are often used.

TABLE 5.

List of Top 10 most frequent service details (in TZS)

| Servicedetail | Service type | Number of claim [% total] | Mean claim value (in TZS) | Total claim value (in million TZS) [% total] |

|---|---|---|---|---|

| Top 10 service details: Sorted by number of claims | ||||

| Ibuprofen + paracetamol (pain) | Medicine | 1,859,265 [7.1%] | 444 | 826 [0.5%] |

| Dispensing bag | Consumables | 1,535,436 [5.8%] | 38 | 58 [0%] |

| Urine analysis | Diagnostic | 1,503,470 [5.7%] | 1680 | 2527 [1.4%] |

| Malaria blood smear (B/S) | Diagnostic | 1,352,523 [5.1%] | 1701 | 2301 [1.3%] |

| Amoxycillin (antibiotics) | Medicine | 638,543 [2.4%] | 2466 | 1575 [0.9%] |

| Stool analysis | Diagnostic | 604,499 [2.3%] | 1588 | 960 [0.5%] |

| Full blood picture (FBP) | Diagnostic | 412,369 [1.6%] | 6220 | 2565 [1.4%] |

| Artemether + Lumefantrine (malaria) | Medicine | 397,579 [1.5%] | 1739 | 691 [0.4%] |

| Metronidazole (antibiotics) | Medicine | 382,269 [1.5%] | 1588 | 607 [0.3%] |

| Ciprofloxacin (eye drops) | Medicine | 340,153 [1.3%] | 2589 | 881 [0.5%] |

| Top 10 service details: Sorted by mean claim value | ||||

| CABG ‐ coronary artery bypass graft | Procedural | 1 [0%] | 15,450,000 | 15 [0%] |

| Mitral valve replacement | Procedural | 4 [0%] | 10,780,000 | 43 [0%] |

| Mitral valve replacement + tricuspid valve repair ‐ devega's | Procedural | 1 [0%] | 10,780,000 | 11 [0%] |

| Dual chamber pace maker insertion (incl. Pace maker device) | Procedural | 3 [0%] | 10,500,000 | 32 [0%] |

| Trastuzumab/Herceptin (cancer) | Medicine | 224 [0%] | 9,836,429 | 2203 [1.2%] |

| Mitral valve repair | Procedural | 4 [0%] | 9,650,000 | 39 [0%] |

| Ventral septal defect (VSD) closure | Procedural | 11 [0%] | 8,850,000 | 97 [0.1%] |

| Tetralogy of fallot (TOF) repair | Procedural | 7 [0%] | 8,850,000 | 62 [0%] |

| Atrial septal defect (ASD) closure | Procedural | 1 [0%] | 8,850,000 | 9 [0%] |

| Atrio‐ventricular canal repair | Procedural | 1 [0%] | 8,850,000 | 9 [0%] |

| Top 10 service details per service type: sorted by total claim value | ||||

| Hemodialysis per session | Procedural | 16,434 [0.1%] | 384,005 | 6311 [3.5%] |

| Amoxycillin + Clavulanic acid (antibiotics) | Medicine | 169,797 [0.6%] | 19,743 | 3352 [1.9%] |

| Caesarian section (C/S) | Surgical | 8189 [0%] | 392,593 | 3215 [1.8%] |

| Full blood picture (FBP) | Diagnostic | 412,369 [1.6%] | 6220 | 2565 [1.4%] |

| Urine analysis | Diagnostic | 1,503,470 [5.7%] | 1680 | 2527 [1.4%] |

| Malaria blood smear (B/S) | Diagnostic | 1,352,523 [5.1%] | 1701 | 2301 [1.3%] |

| Trastuzumab/Herceptin (cancer) | Medicine | 224 [0.0%] | 9,836,429 | 2203 [1.2%] |

| Hydrochlorthiazide + Losartan (blood pressure) | Medicine | 100,859 [0.4%] | 21,823 | 2201 [1.2%] |

| Gabapectin/Gabatin‐300 (neuropathic pain related diseases) | Medicine | 52,036 [0.2%] | 37,893 | 1972 [1.1%] |

| Raberprazole/Rabeloc (stomache acid related diseases) | Medicine | 58,081 [0.2%] | 32,520 | 1889 [1.1%] |

Note: Registration and consultation charges included registration and consultation fees; Inpatient charges included accommodation fees or intensitive care unit service charges. Both categories are not included in the table. Total number of claims in 2016 is 26,299,491 and total claim value is 178,400 million TZS.

Abbreviation: TZS, Tanzanian shilling.

The claims with the highest mean value per claim mostly belong to the procedural charges category for non‐communicable diseases (NCDs) and are often related to cardiovascular or cancer treatments. For example, Trastuzumab/Herceptin, a cancer drug used primarily to treat breast cancer, costs up to 9.8 million TZS (4200 US$), more than an average yearly salary of a public servant (CDC, 2021). Due to the high costs, such treatments must be specially approved by the NHIF (see Footnote 5). Since NCDs in Tanzania are increasing (Roman et al., 2019)— in 2016, deaths related to NCDs already accounted for as many as 33% of all deaths in Tanzania (WHO, 2016)—it will be essential to decrease the rising trend of NCDs and the corresponding rising costs by increasing awareness campaigns for early detection of NCDs, improving access to care and diagnostic capabilities, as well as promoting healthier lifestyles (for similar arguments see e.g., Lyimo et al., 2020; Roman et al., 2019; Katalambula et al., 2018).

Lastly, with regard to the NHIF's total expenditure, treatments for kidney diseases, C‐sections, cancer, and high blood pressure are the driving forces, even though they are only used by a small fraction of beneficiaries (see Table 5). Hence, there are disconcerting discussions in the literature on whether poorer countries should include these treatments in “essential” health care packages because doing so benefits a selected few at a high cost for policyholders in resource‐poor countries, particularly since fatality rates are still high for kidney disease and cancer, even with treatment (Meremo et al., 2017; Mushi et al., 2015; WHO, 2013). On the other hand, these are exactly the treatments that no household could conceivably afford, whereas households are more likely to pay for essential medicines in most cases. Antibacterial and malaria‐related treatments and general screening tests also generate high total costs, but benefit many and are effective in reducing the death rates of malaria and diarrheal diseases that are still responsible for 6% and 8% of child deaths, respectively, in Tanzania (WHO, 2016). However, raising awareness and prevention behavior (e.g., hygiene practice, usage and maintenance of long‐lasting insecticidal nets) and providing better infrastructure (e.g., water and sanitation) could also prevent people from suffering from these diseases and, thus, could also substantially reduce the costs for health insurance schemes (Deressa et al., 2014; Karinja et al., 2020; Yaya et al., 2018).

4.4. Usage and costs of the mandatory insurance by health facilities

Sixty‐two percent of all accredited health facilities had at least one NHIF claim and can, therefore, be considered active NHIF facilities. 20 The rate of active NHIF health facilities differs substantially among health facility type and ownership (see Table 6). It is particularly interesting that private health facilities are active NHIF facilities at a much lower rate than publicly‐owned facilities (46% vs. 67%). It seems surprising that within a year almost half of the private NHIF‐accredited health facilities had not treated even one NHIF patient. Delayed reimbursements from the national insurance scheme to the service provider appear to influence the decision of whether and how a health facility is going to treat an insured person—even when the health facility is technically accredited to treat the patient and submit the claims (Aikins et al., 2019; Amasha, 2015; Ashigbie et al., 2016). However, we could not quantitatively evaluate this effect with the data at hand.

TABLE 6.

National Health Insurance Fund (NHIF)‐accredited health facilities by type and ownership

| Total NHIF‐accredited health facilities | Active NHIF‐ accredited health facilities | ||

|---|---|---|---|

| Number | % | % | |

| Facility type | |||

| Dispensary/Pharmacy | 6236 | 84.40 | 60.36 |

| Health center | 750 | 10.15 | 75.07 |

| Hospital | 307 | 4.15 | 79.15 |

| Clinic | 90 | 1.22 | 25.56 |

| Total | 7389 | 100.00 | 62.15 |

| Ownership | |||

| Private | 1823 | 24.67 | 46.30 |

| Public | 5567 | 75.33 | 67.34 |

| Total | 7390 | 100.00 | 62.15 |

Note: Unit is per health facility (n = 7390). One health facility has a missing value for the facility type. Clinics are specialized health facilities, whereas hospitals include district, regional referral, zone referral and national referral hospitals.

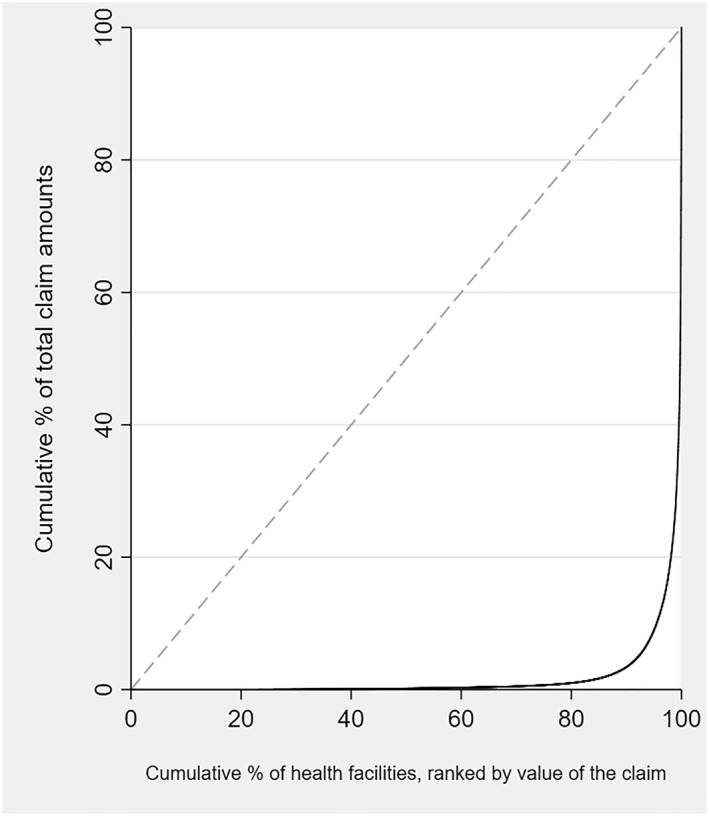

The distribution of the costs per health facility also reveals very high costs for a few health facilities compared to many facilities with very low costs (see Figure 2). In particular, the five health facilities (out of 7390) with the highest claim values represent 30% of the total NHIF claim value. These five health facilities are all hospitals located in Dar es Salaam, and include some specializing in special treatments, for example, for cancer, and therefore have extremely high claim values per treatment. More generally, 90% of health costs occur in only 5% of all health facilities (see Figure 2).

FIGURE 2.

Concentration curves of total National Health Insurance Fund (NHIF) claim amounts by health facilities. The 45° line would indicate that each health facility accounts for the same amount of costs

In Table 7, we further analyze the factors correlated with the probability that an NHIF‐accredited health facility is active, the number of claims, and total claim value. Results are very similar across these three variables. Compared to dispensaries and pharmacies, health centers had 3.4 times the odds of being active, and hospitals had 6.9 times the odds. It appears that the higher the care level of the NHIF‐accredited health facility, the more likely the facility was to have at least one claim. One possible reason is that the claim and reimbursement process is quite time‐ and resource‐intensive. Lower‐care health facilities may thus choose to not treat NHIF patients or to ask them to pay in cash, rather than submitting an official claim to the NHIF (Ashigbie et al., 2016). National Health Insurance Fund‐accredited hospitals and health centers also have by far the most claims and highest total costs compared to dispensaries and pharmacies. This finding is expected since treatments in hospitals and health centers require many more service details (e.g., various drugs, consumables and tests are required for surgeries) and are more complex and expensive, whereas in pharmacies beneficiaries mostly pick up single drug packages only. As the model in Table 7 with region fixed effects shows, in addition to having a high number of NHIF‐accredited health facilities, urban regions such as Dar es Salaam and Kilimanjaro had much higher numbers of claims resulting in a higher total claim amount, whereas more rural and poorer regions, such as Katavi and Geita, had a lower number of claims and costs. The high values are mostly driven by very expensive and specialized treatments, for example, cancer or heart disease, which are mostly offered in special hospitals located in Dar es Salaam or other urban and richer regions.

TABLE 7.

Factors correlated with take‐up of services, number of claims and value of claim per health facility

| (I) | (II) | (III) | |

|---|---|---|---|

| Health facility made a claim | Number of claims per health facility | Total value of claims (log) per health facility | |

| Logit odds ratio | Tobit‐Coefficient | Tobit‐Coefficient | |

| Health facility type (ref. Dispensary/Pharmacy) | |||

| Health center | 3.45 (0.000) | 10,042.3 (0.000) | 5.462 (0.000) |

| Hospital | 6.934 (0.000) | 48,637.2 (0.000) | 10.397 (0.000) |

| Clinic | 0.580 (0.038) | −5763.6 (0.057) | −2.578 (0.016) |

| Health facility ownership (ref. Public) | |||

| Private | 0.272 (0.000) | −2733.4 (0.000) | −4.225 (0.000) |

| Constant | 1.860 (0.000) | 842.3 (0.000) | 6.589 (0.000) |

| Control for region | X | X | X |

| Observations | 6766 | 6771 | 6771 |

| Pseudo R‐squared | 0.130 | 0.013 | 0.034 |

Note: Unit is per health facility (n = 7390). P‐values in parenthesis. Health labs excluded due to few observations.

5. DISCUSSION

This study is one of the first using administrative health insurance claims data to provide insights into the usage and cost structure of a mandatory national health insurance in a low‐income setting and the financial sustainability that would be associated with scaling up the NHIF to a national health insurance scheme. The NHIF in Tanzania has 2.3 million policyholders, corresponding to about 4% of the population in Tanzania. Since the NHIF is mandatory for all Tanzanian public servants, we avoid possible biases in the results due to adverse selection in the form of self‐selected high–risk individuals into the insurance.

Of all mandatory NHIF insured, 47% made at least one claim within a year, with an average annual cost of 76,166 TZS (33 US$) per policyholder and 161,049 TZS (69 US$) per beneficiary (excluding policyholders that did not make any claims). This amounts to about 60% of premiums a family pays per year (as dependents do not have to pay) and in total 3.6% of the yearly income of a public servant. Interestingly, women and individuals between 30 and 59 and middle‐income households use health facilities more often with their insurance card than men and children, the elderly, and the poorest and richest policyholders in our sample.

Our extrapolation of NHIF costs and revenue if health insurance coverage were to be extended to the entire Tanzanian population shows that the NHIF is currently not financially sustainable (see also Lee et al., 2018b; NHIF, 2018). The Tanzanian government will need to subsidize the insurance, for example, with tax‐based revenues or international funds, or by increased insurance premiums charged to the formal sector or extended contribution groups, such as informal sector workers. As an alternative or complementary policies, the government might want to aim to reduce costs by reducing the health services covered and/or increase efficiency by gatekeeping.

It is also interesting to see that the cost structure in Tanzania is extremely skewed. Five hospitals (out of 7390 health facilities) account for 30% of the costs reimbursed through NHIF and 10% of the policyholders account for 80% of total health costs. The most frequently used health services are painkillers, antibiotics and anti‐malaria drugs, together with diagnostics (stool, urine and blood, and malaria blood smears). The most expensive services as a share of total NHIF costs are procedures and surgeries related to cancer, cardiovascular diseases, and hemodialysis. The high costs are a huge challenge for resource‐poor countries because only very few policyholders with high mean costs can benefit. The most frequent services reflect the high burden placed on insurance schemes by diseases such as malaria and diarrhea, which could at least partly be prevented through better infrastructure and hygiene. Investments in preventive services for malaria, hygiene‐related infections, and non‐communicable diseases (NCDs) could be very cost‐effective interventions for mandatory health insurances.

Of all NHIF‐accredited health facilities across the country, 62% had at least one NHIF claim from public servants within a year and could, therefore, be considered active NHIF facilities. Interestingly, privately‐owned health facilities were less likely to be active compared to publicly‐owned facilities. This evidence suggests that treating insured patients is not particularly profitable because of for example, delayed reimbursement of insurance, unfavorable reimbursement prices, labor‐intensive claim processing as well as a large enough patient population that can afford paying cash (Aikins et al., 2019; Amasha, 2015; Ashigbie et al., 2016). It will be important for future research to understand if and to what extent health facilities withhold service provision from insured patients, or only accept them if they pay cash. If service provision remains low, scaling up health insurance enrollment would not necessarily contribute to the overall aim of universal health coverage, since insured patients would still not be financially protected.

In general, the health services incurring the highest costs in Tanzania are quite different from those in HICs (Dieleman et al., 2020; EDI, 2020; Wieser et al., 2014). First, tropical diseases such as malaria and diseases due to bacterial infection are much less prevalent in HICs. Second, lower back and neck pain, other musculoskeletal disorders, and diabetes are cost drivers in HICs (Dieleman et al., 2020; Wieser et al., 2014), whereas in Tanzania, due to the different lifestyles, these categories are not (yet) driving a large proportion of the overall costs. Nevertheless, costs related to cardiovascular diseases, cancer, and kidney‐related treatments are also high in HICs (Dieleman et al., 2020; Wieser et al., 2014). We are aware that the contexts of HICs and LMICs are very different in terms of age structure, disease burden, health infrastructure, income levels, and health systems. Nevertheless, the comparison shows that analyses of claims data in LMICs are essential to better understand the functioning of mandatory health insurances in these settings, rather than simply extrapolating from HIC data.

There are two key limitations of the paper. First, since the claims data is from 2016, it could be that the health insurance system, coverage and behavior have changed. However, data from 2021 show that NHIF coverage rates stayed almost the same over the last five years (7% in 2016 and 8% in 2021). Moreover, a SNHI is still under discussion and not yet implemented. Secondly, it could be that utilization and claims reimbursement trends vary across population groups (e.g., between public servants and informal workers). Indeed, we show that public servants are on average older, have higher wages, and live in more urban areas, with better (higher income) or worse (older) health outcomes and easier access to health services in urban centers. Hence, the projected costs for future universal health coverage might be under‐ or overestimated.

6. CONCLUSION

This study indicates that scaling up the coverage of the NHIF will be extremely challenging. To do so, policy makers will have to decide between reducing the essential package of health care covered by the scheme, deepening financial resources, asking poorer populations to also contribute through insurance premiums which will be administratively and logistically challenging—or investing in disease prevention or some combination of the above. Our analysis also indicates that privately‐accredited health facilities show fewer claims, and that the poorest and richest policyholders use their health insurance less—both results suggesting that out‐of‐pocket expenditures (despite carrying insurance) might still be an issue. Moreover, this first comprehensive study of claims data of a mandatory health insurance from a LMIC shows the benefits and shortcomings of administrative data in analyzing the health system. On the one hand, it provides much deeper insight into the utilization of the health care services, and their costs, than any survey data could ever reveal. On the other hand, administrative data might be incomplete. Last, our analysis has shown the large differences in health care utilization and cost structure that exist between Tanzania and several HICs (Switzerland, Germany and the United States). The results emphasize, that we can learn little about low‐income settings from the multiple insurance claims studies from HICs (e.g., Aljunid et al., 2012; UN, 2007), demonstrating the need for further studies using health provision data in LMICs.

AUTHOR CONTRIBUTIONS

Kathrin Durizzo conducted the statistical analysis and wrote the first version of the manuscript. Kenneth Harttgen, Fabrizio Tediosi and Isabel Günther conceptualized the study, developed the analytical strategy, interpreted the results and contributed to writing the paper. Paola Salari and August Kuwawenaruwa contributed to the interpretation of the results. Maitreyi Sahu contributed to the statistical analysis and writing the paper.

CONFLICT OF INTEREST

The authors declare no conflict of interest.

ETHICS STATEMENT

Ethical clearance for this study was obtained from the Ifakara Health Institute (IHI) Institutional Review Board (IHI/IRB/EXT/No: 028–2016) and the Tanzanian National Institute for Medical Research (NIMR/HQ/R.8a/Vol.IX/2340).

ACKNOWLEDGMENTS

The manuscript is part of the research project “Health systems governance for an inclusive and sustainable social health protection in Ghana and Tanzania” funded by the Swiss Program for Research on Global Issues for Development. This is a joint program by the Swiss National Science Foundation (SNSF) and the Swiss Agency for Development and Cooperation (SDC). The funder of the study had no role in the study design, data gathering, analysis and interpretation, or in writing of the report. The corresponding author had full access to all the data in the study and had final responsibility for the decision to submit for publication. This work was supported by the SNF (Swiss National Science Foundation) R4D grant (grant number 400640_183760).

Open access funding provided by Eidgenossische Technische Hochschule Zurich.

FIGURE A1.

Map of Tanzania with number of National Health Insurance Fund (NHIF)‐accredited health facilities as well as health facilities per 1000 population. Global Positioning System‐coordinates for Pemba and Zanzibar were not available and therefore cannot be shown in the map

TABLE A1.

List of benefit package of NHIF

| The National Health Insurance Fund (NHIF) has an benefits package that is offered to its policyholders through accredited health facilities countrywide. This package has a total of eleven (11) benefits that are offered to beneficiaries as per Standard Treatment Guidelines issued by the Ministry of Health alongside the Fund's regulations. The package includes (based on NHIF, 2019): |

|

|

|

|

|

|

|

|

|

|

|

| There are services that are offered through a special permit, these include: |

|

|

|

|

|

|

|

|

|

|

|

|

|

Abbreviation: ICU, intensitive care unit.

TABLE A2.

Sample deduction of NHIF policyholder and claim data

|

Durizzo, K. , Harttgen, K. , Tediosi, F. , Sahu, M. , Kuwawenaruwa, A. , Salari, P. , & Günther, I. (2022). Toward mandatory health insurance in low‐income countries? An analysis of claims data in Tanzania. Health Economics, 31(10), 2187–2207. 10.1002/hec.4568

ENDNOTES

Discussion with representatives for health financing technical working group.

Since 2018 restructured to improved Community Health Fund (Lee et al., 2018a).

NHIF coverage rates are constant on a 7% level since 2012. 2018 is the most recent year coverage rates are published by NHIF.

In Rwanda, formal employees (members of RAMA) pay a monthly premium of 7.5% of their gross income, matched with 7.5% paid by the employer. Members of the military (MMI members) pay 17.5% of their monthly salary, with 5% matched by their employer. Rural and informal sector workers are covered by the Community‐based Health Insurance where the premium depends on the socio‐economic status–the poorest population groups are exempted from paying any premiums (McIntyre et al., 2018).

In 2018, the proportion of special approvals was around 7% of total payments (NHIF, 2018). The procedure to get a special approval is as follows: Doctors fill out a form and send it to the NHIF for approval. Once approved, the beneficiary may access the service within the desired facility or another facility, based on availability.

Beside public sector employees, NHIF also covers voluntary groups, which are not covered in this paper.

This rate might be even slightly lower since the EES does not include public servants from Tanzania islands. A bias due to different definitions of public servants can be excluded because EES defines the group as “Central Government, Local Government and Parastatal Organization”.

Of these, 21,529 (0.06%) were identified as duplicates and dropped from the analysis. 2,252,387 claims (6.2%) have the same membership number (1,000,000) and are assumed to be wrongly entered into the system. In order to validate the claim values per treatment the price schedule for NHIF accredited health facilities was used to create an upper boundary of claim values. Claims which were above this boundary were excluded (69,978 claims, 0.2% of all claims). 107,890 claims (0.3%) were assumed to be double entries since the same policyholder had the same treatment on the same day at the same health facility–once with a claim value of zero and once with a claim value > 0. The claims with the zero value were excluded from the analysis of the claim values.

For very few claims, also the claim and reimbursement date is given; but this information cannot be used for the analysis because of many missing data entries.

Comparing our dataset of health facilities to the study from Maina et al. (2019), where they use multiple geocoding methods to provide a comprehensive spatial inventory of all health facilities in SSA, including Tanzania, our dataset has many more health facilities (6304 vs. 8943).

Clinics are specialized health facilities, whereas hospitals include district, regional referral, zone referral and national referral hospitals.

Tobit‐model is used because outcomes are left‐censored to 0 (Wooldridge, 2020).

See Table 3.

We compare our results to Switzerland as we were able to obtain similar statistics that are not available for other HICs. The Swiss system is private but still mandatory.

Since no data is available on the beneficiary home location or services received outside of the official NHIF health care, we cannot test which channel drives the results.

Very simple estimation based on the EES report of formal workers wage: 300,000–500,000 TZS average monthly income in the formal sector in Tanzania (Tanzania National Bureau of Statistics, 2018a).

There is one major limitation to this calculation. The financial report of the NHIF shows that costs rose in the following years (NHIF, 2018). Therefore, our projected costs for future universal health coverage might be underestimated.

The term gatekeeping describes the role of primary health care practitioners in authorizing access to specialized care in higher health facility levels.

Two service types, registration/consultation charges and inpatient charges, were excluded from this analysis.

70,5% if taking claims from all membership groups are into account. The patterns stay the same.

DATA AVAILABILITY STATEMENT

The data that support the findings of this study are available from NHIF.

REFERENCES

- Abrokwah, S. O. , Moser, C. M. , & Norton, E. C. (2014). The effect of social health insurance on prenatal care: The case of Ghana. International Journal of Health Care Finance and Economics, 14(4), 385–406. 10.1007/s10754-014-9155-8 [DOI] [PubMed] [Google Scholar]

- Aikins, M. , Owusu, R. , & Akewongo, P. (2019). Top‐ups for health services by clients of the national health insurance scheme in Ghana: The voices of providers and managers. (Unpublished manuscript).

- Aljunid, S. M. , Srithamrongsawat, S. , Chen, W. , Bae, S. J. , Pwu, R. , Ikeda, S. , & Xu, L. (2012). Health‐care data collecting, sharing, and using in Thailand, China mainland, South Korea, Taiwan, Japan, and Malaysia. Value in Health, 15(Suppl 1), S132–S138. 10.1016/j.jval.2011.11.004 [DOI] [PMC free article] [PubMed] [Google Scholar]

- Amasha, S. (2015). Causes and effects of delayed reimbursement to accredited health facilities by National Health Insurance Fund in delivery of health services. A case of regency medical hospital and NHIF head office. Master’s thesis, Mzumbe University. Retrieved from http://scholar.mzumbe.ac.tz/handle/11192/1752 [Google Scholar]

- Amu, H. , Dickson, K. S. , Kumi‐Kyereme, A. , & Darteh, E. K. M. (2018). Understanding variations in health insurance coverage in Ghana, Kenya, Nigeria, and Tanzania: Evidence from demographic and health surveys. PLoS One, 13(8), e0201833. 10.1371/journal.pone.0201833 [DOI] [PMC free article] [PubMed] [Google Scholar]

- Ankrah, D. , Hallas, J. , Odei, J. , Asenso‐Boadi, F. , Dsane‐Selby, L. , & Donneyong, M. (2018). A review of the Ghana national health insurance scheme claims database: Possibilities and limits for drug utilization research. Basic and Clinical Pharmacology and Toxicology, 124(1), 18–27. 10.1111/bcpt.13136 [DOI] [PubMed] [Google Scholar]

- AOK‐Bundesverband. (2019). Zahlen und Fakten 2019. Retrieved from https://aok‐bv.de/imperia/md/aokbv/aok/zahlen/zuf_2019_web.pdf

- Aryeetey, G. C. , Westeneng, J. , Spaan, E. , Jehu‐Appiah, C. , Agyepong, I. A. , & Baltussen, R. (2016). Can health insurance protect against out‐of‐pocket and catastrophic expenditures and also support poverty reduction? Evidence from Ghana’s national health insurance scheme. International Journal for Equity in Health, 15, 116. 10.1186/s12939-016-0401-1 [DOI] [PMC free article] [PubMed] [Google Scholar]

- Ashigbie, P. G. , Azameti, D. , & Wirtz, V. J. (2016). Challenges of medicines management in the public and private sector under Ghana’s National Health Insurance Scheme ‐ a qualitative study. Journal of Pharmaceutical Policy and Practice, 9, 6. 10.1186/s40545-016-0055-9 [DOI] [PMC free article] [PubMed] [Google Scholar]

- Baicker, K. , Taubman, S. L. , Allen, H. L. , Bernstein, M. , Gruber, J. H. , Newhouse, J. P. , Schneider, E. C. , Wright, B. J. , Zaslavsky, A. M. , & Finkelstein, A. N. (2013). The Oregon experiment ‐ effects of Medicaid on clinical outcomes. New England Journal of Medicine, 368, 1713–1722. 10.1056/NEJMsa1212321 [DOI] [PMC free article] [PubMed] [Google Scholar]

- Baker, U. , Okuga, M. , Waiswa, P. , Manzi, F. , Peterson, S. , & Hanson, C. (2015). Bottlenecks in the implementation of essential screening tests in antenatal care: Syphilis, HIV, and anemia testing in rural Tanzania and Uganda. International Journal of Gynecology & Obstetrics, 130(Suppl 1), S43–S50. 10.1016/j.ijgo.2015.04.017 [DOI] [PubMed] [Google Scholar]

- Banerjee, A. , Finkelstein, A. N. , Hanna, R. , Olken, B. A. , Ornaghi, A. , & Sumarto, S. (2021). The challenge of universal health insurance in developing countries: Experimental evidence from Indonesia’s national health insurance. The American Economic Review, 111(9), 3035–3063. [Google Scholar]

- Barasa, E. W. , Maina, T. , & Ravishankar, N. (2017). Assessing the impoverishing effects, and factors associated with the incidence of catastrophic health care payments in Kenya. International Journal for Equity in Health, 16(1), 31. 10.1186/s12939-017-0526-x [DOI] [PMC free article] [PubMed] [Google Scholar]

- Blanchet, N. J. , Fink, G. , & Osei‐Akoto, I. (2012). The effect of Ghana’s national health insurance scheme on health care utilization. Ghana Medical Journal, 46(2), 76–84. [PMC free article] [PubMed] [Google Scholar]

- Boerma, T. , Eozenou, P. , Evans, D. , Evans, T. , Kieny, M. P. , & Wagstaff, A. (2014). Monitoring progress towards universal health coverage at country and global levels. PLoS Medicine, 11(9), e1001731. 10.1371/journal.pmed.1001731 [DOI] [PMC free article] [PubMed] [Google Scholar]

- Borghi, J. , Maluka, S. , Kuwawenaruwa, A. , Makawia, S. , Tantau, J. , Mtei, G. , Ally, M. , & Macha, J. (2013). Promoting universal financial protection: A case study of new management of community health insurance in Tanzania. Health Research Policy and Systems, 11, 21. 10.1186/1478-4505-11-21 [DOI] [PMC free article] [PubMed] [Google Scholar]

- Cai, Q. , Buono, J. L. , Spalding, W. M. , Sarocco, P. , Tan, H. , Stephenson, J. J. , Carson, R. T. , & Doshi, J. A. (2014). Healthcare costs among patients with chronic constipation: A retrospective claims analysis in a commercially insured population. Journal of Medical Economics, 17(2), 148–158. 10.3111/13696998.2013.860375 [DOI] [PubMed] [Google Scholar]

- Centers for Disease Control and Prevention (CDC). (2021). Global health – Tanzania [fact sheet] . U.S. Department of Health and Human Services, Centers for Disease Control and Prevention. Retrieved from https://www.cdc.gov/globalhealth/countries/tanzania/default.htm [Google Scholar]

- Chemouni, B. (2018). The political path to universal health coverage: Power, ideas and community‐based health insurance in Rwanda. World Development, 106, 87–98. 10.1016/j.worlddev.2018.01.023 [DOI] [Google Scholar]

- Chomi, E. N. , Mujinja, P. , Enemark, U. , Hansen, K. , & Kiwara, A. D. (2014). Health care seeking behaviour and utilisation in a multiple health insurance system: Does insurance affiliation matter? International Journal for Equity in Health, 13, 25. 10.1186/1475-9276-13-25 [DOI] [PMC free article] [PubMed] [Google Scholar]

- Chua, K. , & Sommers, B. D. (2014). Changes in health and medical spending among young adults under health reform. JAMA, 311(23), 2437–2439. 10.1001/jama.2014.2202 [DOI] [PubMed] [Google Scholar]

- Cicero, T. J. , Wong, G. , Tian, Y. , Lynskey, M. , Todorov, A. , & Isenberg, K. (2009). Co‐Morbidity and utilization of medical services by pain patients receiving opioid medications: Data from an insurance claims database. Pain, 144(1–2), 20–27. 10.1016/j.pain.2009.01.026 [DOI] [PMC free article] [PubMed] [Google Scholar]

- Demographic and Health Surveys Program (DHS). (2021). Demographic and health survey Tanzania [data]. Retrieved from https://dhsprogram.com

- Deressa, W. , Yihdego, Y. Y. , Kebede, Z. , Batisso, E. , Tekalegne, A. , & Dagne, G. A. (2014). Effect of combining mosquito repellent and insecticide treated net on malaria revalence in Southern Ethiopia: A cluster‐randomised trial. Parasites & Vectors, 7, 132. 10.1186/1756-3305-7-132 [DOI] [PMC free article] [PubMed] [Google Scholar]

- Dieleman, J. L. , Cao, J. , Chapin, A. , Chen, C. , Li, Z. , Liu, A. , Horst, C. , Kaldjian, A. , Matyasz, T. , Scott, K. W. , Bui, A. L. , Campbell, M. , Duber, H. C. , Dunn, A. C. , Flaxman, A. D. , Fitzmaurice, C. , Naghavi, M. , Sadat, N. , Shieh, P. , ., & Murray, C. J. L. (2020). US health care spending by payer and health condition, 1996‐2016. JAMA, 323(9), 863–884. 10.1001/jama.2020.0734 [DOI] [PMC free article] [PubMed] [Google Scholar]

- Do, M. , Micah, A. , Brondi, L. , Campbell, H. , Marchant, T. , Eisele, T. , & Munos, M. (2016). Linking household and facility data for better coverage measures in reproductive, maternal, newborn, and child health care: Systematic review. Journal of Global Health, 6(2), 020501. 10.7189/jogh.06.020501 [DOI] [PMC free article] [PubMed] [Google Scholar]

- Eidgenössisches Departement des Inneren (EDI). (2020). Statistik der obligatorischen Krankenversicherung Ausgabe 2018. Retrieved from https://www.bag.admin.ch/dam/bag/de/dokumente/kuv‐aufsicht/stat/publications‐aos/statistik‐oblig‐kv‐2018.pdf.download.pdf/DE_StatKV2018_200528.pdf

- Fenny, A. P. , Yates, R. , & Thompson, R. (2018). Social health insurance schemes in Africa leave out the poor. International Health, 10(1), 1–3. 10.1093/inthealth/ihx046 [DOI] [PubMed] [Google Scholar]

- Fichera, E. , & Savage, D. (2015). Income and health in Tanzania. An Instrumental Variable Approach, 66, 500–515. World Development. 10.1016/j.worlddev.2014.09.016 [DOI] [PMC free article] [PubMed] [Google Scholar]

- Fiestas Navarrete, L. , Ghislandi, S. , Stuckler, D. , & Tediosi, F. (2019). Inequalities in the benefits of national health insurance on financial protection from out of pocket payments and access to health services: Cross‐sectional evidence from Ghana. Health Policy and Planning, 34(9), 694–705. 10.1093/heapol/czz093 [DOI] [PMC free article] [PubMed] [Google Scholar]

- Finkelstein, A. N. , & Taubman, S. (2015). Using randomized evaluations to improve the efficiency of US healthcare delivery. J‐PAL Research Paper. Retrieved from http://www.povertyactionlab.org/publication/healthcaredelivery/reviewpaper

- Ghislandi, S. , Manachotphong, W. , & Perego, V. M. E. (2015). The impact of universal health coverage on health care consumption and risky behaviours: Evidence from Thailand. Health Economics, Policy and Law, 10, 251–266. 10.1017/S1744133114000334 [DOI] [PubMed] [Google Scholar]

- Hinson, R. , Osei‐Frimpong, K. , Adeola, O. , & Aziato, L. (2020). Health service marketing management in Africa. Productivity Press. [Google Scholar]

- Horumpende, P. G. , Said, S. H. , Mazuguni, F. S. , Antony, M. L. , Kumburu, H. H. , Sonda, T. B. , Mwanziva, C. E. , Mshana, S. E. , Mmbaga, B. T. , Kajeguka, D. C. , & Chilongola, J. O. (2018). Prevalence, determinants and knowledge of antibacterial self‐medication: A cross sectional study in North‐eastern Tanzania. PLoS ONE, 13(10), e0206623. 10.1371/journal.pone.0206623 [DOI] [PMC free article] [PubMed] [Google Scholar]

- Integrated Public Use Microdata Series (IPUMS). (2020). Sample characteristics. Institute for Social Research and Data Innovation, University of Minnesota. Retrieved from: https://international.ipums.org/international%2Daction/sample%5Fdetails/country/tz%23tab%5Ftz2012a [Google Scholar]

- Kamuzora, P. , & Gilson, L. (2007). Factors influencing implementation of the community health fund in Tanzania. Health Policy and Planning, 22(2), 95–102. 10.1093/heapol/czm001 [DOI] [PubMed] [Google Scholar]

- Kanyangarara, M. , Walker, N. , & Boerma, T. (2018). Gaps in the implementation of antenatal syphilis detection and treatment in health facilities across sub‐Saharan Africa. PLoS One, 13(6), e0198622. 10.1371/journal.pone.0198622 [DOI] [PMC free article] [PubMed] [Google Scholar]

- Kapologwe, N. A. , Kagaruki, G. B. , Kalolo, A. , Ally, M. , Shao, A. , Meshack, M. , Stoermer, M. , Briet, A. , Wiedenmayer, K. , & Hoffman, A. (2017). Barriers and facilitators to enrollment and re‐enrollment into the community health funds/Tiba Kwa Kadi (CHF/TIKA) in Tanzania: A cross‐sectional inquiry on the effects of socio‐demographic factors and social marketing strategies. BMC Health Services Research, 17, 308. 10.1186/s12913-017-2250-z [DOI] [PMC free article] [PubMed] [Google Scholar]