Abstract

The full or partial purchase of land has become a cornerstone of efforts to conserve biodiversity in countries with strong private property rights. Methods used to target areas for acquisition typically ignore land market dynamics. We show how conservation purchases affect land prices and generate feedbacks that can undermine conservation goals, either by displacing development toward biologically valuable areas or by accelerating its pace. The impact of these market feedbacks on the effectiveness of conservation depends on the ecological value of land outside nature reserves. Traditional, noneconomic approaches to site prioritization should perform adequately in places where land outside reserves supports little biodiversity. However, these approaches will perform poorly in locations where the countryside surrounding reserves is important for species’ persistence. Conservation investments can sometimes even be counterproductive, condemning more species than they save. Conservation is most likely to be compromised in the absence of accurate information on species distributions, which provides a strong argument for improving inventories of biodiversity. Accounting for land market dynamics in conservation planning is crucial for making smart investment decisions.

Keywords: conservation planning, reserve design, site selection, development pressure, habitat destruction

Protecting land where species and ecosystems are most vulnerable is critical to slowing dramatic losses of biodiversity, and the acquisition of full or partial interests in land is the predominant focus of terrestrial conservation efforts (1, 2). Conservation programs increasingly depend on voluntary land acquisitions and financial incentive schemes (3–5). An example is provided by the burgeoning land trust movement in the United States (ref. 5; www.lta.org), which provides an important complement to the public land system. By 2003, 1,537 diverse nongovernmental organizations had protected 9.4 million acres through voluntary land conservation efforts. These figures do not include The Nature Conservancy, the world’s largest land trust. During the past 50 years, The Nature Conservancy alone has protected >16 million acres of private land across the United States at an upfront cost of approximately $6 billion (P.K., unpublished data).

Whereas past land acquisition strategies were somewhat opportunistic (6), conservation groups increasingly rely on a suite of tools from decision theory to help identify priority areas for investment. The tools score regions or sets of parcels for their biological value (6, 7), conservation cost (8, 9), and threat level (10–12). The available approaches assume these scores can be treated as constant. For example, analyses that account for variation in the costs of conservation assume land prices are fixed and exogenous (e.g., refs. 8 and 13). Similarly, analyses that account for relative threats to biodiversity have represented threats with constant, independent probabilities of habitat conversion (e.g., ref. 11 and 12).

The supply of and demand for land in local land markets will be affected, however, when large areas are purchased or slated for conservation. Local land market dynamics, in turn, will determine the amount of conservation achieved and cost of any future conservation efforts. We address three crucial questions for conservation planning. First, how does the local supply of and demand for land influence the amount of conservation achieved through land purchases? Second, can market feedbacks ever make conservation purchases backfire, resulting in more biodiversity being lost than saved? And third, how should local land market considerations influence conservation priorities over larger spatial scales?

Our results depend, in part, on the contribution nonreserve land can make to biodiversity conservation, land that may be devoted to low-impact land uses like biodiversity-friendly agriculture or forestry. Typically, the contribution of such areas has been ignored in conservation priority-setting. However, a growing body of evidence indicates that many species of conservation concern persist outside reserves (14, 15).

Land Market Dynamics

We use a simple model of supply and demand to show how land market dynamics determine the effectiveness of conservation investments. Additional details are provided in supporting information, which is published on the PNAS web site. For more elaborate land market models, see refs. 16 and 17.

We divide land into three classes: “reserves” that are owned and managed by conservation groups for biodiversity conservation, privately owned “open lands” that contain important habitat features, and fully “developed” areas that have lost their ecological value. We assume parcels that are initially candidates for conservation investment could end up in any of these states. We assume the ecological value of open land is some fraction, α, of the value of reserves. Open land holds no ecological interest when α = 0 and is as valuable as reserves when α = 1.

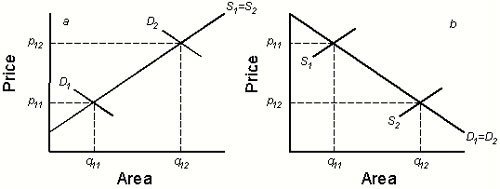

The supply curve in Fig. 1 indicates the quantity of land available for development at a given price, which will reflect the income generated from low-impact uses of open land. The demand curve shows the maximum willingness of developers to pay for each acre. We assume a perfectly competitive land market, one free from distortions due to zoning or other restrictions. The market equilibrates at point (q1, p1), where the supply and demand curves intersect. In equilibrium, q1 acres of land will be developed, each fetching fixed price p1. Parcels to the right of q1 are worth more to private landowners in their undeveloped state than the available market price and remain as open land.

Fig. 1.

Conservation investment in a competitive land market. Horizontal axis shows area of land of conservation interest initially available. D gives area of this land demanded for development at each price, and S is supply of land. Without conservation investment, the competitive equilibrium is (q1, p1); area q1 would be developed, and land to the right of q1 would remain as open land. With conservation buying, we obtain a new aggregate demand curve D̃ and equilibrium (q2, p2). This time, area q2 comprises land bought for development, qd, and conservation, qc, and land to the right of q2 would remain as open land. The area of the shaded rectangle is the conservation budget B = p2qc.

We compare this baseline scenario with the situation when a conservation group with budget B competes in the market. We can construct an aggregate demand curve (Fig. 1) that includes the conservation group and developers and find new market equilibrium (q2, p2). Area q2 can be partitioned into the area purchased by the conservation group, qc = B/p2, and developers, qd (Fig. 1). Parcels to the right of q2 remain as open land.

The improvement in conservation, ΔC, is the increase in the ecological value of the landscape that results from conservation purchases over the baseline of no investment. Let the original land area equal A. The conservation improvement is

|

When open land has no biodiversity value (α = 0), as is typically assumed in analyses of conservation priority-setting, the improvement just equals the area set aside as reserves, qc. At the opposite extreme, when open land and reserves are equally valuable for biodiversity (α = 1), the improvement is simply the change in the amount of land facing development, q1 − qd. These extremes bound the spectrum of possible outcomes traced out as α varies (Fig. 2).

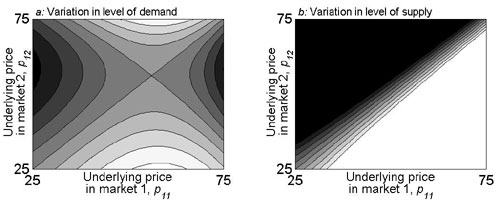

Fig. 2.

Conservation improvement from buying reserves. Conservation improvement that results from buying reserves as a function of the steepness of demand (a) and supply (b), when the ecological value of open land is some fraction of the ecological value of reserves (fraction α = [0, 1/3, 2/3, 1] for dotted, dot-dash, dashed, and solid curves, respectively). Supply and demand curves are assumed to be linear with slopes and intercepts (ms, ps) and (md, pd). Slopes md and ms were varied, but original equilibrium (q1, p1) was held fixed by compensating through pd and ps. Parameters [q1, p1, B] = [50, 50, 500]; a, ms = 1; b, md = −1.

The increase in the overall demand for land with conservation buying results in a higher equilibrium price (Fig. 1). This increase in price reduces the demand for land from developers. However, the higher price also entices some landowners at the margin to put up their land for sale (q2 − q1 in Fig. 1). Therefore, the amount of conservation achieved by buying reserves is less than the total acreage purchased, provided open land has some ecological value, α > 0 (Fig. 2; ΔC = qc − α(q2 − q1) < qc). Although increasing α increases the overall conservation value of a landscape, it diminishes the improvement offered by conservation investments (Fig. 2) because of the growing impact on biodiversity of these additional land sales.

The amount of conservation achieved depends on the total area purchased for reserves and the fraction of this area that comes at the expense of development versus open land. These contributions are determined by the slopes of supply and demand. Development demand curves are steep (inelastic) where there are few substitutes available to developers for land of conservation interest, so the quantity they demand is unresponsive to changes in the price. Supply curves are steep (inelastic) when revenues from alternative low-impact land uses are heterogeneous. In extremis, when land is exhausted, supply can no longer respond to changes in price, and the supply curve eventually becomes vertical.

More land can be bought for reserves when the supply and demand curves are flat (elastic) and the price rise resulting from conservation investment is minimized. When open land has no biodiversity value (α = 0), these conditions are the most favorable for conservation (Fig. 2).

The fraction of reserve land that comes at the expense of development is greater when the development demand curve is flat and there are readily available substitutes for land of conservation interest that can be used in the development process. Consequently, conservation investments would be most effective in markets where developers can build up instead of out or where previously developed properties can be redeveloped. At the opposite extreme, reserve purchases come entirely at the expense of open land when the development demand curve is vertical, making conservation less effective if α > 0. For an example of how to estimate the responsiveness of demand for land and the variation found in estimates from different markets, see ref. 18.

When the supply curve is flat, reserve creation comes at the expense of open land. But as the steepness of supply increases, buying reserves serves to suppress development demand once more. In the limit when the supply curve becomes vertical, all reserve purchases come at the expense of development. This limiting case is exemplified by small areas of coastal sage scrub habitat that remain in land markets in Southern California characterized by intense development demand and tight land supply (19).

Ecological Heterogeneity Within Land Markets

We now examine how individual properties within a land market should be prioritized for investment when considering the ecological heterogeneity of the landscape. We assume that a unique list of species of conservation concern is found on each parcel. Simulated species distributions account for observed frequencies of widespread and rare species (supporting information). A fraction, α, of species are assumed able to persist on open lands, but the remainder depend on reserves for their persistence. No species of conservation concern are assumed able to persist in developed parcels. The interaction of land market dynamics with the conservation investment strategy determines how many acres end up in different land uses, which specific acres those are, and what this land use pattern implies for biodiversity.

In the absence of conservation investments, all properties to the right of q1 in Fig. 1 will remain as open land. A subset of those species able to persist on open land inhabits this set of parcels, giving a baseline species richness that would persist without conservation investments. We compare this baseline with the number of species that would persist when a conservation group competes in the land market.

Conservation groups care about which specific properties they acquire because of their ecological uniqueness, but we assume that developers are indifferent with respect to biodiversity. The initial site selection decision can take on a site swapping characteristic. The conservation group has to compare the ecological contribution of sites just to the right of q1, which may receive displaced development pressure, and the contribution of sites to the left of q1. The steepness of supply and demand determine the ratio at which any site swapping occurs.

Because a fraction of species, 1 − α, is threatened by land uses on open lands, the conservation group may choose to invest in properties not facing development pressure (those to the right of q2). To do so, they have to match the current landowner’s valuation.

We compare three strategies for prioritizing parcels for conservation investment. First, we evaluate an ecologically and economically informed investment strategy in which we assume conservation investors have an accurate inventory of species’ distributions and take into account land market feedbacks (filled diamonds in Fig. 3). With this strategy, we approximate the optimal reserve set by using a myopic heuristic. Specifically, we assume the conservation group sequentially adds sites to the reserved set, so that the next site added offers the greatest benefit-to-cost ratio. We measure the benefit of acquiring a site as the net increase in the number of species that would persist when accounting for the set of species already protected and the impact of any displaced development pressure on biodiversity in the broader landscape. We measure the costs of selecting each site as the increase in the overall cost of the conservation strategy resulting from that choice. Next, we assume conservation investors focus on covering as many species as possible with the set of parcels they acquire, while ignoring the ecological value of the surrounding landscape (gray stars in Fig. 3), which is the typical assumption in analyses of conservation priority setting. This time, we measure the benefits of picking each site as the increase in the number of species found within the reserve set. Finally, we assume conservation investors lack good information on species’ distributions, which is the case in many parts of the world, and acquire parcels effectively at random (open circles in Fig. 3).

Fig. 3.

Change in species richness with reserve buying. Change in species richness with conservation investment is shown for three investment strategies as a function of the conservation budget B for varying slopes of supply and demand. Solid diamonds show ecological-economic strategy in which investors have accurate information on species’ distributions and account for impacts on biodiversity on surrounding open lands. Gray stars show the change when investors have accurate information on species’ distributions and acquire sites to maximize coverage of species within the set of purchased reserves. Open circles show the change when conservation investors lack information on species’ distributions and acquire sites effectively at random. Performance is scored against the baseline species richness that would persist with no investment. Numbers indicate the percentage of simulations in which each investment strategy resulted in a net loss of species. Species lists for each site were randomly generated while accounting for relative frequency of common and rare species. In this figure, α = 1; equivalent figures for alternative α values are given in supporting information. Discretized supply and demand curves are assumed linear with slopes and intercepts (ms, ps) and (md, pd). (a and c). Shallow/elastic demand (|md | = 1/3). (b and d) Steep/inelastic demand (|md | = 3). (a and b) Shallow/elastic supply (ms = 1/3). (c and d) Steep/inelastic supply (ms = 3). Original equilibrium [q1, p1] = [50, 50]. Bars show [5, 95] percentiles for n = 200.

In Fig. 3, we show the change in species richness achieved by conservation investment with each of these strategies for different slopes of supply and demand. In the text, we show the results for the case where α = 1 and open land and reserves are equally valuable for biodiversity. This choice emphasizes the contrasts between our approach and conventional analyses that ignore the fate of biodiversity on open lands. Equivalent figures for smaller α values are given in the supporting information.

In line with our earlier predictions, conservation investments are most effective when the demand for land is responsive to changes in price and the supply of land is unresponsive to them (Fig. 3 Lower Left).

The ecological-economic strategy, which accounts for market feedbacks and biodiversity in the wider countryside, outperforms either the maximal coverage strategy or the random buying strategy. The maximal coverage strategy would use reserves to protect species that can be adequately protected on open land. In contrast, the ecological-economic strategy targets reserves toward the species that need them most.

When ignoring the biodiversity value of open land, conservation investments can actually do more harm than good if they displace development pressure onto particularly valuable sites for rare species that would otherwise have gone unthreatened. When α = 1, a net loss of species results occasionally with the maximal coverage strategy and is more common with the data-poor, random acquisition strategy (for the stars and open circles in Fig. 3, the change in species richness is sometimes negative).

The improvement offered by the ecological-economic strategy or the maximal coverage strategy over the case of random buying provides an estimate of the value of accurate information on species’ distributions. The importance of such information is made especially apparent by the biodiversity per dollar ratios in Fig. 3. When α = 1, the mean biodiversity yield for a given conservation budget is typically doubled or tripled when acquiring land according to the ecological-economic strategy with good information on species’ distributions.

For smaller α values, conservation investments typically result in a net gain in species protection for all investment strategies, because a large part of the assemblage is assumed only to persist in reserves (supporting information). When α is set to zero and all land outside of reserves is assumed uniformly hostile to biodiversity, the ecological-economic strategy and maximal coverage strategy converge, and the importance of the slopes of supply and demand in influencing the effectiveness of investment is diminished (supporting information). However, for intermediate α values, the distinction between the two strategies remains important (supporting information).

Allocating Investments Across Land Markets

Larger-scale conservation planning often involves allocating a fixed budget across distinct areas. Local market dynamics will still partly determine the optimal investment strategy. We focus on the case where α = 1. All else being equal, the optimal allocation of conservation funds across spatially distinct land markets concentrates investments in places with flat demand or steep supply (supporting information). However, variations in the level of supply and demand are also important, because these determine underlying land prices. When higher prices reflect greater development demand, conservation groups must trade off the benefits of protecting less land in high-cost, high-threat locations versus protecting more land in low-cost, low-threat areas. On the other hand, conservation funds stretch further where they are most needed (in low-cost, high-threat locations) when variations in price are due to variations in the levels of supply (supporting information). When making such allocation decisions, conservation groups must also consider whether the biodiversity value of different areas is correlated with the supply of and demand for land for development (20).

Unless land markets are far apart, there will be some overlap in their species’ assemblages. Increasing community similarity across markets favors buying reserves in the most biodiverse locations (solid curves in Fig. 4).

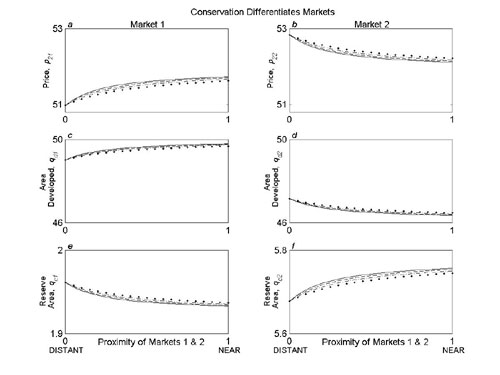

Fig. 4.

Conservation investments differentiate land markets and create additional development opportunities. Optimal allocation of investment across two land markets with increasing proximity (Γ/min(Ti) = γ/4) is shown when the level of conservation investment determines the substitutability of land in each market (a and b), and conservation investments also create additional opportunities for developers (b). Vertical axis shows the fraction of the overall conservation budget that should be allocated to land market 2, which is richer in biodiversity. Horizontal axis shows the proximity of the two land markets (0 is isolated, 1 is near), which determines the potential for development pressure to be displaced across them and the nestedness of the ecological communities they contain. The four curves determine how strongly conservation investments differentiate the land markets (ε = [0, 0.04, 0.08, 0.12] for solid, dashed, dot-dash, and dotted curves, respectively) (a and b) and the extent to which conservation investments attract new development demand (ν = 4ε) (b). The baseline levels of supply and demand were given by Ms = I and Md = −I, where I is the identity matrix when the land markets were isolated (Γ = γ = 0). Other parameters were [q1i, p1i, B, ci, Ai, z1, z2] = [50, 50, 400, 10, 100, 0.3, 0.31].

The economic analogy to overlaps in species’ assemblages is the degree to which land is substitutable for development across markets. As this cross-market substitutability increases, land prices will converge, because developers will not pay a higher price in one location if land elsewhere serves their needs just as well (supporting information). The degree of this substitutability can determine the relative effectiveness of conservation investment strategies. For example, if there are alternative development markets nearby, a narrowly concentrated reserve buying strategy could displace development across markets, as reserve purchases bid up the local price of land. All else being equal, this displacement will act to mitigate feedbacks within markets that are rich in biodiversity, and a narrowly concentrated reserve buying strategy can be optimal (solid curves in Fig. 4). On the other hand, if alternative development markets are more distant so that land is not substitutable across them, then investment strategies that concentrate conservation funds in single localities will be less effective, because conservation groups have to work against rising prices that result from the local build-up of demand to which they themselves contribute.

What happens if consumer preferences for land and, hence, development demand, respond to the configuration of the landscape (21)? In this case, the feedbacks from buying reserves are more complicated than those emphasized thus far. For example, the proximity of parcels to reserves often increases their development potential (16, 17, 22). We examine first the case where aggregated conservation investments differentiate markets, so that land in areas with few nature reserves provides a poor substitute for developers for land in areas with many. Second, we consider the possibility that conservation investments attract additional development pressure to an area.

Fig. 4a illustrates the optimal conservation strategy when establishing reserves differentiates markets for developers. The figure shows the optimal allocation of conservation funds across two land markets when market 2 is more ecologically diverse (supporting information). As proximity increases, the ecological communities become increasingly nested, which favors buying reserves only in market 2. If land in each market is substitutable for development, investing all your funds in market 2 can be optimal because this substitutability mitigates the effects of rising prices there. However, the more strongly conservation investments differentiate the markets for developers, the less the price buildup in market 2 can be dispersed, and a more evenly distributed investment strategy is favored (dashed, dot-dash, and dotted curves in Fig. 4a). Overall, conservation effectiveness decreases as the differentiation of markets induced by buying reserves becomes more pronounced.

In Fig. 4b, we assume that conservation investments increase development pressure by creating new opportunities for developers. We continue to assume that variation in investment levels differentiates markets. Conservation investments are less effective in this case. Indeed, in extremis, buying reserves can again do more harm than good if it induces the development of more land than is protected. With little or no spillover of development across markets, the additional development pressure is retained locally. This build-up of development pressure makes putting your entire budget in the most ecologically valuable market less appealing (vertical intercepts in Fig. 4b). However, the additional development pressure is redistributed across the markets with increasing proximity, which changes the balance of benefits and costs of investing in each location. This change can again favor a more focused investment strategy but is moderated by any differentiation of the markets that results from buying reserves (Fig. 4b).

Discussion

Conservation groups typically ignore land market dynamics when prioritizing areas for investment. Applying first principles in economics, we illustrate how endogenous market feedbacks can undermine conservation efforts and how these dynamics should change conservation priorities both locally and over larger spatial scales.

Various market feedbacks combine to determine the effectiveness of conservation investments. First, land prices rise when conservation groups invest significant sums in local land markets, making future investments more difficult. Second, conservation buying can displace development pressure locally, and the net increase in area protected through buying land is typically less than the full area purchased. Development pressure can potentially be displaced onto properties of higher conservation value that would otherwise have gone unthreatened, meaning conservation efforts may sometimes do more harm than good. This outcome is particularly likely in the absence of accurate information on species distributions, which provides a strong argument for improving inventories of biodiversity. Finally, reserve buying can change the overall attractiveness of an area to developers seeking to capitalize on conservation amenities.

The importance of these market feedbacks in determining conservation performance depends on what fraction of the biota can persist on open land outside reserves. If only species found inside the boundaries of recognized nature reserves “count” as having been “conserved,” then land market feedbacks will play only a relatively minor role in determining the effectiveness of conservation investments. This position is becoming increasingly hard to justify, however, in light of growing evidence that many areas not in conservation ownership contain key components of biodiversity (14, 23, 24) and that many species appear able to persist alongside biodiversity-friendly production (15, 25–27). When acknowledging the ecological value of nonreserve land, the effectiveness of conservation investments is improved by accounting for land market dynamics. In this situation, conservation strategies that aim to cover as much biodiversity as possible inside a given set of reserves, as recommended in most conservation priority- setting exercises, are inefficient. More biodiversity will persist if investments are specifically targeted toward those species that can survive only inside nature reserves, while also taking into account the impact any conservation efforts will have on species in the wider countryside.

The effectiveness of conservation investments also depends on the relative scales over which economic and ecological processes operate. Reserve buying is less effective when it primarily serves to displace development pressure within a priority area for conservation. But our models for allocating investments across land markets show how conservation effectiveness can improve when reserve buying displaces development further afield, away from areas rich in biodiversity. A more thorough exploration of the importance of scale mismatches between ecological processes, like community turnover or species’ dispersal, and economic factors, like the substitutability of land for development, would be worthwhile.

Even though our simple models provide important insights into the fundamental processes at work, three potential extensions are worth mentioning. First, it would be worthwhile incorporating population and community dynamics (28, 29). Our results regarding the possibility that conservation investments may sometimes do more harm than good require only that individual parcels have heterogeneous ecological values. We chose to focus on community complementarity, but similar results should be anticipated if focusing on the contribution of different parcels to metapopulation and metacommunity dynamics. Second, we considered a one-off planning decision. Relaxing this assumption to permit dynamic decisionmaking would allow us to explore how the optimal spatiotemporal allocation of investments responds to uncertainty either about future land supply and demand (11, 12) or about species’ distributions in the face of a changing climate (30). Another extension would be to consider the use of partial-purchase mechanisms like conservation easements, which many conservation groups rely on (5). Analyzing easements introduces questions regarding how conservation investors might avoid the adverse selection problem and target their investments most effectively. Other investment strategies might focus on providing incentives for landowners to improve the quality of open land for biodiversity (i.e., increase α) while leaving the fee title unencumbered. If the landowner’s choice of α affects his or her returns to land, then there is another feedback in the market that needs to be considered, because the returns to land affect the land price.

Conservation purchases alter the supply of and demand for land. Taking this principle as a starting point, the laws of supply and demand make clear the value of a comprehensive strategy that targets species on private lands as well as reserves, and that is informed by accurate inventories of species. Continuing to ignore market forces risks making wasteful use of limited conservation resources, and in some circumstances, may even result in conservation investments doing more harm than good.

Supplementary Material

Acknowledgments

We thank the editor, anonymous referees, colleagues in Stanford’s Department of Biological Sciences and Center of Environmental Science and Policy, and the members of the Stanford–The Nature Conservancy Conservation Finance Working Group for useful suggestions and discussions. This work was made possible by The Nature Conservancy through the Smith Senior Fellows program, the Nuffield Foundation, the British Ecological Society, and Resources for the Future.

Conflict of interest statement: No conflicts declared.

This paper was submitted directly (Track II) to the PNAS office.

See Commentary on page 5245.

References

- 1.Ferraro P. J., Kiss A. Science. 2002;298:1718–1719. doi: 10.1126/science.1078104. [DOI] [PubMed] [Google Scholar]

- 2.Environmental Law Institute. Washington, DC: Environ. Law Inst; 2003. Legal Tools and Incentives for Private Lands Conservation in Latin America. [Google Scholar]

- 3.Binning C. Frontiers in Ecology: Building the Links. In: Klomp N., Lunt I., editors. Oxford: Elsevier; 1997. pp. 155–168. [Google Scholar]

- 4.Pence G. Q. K., Botha M. A., Turpie J. K. Biol. Conserv. 2003;112:253–273. [Google Scholar]

- 5.Merenlender A. M., Huntsinger L., Guthey G., Fairfax S. K. Conserv. Biol. 2004;18:65–75. [Google Scholar]

- 6.Margules C. R., Pressey R. L. Nature. 2000;405:243–253. doi: 10.1038/35012251. [DOI] [PubMed] [Google Scholar]

- 7.Dobson A. P., Rodriguez J. P., Roberts W. M., Wilcove D. S. Science. 1997;275:550–553. doi: 10.1126/science.275.5299.550. [DOI] [PubMed] [Google Scholar]

- 8.Ando A., Camm J., Polasky S., Solow A. Science. 1998;279:2126–2128. doi: 10.1126/science.279.5359.2126. [DOI] [PubMed] [Google Scholar]

- 9.Balmford A., Gaston K. J., Blyth S., James A., Kapos V. Proc. Natl. Acad. Sci. USA. 2003;100:1046–1050. doi: 10.1073/pnas.0236945100. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 10.O’Connor C., Marvier M., Kareiva P. Ecol. Lett. 2003;6:706–711. [Google Scholar]

- 11.Costello C., Polasky S. Resour. Energy Econ. 2004;26:157–174. [Google Scholar]

- 12.Meir E., Andelman S., Possingham H. P. Ecol. Lett. 2004;7:615–622. [Google Scholar]

- 13.Polasky S., Camm J. D., Garber-Yonts B. Land Econ. 2001;77:68–78. [Google Scholar]

- 14.Groves C. R., Kutner L. S., Stoms D. S., Murray M. P., Scott J. M., Schafale M., Weakley A. S., Pressey R. L. Precious Heritage: the Status of Biodiversity in the United States. In: Stein B. A., Kutner L. S., Adams J. S., editors. New York: Oxford University; 2000. pp. 275–300. [Google Scholar]

- 15.Daily G. C., Ceballos G., Pacheco J., Suzan G., Sanchez-Azofeifa A. Conserv. Biol. 2003;17:1814–1826. [Google Scholar]

- 16.Irwin E. G., Bockstael N. E. J. Econ. Geogr. 2002;2:31–54. [Google Scholar]

- 17.Smith V. K., Poulos C., Kim H. Resour. Energy Econ. 2002;24:107–129. [Google Scholar]

- 18.Cheshire P., Sheppard S. Oxf. Bull. Econ. Stats. 1998;60:357–382. [Google Scholar]

- 19.Atwood J. L. Interface Between Ecology and Land Development in California. In: Kelley J. E., editor. Los Angeles: S. Calif. Acad. Sci; 1993. pp. 149–169. [Google Scholar]

- 20.Luck G. W., Ricketts T. H., Daily G. C., Imhoff M. Proc. Natl. Acad. Sci., USA. 2004;101:182–186. doi: 10.1073/pnas.2237148100. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 21.Geoghegan J., Wainger L., Bockstael N. E. Ecol. Econ. 1997;23:251–264. [Google Scholar]

- 22.Irwin E. G. Land Econ. 2002;78:465–480. [Google Scholar]

- 23.Scott J. M., Davis F. W., McGhie R. G., Wright R. G., Groves C., Estes J. Ecol. Appl. 2001;11:999–1007. [Google Scholar]

- 24.Shaffer M. L., Scott J. M., Casey F. Bioscience. 2002;52:439–443. [Google Scholar]

- 25.Daily G. C., Ehrlich P. R., Sanchez-Azofeifa A. Ecol. Appl. 2001;11:1–13. [Google Scholar]

- 26.McNeely J. A., Scherr S. J. Ecoagriculture: Strategies to Feed the World and Save Wild Biodiversity. Washington, DC: Island; 2002. [Google Scholar]

- 27.Mayfield M. M., Daily G. C. Ecol. Appl. 2005;15:423–439. [Google Scholar]

- 28.Cabeza M., Moilanen A. Conserv. Biol. 2003;17:1402–1413. [Google Scholar]

- 29.Armsworth P. R., Roughgarden J. E. Am. Nat. 2005;165:449–465. doi: 10.1086/428595. [DOI] [PubMed] [Google Scholar]

- 30.Araujo M. B., Cabeza M., Thuiller W., Hannah L., Williams P. H. Glob. Change Biol. 2004;10:1618–1626. [Google Scholar]

Associated Data

This section collects any data citations, data availability statements, or supplementary materials included in this article.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}