Abstract

Background and Aims

Although over half of United States states have passed taxes on electronic nicotine delivery systems (ENDS), recent evidence links ENDS tax rates to increases in smoking, suggesting potentially substantive health costs. Overall health implications will depend on how these taxes affect transitions from experimentation to regular smoking and vaping. Current analyses have not assessed ENDS tax rates' effects in young adulthood (ages 18–25). This study measures the relationship between ENDS and cigarette tax rates and ENDS use and smoking in young adulthood, a key period for initiation of regular tobacco use.

Design

Observational study of data from the Current Population Survey's 2010–2019 Tobacco Use Supplements.

Setting

The United States.

Participants/Cases

A total of 38 906 18 to 25 year‐olds

Measurements

Multivariable linear regressions estimated two‐way fixed effects analyses to assess ENDS and cigarette tax rates' relationships to recent and daily smoking and vaping, adjusting for an array of potential sociodemographic and policy confounders along with state and year fixed effects.

Findings

A $1 increase in ENDS taxes yielded significant reductions in young adults' daily vaping ( = −0.025; 95% CI, −0.037, −0.014) alongside increases in recent smoking ( = 0.037; 95% CI, 0.013, 0.061), primarily reflecting greater dual use ( =2.078; 95% CI, 0.890, 4.852; P = 0.09). A $1 cigarette tax increase yielded 2.1 and 2.5 percentage point increases in recent and daily vaping, with 95% CIs of (0.004, 0.038) and (0.018, 0.032) respectively.

Conclusions

In the United States, higher ENDS tax rates are associated with decreased ENDS use but increased cigarette smoking among 18‐ to 25‐year‐olds, with associations reversed for cigarette taxes.

Keywords: Cigarettes, electronic nicotine delivery systems, smoking, taxes, tobacco control, vaping

INTRODUCTION

The past decade's surge in use of electronic nicotine delivery systems (ENDS) has prompted tension between perceptions that ENDS may fuel new nicotine dependence versus facilitate harm reduction. Corresponding research tends to consider youths or adults, obscuring liminal age‐groups. In particular, 18‐ to 25‐year‐olds are often analyzed as adults and sometimes considered as youths, but are more precisely categorized as young adults or “emerging adults,” a period of ongoing brain development and high rates of risky behaviors [1]. Although first tobacco use often occurs before age 18, transitions to regular use are more common in young adulthood: among 22‐ to 23‐year‐olds in the United States (US) who smoked daily in 2018, 56% reported transitioning to daily smoking at or after age 18 [2]. To the extent that young adulthood marks a transitional period when youth may either solidify or abandon a smoking habit, policies that reduce 18 to 25 year‐olds' initiation of habitual smoking may have added value for health over the life course. Therefore, our objective is to estimate how cigarette and ENDS tax rates relate to young adults' use of both products.

Although a large evidence base suggests substantive effects of conventional cigarette tax rates on adult smoking [3], evidence for young adults is more limited and mixed. One study of youth interviewed first as high school seniors and again around age 26 found no effect of state‐level cigarette taxes on smoking participation, but some evidence of increased cessation among baseline light smokers facing higher taxes [4]. In contrast, an interrupted time series study found that the 2009 federal cigarette tax increase (from $0.39 to $1.01 per pack) reduced the odds of smoking initiation among 18‐ to 25‐year‐olds, but had no effect on smoking cessation [5].

With the first US ENDS tax implemented in 2010, the literature on these taxes' effects is smaller than that for cigarette taxes, and primarily estimates associations between binary indicators for ENDS tax adoption and product use. Consequent findings are inconsistent. Estimating the association between ENDS use and ENDS tax adoption (i.e. not accounting for variation in tax sizes), three studies found evidence for a negative relationship [6, 7, 8], whereas two suggested a positive relationship [9, 10]. Considering cigarette use, a synthetic control analysis found evidence that ENDS tax adoption increased smoking [11], whereas two other studies yielded imprecisely estimated relationships [7, 9]. As each of the analyses using ENDS tax adoption implicitly treated all ENDS taxes equally, their contradictions might be resolved by accounting for variation and changes in the size of ENDS taxes, alongside adoption per se.

To this end, we consider a standardized ENDS tax rate; that is, converting per unit, per mL, and percent‐of‐cost ENDS taxes into a single tax measure in per fluid mL units using a recently published standardized ENDS tax methodology and database [12]. Thus, our analyses capture responses to tax sizes and changes as well as initial adoption. Broad differences in ENDS tax rates, which range from $0.05 to $2.52 per fluid mL, suggest that such variation likely impacts consumer responses to these policies. Evidence that ENDS taxes are almost fully passed‐through to consumers in the form of higher prices supports the use of tax variation to test for economic substitution/complementarity [13].

Matching standardized ENDS tax rates to adult respondents from two nationally‐representative surveys, the study most closely related to ours linked higher ENDS taxes to reduced vaping and increased smoking [14]. In particular, it found that, among 18‐ to 40‐year‐old adults, a $1 increase in ENDS taxes was associated with a 0.6 percentage point (ppt) reduction in daily ENDS use alongside 1.2 ppt increases in daily cigarette use, whereas a $1 increase in cigarette taxes yielded 0.7 ppt reductions in daily cigarette use but 0.5 ppt increases in daily ENDS use [14]. Findings from several working papers assessing the effect of ENDS tax rates—on teenagers [15], pregnant women [16], and using sales data [13]—concur in suggesting that ENDS and cigarettes are economic substitutes; that is, two products for which raising the price of one increases demand for the other. This finding is consistent with results from analyses of other policies' variation, such as enactment of minimum legal sales age laws for ENDS [17, 18, 19, 20].

Still, none of these papers estimated the effect of ENDS tax rates on young adults alone. Because this age‐group marks a critical period for transitions to regular tobacco and nicotine use, understanding their smoking‐ and vaping‐responses to ENDS taxes is crucial for informing policy decisions to promote population health.

The project aims are to estimate ENDS and cigarette tax rates' relationships to ENDS and cigarette use among 18‐ to 25‐year‐olds.

METHODS

Data

To address this gap in the evidence, we matched state policy and economic information to nationally representative data from nine waves of the Current Population Survey's Tobacco Use Supplement (CPS‐TUS), collected between 2010 and 2019 (response rate ≈58%) [21]. Our inclusion criteria limited consideration to 18‐ to 25‐year‐olds, the ages when most US smokers report first transitioning to daily use [2].

Measures

Outcomes were binary indicators for recent and daily cigarette and ENDS use, based on survey questions asking whether respondents “now use” each product “every day, some days, or not at all.” ENDS data were only available post‐2013. Therefore, the analytic sample covers 2014 to 2019 for ENDS outcomes, but 2010 to 2019 for cigarette outcomes to ensure greater statistical power while focusing on the same decade.

Exposures were continuous measures of cigarette taxes (dollars/pack) and ENDS taxes in standardized dollar/mL units—standardized across both percent‐of‐cost and per‐unit ENDS taxes in accordance with a recently published methodology and database [12].

Covariates included state and month‐year fixed effects to adjust for time‐invariant state characteristics and common time trends respectively, indicators for respondent demographics that are correlated with cigarette or ENDS use and may differ between states (i.e. sex, year of age, race/ethnicity, any college education, and employment status), and relevant state characteristics and policies by interview quarter: unemployment and poverty rates, smoke‐ and vape‐free indoor air law indexes, percent of population covered by tobacco‐21 laws, indicators for whether the respondent could legally be sold cigarettes in their state, and significant Medicaid expansions, as well as policies likely to affect consumption of potential substitutes or complements for tobacco and nicotine products (i.e. beer taxes, indicators for medical and recreational marijuana legalization) (see Supporting information for further details).

Statistical Analysis

Using the CPS‐TUS sample weights, χ2, and Wald tests compared sample‐weighted means in states with versus without ENDS taxes. Multivariable linear regressions used respondent‐level data to estimate each outcome's relationship to cigarette and ENDS taxes, controlling for the aforementioned covariates and clustering standard errors by state (the level of policy exposure) [22]. Sometimes called a “dose‐response difference‐in‐differences analysis,” these regressions compared outcomes in areas with different levels of ENDS and cigarette taxes, before versus after the taxes were adopted/changed. Such analyses may yield causal estimates if adopting versus non‐adopting areas' outcomes were trending in parallel before the tax was implemented. We test this by repeating the main analyses with leads on each tax as covariates, to assess whether outcome trends shifted in advance of tax changes.

Although linear models were preferred here because of concerns about attenuation bias in non‐linear models with large numbers of fixed effects [23], sensitivity checks repeated the main analyses as logistic regressions. Additionally, sex‐stratified regressions were run to clarify whether a single sex drove the full sample responses. Finally, we estimated these relationships as a discrete choice analysis: multinomial logistic regressions tested how cigarette and ENDS taxes related to exclusive smoking, exclusive vaping, and dual use—all based on self‐reported recent use variables, with “no recent use” as the reference group—adjusting for the same covariates as above. Critically, this analysis has a caveat: with only two waves of data capturing cigarette and ENDS use as well as dual use's relatively low prevalence, these results may be under‐powered.

The Georgia State University Institutional Review Board (IRB) deemed this study exempt from human subjects review (Protocol H18423). The research question and analysis plan considered here were not pre‐registered on a publicly available forum. However, applying difference‐in‐differences methods to address this research question was a component of grant proposals submitted and funded before the full data's availability.

RESULTS

Comparing means in states with versus without ENDS taxes, Table 1 finds statistically significant differences in all but two covariates—percent female and recreational marijuana legalization—supporting their inclusion as controls. Both recent and daily smoking are more common in states without ENDS taxes (15.6% vs 12.8% and 11.2% vs 8.8%, respectively; P < 0.001 for both), reinforcing the need for state fixed effects in multivariable analyses (to absorb average differences in the outcome variable between states).

TABLE 1.

Summary statistics by ENDS taxation in respondent's state of residence

| ENDS tax | No ENDS tax | χ 2 test P‐values | |

|---|---|---|---|

| Recent ENDS use | 3.7% | 4.0% | 0.500 |

| Daily ENDS use | 1.3% | 1.3% | 0.825 |

| Recent smoking | 12.8% | 15.6% | <0.001 |

| Daily smoking | 8.8% | 11.2% | <0.001 |

| Female | 50.3% | 50.7% | 0.550 |

| Race/ethnicity | <0.001 | ||

| Non‐Hispanic White | 50.9% | 58.8% | |

| Non‐Hispanic Black | 13.8% | 14.5% | |

| Non‐Hispanic Asian | 8.0% | 5.4% | |

| Non‐Hispanic, other race | 2.0% | 2.2% | |

| Hispanic | 25.3% | 19.1% | |

| Any college | 57.1% | 53.1% | <0.001 |

| Employment status | 0.001 | ||

| Employed | 60.4% | 62.8% | |

| Unemployed | 11.0% | 10.1% | |

| Not in labor force | 28.7% | 27.0% | |

| State characteristics | |||

| Standardized ENDS tax rate | $0.15/mL | – | <0.001 |

| Cigarette tax | $2.54/pack | $2.74/pack | <0.001 |

| Index of indoor vaping restrictions | 0.174 | 0.074 | <0.001 |

| Index of indoor smoking restrictions | 0.888 | 0.728 | <0.001 |

| Individual cannot be legally sold cigarettes per state law | 2.2% | 0.5% | <0.001 |

| Percent of population with tobacco‐21 | 5.3% | 3.7% | <0.001 |

| Poverty rate | 13.9% | 14.5% | <0.001 |

| Unemployment rate | 7.6% | 6.8% | <0.001 |

| Significant Medicaid expansions | 45.1% | 31.4% | <0.001 |

| Beer tax (per gallon) | $0.32 | $0.23 | <0.001 |

| Medical marijuana legalization | 60.4% | 29.2% | <0.001 |

| Recreational marijuana legalization | 4.3% | 4.1% | 0.307 |

| n | 11 141 | 27 765 | 38 906 |

Notes: Sample‐weighted means are calculated for 18‐ to 25‐year‐old respondents in states that did versus did not have an ENDS tax at any point during the study period (expressed as percentages for binary variables and rates or means for continuous variables). Illinois and Maryland, which have sizable county‐ and/or city‐level taxes, are also classified as having an ENDS tax. χ2 tests (for categorical variables) and Wald tests (for continuous variables) confirm whether variable values are statistically different between states with versus without ENDS taxes. Data are complete for all variables except vaping (n = 199 missing recent and daily ENDS use, out of 22 478 post‐2013 respondents ages 18–25 years) and smoking (n = 121 missing for recent and daily smoking). Vaping and smoking variable means are calculated across non‐missing observations only. ENDS = electronic nicotine delivery system.

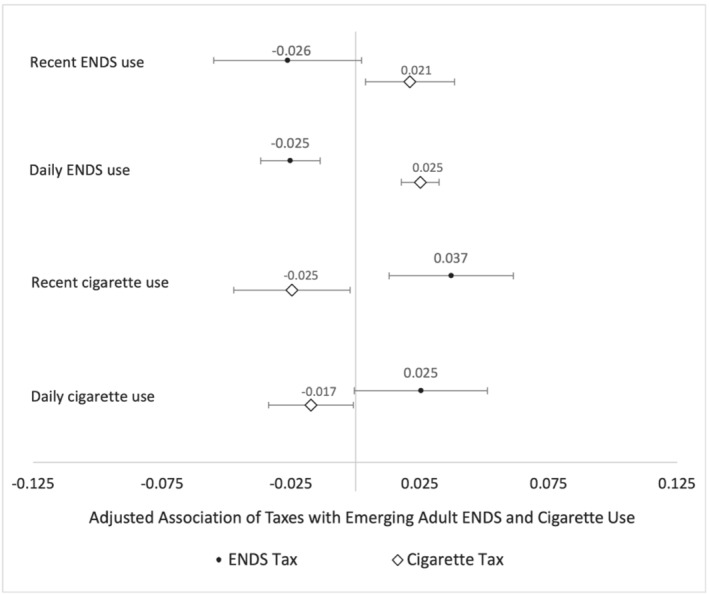

Figure 1 presents each regression's tax coefficients and 95% CIs, adjusting for the aforementioned covariates. ENDS taxes yielded statistically significant reductions in daily ENDS use and increases in recent cigarette use, alongside marginally non‐significant reductions in recent ENDS use (P = 0.07) and increases in daily cigarette use (P = 0.054). Cigarette tax estimates were flipped, yielding significant reductions in recent and daily cigarette use, versus increases in recent and daily ENDS use. In particular, a $1 increase in ENDS taxes was associated with a 2.5 ppt reduction in daily ENDS use (95% CI, −3.68,−1.38), and 3.7 ppt increase in recent smoking (95% CI, 1.30, 6.12). Symmetrical effects were seen with cigarette taxes, with a $1 increase yielding a 2.5 ppt reduction in recent smoking (95% CI, −4.73, −0.21) alongside a 2.5 ppt increase in daily ENDS use (95% CI, 1.77, 3.24).

FIGURE 1.

Tax associations with ENDS and cigarette use, 18‐ to 25‐year‐olds. Sample‐weighted multivariable linear regressions use data on 18‐ to ‐25‐ year‐olds from the 2010–2019 waves of the Current Population Survey's Tobacco Use Supplement to estimate ENDS and cigarette tax rates' relationships to recent ENDS use, daily ENDS use, recent cigarette use, and daily cigarette use. Covariates adjust for state and month‐by‐year fixed effects, individual sociodemographics—indicators for sex, year of age, race/ethnicity, any college education, and employment status—and state covariates: unemployment and poverty rates, smoke‐ and vape‐free indoor air law indexes, percent of population covered by tobacco‐21 laws, beer tax rates, and binary indicators for whether the respondent could legally be sold cigarettes, medical and recreational marijuana legalization, and significant Medicaid expansions. Standard errors are clustered by state. Coefficient estimates and 95% confidence intervals are given for each tax variable above, with the corresponding outcome noted along the plot's left‐hand side. Each outcome is a separate regression. The Supporting information Table S1 gives these findings in tabular form. ENDS = electronic nicotine delivery system.

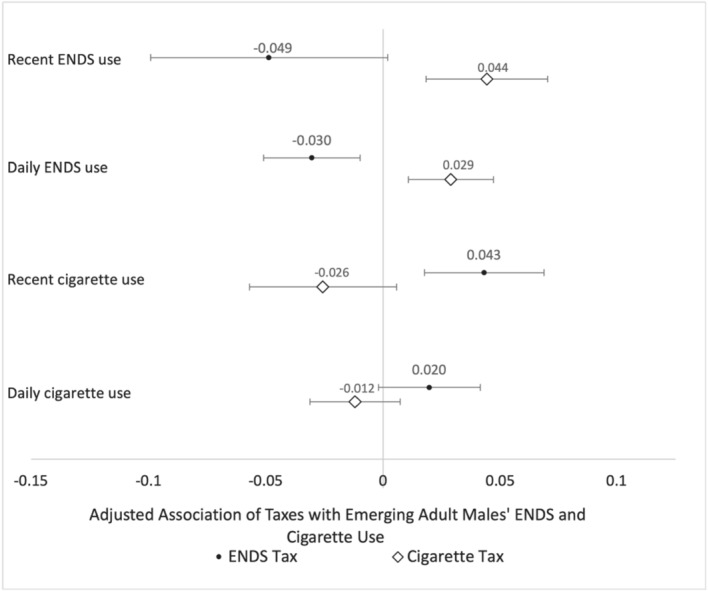

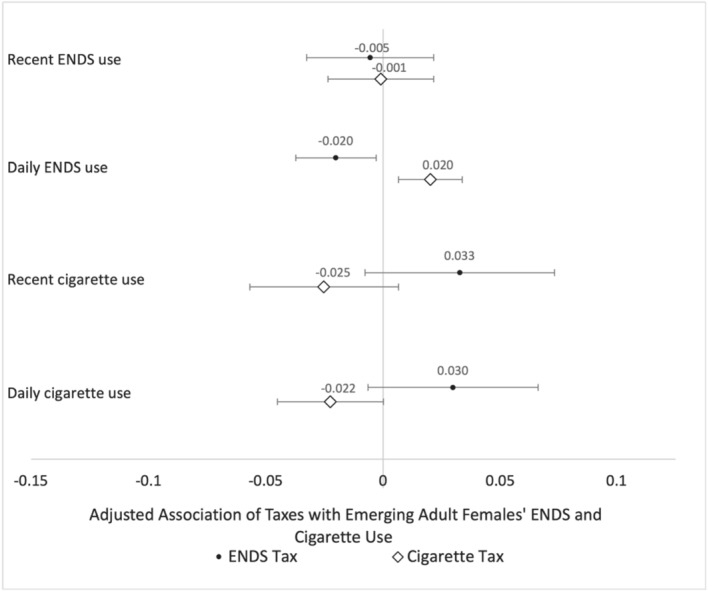

Implications were similar when assessed via logistic regression (See Supporting information Table S2) and when stratified by sex (see Figs. 2 and 3), particularly for ENDS taxes' relationship to daily ENDS use and, among males, recent smoking.

FIGURE 2.

Tax associations with ENDS and cigarette use, 18‐ to 25‐year‐old males. Sample‐weighted multivariable linear regressions use data on 18‐ to ‐25‐year‐old males from the 2010–2019 waves of the Current Population Survey's Tobacco Use Supplement to estimate ENDS and cigarette tax rates' relationships to recent ENDS use, daily ENDS use, recent cigarette use, and daily cigarette use. Covariates adjust for state and month‐by‐year fixed effects, individual sociodemographics—indicators for sex, year of age, race/ethnicity, any college education, and employment status—and state covariates: unemployment and poverty rates, smoke‐ and vape‐free indoor air law indexes, percent of population covered by tobacco‐21 laws, beer tax rates, and binary indicators for whether the respondent could legally be sold cigarettes, medical and recreational marijuana legalization, and significant Medicaid expansions. Standard errors are clustered by state. Coefficient estimates and 95% CIs are given for each tax variable above, with the corresponding outcome noted along the plot's left‐hand side. Each outcome is a separate regression. ENDS = electronic nicotine delivery system.

FIGURE 3.

Tax associations with ENDS and cigarette use, 18‐ to 25‐year‐old females. Sample‐weighted multivariable linear regressions use data on 18‐ to 25‐year‐old females from the 2010–2019 waves of the Current Population Survey's Tobacco Use Supplement to estimate ENDS and cigarette tax rates' relationships to recent ENDS use, daily ENDS use, recent cigarette use, and daily cigarette use. Covariates adjust for state and month‐by‐year fixed effects, individual sociodemographics—indicators for sex, year of age, race/ethnicity, any college education, and employment status—and state covariates: unemployment and poverty rates, smoke‐ and vape‐free indoor air law indexes, percent of population covered by tobacco‐21 laws, beer tax rates, and binary indicators for whether the respondent could legally be sold cigarettes, medical and recreational marijuana legalization, and significant Medicaid expansions. Standard errors are clustered by state. Coefficient estimates and 95% CIs are given for each tax variable above, with the corresponding outcome noted along the plot's left‐hand side. Each outcome is a separate regression. ENDS = electronic nicotine delivery system.

Adding controls for next‐year's cigarette and ENDS taxes to the main specification yielded statistically insignificant coefficients on taxation‐leads in all cases except next‐year's cigarette tax in the recent‐ENDS‐use analysis ( = 0.029, 95% CI, 0.015, 0.044) (see Supporting information Table S3). Therefore, respondent behavior did not appear to respond to ENDS taxes before they were in effect.

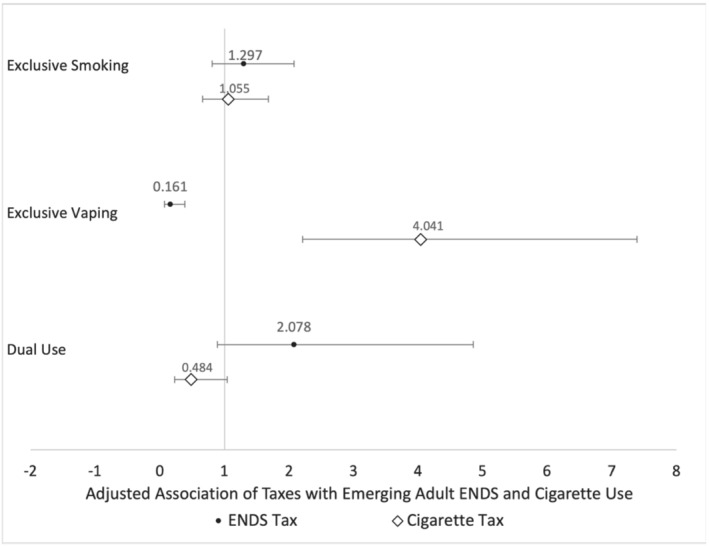

Taking a discrete choice approach, Fig. 4 presents relative risk ratios (RRRs) from a multinomial logistic regression assessing the tax variables' associations with exclusive smoking, exclusive vaping, and dual use (reference group: “no use”). This analysis used only the last two waves of data, as it required information on cigarette and ENDS use. Both taxes yielded statistically insignificant RRRs for exclusive smoking. Their RRRs for exclusive vaping and dual use; however, had similar implications to earlier analyses: higher ENDS taxes were associated with reductions in exclusive vaping (RRR = 0.161, 95% CI, 0.067, 0.384; P < 0.001) and increases in dual use (RRR = 2.078, 95% CI, 0.890, 4.852; P = 0.09), whereas higher cigarette taxes yielded increases in exclusive vaping (RRR = 4.041, 95% CI, 2.211, 7.385; P < 0.001) and decreases in dual use (RRR = 0.484, 95% CI, 0.225, 1.040; P = 0.06). Although both taxes' associations with dual use were marginally nonsignificant (i.e. P < 0.1), the sample's lower prevalence of dual use (2%) suggests that more limited statistical power may have been a factor here.

FIGURE 4.

Relative risk ratios for tax associations with exclusive vaping, exclusive smoking, and dual use, 18‐ to 25‐year‐olds. A single sample‐weighted multinomial logistic regression uses data on 18‐ to 25‐year‐olds from the 2014–2019 waves of the Current Population Survey's Tobacco Use Supplement to estimate ENDS and cigarette tax rates' relationships to exclusive cigarette use (“smoking”), exclusive ENDS use (“vaping”), and dual use, taking “no use” as the reference group. Covariates adjust for state and month‐by‐year fixed effects, individual sociodemographics—indicators for sex, year of age, race/ethnicity, any college education, and employment status—and state covariates: unemployment and poverty rates, smoke‐ and vape‐free indoor air law indexes, percent of population covered by tobacco‐21 laws, beer tax rates, and binary indicators for whether the respondent could legally be sold cigarettes, medical and recreational marijuana legalization, and significant Medicaid expansions. Standard errors are clustered by state. Each tax variable's estimated relative risk ratios are presented with their 95% CI, alongside the corresponding outcome category noted on the plot's left‐hand side. The Supporting information Table S4 gives these results in tabular form.

DISCUSSION

Among 18‐ to 25‐year‐olds, ENDS taxes were associated with increased cigarette use, whereas cigarette taxes yielded increased ENDS use, consistent with prior evidence that the two products are economic substitutes [14, 16, 17, 18, 19, 20, 24]. Moreover, tax coefficient estimates for this sample of young adults were roughly three times larger in magnitude than those estimated for adults ages 18 to 40 years in a similar specification, [14] underscoring the importance of assessing young adult nicotine and tobacco use separately from other age groups.

To our knowledge, this study provides the first analysis of how ENDS and cigarette tax rates relate to use of both products among 18‐ to 25‐year‐olds, a critical period for transitions to regular tobacco use. Limitations include, first, reliance on self‐reported cigarette and ENDS use, which may introduce social desirability bias. Consequent under‐reporting, however, would have to be correlated with tax increases, and in opposite directions for smoking versus vaping, to explain our findings. Second, because most ENDS taxes implemented during the analytic period (2010–2019) came into effect between 2015 and 2017, many young adults facing an ENDS tax in our sample were not exposed to those taxes as minors. Therefore, findings may be best interpreted as estimating ENDS taxes' short‐run effects. A third data issue concerns the level of the analysis: without substate geocodes for all respondents, we cannot link individuals to local taxes. Instead of omitting local ENDS and cigarettes taxes—which might bias estimates away from the null by under‐estimating the true tax respondents are exposed to—our data use population‐weighted tax variables at the state level. Consequently, some respondents in states with local taxes are assigned to higher ENDS taxes than they actually faced (e.g. Illinois residents who do not live in Cook County) and others lower taxes than they actually faced (e.g. Cook County residents), potentially reducing our estimates' precision. A fourth limitation is our inability to conduct an event study to validate the analytic approach: with the CPS‐TUS fielded in only 9 months between 2010 and 2019, extended breaks between infrequent data collection periods preclude an event study. Instead, regressions assess pre‐trends by testing whether leads on the tax variables predict either outcome (Supporting information Table S3), as in prior work [15]. Finally, our results may not generalize to taxes that are substantially larger than those observed in our data. Specifically, this sample's ENDS and cigarette tax exposures range from $0 to $2.52 per mL in the former case, and $1.13 to $6.49 per pack in the latter. Consumer responses to a $1 tax increase (i.e. our regression estimates) might differ at much higher initial tax rates (e.g. ≥$10/mL).

An increase in combustible tobacco product use in response to ENDS taxes complicates tobacco policymaking, as various reviews and expert opinions have concluded that cigarettes are the more lethal product. In 2018, the National Academies of Sciences, Engineering, and Medicine concluded that vaping ENDS is “likely to be far less harmful than combustible tobacco cigarettes,” [25] a conclusion endorsed more recently by 15 former presidents of the Society for Research on Nicotine and Tobacco in a 2021 summary of the evidence [26]. Still, in the interval between these publications, the percent of the general population who believed that ENDS use was more harmful than smoking increased, specifically following the 2019 outbreak of vaping‐associated lung injuries [27]. Yet that concern was misplaced: the Centers for Disease Control and Prevention (CDC) subsequently identified additives in informally‐sourced tetrahydrocannabinol (THC) concentrates (i.e. products not purchased from a formal retailer) as the outbreak's primary cause. [28] When Allcott and Rafkin [29] assessed 137 experts' perceptions of ENDS' harms relative to cigarettes in August 2020, their average response was that “vaping [ENDS] is 37 percent as harmful as smoking cigarettes.” This estimate is consistent with a 2021 biomarker study suggesting that ENDS use is 33% as harmful as smoking [30]; a systematic review finding a 40% lower odds of respiratory outcomes among smokers who switched to ENDS [31]; randomized controlled trial findings of improvements in vascular function within a month of switching from smoking to ENDS [32]; and evidence of significant reductions in carcinogen and toxicant exposure among smokers who switched to ENDS [33]. Therefore, if choosing between a policy that produces net increases in ENDS‐use versus one that generates net increases in smoking, current evidence suggests that the latter is likely to be substantively worse for public health.

CONCLUSIONS

There has been some discussion in the literature recently that cigarette taxes have “lost their bite” potentially because of the hardening of remaining smokers [34]. Focusing on young adults during a period of time when ENDS were available, we find evidence that cigarette taxes remain effective in preventing smoking in this age‐group. At the same time, however, the evidence links ENDS taxes to increases in young adult smoking.

Alongside current evidence on the relative health risks of using ENDS versus smoking and prior work indicating that ENDS taxes reduce adult smoking cessation [11], our findings suggest a need for nuance in ENDS policymaking. Specifically, although higher ENDS taxes risk incentivizing young adult smoking, this can perhaps be offset with a sufficiently large cigarette tax increase. Similarly, cigarette tax increases alone may increase ENDS use in this age‐group, which is not necessarily a bad outcome if that increase stems from people who would otherwise smoke. As prior work has demonstrated that life expectancies for smokers who quit before age 35 are not statistically different than those for never smokers, young adults' responses to these policies may have significant consequences for population health [35]. Still, caution is called for: to fully understand which policy combination best serves public health, future research needs to assess such taxes' effects, not only on use of mainstream ENDS products, but also on use of informally‐sourced vaping concentrates, which can impose even larger health risks (i.e. from contaminants or additives in street‐purchased products) [36]. Given young adulthood's significance as a time of transitions toward regular tobacco use, tailoring differential tobacco and nicotine product taxes to reduce this age‐group's use of more lethal products—both combustibles and informally sourced vaping concentrates—is a critical goal for public health policy.

Recently, 15 former presidents of the Society for Research on Nicotine and Tobacco endorsed a position on ENDS and cigarette taxation: “Tax cigarettes and other combustible tobacco products heavily; impose a more modest tax on e‐cigarettes. Taxes should be proportionate to risk. A much higher tax on combustibles will encourage adult smokers to quit smoking or to switch to less expensive e‐cigarettes. By raising the price of e‐cigarettes, a modest tax will discourage their use by price‐sensitive youths.” [26] Our results provide empirical support for this strategy as a means to interrupt transitions to habitual use, by disincentivizing young adult vaping without increasing smoking in this key age‐group. These findings are consistent with other studies linking ENDS tax rates to increased smoking among adults [14], teenagers [15], and pregnant women [16], and cigarette sales in retail data [13]. Further research is needed to confirm whether they hold post‐2019 and clarify what size tax differential would be optimal for population health.

DECLARATION OF INTERESTS

Neither author has conflicts of interest to disclose.

AUTHOR CONTRIBUTIONS

Abigail Friedman: Conceptualization; formal analysis; funding acquisition; investigation; methodology; visualization. Michael Pesko: Conceptualization; formal analysis; funding acquisition; investigation; methodology; visualization.

Supporting information

Table S1 Taxes and young adult cigarette and ENDS use, coefficient/[95% CI]/(P‐value)

Table S2 Taxes and young adult cigarette and ENDS use, odds ratio/[95% CI]/(P‐value)

Table S3 Pre‐trends tests, coefficient/[95% CI]/(P‐value)

Table S4 Multinomial logistic regression: tax associations with exclusive vaping, exclusive smoking, and dual use among 18–25 year‐olds, relative risk ratio/[95% CI]/(P‐value)

Table S5 ENDS tax changes through May 2019

ACKNOWLEDGEMENTS

This research was supported by an Evidence for Action grant from the Robert Wood Johnson Foundation (74869) (A.S.F.), the National Institute on Drug Abuse of the National Institutes of Health (NIDA‐NIH) (R01DA045016) (M.F.P.), and the University of Kentucky's Institute for the Study of Free Enterprise (M.F.P.). None of the funders had any role in the study's design or conduct; the data's collection, analysis, or interpretation, or the manuscript's preparation. Content is solely the responsibility of the authors and does not necessarily represent the official views of the Robert Wood Johnson Foundation, NIDA‐NIH, or the Institute for the Study of Free Enterprise.

Friedman AS, Pesko MF. Young adult responses to taxes on cigarettes and electronic nicotine delivery systems. Addiction. 2022;117(12):3121–3128. 10.1111/add.16002

Author order is alphabetical: both authors contributed equally to the study design and analysis, as well as drafting and revision of the manuscript. Both authors approved the final manuscript as submitted and agree to be accountable for all aspects of the work.

Funding information National Institute on Drug Abuse, Grant/Award Number: R01DA045016; University of Kentucky’s Institute for the Study of Free Enterprise; Robert Wood Johnson Foundation, Grant/Award Number: 74869

REFERENCES

- 1. Arnett JJ. Emerging adulthood: A theory of development from the late teens through the twenties. Am Psychol. 2000;55(5):469–80. [PubMed] [Google Scholar]

- 2. Barrington‐Trimis JL, Braymiller JL, Unger JB, et al. Trends in the age of cigarette smoking initiation among young adults in the US from 2002 to 2018. JAMA Netw Open. 2020;3(10):e2019022. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 3. Gallet CA, List JA. Cigarette demand: A meta‐analysis of elasticities. Health Econ. 2003;12(10):821–35. [DOI] [PubMed] [Google Scholar]

- 4. DeCicca P, Kenkel D, Mathios A. Cigarette taxes and the transition from youth to adult smoking: Smoking initiation, cessation, and participation. J Health Econ. 2008;27(4):904–17. [DOI] [PubMed] [Google Scholar]

- 5. van Hasselt M, Kruger J, Han B, Caraballo RS, Penne MA, Loomis B, et al. The relation between tobacco taxes and youth and young adult smoking: What happened following the 2009 U.S. federal tax increase on cigarettes? Addict Behav. 2015;45:104–9. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 6. Jun J, Kim JK. Do state regulations on e‐cigarettes have impacts on the e‐cigarette prevalence? Tob Control. 2021;30:221–6. [DOI] [PubMed] [Google Scholar]

- 7. Anderson DM, Matsuzawa K, Sabia JJ. Cigarette taxes and teen marijuana use. Natl Tax J. 2020;73(2):475–510. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 8. Han D, Seo D, Lin H. Statewide vaping product excise tax policy and use of electronic nicotine delivery systems among US young adults, 2014–2019. Tob Control. 2021. 10.1136/tobaccocontrol-2021-056653 [DOI] [PubMed] [Google Scholar]

- 9. Katchmar A, Gunawan A, Siegel M. Effect of Massachusetts house bill no. 4196 on electronic cigarette use: A mixed‐methods study. Harm Reduct J. 2021;18(50):1–15. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 10. Choi K, Omole T, Wills T, Merianos AL. E‐cigarette‐inclusive smoke‐free policies, excise taxes, tobacco 21 and changes in youth e‐cigarette use: 2017–2019. Tob Control. 2021. 10.1136/tobaccocontrol-2020-056 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 11. Saffer H, Dench D, Grossman M, Dave D. E‐cigarettes and adult smoking: Evidence from Minnesota. J Risk Uncertain. 2020;60(3):207–28. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 12. Cotti CD, Nesson ET, Pesko MP, Phillips S, Tefft N. Standardizing the measurement of e‐cigarette taxes in the USA, 2010–2020. Tob Control. Published Online First: PMID: 34911814. 15 December 2021. 10.1136/tobaccocontrol-2021-056865 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 13. Cotti CD, Courtemanche CJ, Maclean JC, Nesson ET, Pesko MP, Tefft N. The Effects of E‐Cigarette Taxes on E‐Cigarette Prices and Tobacco Product Sales: Evidence from Retail Panel Data. NBER Working Paper. No. w26724. 2022. [DOI] [PMC free article] [PubMed]

- 14. Pesko MF, Courtemanche CJ, Maclean JC. The effects of traditional cigarette and e‐cigarette tax rates on adult tobacco product use. J Risk Uncertain. 2020;60:229–58. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 15. Abouk R, Courtemanche C, Dave D, Feng B, Friedman AS, Maclean JC, Pesko MF, Sabia JJ, Safford S. Intended and Unintended Effects of E‐cigarette Taxes on Youth Tobacco Use. NBER Working Paper No 29216. 2021. [DOI] [PMC free article] [PubMed]

- 16. Abouk R, Adams S, Feng B, Maclean JC, Pesko MF. The Effect of E‐Cigarette Taxes on Pre‐pregnancy and Prenatal Smoking. NBER Working Paper. No. w26126. 2019.

- 17. Friedman AS. How does electronic cigarette access affect adolescent smoking? J Health Econ. 2015;44:300–8. [DOI] [PubMed] [Google Scholar]

- 18. Pesko MF, Hughes JM, Faisal FS. The influence of electronic cigarette age purchasing restrictions on adolescent tobacco and marijuana use. Prev Med. 2016;87:207–12. [DOI] [PubMed] [Google Scholar]

- 19. Pesko MF, Currie JM. E‐cigarette minimum legal sales age laws and traditional cigarette use among rurla pregnant teenagers. J Health Econ. 2019;66:71–90. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 20. Dave D, Feng B, Pesko MF. The effects of e‐cigarette minimum legal sale age laws on youth substance use. Health Econ. 2019;28(3):419–36. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 21. National Cancer Institute: Division of Cancer Control and Population Sciences . TUS‐CPS Questionnaires and Data Files. 10 August 2021. [Online]. Available: https://cancercontrol.cancer.gov/brp/tcrb/tus-cps/questionnaires-data#harmonized. [Accessed 12 August 2021].

- 22. Abadie A, Athey S, Imbens GW, Woolridge J. When should you adjust standard errors for clustering?. NBER Working Paper. No. w24003. 2017.

- 23. Greene W. The behaviour of the maximum likelihood estimator of limited dependent variable models in the presence of fixed effects. Econom J. 2004;7(1):98–119. [Google Scholar]

- 24. Pesko MF, Warman C. Re‐exploring the early relationship between teenage cigarette and e‐cigarette use using price and tax changes. Health Econ. 2022;31(1):137–53. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 25. National Academies of Sciences, Engineering, and Medicine . Public Health Consequences of E‐Cigarettes Washington, DC: The National Academies Press. 10.17226/24952; 2018. [DOI] [PubMed] [Google Scholar]

- 26. Balfour DJK, Benowitz NL, Colby SM, Hatsukami DK, Lando HA, Leischow SJ, et al. Balancing consideration of the risks and benefits of E‐ cigarettes. Am J Public Health. 2021;e1–e12. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 27. Dave D, Dench D, Kenkel D, Mathios A, Wang H. News that takes your breath away: Risk perceptions during an outbreak of vaping‐related lung injuries. J Risk Uncertain. 2020;60:281–307. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 28. Centers for Disease Control and Prevention . CDC.gov. 27 11 2020. [Online]. Available: https://www.cdc.gov/tobacco/basic_information/e-cigarettes/severe-lung-disease.html. [Accessed 9 August 2021].

- 29. Allcott H, Rafkin C. Optimal regulation of E‐cigarettes: Theory and evidence. Am Econ J Econ Policy. 2022. [Google Scholar]

- 30. Wilson N, Summers JA, Ouakrim DA, Hoek J, Edwards R, Blakely T. Improving on estimates of the potential relative harm to health from using modern ENDS (vaping) compared to tobacco smoking. medRxiv. 2020. 10.1101/2020.12.22.20248737 [DOI] [PMC free article] [PubMed]

- 31. Goniewicz ML, Miller CR, Sutanto E, Li D. How effective are electronic cigarettes for reducing respiratory and cardiovascular risk in smokers? A systematic review. Harm Reduct J. 2020;17(91):1–9. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 32. George J, Hussain M, Vadiveloo T, Ireland S, Hopkinson P, Struthers AD, et al. Cardiovascular effects of switching from tobacco cigarettes to electronic cigarettes. J am Coll Cardiol. 2019;74(25):3112–20. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 33. Goniewicz ML, Gawron M, Smith DM, Peng M, Jacob P, Benowitz NL. Exposure to nicotine and selected toxicants in cigarette smokers who switched to electronic cigarettes: A longitudinal within‐subjects observational study. Nicotine Tob Res. 2017;19(2):160–7. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 34. Hansen B, Sabia JJ, Rees DI. Have cigarette taxes lost their bite? New estimates of the relationship between cigarette taxes and youth smoking. Am J Health Econ. 2017;3(1):60–75. [Google Scholar]

- 35. Jha P, Ramasundarahettige C, Landsman V, et al. 21st‐century hazards of smoking and benefits of cessation in the United States. N Engl J Med. 2013;368(4):341–50. [DOI] [PubMed] [Google Scholar]

- 36. Krishnasamy VP, Hallowell BD, Ko JY, Board A, Hartnett KP, Salvatore PP, et al. Update: Characteristics of a Nationwide outbreak of E‐cigarette, or vaping, product use–associated lung injury — United States, august 2019–January 2020. MMWR Morb Mortal Wkly Rep. 2020;69:90–4. [DOI] [PMC free article] [PubMed] [Google Scholar]

Associated Data

This section collects any data citations, data availability statements, or supplementary materials included in this article.

Supplementary Materials

Table S1 Taxes and young adult cigarette and ENDS use, coefficient/[95% CI]/(P‐value)

Table S2 Taxes and young adult cigarette and ENDS use, odds ratio/[95% CI]/(P‐value)

Table S3 Pre‐trends tests, coefficient/[95% CI]/(P‐value)

Table S4 Multinomial logistic regression: tax associations with exclusive vaping, exclusive smoking, and dual use among 18–25 year‐olds, relative risk ratio/[95% CI]/(P‐value)

Table S5 ENDS tax changes through May 2019